Why do over 70% of Kiwis use brokers now, and we address the bank vs broker here too.

Choosing between using a bank or mortgage broker is one of the biggest decisions first home buyers face. This choice directly impacts your choices, your approval chances, the home loan rates, and of course the level of support you receive throughout the buying process.

Banks might say they can offer these things, but they can’t. For starters they just do not have the choices for you and so you never know if you are going to be offered the best home loan even if the home loan rates look okay and the level of support seems okay.

It’s reported that over 70% of New Zealand first-home buyers now use mortgage advisers due to better loan choices and options. We all know that advisers will make sure that you get competitive rates, and personalised service is where advisers really excel.

In this article we explain your options specifically for first home buyers looking to make an informed decisions.

Our Discussion Points:

- Understanding Banks: What Do They Offer First Home Buyers?

- Understanding Mortgage Brokers: How They Help More Than Just Access

- Comparing Banks and Brokers: Pros, Cons, and When Each Makes Sense

- Common Misconceptions About Banks and Brokers

- Making Your Decision: Practical Steps for Auckland First Home Buyers

- Conclusion: Empowered Choices for Your Home Loan Journey

- Talk To Auckland Mortgage Brokers That Can Help

Bank vs Broker – The Key Points

| Point | Details |

|---|---|

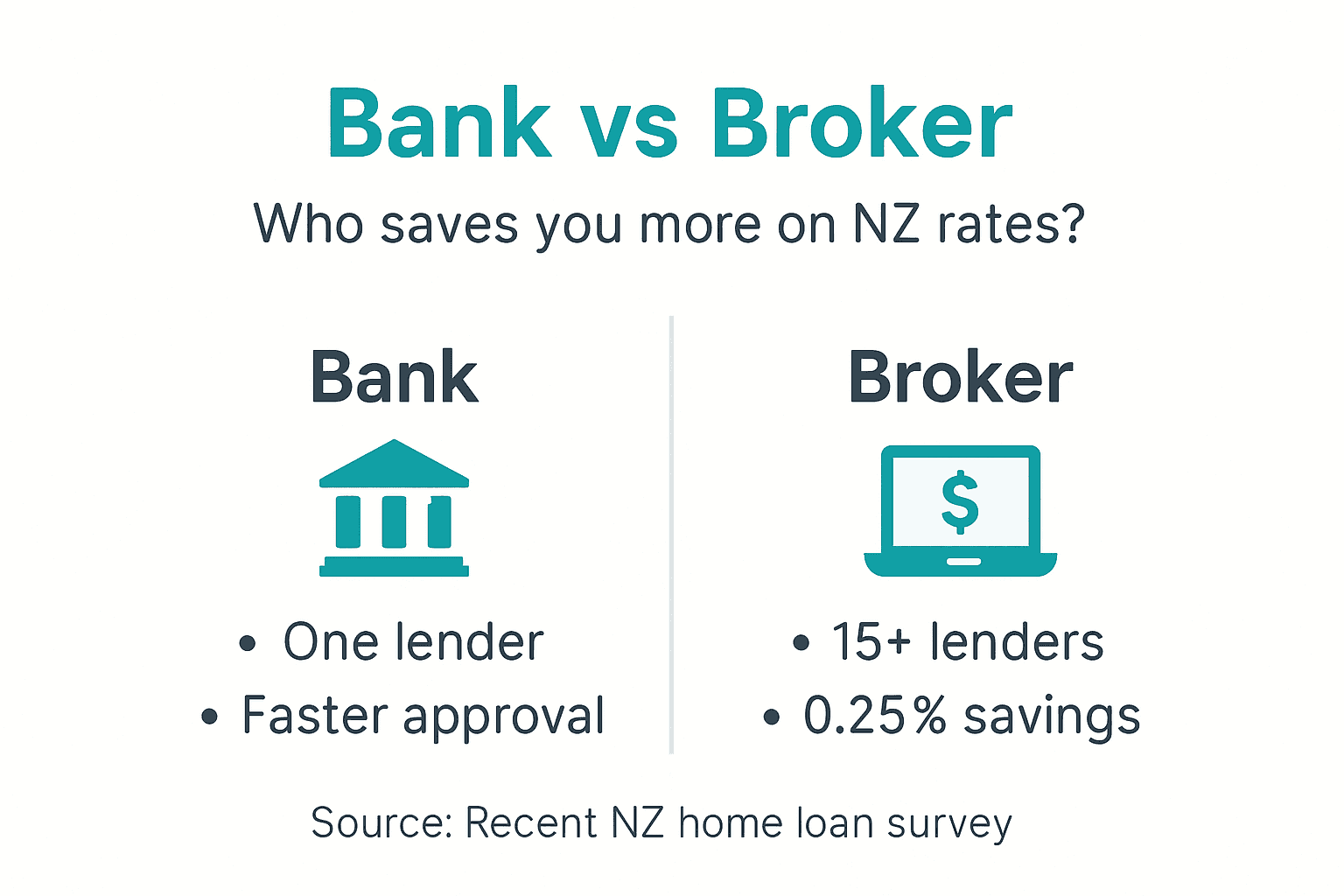

| Lender Access | Mortgage brokers access 15-25+ lenders while banks offer only their own products. |

| Buyer Preference | Over 70% of NZ first home buyers choose mortgage brokers for better rates and personalised service. |

| Rate Savings | Brokers often negotiate lower rates than banks will offer, saving thousands over the loan term. |

| Fast Approval Option | Banks can offer faster approval if you are an existing customer with established relationship. |

| Free Service | Banks are generally free but also mortgage broker services are generally free to borrowers as lenders pay their commission. |

Understanding Banks: What Do They Offer First Home Buyers?

Banks remain a familiar starting point for many Auckland first home buyers. They provide mortgage products, but only from their own lending portfolio. This limits your choice to whatever that specific bank offers at the time.

Going direct to a bank may speed up straightforward loan approvals due to existing customer relationships and access to financial history within the bank. If you already hold accounts, credit cards, or KiwiSaver with a particular bank, they can review your transaction history quickly. This internal data access sometimes translates to faster initial approval for simple lending scenarios.

However, banks tend to have stricter lending criteria, especially for first home buyers. They follow rigid policies that may not accommodate unique situations. Self-employed buyers or those with non-traditional income often face challenges getting approved through banks alone.

Key characteristics of working with banks include:

- Only their own loan products available, restricting your options

- Faster approval possible if you’re an existing customer with good banking history

- Stricter lending criteria that may exclude complex borrower profiles

- Loyalty perks like fee waivers or interest rate discounts for long-term customers

- Limited negotiation flexibility on rates and loan terms

Banks can work well if your financial situation is straightforward. You have stable employment, a solid deposit, and no complications in your credit history.

The mortgage broker guide shows how brokers offer different advantages for those needing more flexibility.

For Auckland buyers with simple profiles, the relationship banking approach offers convenience. You handle everything in one place. But this convenience comes at the cost of limited choice and potentially higher interest rates compared to what brokers can negotiate across multiple lenders.

Mortgage Brokers: How They Help & Offer Better Choices

Mortgage brokers operate differently from the banks and bank employees.

They act as intermediaries between you and multiple lenders. Mortgage advisers in New Zealand typically provide access to 15-25+ lenders, whereas going directly to a bank limits access to that single bank’s mortgage products.

This broad lender access means more loan options tailored to your specific situation. Brokers compare products across major banks, second-tier lenders, and non-bank lenders. They identify which lenders are most likely to approve your application based on your financial profile.

The commission model works in your favour. Most brokers in New Zealand are paid by the lender, not by you which means you receive professional mortgage advice and application support without paying upfront fees. They can offer this as the lender pays the broker a commission once your loan settles. While they are paid by the lenders, the commission is reversed if the lending is paid off within 2-years and therefore mortgage brokers will often have a deferred establishment fee should they need to repay the commission.

Brokers will also try to negotiate better interest rates and loan terms on your behalf. They understand each lender’s appetite for different borrower types. This knowledge lets them position your application strategically. Mortgage brokers can save you (borrowers) 20-30+ hours of research, paperwork, and coordination, especially with a complex home loan application processes.

Key advantages of using mortgage brokers:

- Access to 15-25+ lenders instead of just one bank’s products

- Services typically free to borrowers as lenders pay commission

- Expert negotiation resulting in competitive rates and terms

- Guidance through complex criteria for self-employed or small deposit buyers

- Significant time savings on research, paperwork, and lender coordination

Brokers shine when your situation has complexity.

Perhaps you’re self-employed with variable income or maybe you’re stretching your deposit using KiwiSaver. Brokers understand which lenders accommodate these scenarios and how to present your application for best results.

The broker loan options available through advisers often include products not advertised publicly. Some lenders only work through broker channels, giving you access to exclusive deals you won’t find going direct.

Comparing Banks and Brokers: Pros, Cons, and When Each Makes Sense

Now that you understand how each option works, let’s compare them directly. This side-by-side view helps you decide which route suits your Auckland home buying journey.

| Feature | Banks | Mortgage Brokers |

|---|---|---|

| Lender Access | Single bank only | 15-25+ lenders |

| Rate Negotiation | Limited flexibility | Strong negotiation power |

| Service Cost | Free (direct) | Free (lender-paid commission) |

| Approval Speed | Faster for existing customers | Varies by lender choice |

| Complex Cases | Stricter criteria | Expert guidance for complexity |

| Time Investment | You research everything | Broker handles coordination |

Mortgage brokers can often negotiate home loan interest rates 0.10-0.25% lower than banks’ standard rates, potentially saving thousands over a loan term. On a $600,000 mortgage, a 0.20% rate reduction saves approximately $12,000 over a 30-year term.

Banks make sense when:

- Your financial profile is straightforward with stable income and good credit

- You’re an existing customer with strong banking relationship and history

- You value handling everything through one familiar institution

- Your timeline allows for researching and comparing multiple banks yourself

Brokers make sense when:

- You want access to the widest range of loan products and lenders

- Your situation has complexity such as self-employment or small deposit

- You value expert guidance and time savings through the application process

- You want someone negotiating the best possible rate on your behalf

Pro Tip: Even if you think your situation is simple, getting a broker’s assessment costs nothing and might reveal better options than your bank offered.

Mortgage brokers may have potential conflicts of interest due to commission-based payment, but are regulated by the New Zealand Financial Markets Authority to act ethically and in clients’ best interests. This regulation requires brokers to disclose their commission structure and recommend products suitable for your needs, not just the highest-paying option.

The why use a broker decision often comes down to weighing choice and expertise against the convenience of your existing banking relationship. For most first home buyers, the broader access and rate savings tip the scales toward brokers.

However, if you have a unique relationship with your bank or an exceptionally simple profile, the direct route remains a viable option. In most cases there is still going to be no disadvantage to work with a mortgage broker.

Some brokers with non-bank lenders on their panel can arrange financing that traditional banks simply won’t consider. This proves invaluable for buyers with non-traditional income sources or unique property types.

Common Misconceptions About Banks and Brokers

Several myths persist about mortgage brokers and banks.

Clearing these up helps you make decisions based on facts rather than assumptions.

Misconception: Mortgage brokers cost borrowers money. Reality: Most mortgage brokers in New Zealand are paid commissions by lenders, so their services are generally free to borrowers. You don’t pay for advice, application support, or ongoing service.

Misconception: Banks always offer their customers the best rates. Reality: Banks advertise standard rates but often have discretion to negotiate. However, brokers negotiating across multiple lenders typically secure better rates than individual borrowers can get direct from banks.

Misconception: Brokers push products that pay them the most commission. Reality: Mortgage brokers in New Zealand are regulated by the Financial Markets Authority to act in clients’ best interests and avoid biased recommendations. They must disclose commission structures and recommend suitable products.

Common myths to dismiss:

- Brokers charge borrowers fees for their service (usually false)

- Going direct to your bank guarantees the best deal (often false)

- Brokers only work with risky lenders (false, they access all major banks too)

- Banks have more flexibility than brokers (opposite is true)

- Using a broker complicates the application process (brokers simplify it)

Understanding these realities helps you approach both options with clear expectations. The mortgage broker myths article explores additional misconceptions worth understanding before making your choice.

The regulation piece matters significantly. Brokers must hold a Financial Advice Provider license and follow strict conduct standards. This regulatory oversight protects you from biased advice and ensures brokers prioritize your interests over commission considerations.

Making Your Decision: Practical Steps for First Home Buyers

You’ve learned how banks and brokers work. Now let’s turn that knowledge into action with concrete steps for your Auckland home buying journey.

Assess your financial situation honestly. Calculate your income, expenses, savings, and credit history. Identify any complexity like self-employment, contract work, or recent credit issues. Complex situations benefit significantly from broker expertise.

Research mortgage brokers with broad lender panels. Look for advisers who access 20+ lenders including major banks, second-tier lenders, and non-bank options. Check their credentials, client reviews, and whether they specialize in first home buyers.

Request initial consultations from both your bank and selected brokers. Most brokers offer free initial meetings. Ask about lender access, estimated rates, and approval likelihood based on your profile. Compare the options and service quality you receive.

Compare not just rates but total costs and loan features. Look at application fees, ongoing fees, offset account options, and repayment flexibility. The lowest rate doesn’t always mean the best overall deal.

Choose the provider offering the best combination of rate, service, and loan features. Consider who you trust to guide you through the process. Proceed with your application confidently knowing you made an informed choice.

Pro Tip: Getting pre-approval from a broker before house hunting gives you negotiating power and clarity on your budget. You can then move quickly when you find the right property and that means you might beat the competition.

Document preparation matters regardless of which route you choose. Gather payslips, bank statements, IRD tax summaries, and identity documents early. Having these ready speeds up the application process whether you’re working with a bank or broker.

Timing your application strategically also helps. Avoid applying during end-of-month rushes when lenders are busy. Give yourself buffer time before auction dates or settlement deadlines. This reduces stress and allows proper comparison of offers.

Conclusion: Empowered Choices for Your Home Loan Journey

Choosing between banks vs brokers shapes your entire home buying experience. Brokers offer broader lender access, better negotiated rates, and expert guidance through complex situations. As mentioned, over 70% of New Zealand first home buyers choose this path for good reason.

Banks serve simple scenarios well, particularly for existing customers with straightforward financial profiles. The relationship banking approach offers convenience and potentially faster approval if you fit their lending criteria neatly.

Your specific situation determines the best choice. Complex profiles with self-employment, small deposits, or unique income benefit enormously from broker expertise. Simple profiles with strong banking relationships might find the direct route sufficient.

Regardless of which path you choose, seek professional advice tailored to your needs. The mortgage you secure affects your financial wellbeing for years to come. Taking time to explore both options ensures you make an informed decision rather than defaulting to what seems familiar.

Auckland’s property market demands strategic financing. The right mortgage partner, whether bank or broker, helps you navigate this market confidently and secure your first home on the best possible terms.

Talk To Mortgage Brokers That Can Help

Getting expert guidance makes all the difference in securing the right home loan.

Our team of mortgage brokers understand the local market and have relationships with multiple lenders to find solutions tailored to your situation.

Connecting with experienced advisers gives you access to loan options you won’t find going direct to banks. Talk to Auckland mortgage brokers who work across major banks and specialist lenders. These personal mortgage advisers act as your advocate, negotiating rates and terms while handling the paperwork complexity. Save time and secure competitive rates by working with professionals who understand the loan options brokers provide that banks simply can’t match.

Frequently Asked Questions

Do mortgage brokers charge fees to first home buyers?

Most mortgage brokers in New Zealand don’t charge borrowers any fees for bank mortgages as the banks pay them commission when your loan settles. This means that you receive professional advice and application support at no direct cost. For non-bank home loans there almost certainly will be a fee but this will be explained during your initial consultation.

When should I go direct to a bank instead of using a broker?

Go direct to your bank if you have a very straightforward financial profile, strong existing relationship with excellent banking history, and don;t need any choices as you have had time to research options yourself. Banks can offer faster approval for simple cases when you’re already a customer; however, even simple situations often benefit from having a broker review.

What documents do I need when applying through a mortgage broker?

You’ll need proof of identity like passport or driver license, recent payslips or income evidence, bank statements showing savings and expenses, plus details of any debts or credit commitments. Brokers guide you through exactly what’s required and help you prepare a strong application.

Are mortgage brokers properly regulated in New Zealand?

Yes, mortgage brokers must belong to a Financial Advice Provider that is licensed and follows strict conduct rules set by the Financial Markets Authority. They’re legally required to act in your best interests, disclose commission structures, and recommend suitable products. This information will be available in the brokers disclosure and the regulation protects borrowers from biased advice.

Can mortgage brokers help self-employed first home buyers?

Absolutely – most brokers are self-employed and specialise in complex lending scenarios including self-employment, contract work, and variable income. They know which lenders accommodate non-traditional income and how to present your application for best approval chances. This expertise proves invaluable when banks decline applications based on rigid criteria.