Many first home buyers and even existing home owners are not aware of the benefits of offset mortgages.

Probably the main reason is that Offset Mortgages are only available from three banks here, and even those banks struggle to explain how they work. It’s really only some of the best mortgage advisers that have made the effort to really understand and know the benefits of Offset Mortgages from all three of the banks that offer them.

Australian homeowners have known the benefits of Offset Mortgages for many years and have implemented these into the advanced loan strategies used, but New Zealand banks now offer the same tools to cut mortgage costs.

With home loan rates climbing, every dollar saved matters when you are balancing a family budget.

We have created this like a no-nonsense guide that explains how offset mortgages work, why they are not just for high-income earners, and how smart banking habits can lead to real, long-term savings.

Table of Contents

- Offset Mortgages Defined And Common Misconceptions

- How Offset Mortgages Work In New Zealand

- Types Of Offset Arrangements Offered By Lenders

- Eligibility And Setting Up An Offset Account

- Interest Savings, Costs And Financial Risks

- Offset Mortgages Versus Redraw Facilities Compared

Key Information about Offset Mortgages

| Point | Details |

|---|---|

| Understanding Offset Mortgages | Offset mortgages link savings accounts to home loans, lowering interest charges based on linked account balances. |

| Flexible Options | Lenders offer various offset strategies, including full offset, partial offset, and selective linking, catering to diverse financial profiles. |

| Eligibility Criteria | Approval for offset mortgages typically requires stable income and a solid credit history, often favouring existing customers with significant savings. |

| Financial Assessment | Borrowers should weigh potential interest savings against opportunity costs and actively manage linked savings to maximise benefits. |

Offset Mortgages Defined and Common Misconceptions

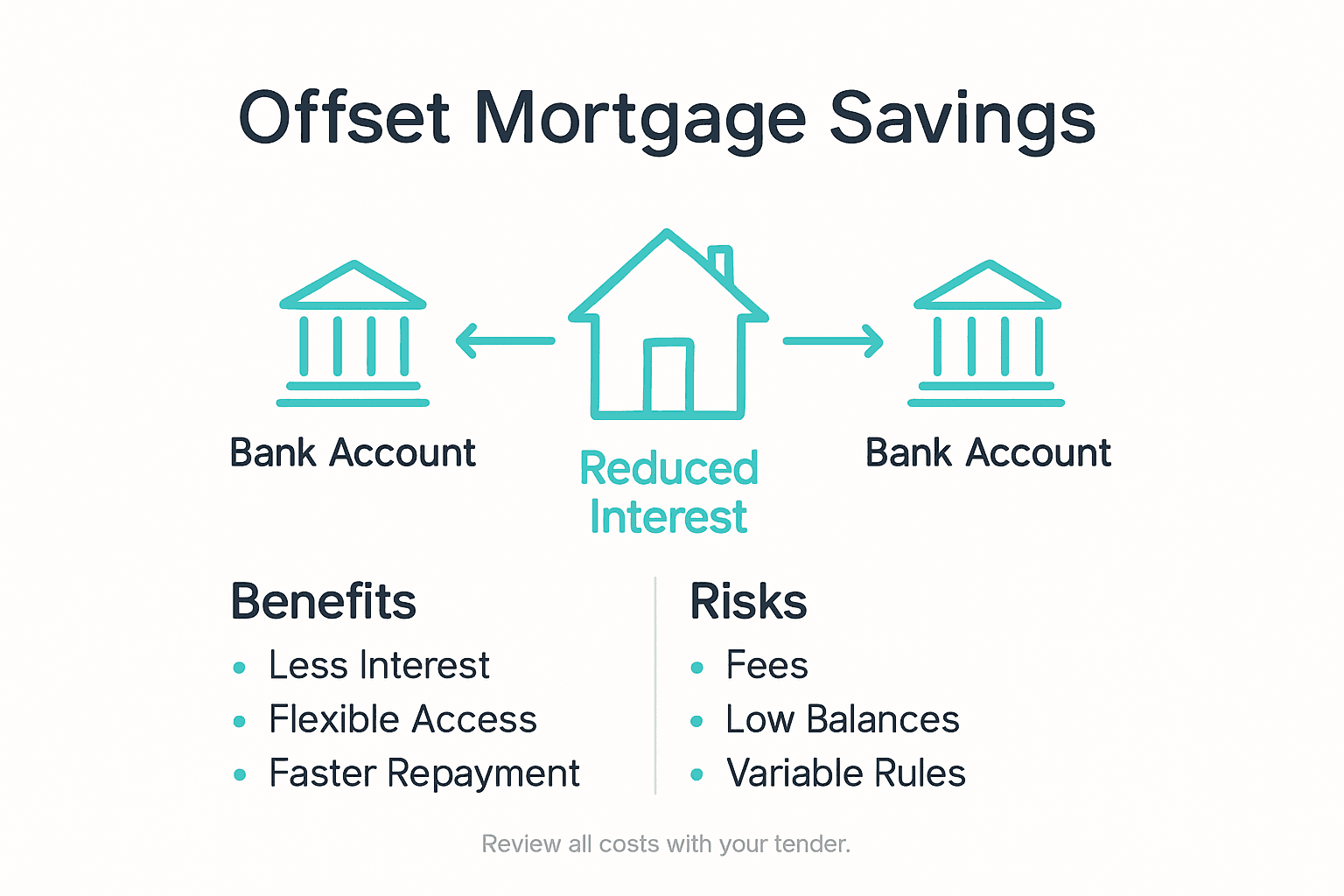

An offset mortgage is a powerful financial tool designed to help Kiwi homeowners reduce their overall interest payments by strategically linking their savings and transaction accounts directly to their home loan. Unlike traditional mortgage structures, this approach allows borrowers to effectively lower their interest charges by maintaining funds in linked accounts that are “offset” against their loan principal.

The fundamental mechanism involves linking multiple deposit accounts to a home loan account, enabling borrowers to reduce the amount of interest calculated on their mortgage balance. For instance, if you have a $500,000 home loan and $50,000 in linked savings accounts, you would only be charged interest on $450,000. This approach can potentially save significant money over the loan’s lifetime by minimising the interest accrual.

However, several common misconceptions persist about offset mortgages that can confuse potential borrowers. Many people mistakenly believe these arrangements are complex or only suitable for high-income earners. In reality, offset mortgages can benefit a wide range of New Zealand homeowners, particularly those with consistent savings habits and flexible banking arrangements. The key is understanding that every dollar in your linked account works to reduce your overall interest burden.

Pro tip: Before selecting an offset mortgage, carefully compare the interest rates and fees across different lenders to ensure the potential savings outweigh any additional account maintenance costs.

How Offset Mortgages Work in New Zealand

Offset mortgages represent an innovative financial strategy for New Zealand homeowners seeking to reduce their overall interest expenses. These unique home loan arrangements dynamically link savings and transaction accounts to create a more flexible approach to mortgage management. The core principle involves using the funds in your linked accounts to directly minimise the interest charged on your home loan principal.

The mechanism is straightforward yet powerful. When you maintain funds in a linked account, those balances are effectively subtracted from your total mortgage amount before interest calculations occur. For example, if you have a $400,000 mortgage and consistently keep $50,000 in linked savings, you would only be charged interest on $350,000. This approach can potentially save thousands of dollars over the lifetime of your loan by reducing the compound interest accumulation.

Understanding the nuanced workings of offset mortgages requires examining how banks calculate and apply these reductions. The daily balance offset means that every dollar in your linked accounts works immediately to reduce your loan’s interest burden. This differs significantly from traditional mortgage structures, where savings and loan accounts remain completely separate. Particularly for Kiwi borrowers with variable income or those who maintain substantial savings, offset mortgages can provide remarkable financial flexibility and potential long-term savings.

Pro tip: Review your bank’s specific offset mortgage rules carefully, as the exact mechanisms and benefits can vary between different financial institutions.

Types of Offset Arrangements Offered by Lenders

Offset mortgage arrangements in New Zealand represent a diverse range of financial strategies that allow borrowers to strategically manage their home loan interest.

Different lenders offer unique variations, each designed to provide flexibility and potential interest savings for homeowners. These arrangements typically fall into three primary categories: full offset, partial offset, and selective account linking.

In a full offset arrangement, all linked accounts’ balances are completely subtracted from the mortgage principal before interest calculations. This means if you have a $500,000 mortgage and $75,000 across various linked accounts, you would be charged interest only on $425,000. Partial offset arrangements work similarly but only apply a percentage of the linked account balances, providing a more conservative approach to interest reduction. Some lenders might offset only 80% of your linked account balances, offering a middle ground between traditional mortgages and full offset options.

The complexity of these arrangements extends beyond simple balance reduction. Lenders often have specific rules about which types of accounts can be linked, the minimum balance requirements, and how frequently the offset is calculated. Some banks may allow linking of transaction accounts, savings accounts, and even business accounts, while others might restrict linkages to personal savings accounts. This variability underscores the importance of carefully reviewing each lender’s specific offset mortgage terms and understanding how they align with your personal financial situation and savings patterns.

Here’s a side-by-side comparison of the main types of offset arrangements offered by New Zealand lenders:

| Arrangement Type | Offset Mechanism | Key Benefit | Typical Limitation |

|---|---|---|---|

| Full Offset | All linked balances fully offset loan | Maximum interest savings | May require higher minimum balances |

| Partial Offset | Only a percentage offset applies | Accessible for more borrowers | Lower potential savings than full offset |

| Selective Linking | Specific account types can be linked | Flexibility in account selection | May restrict business or some personal accounts |

Pro tip: Always request a detailed breakdown of offset calculation methods from potential lenders, as the nuances can significantly impact your long-term interest savings.

Eligibility and Setting Up an Offset Account

Establishing an offset account requires meeting specific banking and regulatory requirements designed to protect both financial institutions and customers. Potential borrowers must navigate a series of eligibility criteria that encompass financial standing, credit history, and personal documentation. Generally, New Zealand banks look for individuals with a stable income, a solid credit record, and an existing relationship with the financial institution.

The documentation process involves comprehensive identity verification and financial assessment. Typically, banks will require proof of identity (such as a passport or driver’s licence), proof of address, recent payslips or income statements, and a detailed overview of your current financial situation. Credit assessments examine factors like your income-to-debt ratio, employment stability, and previous banking history. Those with a strong financial profile and a consistent savings pattern are more likely to be approved for an offset mortgage arrangement that maximises their potential interest savings.

Unique to New Zealand’s banking landscape, offset accounts offer flexibility for various customer profiles. Some lenders provide more lenient requirements for existing customers or those with substantial savings, while others might have stricter criteria for new account holders. The key considerations include minimum balance requirements, the types of accounts that can be linked, and the specific terms of the offset arrangement. Different banks may offer varying levels of account linkage, from personal transaction accounts to savings and even business accounts, each with its own set of eligibility parameters.

Pro tip: Gather all financial documentation in advance and consider speaking with a mortgage adviser who can help you understand the specific eligibility requirements of different lenders.

Interest Savings, Costs and Financial Risks

Offset mortgages present a nuanced approach to managing home loan interest that requires careful financial planning and disciplined savings behaviour. The potential for interest savings is substantial, but borrowers must understand the intricate balance between financial benefits and potential risks associated with these innovative mortgage structures.

The primary financial advantage lies in the daily interest reduction mechanism. By maintaining substantial balances in linked accounts, borrowers can significantly decrease the effective loan principal on which interest is calculated. For instance, a $400,000 mortgage with a consistent $50,000 offset balance could save thousands in interest over the loan’s lifetime. However, this strategy comes with important caveats. The linked accounts typically do not earn traditional interest, which represents an opportunity cost that borrowers must carefully evaluate against the potential interest savings.

Financial risks emerge from several critical factors that can impact the effectiveness of an offset mortgage arrangement. Economic fluctuations, interest rate changes, and personal financial stability can all influence the strategy’s success. Borrowers must maintain disciplined savings patterns and avoid frequent large withdrawals that could negate the interest reduction benefits. Some lenders impose fees for offset account maintenance, and the complex calculations require ongoing attention to ensure the arrangement continues to provide financial advantages.

Pro tip: Maintain a consistent offset account balance and regularly review your mortgage structure to maximise interest savings while monitoring potential hidden costs.

Offset Mortgages Versus Redraw Facilities Compared

Mortgage strategies in New Zealand offer borrowers multiple approaches to managing their home loan finances, with offset mortgages and redraw facilities representing two distinct yet potentially complementary options. While both strategies aim to provide financial flexibility, they operate through fundamentally different mechanisms that can significantly impact a borrower’s long-term financial planning.

Offset mortgages function by directly linking savings accounts to the mortgage, reducing the daily interest calculation based on the combined account balances. In contrast, redraw facilities allow borrowers to make additional repayments into their mortgage and subsequently withdraw those extra funds if needed. The key distinction lies in how these approaches handle surplus funds. Offset accounts provide an immediate interest reduction benefit, whereas redraw facilities require extra repayments first and may involve more administrative steps to access funds.

The practical implications of these differences can be substantial for New Zealand homeowners. Offset accounts typically offer more immediate liquidity and daily interest savings, making them attractive for those with consistent savings and variable income streams. Redraw facilities, however, might suit borrowers who prefer a more structured approach to additional repayments and are comfortable with potential withdrawal restrictions. Each strategy carries unique advantages: offset accounts provide ongoing interest reduction, while redraw facilities offer a more traditional extra repayment model with the flexibility to reclaim surplus funds.

To clarify, here’s how offset mortgages compare with redraw facilities for Kiwi homeowners:

| Feature | Offset Mortgage | Redraw Facility |

|---|---|---|

| Access to Funds | Immediate via linked accounts | Withdraw extra repayments only |

| Interest Savings | Reduces interest daily based on balance | Based on extra repayments, less immediate |

| Account Structure | Funds remain accessible | Requires prior extra payment |

| Suitable For | Regular savers, variable income | Structured repayment, less frequent access |

Pro tip: Carefully assess your personal financial habits and cash flow patterns before selecting between offset mortgages and redraw facilities to maximise your potential savings.

Maximise Your Interest Savings with Expert Offset Mortgage Advice

Navigating the complexities of offset mortgages can feel overwhelming, especially when trying to balance your savings and home loan to reduce interest effectively. This article highlights how offset arrangements can save thousands but also shows the importance of understanding lender differences, eligibility, and potential costs. If you want to unlock the full benefits of offset mortgages and avoid costly mistakes, tailored guidance is essential.

At Mortgage Managers, our Auckland-based mortgage advisers specialise in helping Kiwi homeowners like you optimise home loan structures including offset mortgages. We provide personalised strategies that align with your financial goals and saving habits. Don’t let uncertainty or complex terms hold you back from reducing your mortgage interest.

Visit our website today, explore how we can assist you, and take the next step towards smarter borrowing with Mortgage Managers.

Explore more about home loan solutions with our dedicated support to ensure you get the best outcome from your offset mortgage journey.

Frequently Asked Questions

What is an offset mortgage?

An offset mortgage is a type of home loan that links your savings and transaction accounts directly to the mortgage, allowing your savings to reduce the loan principal on which interest is calculated. This can lead to significant interest savings over the life of the loan.

How do offset mortgages save you money on interest?

Offset mortgages save you money by using the balances in your linked accounts to offset the mortgage amount. For example, if you have a $500,000 mortgage and $50,000 in linked accounts, you would only be charged interest on $450,000, which can reduce overall interest payments significantly.

Can you link and offset someone else’s account?

The answer is generally YES and this is used a lot. When set up correctly your mortgage can be offset against someone else’s bank account. The most common example is parents who want to help their child while retaining control of their own money.

Ask your mortgage adviser and they can explain how to set this up, and the advantages of these arrangements.

Are there different types of offset arrangements offered by lenders?

Yes, lenders typically offer three main types of offset arrangements: full offset, where all linked balances offset the loan; partial offset, where only a percentage of balances is considered; and selective linking, where specific account types can be linked for an offset.

What are the eligibility requirements for setting up an offset mortgage?

Eligibility requirements for offset mortgages usually include having a stable income, a good credit history, and providing the necessary documentation, such as proof of identity and income. Different lenders may have different criteria, especially for existing customers versus new account holders.