Every australian first home buyer in Hobsonville faces a critical hurdle: early repayment charges can shrink your mortgage flexibility more than expected. Nearly half of Auckland banks impose break fees on fixed-rate loans, potentially costing thousands if you change your repayment plans. Understanding how and why these charges work matters for anyone mapping out long-term financial strategies. This guide gives clear insight into the ways these fees impact real savings and future choices for new property owners.

Table of Contents

- Defining Early Repayment Charges In New Zealand

- Types Of Early Repayment Charges For Mortgages

- How Early Repayment Fees Are Calculated

- Legal Rules And Lender Obligations In Auckland

- Managing Costs And Avoiding Common Pitfalls

Key Takeaways

| Point | Details |

|---|---|

| Understanding Early Repayment Charges | These financial penalties apply when borrowers modify or terminate fixed-rate mortgages prematurely, protecting lenders from potential revenue loss. |

| Importance of Transparency | Lenders are required to clearly disclose early repayment charges and their calculation methods, allowing borrowers to make informed decisions. |

| Types of Early Repayment Charges | Various fees, such as Fixed Rate Break Fees and Partial Repayment Penalties, can be triggered by specific actions during the loan term. |

| Strategic Cost Management | Homeowners should assess market conditions and consult advisers to minimise early repayment charges effectively. |

Defining Early Repayment Charges In New Zealand

Early repayment charges are financial penalties applied by banks when borrowers terminate or modify their fixed-rate mortgage before the agreed contract period ends. These charges, also known as break fees, serve as compensation mechanisms for financial institutions to protect their projected earnings. Early repayment fees represent a critical consideration for Auckland homeowners contemplating changes to their mortgage structure.

The fundamental purpose of these charges is to reimburse banks for potential financial losses when a borrower exits a fixed-rate loan prematurely. Typically, the fee is calculated based on the difference between the original wholesale interest rate at loan origination and the current market rates. This calculation ensures banks can recover the potential lost revenue associated with early loan termination. The specific amount can vary significantly depending on factors like remaining loan term, current interest rates, and the total loan amount.

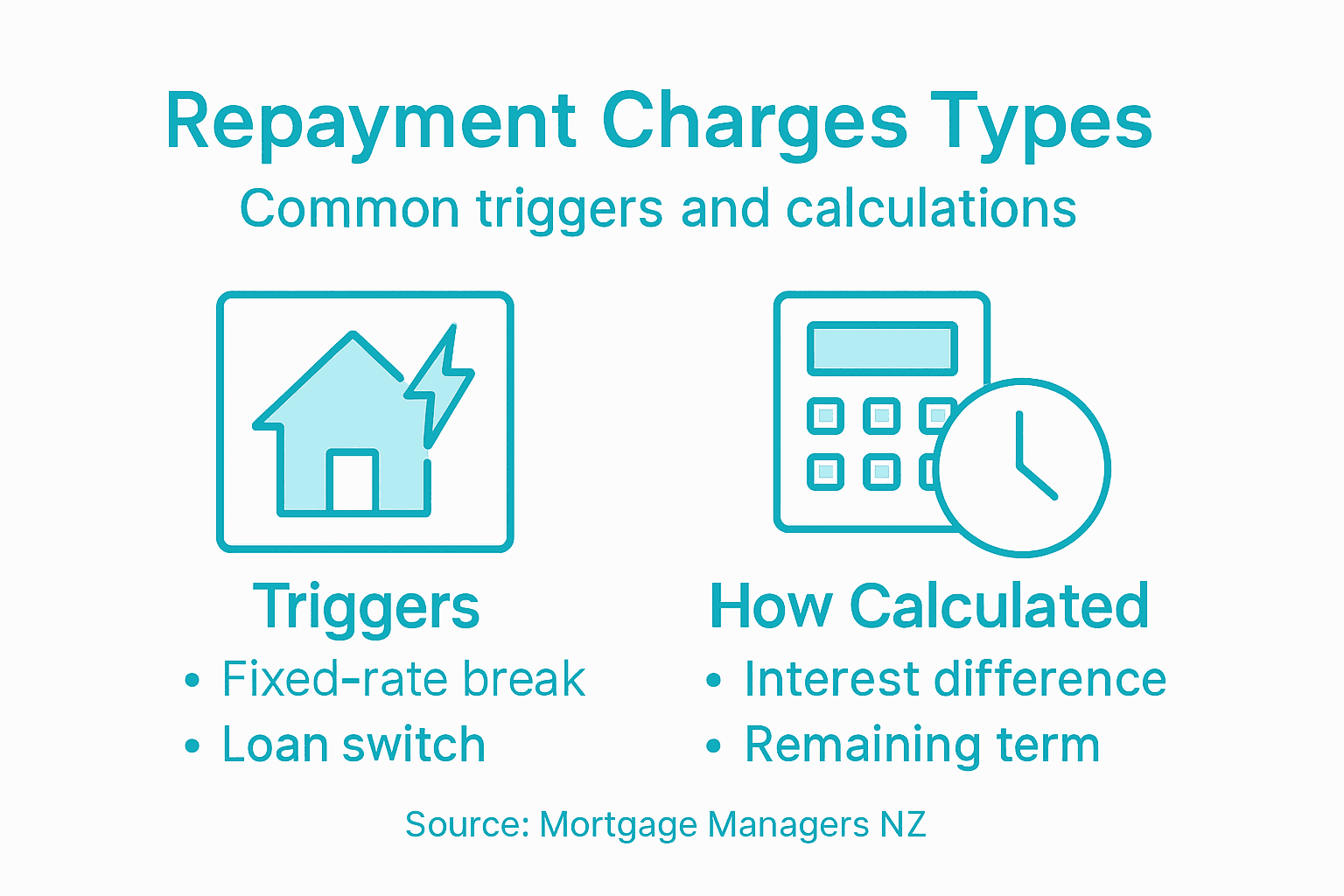

Under New Zealand banking regulations, financial institutions must clearly outline these charges within the loan agreement. Borrowers are legally required to understand and acknowledge these potential fees before signing their mortgage contract. Key triggering events for early repayment charges might include:

- Switching from a fixed to a variable rate before term completion

- Making substantial lump-sum payments beyond permitted thresholds

- Fully repaying the mortgage prior to the fixed-rate period’s conclusion

- Refinancing with a different lending institution

Pro tip: Always request a detailed breakdown of potential early repayment charges from your mortgage adviser before finalising any fixed-rate loan agreement to understand your financial obligations precisely.

Types Of Early Repayment Charges For Mortgages

Early repayment charges in New Zealand mortgage lending manifest in several distinct categories, each designed to protect financial institutions from potential revenue losses. Early repayment charges encompass multiple scenarios that can trigger financial penalties for borrowers seeking to modify their loan arrangements before contractual terms conclude.

The primary types of early repayment charges include Fixed Rate Break Fees, which occur when borrowers exit a fixed-rate mortgage before the agreed term expires. These fees are calculated based on the difference between the original wholesale interest rate and current market rates. Another significant category is Partial Repayment Penalties, where borrowers exceed predetermined annual lump-sum payment thresholds outlined in their loan agreement.

Additional early repayment charge variations include:

- Interest Rate Switching Fees: Charges applied when transitioning between fixed and variable rate structures

- Refinancing Penalties: Financial penalties incurred when replacing the existing mortgage with a new loan from another institution

- Administrative Early Termination Charges: Additional fees covering processing and administrative costs associated with loan restructuring

- Prepayment Limitation Fees: Penalties for repaying more than the contractually permitted percentage of the loan principal

Pro tip: Request a comprehensive written breakdown of potential early repayment charges during your initial mortgage consultation to avoid unexpected financial surprises.

Here’s a quick comparison of the main types of early repayment charges in New Zealand mortgages:

| Charge Type | Triggering Event | Typical Calculation Basis |

|---|---|---|

| Fixed Rate Break Fee | Exiting fixed-rate mortgage early | Rate difference × balance × remaining term |

| Partial Repayment Penalty | Lump-sum exceeds allowed threshold | Amount over limit × set percentage |

| Interest Rate Switching Fee | Changing between fixed/variable rate | Flat fee or percentage of balance |

| Refinancing Penalty | Loan replaced by new lender | Similar to break fee calculation |

| Administrative Termination Fee | Contract restructure or closure | Flat/variable administrative cost |

How Early Repayment Fees Are Calculated

Calculating early repayment fees involves a complex mathematical process that protects financial institutions from potential revenue losses. Early repayment charges are fundamentally determined by comparing the original loan’s wholesale interest rate against current market rates, multiplied by the outstanding loan balance and remaining fixed-term duration.

The primary calculation method incorporates several critical variables that influence the final penalty amount. Wholesale Interest Rate Differential forms the core of most fee calculations, representing the financial gap between the original loan’s interest rate and the prevailing market rate. Banks typically multiply this differential by the loan’s remaining principal and the number of months left in the fixed-rate term to determine the precise early repayment charge.

Key components involved in early repayment fee calculations include:

- Original Wholesale Interest Rate: The rate at loan origination

- Current Market Wholesale Rate: Present-day interest rate benchmark

- Remaining Loan Principal: Total outstanding balance

- Fixed-Term Duration: Months left in the original fixed-rate period

- Administrative Cost Factors: Processing and administrative expenses

Some financial institutions utilise the Credit Contracts and Consumer Finance Act 2003’s ‘safe harbour’ formula, while others develop proprietary calculation methods that must be transparently disclosed to borrowers. The complexity of these calculations means that early repayment fees can vary significantly between different lenders and individual mortgage contracts.

Pro tip: Request a detailed written breakdown of your specific early repayment fee calculation during your mortgage consultation to understand exactly how potential charges would be determined.

The following table summarises key variables impacting the amount of early repayment charges:

| Variable | Impact on Charge Size |

|---|---|

| Remaining Fixed Term | Longer remaining term = higher fee |

| Original Interest Rate | Higher original rate may increase penalty |

| Current Market Rate | Lower market rate raises break fee |

| Outstanding Loan Balance | Larger balance leads to larger charges |

| Administrative Costs | Can add a significant fixed amount |

Legal Rules And Lender Obligations In Auckland

Auckland mortgage lenders operate under stringent legal frameworks designed to protect borrowers and ensure transparent financial practices. Legal lending regulations mandate comprehensive disclosure of early repayment charges, ensuring consumers understand their financial commitments before signing mortgage agreements.

The Credit Contracts and Consumer Finance Act 2003 forms the cornerstone of lender obligations in New Zealand, specifically addressing early repayment charge transparency. This legislation requires financial institutions to clearly articulate calculation methods, fee structures, and potential penalties within loan contracts. Banks cannot arbitrarily impose early repayment charges; these must be explicitly outlined and agreed upon during the initial contract negotiation.

Key legal obligations for Auckland mortgage lenders include:

- Transparent Fee Disclosure: Providing clear, comprehensible explanations of all potential charges

- Statutory Compliance: Adhering to the Credit Contracts and Consumer Finance Act 2003

- Fair Calculation Methods: Using either the statutory ‘safe harbour’ formula or alternative methods that can be objectively justified

- Consumer Protection: Ensuring borrowers understand their rights and potential financial implications

- Contract Clarity: Specifying exact circumstances triggering early repayment charges

Pro tip: Always request a written breakdown of potential early repayment charges and request that your mortgage adviser explains each component in plain language before signing any loan agreement.

Managing Costs And Avoiding Common Pitfalls

Navigating early repayment charges requires strategic financial planning and proactive management. Minimising mortgage break fees involves understanding the complex interplay between loan terms, market conditions, and potential financial penalties.

Homeowners can employ several strategic approaches to mitigate potential early repayment charges. Careful Timing becomes crucial when considering loan restructuring or refinancing. This involves monitoring wholesale interest rates, understanding your remaining fixed-term duration, and calculating whether potential savings outweigh break fee costs. Some borrowers might find that waiting for a more opportune market moment can significantly reduce or eliminate early repayment penalties.

Key strategies for managing and avoiding early repayment charges include:

- Partial Repayment Allowances: Utilise annual lump-sum repayment options within your loan contract

- Mortgage Portability: Investigate options to transfer your existing mortgage to a new property

- Staged Refinancing: Consider gradual loan restructuring to minimise break fee exposure

- Professional Consultation: Seek mortgage adviser guidance before making significant financial changes

- Rate Comparison: Thoroughly analyse potential savings against break fee costs

Pro tip: Request a detailed scenario analysis from your mortgage adviser that demonstrates the precise financial implications of potential early repayment, including a comprehensive breakdown of all associated costs and potential savings.

Avoid Costly Early Repayment Charges on Your Auckland Home Loan

Early repayment charges can create unexpected financial stress when you decide to adjust or pay off your fixed-rate mortgage early. Understanding terms like break fees, partial repayment penalties, and interest rate switching fees is key to managing your mortgage without surprises. Many Auckland homeowners face the challenge of balancing potential savings against these charges and need a clear strategy to avoid costly mistakes.

Take control of your home loan today with expert support from Mortgage Managers. As local Auckland mortgage advisers based in Hobsonville, we specialise in personalised mortgage solutions that minimise early repayment costs and help you navigate complex fee structures. Reach out now to receive a clear breakdown of your options and protect yourself from unnecessary break fees. Visit Mortgage Managers to get started and ensure your next mortgage decision is informed and cost-effective.

Frequently Asked Questions

What are early repayment charges for home loans?

Early repayment charges, also known as break fees, are financial penalties imposed by lenders when borrowers terminate or modify their fixed-rate mortgage before the agreed contract period ends.

How are early repayment charges calculated?

Early repayment charges are typically calculated based on the difference between the original wholesale interest rate at loan origination and current market rates, multiplied by the outstanding loan balance and the remaining fixed-term duration.

What circumstances can trigger early repayment charges?

Early repayment charges can be triggered by several actions, including switching from a fixed to a variable rate, making substantial lump-sum payments beyond permitted thresholds, fully repaying the mortgage before the fixed-rate period ends, or refinancing with a different lender.

How can I manage and potentially avoid early repayment charges?

To manage and avoid early repayment charges, homeowners can consider timing their loan restructuring, take advantage of partial repayment allowances, explore mortgage portability options, and consult with a mortgage adviser to carefully assess the financial implications before making decisions.