TL;DR:

- A second mortgage is an additional loan secured against your home, allowing access to equity without replacing the primary mortgage. It remains subordinate to the first mortgage and typically has higher interest rates due to its junior position. In New Zealand, homeowners use second mortgages for renovations, debt consolidation, or investments, provided they meet eligibility criteria like credit score and equity requirements.

A second mortgage is an additional loan secured against your home that lets you borrow against your existing equity without replacing your primary mortgage. It sits behind your first mortgage in priority, which is why lenders treat it differently and price it accordingly. New Zealand homeowners are increasingly using this structure to fund renovations, consolidate debt, or invest in property, all while keeping their original home loan intact. Understanding how does a 2nd mortgage work is the first step toward deciding whether it fits your financial situation.

How does a 2nd mortgage work?

A second mortgage is a separate loan registered against your property, secured by the equity you have built up over time. Your first mortgage remains untouched. The second mortgage lender sits in a junior lien position, meaning they are repaid only after your primary lender in the event of a default. That junior lien position is the core reason second mortgage interest rates are higher than primary mortgage rates.

The amount you can borrow depends on how much equity you hold. Lenders calculate your combined loan-to-value ratio across both loans. If your home is worth $800,000 and your first mortgage balance is $400,000, you hold $400,000 in equity. However, lenders do not let you access all of it. They require you to retain a meaningful buffer, which brings us to the eligibility requirements covered shortly.

Second mortgages are not a niche product. They are a recognised tool for homeowners who want to access liquidity without disturbing a low-rate primary mortgage. That distinction matters most when interest rates are rising, because accessing liquidity without altering your primary mortgage’s favourable rate can save you thousands over the life of your loan.

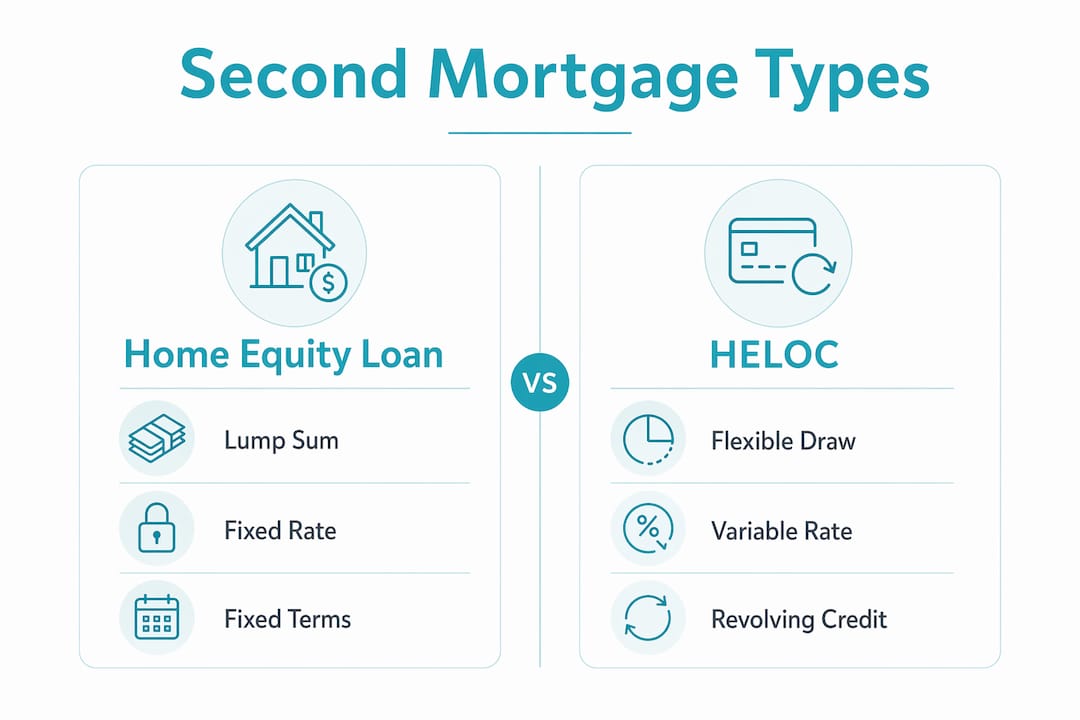

What types of second mortgages are available in New Zealand?

Two primary types of second mortgages exist: home equity loans and home equity lines of credit, commonly called HELOCs.

A home equity loan delivers a lump sum at a fixed interest rate. You repay it in equal monthly instalments over a set term, typically 5–20 years. This suits homeowners who have a defined project, such as a kitchen renovation or a specific debt consolidation amount, and want predictable repayments.

A HELOC works more like a credit card secured against your home. You are approved for a credit limit and draw from it as needed during a set draw period, usually 5–10 years. Interest rates are variable, so your repayments can fluctuate. HELOCs suit homeowners with ongoing or uncertain funding needs, such as a staged building project or investment property costs.

| Feature | Home equity loan | HELOC |

|---|---|---|

| Disbursement | Lump sum | Draw as needed |

| Interest rate | Fixed | Variable |

| Repayment structure | Equal monthly instalments | Interest only during draw period |

| Best suited for | Defined, one-off costs | Ongoing or staged expenses |

| Predictability | High | Lower |

A cash-out refinance is a third option, but it works differently. It replaces your primary mortgage entirely with a new, larger loan. A second mortgage, by contrast, keeps your original loan intact. If your primary mortgage carries a low fixed rate, a cash-out refinance could cost you significantly more over time.

Pro Tip: If your primary mortgage rate is below current market rates, a second mortgage almost always preserves more value than refinancing. Run the numbers on both before committing.

What are the eligibility criteria for a second mortgage in New Zealand?

Lenders assess several financial metrics before approving a second mortgage. Meeting these benchmarks is not optional. They are the gatekeepers to approval.

-

Credit score. Most lenders require a credit score of 620 to 640 as a minimum. A higher score improves your rate and borrowing capacity. A score below 620 will limit your options significantly.

-

Debt-to-income ratio. Lenders expect your total debt repayments to sit below 43% of your gross monthly income. If your combined mortgage repayments, credit card minimums, and other loans exceed that threshold, approval becomes difficult. You can review how your debt-to-income ratio affects your borrowing power before you apply.

-

Equity buffer. You must retain at least 15–20% equity in your home after the second mortgage is drawn. Lenders cap combined borrowing at 80–85% of your property’s value. On an $800,000 home, that means your total debt across both loans cannot exceed $640,000–$680,000.

-

Stable income. Lenders verify your income through payslips, tax returns, and bank statements. Self-employed borrowers face more scrutiny and should prepare at least two years of financial statements.

-

Property valuation. A registered valuation confirms your home’s current market value. This determines how much equity you actually hold, not how much you think you hold.

Homeowners often misunderstand equity limits. Lenders cap total borrowing to preserve a buffer, so you cannot access your full equity even if the numbers look generous on paper. Understanding equity requirements before you apply saves time and avoids disappointment.

Pro Tip: Pull your credit report before applying. Errors on your credit file are common and can cost you approval. Fixing them takes time, so do it early.

How does the second mortgage application and approval process work?

The application process is structured and methodical. Knowing what to expect reduces stress and speeds up approval.

-

Submit your application. Most lenders offer online applications that take 15–30 minutes to complete. You will provide personal details, property information, and a summary of your finances.

-

Provide documentation. Lenders verify your income, assets, and existing debts. Typical documents include recent payslips, two years of tax returns, bank statements, and a list of current liabilities. Self-employed borrowers should prepare extensive documentation, as scrutiny is higher and delays are more common.

-

Property appraisal. Your lender orders a home appraisal to confirm current market value. Appraisals typically cost $400–$600 and are a non-negotiable step. The result directly determines how much you can borrow.

-

Underwriting. The lender’s credit team reviews your full application, verifies all documentation, and assesses risk. This stage takes the most time. The total approval process from application to settlement typically spans 2–4 weeks.

-

Approval and settlement. Once approved, you sign the loan documents and the funds are released. For a home equity loan, this is a single lump sum. For a HELOC, your credit line becomes available to draw from.

A mortgage application checklist helps you prepare every document before you start. Inaccurate information is one of the most common reasons applications stall or fail. Accurate financial information and readiness for underwriting reduces the risk of delays significantly.

What are the benefits and risks of a second mortgage?

Second mortgages carry genuine advantages, but they also carry real risks. A clear-eyed view of both helps you make the right call.

Benefits worth knowing

- Preserved primary mortgage rate. Your original loan stays untouched. If you locked in a low rate, that rate stays in place.

- Predictable repayments. Home equity loans offer fixed monthly payments, making budgeting straightforward.

- Flexible access. HELOCs let you draw only what you need, when you need it, reducing unnecessary interest costs.

- Broad use cases. Common uses include home renovations, debt consolidation, investment property deposits, and education costs.

Risks to weigh carefully

- Higher interest rates. Because the second mortgage lender sits in a junior position, they carry more risk. That risk is priced into the rate you pay.

- Foreclosure exposure. If you cannot meet combined repayments on both loans, your lender can initiate foreclosure proceedings. This is a real consequence, not a theoretical one.

- Reduced equity buffer. Borrowing against your equity reduces your financial cushion. If property values fall, you could find yourself in negative equity territory.

“Second mortgages allow accessing liquidity without disturbing a low-rate primary mortgage, a key benefit in high-interest rate environments.” — Lower.com

Pro Tip: Only borrow what you need. A HELOC approved for $150,000 does not mean you should draw $150,000. Draw in stages and review your position regularly.

How do second mortgages compare to other equity borrowing options?

Choosing the right borrowing structure depends on your existing mortgage rate, credit profile, and how much equity you hold.

Cash-out refinancing replaces your primary mortgage with a new, larger loan. If current rates are higher than your existing rate, refinancing costs you more every month for the life of the loan. A second mortgage avoids that problem entirely. Second mortgages are not always the cheapest option, though. If you have excellent credit and significant equity, a cash-out refinance may offer a lower blended rate.

Personal loans are unsecured, so they carry higher interest rates than either option. They are faster to arrange and do not put your home at risk, but borrowing limits are lower and terms are shorter.

| Option | Impact on primary mortgage | Typical rate | Best suited for |

|---|---|---|---|

| Second mortgage | None | Higher than primary | Preserving low primary rate |

| Cash-out refinance | Replaces primary loan | Current market rate | Large equity access, rate neutral |

| Personal loan | None | Highest | Small amounts, no home equity |

For New Zealand homeowners who locked in low rates in recent years, a second mortgage is often the most cost-effective way to access equity. You can also review how second mortgage lenders compare across different financing scenarios to find the best fit for your situation.

Key takeaways

A second mortgage is a separate loan secured against your home equity that keeps your primary mortgage intact, making it a practical option for New Zealand homeowners who want to access funds without resetting their existing loan terms.

| Point | Details |

|---|---|

| Two main types | Home equity loans offer fixed lump sums; HELOCs provide flexible, variable-rate credit lines. |

| Eligibility benchmarks | You need a credit score of 620+, a debt-to-income ratio below 43%, and at least 15–20% equity retained after borrowing. |

| Application timeline | Expect 2–4 weeks from application to settlement, including a mandatory home appraisal. |

| Key benefit | A second mortgage preserves your primary mortgage rate, which matters most when current rates are higher than your existing rate. |

| Main risk | The junior lien position means higher rates and foreclosure risk if combined repayments become unmanageable. |

Why I think most homeowners approach second mortgages the wrong way

Most people I speak with come to a second mortgage conversation thinking about how much they can borrow. The better question is whether they should borrow at all, and if so, which structure actually serves their goals.

The most common mistake I see is homeowners overestimating their available equity. Lenders cap combined borrowing at 80–85% of property value. That buffer exists for good reason. If property values soften, that buffer is the difference between a manageable position and a stressful one.

The second mistake is ignoring the rate comparison. A second mortgage carries a higher rate than your primary loan. That is the cost of keeping your original rate intact. Whether that trade-off makes sense depends entirely on the gap between your existing rate and current market rates. If that gap is small, refinancing might actually be cheaper overall.

Where second mortgages genuinely shine is for homeowners with a low primary rate who need a defined amount for a specific purpose, such as a renovation or an investment deposit. In that context, the structure is logical and cost-effective. A good mortgage adviser in New Zealand will model both options side by side before recommending one.

My honest advice: prepare your documentation thoroughly before you start. Inaccurate information is the single biggest cause of delays and declined applications. Know your credit score, your debt-to-income ratio, and your actual equity position before you walk into any conversation with a lender.

— Stuart

How Mortgagemanagers can help with your second mortgage

Mortgagemanagers is a locally owned Auckland mortgage advisory business, and we work with homeowners across New Zealand who are considering a second mortgage to access their equity. We act as your personal mortgage shoppers, comparing lenders and structures to find the option that fits your specific situation, not a generic product off a shelf.

Whether you are planning a renovation, consolidating debt, or funding an investment, we take the time to understand your goals and match you with the right lender. We have direct access to a wide panel of lenders and know their criteria inside out. Getting the right advice before you apply can save you time, money, and unnecessary credit inquiries. Reach out to the team at Mortgagemanagers for a no-obligation conversation about your second mortgage options.

FAQ

What is a second mortgage?

A second mortgage is an additional loan secured against your home that sits behind your primary mortgage in repayment priority. It lets you borrow against your equity without replacing your existing home loan.

How much can I borrow with a second mortgage?

Most lenders cap combined borrowing at 80–85% of your property’s value, and you must retain at least 15–20% equity after the loan is drawn. The exact amount depends on your home’s current valuation and your existing mortgage balance.

What credit score do I need for a second mortgage?

Lenders typically require a minimum credit score of 620 to 640. A higher score improves your rate and increases your borrowing options.

How long does a second mortgage application take?

The online application takes 15–30 minutes, but the full process including appraisal and underwriting typically takes 2–4 weeks from start to settlement.

Is a second mortgage better than refinancing?

A second mortgage is the better choice when your primary mortgage carries a lower rate than current market rates. Refinancing replaces your primary loan entirely, which can cost more if rates have risen since you first borrowed.