Many first home buyers mistakenly believe the Reserve Bank of New Zealand directly sets their mortgage interest rates.

The truth is more nuanced – the Reserve Bank influences mortgage costs primarily through the Official Cash Rate and lending regulations like LVR restrictions.

In this article we explain how these mechanisms affect your borrowing options, affordability, and home loan decisions in New Zealand. Understanding this relationship helps you make smarter mortgage choices and potentially save thousands of dollars.

Table of Contents

- Introduction To The Reserve Bank Of New Zealand And Mortgages

- Understanding The Official Cash Rate And Its Impact On Mortgages

- How Ocr Movements Influence Mortgage Interest Rates

- Factors Affecting Mortgage Interest Rates Beyond The Ocr

- Reserve Bank Regulatory Role In Mortgage Lending

- Common Misconceptions About Reserve Bank’s Role In Mortgages

- Impact Of Ocr And Mortgage Rate Changes On Borrower Affordability

- Reserve Bank Policy Outlook And Mortgage Market Implications

- How Mortgage Managers Can Help Navigate Reserve Bank Policies

- Frequently Asked Questions About The Reserve Bank And Mortgages

Key Takeaways

| Point | Details |

|---|---|

| OCR influences rates indirectly | The Reserve Bank sets the OCR at 2.25%, which guides bank lending costs but doesn’t dictate exact mortgage rates. |

| LVR restrictions regulate lending | Loan-to-Value Ratio caps typically require 20% deposits, promoting financial stability while challenging first home buyers. |

| Rates lag OCR changes | Mortgage rates adjust gradually after OCR movements, influenced by wholesale funding costs and market expectations. |

| Banks set actual rates | The Reserve Bank provides the framework, but individual lenders determine your specific mortgage interest rate. |

| Understanding saves money | Knowing how policies work helps you time loans effectively and negotiate better terms with lenders. |

Introduction to the Reserve Bank of New Zealand and Mortgages

The Reserve Bank of New Zealand operates with a clear mandate: maintain price stability and support maximum sustainable employment. These goals drive monetary policy decisions that ripple through the entire economy, including the mortgage market. For first home buyers, understanding this connection is crucial for effective financial planning.

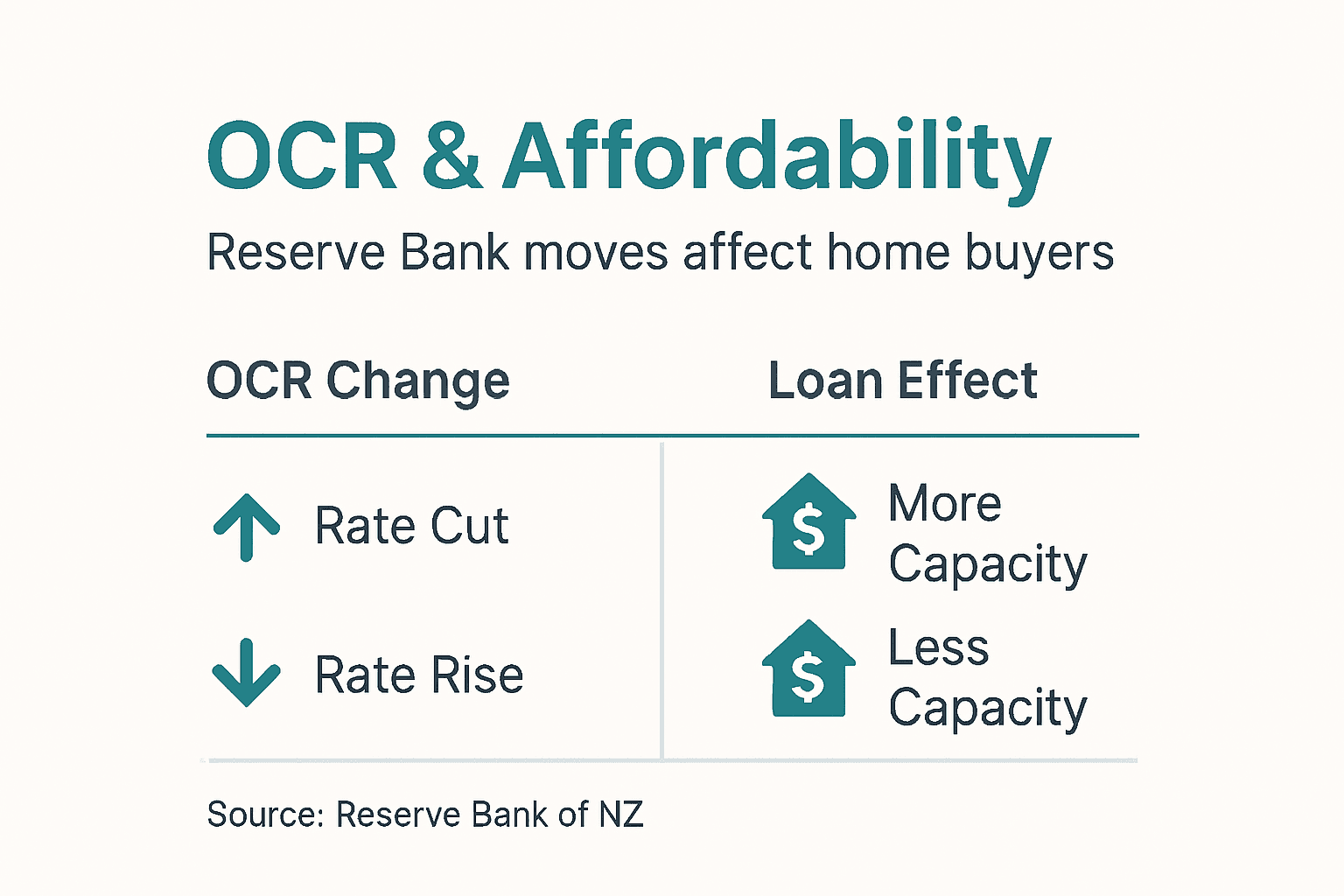

The primary tool in the Reserve Bank’s arsenal is the Official Cash Rate. This benchmark rate influences borrowing costs across the banking system. When the Reserve Bank adjusts the OCR, it signals to commercial banks how expensive or cheap money should be, which directly affects mortgage interest rates you’ll pay.

Key functions affecting mortgages include:

- Setting the OCR to manage inflation and economic growth

- Establishing lending regulations like LVR restrictions

- Monitoring financial system stability and bank behavior

- Publishing economic forecasts that shape market expectations

- Ensuring banks maintain adequate capital reserves

These tools work together to influence the impact of interest rates on home buyers throughout New Zealand. The Reserve Bank doesn’t approve or decline your mortgage application, but its policies shape the environment where banks make those decisions. The Reserve Bank’s Monetary Policy Statement 2026 provides detailed insights into current policy directions.

First home buyers who grasp these fundamentals can anticipate rate changes and plan deposits accordingly. You’re not at the mercy of random rate movements. There’s a logical structure behind mortgage pricing that you can learn to read and use to your advantage.

Understanding the Official Cash Rate and Its Impact on Mortgages

The Official Cash Rate represents the interest rate on overnight loans between commercial banks and the Reserve Bank. The Monetary Policy Committee reviews and sets this rate eight times yearly based on inflation data, employment figures, and economic growth projections. As of February 2026, the OCR sits at 2.25%, down significantly from its peak.

This rate serves as the foundation for all bank lending costs. When the OCR rises, banks pay more to borrow funds, which they pass on to mortgage customers through higher interest rates. When the OCR falls, borrowing becomes cheaper, and mortgage rates typically decline in response.

Here’s how the OCR transmission mechanism works:

- Reserve Bank announces OCR decision based on economic conditions

- Banks adjust their wholesale funding costs immediately

- Retail products like mortgages see rate changes within days or weeks

- Borrowers experience different monthly repayments based on new rates

- Housing market affordability shifts as borrowing capacity changes

The relationship isn’t perfectly linear. Banks maintain margins above the OCR to cover operating costs and profit requirements. A 0.25% OCR cut might translate to a 0.20% or 0.30% mortgage rate reduction depending on competitive pressures and funding conditions.

For first home buyers, OCR movements directly affect how much house you can afford. Lower rates mean higher borrowing capacity with the same income. Higher rates reduce what banks will lend you. Tracking why mortgage rates change helps you time your purchase and loan application strategically.

Pro Tip: Subscribe to Reserve Bank OCR announcement alerts and review the accompanying statement. The commentary reveals whether future moves are likely up, down, or stable, helping you decide between fixed and floating mortgage options.

How OCR Movements Influence Mortgage Interest Rates

The OCR’s journey from 2023 to 2026 illustrates the powerful effect of monetary policy on mortgage costs. The OCR fell from 5.5% in late 2023 to 2.25% by February 2026, representing a substantial easing cycle. Mortgage rates followed this trajectory with typical lag periods.

| Period | OCR Level | Average Mortgage Rate | Monthly Payment ($300k loan, 30 years) |

|---|---|---|---|

| Late 2023 | 5.50% | 6.80% | $1,940 |

| Mid 2025 | 4.25% | 5.90% | $1,770 |

| Early 2026 | 2.25% | 4.60% | $1,540 |

This data shows monthly savings of approximately $400 for borrowers who refinanced or purchased during the rate decline. Over a year, that’s $4,800 back in your pocket simply from OCR policy changes.

Several factors explain why mortgage rates don’t mirror OCR movements exactly:

- Banks factor in wholesale swap rates for fixed-term mortgages

- Lender funding costs include offshore borrowing not tied directly to OCR

- Competitive positioning among banks creates rate variations

- Risk assessments differ by borrower profile and loan characteristics

- Regulatory capital requirements affect lending margins

The Reserve Bank OCR drops today often triggers immediate responses from major banks, with second-tier lenders following within days. Shopping around during these windows can yield better deals as banks compete for market share.

Timing matters significantly. Borrowers who locked fixed rates at the 2023 peak paid premiums for years. Those who waited or refinanced as rates fell saved substantially. Analysis of OCR drops impact on mortgages shows the cumulative savings can exceed $50,000 over a typical mortgage term.

Pro Tip: When the Reserve Bank signals a cutting cycle, consider shorter fixed terms or floating rates to capture further decreases. When rate hikes loom, lock in longer fixed periods to protect against increases.

Factors Affecting Mortgage Interest Rates Beyond the OCR

While the OCR dominates headlines, other market forces significantly influence the mortgage rates banks offer. Swap rates, which reflect longer-term money market costs, particularly affect fixed mortgage pricing. These rates move independently based on global interest rate trends and economic expectations.

Wholesale funding costs create another layer of complexity. New Zealand banks source funds domestically through deposits and internationally through bond markets. When global credit conditions tighten, banks pay more for offshore funding regardless of OCR levels. This premium gets passed to mortgage customers.

Additional influences on mortgage rates include:

- Bank competition intensity and market share objectives

- Regulatory capital requirements set by the Reserve Bank

- Credit risk assessments based on borrower profiles

- Economic outlook and inflation expectations

- Property market conditions and lending volume targets

Market expectations play a crucial role. If investors anticipate future OCR increases, long-term fixed rates may rise even before the Reserve Bank acts. Conversely, expectations of cuts can lower fixed rates ahead of official OCR reductions.

Mortgage rates also vary significantly by product type and borrower circumstances. First home buyers with 10% deposits typically pay higher rates than those with 30% deposits due to perceived risk. Similarly, investors face different pricing than owner-occupiers under current lending policies.

Understanding these factors affecting mortgage rates helps you interpret why your quoted rate differs from advertised rates or why rates change between application and settlement. Banks balance multiple variables beyond just the OCR when pricing mortgages.

The lag between OCR changes and mortgage rate adjustments reflects these complexities. Banks need time to assess how funding costs, competition, and risk profiles interact with new OCR settings before finalizing retail rate changes.

Reserve Bank Regulatory Role in Mortgage Lending

Beyond monetary policy, the Reserve Bank wields significant regulatory authority over mortgage lending standards. Loan-to-Value Ratio restrictions represent the most visible regulatory tool affecting first home buyers. These rules limit how much banks can lend relative to property values, directly impacting deposit requirements.

LVR restrictions aim to reduce financial system risk by ensuring borrowers have meaningful equity stakes in their properties. When property prices fall, borrowers with larger deposits are less likely to default because they retain equity. This protects both individual households and the broader banking system.

Current LVR framework typically requires:

- 20% deposit for standard home loans (80% LVR maximum)

- 10% deposit for first home buyers under exemptions (90% LVR)

- Higher deposits for investors and multiple property owners

- Stricter requirements during periods of housing market overheating

| Borrower Type | Typical Deposit Required | LVR Limit | Impact on Access |

|---|---|---|---|

| First Home Buyer (exempt) | 10% | 90% | Moderate barrier |

| Standard Owner-Occupier | 20% | 80% | Significant barrier |

| Property Investor | 30-40% | 60-70% | High barrier |

These requirements create challenges for first home buyers accumulating deposits. A $600,000 property requires $60,000 to $120,000 saved depending on your LVR eligibility. For many young buyers, this represents years of savings, particularly in high-cost Auckland markets.

The Reserve Bank adjusts LVR settings based on housing market conditions and financial stability concerns. During rapid price growth, restrictions tighten. When markets cool, they may ease. Understanding lender criteria for first home loans helps you navigate these requirements.

The LVR restrictions impact on first home buyers extends beyond deposit size. Banks assess borrowing capacity differently at various LVR levels. Lower LVRs often unlock better interest rates and more flexible loan terms.

Pro Tip: Start building your deposit early and maintain clean credit. Some banks offer first home buyer programs with lower LVR requirements, but competition for these spots is fierce. Working with experienced advisers increases your chances of approval.

Common Misconceptions about Reserve Bank’s Role in Mortgages

Confusion about the Reserve Bank’s mortgage influence leads many first home buyers to misunderstand how lending actually works. Clearing up these misconceptions helps you make better borrowing decisions and set realistic expectations.

The most prevalent myth: the Reserve Bank directly sets your mortgage interest rate. Surveys show many borrowers think the RBNZ directly sets mortgage rates, but it only establishes the OCR and regulatory frameworks. Banks independently determine retail rates based on multiple factors including the OCR, competition, and risk assessments.

Other common misunderstandings include:

- Believing the Reserve Bank approves individual mortgage applications (banks make these decisions)

- Thinking OCR changes instantly affect existing fixed-rate mortgages (only new loans or refixes)

- Assuming all banks must charge identical rates (competition creates variation)

- Expecting mortgage rates to match OCR movements exactly (margins and other costs apply)

- Believing Reserve Bank controls property prices directly (influence is indirect through credit conditions)

The Reserve Bank’s role is foundational but indirect. It sets the rules and benchmark rates within which banks operate. Your actual mortgage terms depend on your bank’s assessment of your financial situation, the competitive landscape, and broader funding costs.

Another misconception involves timing. Many buyers assume rate changes happen immediately after OCR announcements. In reality, banks need time to adjust systems, assess competitive positioning, and recalculate risk profiles. Fixed rates may not move at all if swap rates remain stable despite OCR changes.

Understanding the clarification on RBNZ role in mortgage rates prevents frustration when your mortgage application doesn’t follow expected patterns. The Reserve Bank creates the environment, but commercial banks execute within that framework based on business objectives.

First home buyers benefit from viewing the Reserve Bank as setting the stage rather than directing every scene. Your mortgage outcome depends on how you and your bank navigate that stage together.

Impact of OCR and Mortgage Rate Changes on Borrower Affordability

Mortgage rate movements directly transform housing affordability through monthly repayment changes and borrowing capacity adjustments. The 2023 to 2026 OCR reduction cycle demonstrates this connection clearly through real dollar impacts.

Consider a $300,000 mortgage over 30 years:

- At 6.8% interest (late 2023 rates): monthly payment of $1,940

- At 4.6% interest (early 2026 rates): monthly payment of $1,540

- Monthly savings: approximately $400

- Annual savings: $4,800

- Savings over 5 years: $24,000

These numbers represent real money back in borrower pockets, available for other expenses, savings, or additional principal payments. For first home buyers on tight budgets, this difference determines whether homeownership feels manageable or stressful.

Borrowing capacity shifts even more dramatically. At higher rates, banks lend less because they must ensure you can service loans at stressed test rates. Lower rates increase what banks will lend with the same income. A household earning $100,000 annually might qualify for $450,000 at 6.8% rates but $550,000 at 4.6% rates.

This $100,000 borrowing capacity increase opens access to different property markets and neighborhoods. What seemed unaffordable becomes achievable simply through OCR policy changes, even without income growth or additional savings.

Timing loans strategically amplifies these benefits. Buyers who waited through the 2023 high-rate period and purchased in 2026 as rates fell captured both lower repayments and better property values in softer markets. The impact of LVR changes on affordability compounds these effects when regulations ease alongside rate reductions.

Pro Tip: When OCR cuts begin, don’t assume rates will fall forever. Lock in competitive fixed rates once you identify a favorable environment. Waiting for the absolute bottom often means missing good opportunities as markets adjust quickly.

Following mortgage management tips for first home buyers helps you maximize savings from favorable rate environments while protecting against future increases through smart loan structuring.

Reserve Bank Policy Outlook and Mortgage Market Implications

Looking forward through 2026 and beyond, the Reserve Bank signals a relatively stable OCR environment barring unexpected economic shocks. Current forecasts suggest the OCR will remain near 2.25% through mid-2026, with potential adjustments depending on inflation performance and global economic conditions.

This stability benefits first home buyers through predictable mortgage rate environments. Banks can offer competitive fixed rates without large risk premiums for uncertainty. Borrowers can plan purchases and budgets with greater confidence than during volatile periods.

Key factors shaping the outlook include:

- Inflation tracking toward the Reserve Bank’s 1-3% target band

- Employment remaining strong but wage growth moderating

- Housing market activity recovering from 2023-2024 slowdown

- Global interest rate trends as major central banks adjust policies

- Potential regulatory changes to LVR restrictions if market conditions warrant

First home buyers should monitor these indicators through regular Reserve Bank statements and economic data releases. Sudden inflation spikes could trigger OCR increases, while economic weakness might prompt further cuts. Neither scenario appears immediately likely, but conditions change rapidly.

The current environment favors borrowers who can act decisively. Mortgage rates in the mid-4% range represent significant affordability improvements compared to recent history. However, property prices may rise as more buyers enter markets, potentially offsetting some rate advantages.

Timing considerations for 2026:

- Lock fixed rates if current levels meet your budget and goals

- Don’t wait indefinitely for perfect timing that may never arrive

- Consider 2-3 year fixed terms to balance security and flexibility

- Maintain emergency funds as economic conditions remain somewhat uncertain

- Review loan structures annually to ensure they still suit your circumstances

Staying informed through regular monitoring helps you adapt borrowing strategies as conditions evolve. The Reserve Bank publishes detailed forecasts and policy rationale that provide valuable planning insights for proactive buyers.

How Mortgage Managers Can Help Navigate Reserve Bank Policies

Understanding Reserve Bank policies intellectually differs from applying that knowledge to secure optimal mortgage outcomes.

All the team at Mortgage Managers are good at translating complex policy environments and home loan rate predictions into practical strategies for first home buyers throughout New Zealand.

Our mortgage advisers for home loans monitor OCR developments, LVR changes, and bank lending criteria continuously. This expertise helps you time applications strategically and structure loans that maximize affordability while managing risk.

We provide personalized guidance on navigating LVR restrictions, including identifying lenders offering favorable first home buyer programs. Our relationships across the banking sector reveal opportunities not always visible to individual buyers shopping alone. The role of a mortgage adviser in NZ extends beyond simply arranging loans to becoming your strategic partner through the entire home buying journey.

Based in Hobsonville with expertise across Auckland and remote service throughout New Zealand, our expert mortgage advisers and brokers deliver local market knowledge combined with national lending access. We help you understand how Reserve Bank policies specifically affect your situation and what actions optimize your position.

Start your home buying journey informed and supported. Contact Mortgage Managers today to discuss how current Reserve Bank settings create opportunities for your first home purchase.

Frequently Asked Questions about the Reserve Bank and Mortgages

What exactly does the Reserve Bank’s OCR mean for my mortgage?

The OCR serves as the benchmark rate influencing what banks charge for mortgages. When the OCR falls, mortgage rates typically decline within weeks, reducing your monthly repayments and increasing borrowing capacity. Your specific rate depends on the OCR plus bank margins and your risk profile.

Can the Reserve Bank stop banks from raising mortgage rates?

No, the Reserve Bank cannot prevent banks from setting their own retail mortgage rates. Banks operate as independent businesses that price loans based on funding costs, competition, and risk management. The Reserve Bank influences the environment but doesn’t control individual bank pricing decisions.

How do LVR restrictions affect my ability to buy a home?

LVR restrictions determine minimum deposit requirements, typically 20% for standard buyers or 10% for eligible first home buyers. These rules can delay purchases while you save larger deposits but protect financial stability. Some banks offer exemption programs worth exploring with experienced advisers.

Why don’t mortgage rates always change immediately when the OCR changes?

Mortgage rates reflect multiple factors beyond the OCR, including wholesale swap rates, bank funding costs, and competitive positioning. Fixed rates particularly depend on longer-term money market conditions that don’t move in lockstep with OCR changes. Banks also need time to assess and implement pricing adjustments.

Should I wait for OCR forecasts before locking a mortgage rate?

Waiting for perfect timing often backfires as markets adjust quickly and property prices may rise. If current rates fit your budget and goals, locking in provides certainty and protection. Consider shorter fixed terms if you expect further falls, allowing you to refix at potentially lower rates without excessive break fees.