Applying for a mortgage in Auckland can feel overwhelming when property prices keep climbing and lenders tighten requirements. First home buyers often struggle with deposit sizes, credit checks, and complex paperwork. This guide walks you through each step of the mortgage application process, from pre-approval to final settlement, helping you secure financing even with a modest deposit or limited credit history.

Table of Contents

- Introduction To Mortgage Application In Auckland

- Prerequisites: What You Need Before Applying

- Step 1: Getting Mortgage Pre-Approval

- Step 2: Preparing And Submitting Your Mortgage Application

- Step 3: Understanding Loan Types And Structuring Options

- Step 4: Low Deposit Options And Government Assistance

- Step 5: Common Pitfalls And Mistakes To Avoid

- Step 6: Expected Timelines, Fees, And Final Approval

- Talk To Auckland Mortgage Brokers That Can Help

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Government loan schemes allow 5% deposits for eligible buyers | Kāinga Ora First Home Loan reduces upfront cash requirements significantly |

| Mortgage pre-approval clarifies borrowing power and expedites buying | Valid for 3 to 6 months, showing sellers you’re serious |

| Proper document preparation increases chances of loan approval | Income proof, deposit evidence, and ID must be complete |

| Choosing the right loan type affects repayments and flexibility | Fixed, variable, and split loans each suit different financial goals |

| Mortgage brokers save time and help secure better deals | They navigate lender requirements and find tailored options |

Introduction to mortgage application in Auckland

Auckland’s property market presents unique challenges for first home buyers. High Auckland property prices compared to national averages affect deposit sizes and loan amounts, making affordability a genuine concern. While traditional deposits sit around 20% of purchase price, government-backed schemes now enable entry with as little as 5% down.

Recent lending rules introduced mid-2024 enforce stricter debt-to-income ratios, meaning lenders scrutinise your income against total borrowing more carefully. Understanding these conditions prepares you for realistic planning and prevents surprises during applications.

Key factors shaping Auckland mortgage applications include:

- Property prices exceeding national averages by significant margins

- Deposit requirements ranging from 5% through government schemes to 20% for standard loans

- Tighter lending standards focusing on debt-to-income ratios

- Extended processing times during peak market periods

Navigating this landscape requires clear preparation and knowledge of available support mechanisms. Kāinga Ora First Home Loan offers pathways for buyers who meet income caps and other criteria. Planning ahead and managing mortgage in Auckland strategically positions you for success.

Prerequisites: what you need before applying

Lenders require specific documentation and financial readiness before processing mortgage applications. Proof of stable income, a minimum deposit, and proper identification are essential before applying. Preparing these items in advance streamlines the process and demonstrates financial responsibility.

Core requirements include:

- Stable employment history spanning at least three months, preferably longer

- Deposit funds ranging from 5% for government-backed loans to 20% for conventional mortgages

- Valid government-issued identification such as passport or driver licence

- KiwiSaver account statements if planning to use savings for deposits

- Recent credit report showing your borrowing history and current obligations

Income verification typically demands recent payslips, tax returns for self-employed applicants, and bank statements covering three to six months. Lenders assess your ability to service the loan by examining income stability and existing debt commitments.

Your deposit source matters. Whether from savings, KiwiSaver withdrawals, or family gifts, lenders need documentation proving legitimate origins. Gift letters from family members should clearly state the funds are non-repayable.

Pro Tip: Check your credit report three months before applying. Dispute any errors immediately, as correcting mistakes can take weeks and directly impacts approval chances.

Review the comprehensive mortgage application checklist to ensure nothing is missed. Organised documentation signals reliability to lenders and expedites approval timelines significantly.

Step 1: getting mortgage pre-approval

Mortgage pre-approval establishes your borrowing capacity before house hunting begins. Pre-approval provides a valid borrowing limit for 3 to 6 months and shows sellers you are serious. This conditional commitment from lenders clarifies your budget and strengthens negotiating positions.

The pre-approval process follows these steps:

- Gather preliminary documentation including income proof, deposit evidence, and identification

- Submit application to chosen lender or through a mortgage broker

- Lender reviews finances and credit history to determine borrowing capacity

- Receive pre-approval letter stating maximum loan amount and validity period

- Use pre-approval to shop for properties within confirmed budget limits

Pre-approval differs from full approval. It’s conditional on property valuation, employment stability, and no significant financial changes. Lenders reserve the right to withdraw pre-approval if circumstances shift.

Validity periods typically span three to six months. If house hunting extends beyond this timeframe, you’ll need to renew pre-approval with updated documentation. Market conditions and lending criteria may change, affecting borrowing capacity.

Pro Tip: Apply for pre-approval even before seriously house hunting. Knowing your exact budget prevents wasting time on properties outside your price range and helps you act quickly when the right home appears.

Understanding the full steps to get a mortgage helps position pre-approval as the critical first milestone in your home buying journey.

Step 2: preparing and submitting your mortgage application

Once you’ve found a property and negotiated terms, the formal mortgage application begins. Completing detailed application forms with financial and employment information is critical to lender assessment. This stage requires comprehensive documentation and honest disclosure.

Application submission involves:

- Completing lender-specific application forms with personal, employment, and financial details

- Providing updated income verification, bank statements, and asset documentation

- Submitting property purchase agreement and deposit receipt

- Authorising credit checks and employment verification

- Declaring all liabilities including credit cards, personal loans, and other commitments

Lenders accept applications digitally through online portals or in person at branches. Digital submissions often process faster, with automated systems flagging incomplete sections immediately.

Assessment criteria focus on three key areas. Income stability demonstrates ability to maintain repayments through employment history and earnings consistency. Debt levels reveal existing commitments that impact disposable income available for mortgage repayments. Living expenses are scrutinised to ensure realistic budgeting after mortgage costs.

Mortgage brokers streamline this process significantly. They understand individual lender requirements, pre-screen applications for completeness, and match your profile to suitable lenders. Using benefits of mortgage brokers means accessing multiple lenders simultaneously without separate applications.

Transparency matters enormously. Omitting debts or overstating income triggers automatic declines and damages future applications. Refer to the mortgage application checklist to verify completeness before submission.

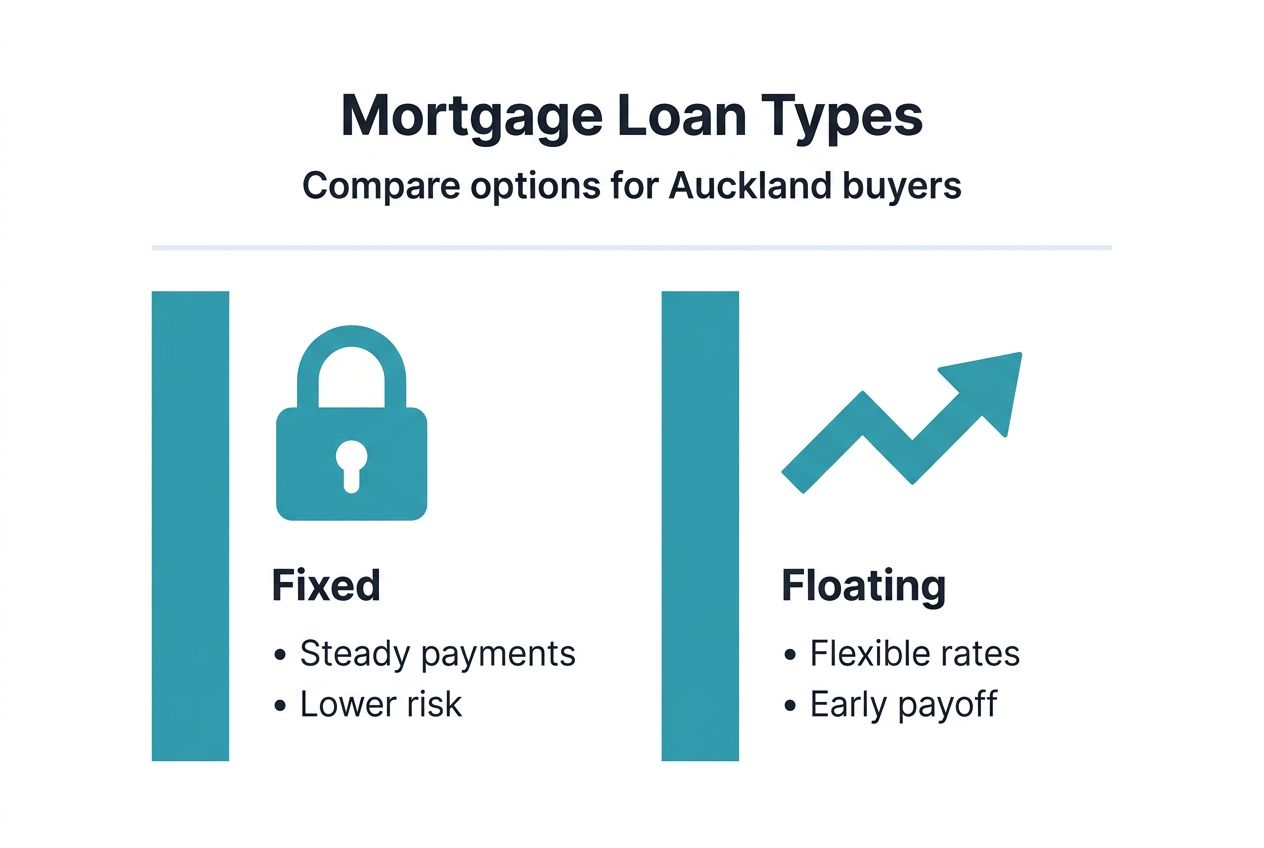

Step 3: understanding loan types and structuring options

Choosing the right loan structure affects monthly repayments, flexibility, and long-term costs. Fixed rates give budgeting certainty, variable rates offer flexibility, and split loans combine advantages of both. Understanding each option helps match loans to your financial situation and risk tolerance.

Main loan types include:

- Fixed rate loans lock interest rates for one to five years, providing predictable repayments ideal for tight budgets

- Variable rate loans fluctuate with market conditions, offering potential savings when rates drop plus repayment flexibility

- Split loans divide borrowing between fixed and variable portions, balancing certainty with flexibility

- Interest-only loans defer principal repayments temporarily but cost more long-term and suit specific investment scenarios

Principal and interest repayments remain the standard choice. Each payment reduces the loan balance while covering interest charges, building equity steadily. Interest-only options delay equity building and typically cost more over the loan lifetime.

| Loan Type | Best For | Key Advantage | Main Risk |

|---|---|---|---|

| Fixed | First-time buyers needing budget certainty | Predictable repayments regardless of rate changes | Missing out if market rates drop |

| Variable | Financially flexible buyers comfortable with risk | Lower rates when market falls, extra repayment freedom | Higher costs if rates rise unexpectedly |

| Split | Buyers wanting balance between certainty and flexibility | Hedge against rate movements in either direction | More complex management and paperwork |

Consider your employment stability, risk appetite, and financial goals when selecting loan types. Review mortgage application tips for guidance on matching loan structures to personal circumstances.

Step 4: low deposit options and government assistance

Government schemes and KiwiSaver withdrawals help buyers overcome deposit barriers. Kāinga Ora offers mortgages with a 5% deposit for eligible buyers within income caps. These programmes specifically target first home buyers facing affordability challenges in Auckland’s competitive market.

Key assistance options include:

- Kāinga Ora First Home Loan requiring only 5% deposit with income limits of $95,000 for individuals or $150,000 for couples

- KiwiSaver members can withdraw savings after three years’ contributions, leaving $1,000 minimum balance

- First Home Grant providing up to $5,000 for individuals or $10,000 for couples meeting eligibility criteria

- Welcome Home Loan available through selected lenders for buyers meeting income and price caps

Low deposit loans typically require lender’s mortgage insurance protecting lenders against default risk. Lender’s Mortgage Insurance is typically 1.2% of the loan and may be added to the loan or paid upfront. While this increases overall borrowing costs, it enables market entry years earlier than saving a full 20% deposit.

Eligibility criteria vary by scheme. Kāinga Ora assesses income levels, property prices, and whether applicants have owned homes previously. KiwiSaver withdrawals require three consecutive years of contributions with special provisions for earlier access in hardship cases.

Government schemes dramatically reduce deposit barriers, but understanding eligibility criteria and associated costs ensures realistic planning and prevents application disappointments.

Explore Kāinga Ora First Home Loan options in detail and check low deposit lenders to compare available programmes and requirements.

Step 5: common pitfalls and mistakes to avoid

Many applications fail due to preventable errors. Incomplete income documents and poor credit history are leading causes of application delays and declines. Understanding frequent mistakes helps you avoid them and increases approval chances significantly.

Common application errors include:

- Submitting inconsistent or incomplete income documentation that raises verification questions

- Making large purchases or opening new credit accounts during application processing

- Failing to disclose all income sources including gifts, side jobs, or rental income

- Ignoring credit report errors that negatively impact credit scores and lending decisions

- Overstating affordability by underreporting regular expenses like subscriptions or lifestyle costs

Lenders verify every claim meticulously. Inconsistencies between payslips, tax returns, and bank statements trigger automatic reviews and delays. Gift deposits require formal letters stating funds are non-repayable; vague explanations cause problems.

Timing matters significantly. Avoid changing jobs during application processing unless absolutely necessary. Employment changes require additional verification and may reset assessment timelines. Similarly, major purchases like cars or furniture deplete savings lenders expect you to maintain post-settlement.

Pro Tip: Review your credit report three months before applying and dispute errors immediately. Credit reporting agencies take weeks to investigate and correct mistakes, so early action prevents last-minute complications.

Transparency throughout the process builds lender confidence. When uncertain about whether to disclose information, always err on the side of full disclosure. Read mortgage application tips for detailed guidance on avoiding common mistakes.

Step 6: expected timelines, fees, and final approval

Understanding processing timelines and costs helps manage expectations and plan finances accurately. Typical application processing takes 3 to 7 days; lender’s mortgage insurance costs approximately 1.2% of loan if deposit is low. These timeframes assume complete documentation and straightforward financial situations.

Typical mortgage timeline stages:

- Application submission and initial review taking 1 to 2 business days

- Property valuation arranged by lender within 2 to 3 business days

- Formal assessment and credit checks spanning 2 to 4 business days

- Conditional approval issued with outstanding requirements listed

- Final approval granted once all conditions satisfied, usually within 1 to 2 days

- Settlement scheduled typically 4 to 6 weeks after unconditional offer acceptance

Pre-approvals remain valid for three to six months. If property searches extend beyond this period, renewal applications require updated documentation and reassessment. Market conditions and lending criteria may shift during extended searches, potentially affecting borrowing capacity.

Key fees and costs to budget include:

| Fee Type | Typical Cost | When Payable | Notes |

|---|---|---|---|

| Lender’s mortgage insurance | 1.2% of loan amount | Settlement or added to loan | Required for deposits under 20% |

| Property valuation | $300 to $600 | During application | Paid upfront, varies by property |

| Legal fees | $1,500 to $3,000 | Settlement | Covers conveyancing and searches |

| Building inspection | $400 to $800 | Pre-purchase | Optional but highly recommended |

Final approval depends on satisfying all lender conditions. These typically include satisfactory property valuation, confirmation employment hasn’t changed, and no significant financial status shifts since pre-approval. Understanding the complete mortgage application steps ensures realistic timeline expectations.

Talk to Auckland mortgage brokers that can help

Securing your first Auckland mortgage becomes significantly easier with expert guidance. Our Auckland mortgage brokers specialise in helping first home buyers navigate complex lending requirements and find suitable loan products.

Mortgage brokers handle application complexities, compare multiple lenders simultaneously, and negotiate terms on your behalf. They understand nuances of government schemes like Kāinga Ora First Home Loan assistance and can match your circumstances to lenders most likely to approve your application. Using personal mortgage advisers saves countless hours of research and potentially secures better interest rates through lender relationships.

Our Auckland-based team understands local market conditions and maintains strong relationships with major banks and specialist lenders. Whether you’re working with a modest deposit, navigating credit challenges, or simply want expert guidance through your first purchase, professional mortgage advice transforms the experience from overwhelming to manageable.

Frequently asked questions

What income documents are required for mortgage applications?

Lenders typically require three months of recent payslips, proof of employment, and bank statements covering the same period. Self-employed applicants must provide two years of tax returns, financial statements, and evidence of business stability. Additional income sources like rental income or side jobs require supporting documentation.

Can I use KiwiSaver savings for my first home deposit?

Yes, you can withdraw KiwiSaver funds for your first home after making contributions for at least three years. You must leave a minimum balance of $1,000 in your account. The withdrawal applies to deposits only, not other purchase costs like legal fees or moving expenses.

How long does mortgage pre-approval last?

Pre-approval typically remains valid for three to six months depending on the lender. If you don’t find a property within this timeframe, you’ll need to reapply with updated documentation. Lenders reassess your financial situation and may adjust borrowing capacity based on any changes to income, debts, or lending criteria.

What if my credit history is poor?

Poor credit history doesn’t automatically disqualify you, but it limits options and may result in higher interest rates. Focus on correcting credit report errors, paying down existing debts, and demonstrating stable income. Some specialist lenders cater specifically to borrowers with credit challenges, though they charge premium rates.

Are mortgage brokers free to use?

Most mortgage brokers receive commission from lenders when loans settle, meaning no direct cost to you. Some brokers charge fees for complex situations or when applications require extensive work. Always clarify fee structures upfront, as reputable brokers disclose all costs transparently before beginning work on your application.