TL;DR:

- Bridging finance is a short-term loan covering the gap between buying and selling properties.

- It involves higher interest rates and costs, requiring careful planning and backup strategies.

- Expert advice and early planning are essential for using bridging finance safely and effectively.

Many Kiwi homebuyers assume that buying a new property while selling their existing one is simply a matter of timing things perfectly. The reality is far messier. Settlement dates clash, auction deadlines don’t wait, and standard home loans simply aren’t built to carry you through the financial gap between owning two properties at once. Bridging finance exists precisely for this moment, yet it remains one of the most misunderstood tools in the New Zealand property market. By the end of this guide, you’ll know exactly how it works, what it costs, and how to use it wisely.

Table of Contents

- What is bridging finance?

- When do homebuyers in NZ use bridging finance?

- Costs, rates and risks: What you really pay

- How to approach bridging finance safely

- Why most buyers misunderstand bridging finance (and what to do instead)

- Where to get help with bridging finance in New Zealand

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Bridging finance basics | Bridging finance helps cover the gap when buying a new home before your old one is sold. |

| Costs and risks | Bridging loans are usually more expensive and carry the risk of paying two loans if your sale is delayed. |

| Broker guidance essential | Consult a mortgage adviser early to avoid costly mistakes and develop a safe bridging finance strategy. |

| Backup plans | Always have an exit strategy in case your property doesn’t sell as expected. |

What is bridging finance?

To understand why bridging finance matters, let’s break down what it actually is and who uses it.

Bridging finance is a short-term loan designed to “bridge” the financial gap between purchasing a new property and receiving the proceeds from selling your existing one. Think of it as a temporary financial runway that keeps you moving forward when the timing between buying and selling doesn’t line up neatly. It’s not a permanent solution, and it’s not meant to be. It’s a structured tool for a specific, time-limited situation.

Here’s how it typically works in practice. You find a property you want to buy, but your current home hasn’t sold yet. Rather than losing the opportunity, you take out a bridging loan to cover the purchase. Once your existing property sells, the proceeds pay down the bridging loan, and you’re left with a standard mortgage on your new home.

When it comes to how bridging loans work, the key features are:

- Interest-only repayments during the bridging period, meaning you’re not paying down principal

- Floating interest rates rather than fixed, which means your rate can shift during the loan term

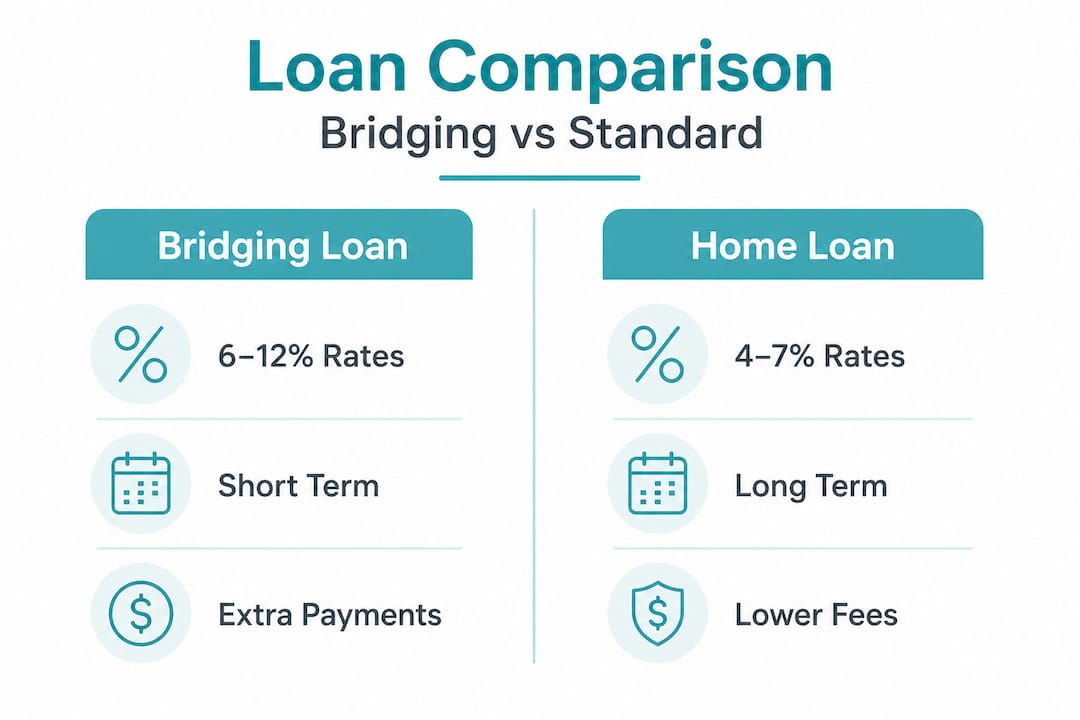

- Higher rates than standard home loans, with bridging rates ranging from 6% to 10% per annum for most banks, and up to 11.95% p.a. for some non-bank lenders, often sitting around 1.5% above standard floating rates

- Short loan terms, typically from a few weeks up to 12 months

In New Zealand, both banks and non-bank lenders offer bridging loans. Banks tend to have stricter lending criteria but may offer slightly lower rates. Non-bank lenders are often more flexible, particularly if your situation is complex or your timeline is tight. Knowing which type of lender suits your circumstances is where expert guidance becomes genuinely valuable.

Pro Tip: Don’t assume your existing bank will automatically approve a bridging loan. Their criteria can be quite strict, and a mortgage adviser can often find a better-suited lender for your specific situation.

When do homebuyers in NZ use bridging finance?

Now that you know what bridging finance is, it helps to see the specific situations where Kiwi homebuyers turn to it.

The most common scenarios include:

- Buying before selling: You’ve found your dream home and can’t afford to wait. You need to secure it now, even though your current property is still on the market.

- Auction purchases: Auctions require unconditional offers and fast settlement. If your sale hasn’t completed, bridging finance fills the gap.

- Tight or mismatched settlement dates: Your new purchase settles in three weeks, but your existing home doesn’t settle for another six. Bridging finance covers that window.

- New build completions: Sometimes a new build finishes earlier than expected, and you need funds before your existing property is sold.

- Renovation or holding strategies: Less common, but some buyers use bridging finance to hold a property while completing work before selling.

To illustrate this with a real-world example: imagine a family in West Auckland who finds a larger home that suits their growing needs. They make an offer, it’s accepted, and settlement is in 45 days. Their existing home is listed but hasn’t sold. A bridging loan allows them to settle on the new property, move in, and continue marketing the old one. When it sells eight weeks later, the bridging loan is repaid and they transition to a standard mortgage.

Here’s a quick comparison of bridging finance versus waiting to sell first:

| Scenario | Bridging finance | Selling first |

|---|---|---|

| Speed to purchase | Fast, no delay | Slower, conditional on sale |

| Risk of missing property | Low | High |

| Financial pressure | Higher (dual costs) | Lower |

| Flexibility | High | Limited |

| Ideal for | Competitive markets | Slower markets |

The risks of carrying two loans simultaneously are real. You’re managing repayments on both your existing mortgage and the bridging loan at the same time. This puts pressure on your monthly cash flow and your overall financial resilience. If your property takes longer to sell than expected, those costs compound quickly.

Expert guidance strongly recommends consulting a broker before committing to any purchase that relies on bridging finance. Backup plans are essential, because bridging finance is an expensive short-term tool that isn’t right for everyone, particularly given the dual costs and uncertainties around sale timelines.

Understanding the reasons to use a mortgage broker becomes especially clear in these situations. A broker doesn’t just find you a loan; they help you stress-test your plan before you’re committed to it. For buyers navigating complicated mortgage situations, this kind of structured support is genuinely a game-changer.

Costs, rates and risks: What you really pay

Having identified when bridging finance may apply, let’s examine what it costs and the financial risks you need to know.

Bridging loans are priced differently from standard home loans, and the difference matters. Because they’re on floating rates with a premium above standard floating rates, typically around 1.5%, the effective rate can sit anywhere from 6% to 11.95% per annum depending on the lender and your profile. This is meaningfully higher than the fixed rates many Kiwi homeowners are used to.

To put this into concrete terms, here’s what a $500,000 bridging loan might cost you across different timeframes at an 8% interest rate (interest-only):

| Loan term | Monthly interest cost | Total interest paid |

|---|---|---|

| 3 months | $3,333 | $10,000 |

| 6 months | $3,333 | $20,000 |

| 9 months | $3,333 | $30,000 |

| 12 months | $3,333 | $40,000 |

These figures don’t include your existing mortgage repayments, legal fees, or lender establishment fees, which can add several thousand dollars to the total cost. Use a mortgage payment calculator to model your specific numbers before committing.

Key insight: The longer your bridging period, the more expensive it becomes. Every additional month adds thousands of dollars in interest. Speed of sale is not just convenient, it’s financially critical.

Beyond the interest rate, the full cost picture includes:

- Lender establishment fees, often ranging from $500 to $2,000 or more

- Legal costs for both the purchase and the bridging loan documentation

- Valuation fees on both properties

- Ongoing holding costs such as rates, insurance, and maintenance on two properties simultaneously

Understanding the impact of interest rates on your overall borrowing position is crucial here. Even a modest rate premium compounds significantly over a six to twelve month bridging period.

The biggest risk in bridging finance is straightforward but often underestimated: what happens if your existing property doesn’t sell as planned? In a slower market, or if your property receives lower offers than expected, you could be stuck with two loans for longer than anticipated. Your bridging loan term may need to be extended, often at additional cost, or you may need to refinance urgently. This is why having a backup strategy is not optional; it’s essential.

Working with non-bank lenders can sometimes provide more flexibility in these situations, but their rates tend to be higher. It’s a trade-off between flexibility and cost that your adviser can help you navigate. And when you’re ready to transition out of bridging finance into a standard mortgage, knowing how to compare home loans properly will save you money in the long run.

How to approach bridging finance safely

Understanding the costs and risks is crucial, but using bridging finance responsibly makes all the difference.

Here’s a step-by-step approach to using bridging finance safely:

- Review your financial position honestly. Before anything else, calculate your cash flow under a worst-case scenario. What if your property takes three months longer to sell than you expect? Can you still meet all repayments?

- Get a realistic market appraisal. Have your existing property appraised by at least two agents before committing to a purchase. Overestimating your sale price is one of the most common and costly mistakes.

- Speak to a mortgage adviser before you make an offer. Not after. Before. This is the single most important step, because your adviser can structure the loan correctly from the outset and identify any red flags.

- Understand your lender’s bridging loan terms in detail. Know the maximum loan term, the rate, the fees, and what happens if you need an extension.

- Have a documented backup plan. What will you do if the property doesn’t sell within your expected timeframe? Could you rent it out temporarily? Could you reduce the asking price? These aren’t pessimistic questions; they’re responsible ones.

- Consider the full cost, not just the interest rate. Factor in all fees, legal costs, and holding costs before deciding whether bridging finance is the right move for your situation.

Expert advice is clear on this point: bridging finance is an expensive short-term tool that requires backup plans and broker consultation before purchase. It’s not a fallback; it’s a structured financial strategy.

Checklist for safe bridging finance use:

- Financial position reviewed and stress-tested

- Realistic property valuation obtained

- Mortgage adviser consulted before making an offer

- Full cost breakdown calculated including fees and holding costs

- Backup plan documented and discussed with your adviser

- Lender terms understood in full

Pro Tip: If you’re worried about the cost of bridging finance, explore whether extra mortgage payments on your existing loan before the bridging period could reduce your overall debt load and ease the transition.

Accessing home loan options banks can’t always offer is another reason to work with an independent adviser. They can access a broader panel of lenders and structure your bridging arrangement in ways that a single bank simply cannot. And once you’re through the bridging period, your adviser can help you secure better home loan rates on your long-term mortgage.

Why most buyers misunderstand bridging finance (and what to do instead)

After covering all angles of bridging finance, it’s time for a straight-talking take on what buyers usually overlook.

Here’s the uncomfortable truth: most Kiwi buyers treat bridging finance as a safety net rather than a strategy. They assume that if things get complicated, they’ll “just get a bridging loan” and sort it out later. This mindset is precisely what leads to financial stress, unexpected costs, and rushed decisions.

Bridging finance is not a fallback. It’s a precision tool. Used correctly, with clear timelines, a realistic sale price, and a structured exit plan, it genuinely enables buyers to move confidently in competitive markets. Used carelessly, it can turn a promising property purchase into a prolonged financial burden.

The hidden advantage that most buyers miss is this: the conversation with your mortgage adviser should happen before you start seriously looking at properties, not after you’ve fallen in love with one. When you understand your bridging capacity early, you can bid at auction with confidence, make unconditional offers strategically, and negotiate from a position of strength rather than desperation.

New Zealand’s property market has its own rhythms. In Auckland particularly, properties can move quickly in some suburbs and sit for months in others. Your bridging strategy needs to account for the specific market dynamics of the suburb you’re selling in, not just the one you’re buying in. A good adviser who knows the local market is genuinely invaluable here.

The lesson from buyers who’ve navigated bridging loans in NZ successfully is consistent: they planned early, consulted experts before committing, and treated the bridging period as a defined, temporary phase with a clear endpoint. Those who struggled did the opposite. They improvised, underestimated costs, and hoped timing would work itself out.

Don’t leave your property transition to hope. Build a plan instead.

Where to get help with bridging finance in New Zealand

If you’re considering bridging finance, it pays to reach out for tailored advice. Here’s where to start.

Navigating bridging finance on your own is possible, but it’s a bit like navigating Auckland without a map. You might get there eventually, but you’ll likely take a few wrong turns along the way. Working with personal mortgage advisers means you have someone in your corner who understands the full landscape, from lender criteria to rate negotiations to structuring your exit strategy.

At Mortgage Managers, we’re a locally owned and operated team of Auckland mortgage advisers based in Hobsonville. We work with buyers across West Auckland, the North Shore, and throughout New Zealand remotely. Whether you’re buying your first home, upsizing, or managing a complex property transition, our advisers can assess your bridging finance options and build a strategy that suits your specific situation. Visit Mortgage Managers to get started with a conversation that could save you thousands and a great deal of stress.

Frequently asked questions

How long can you get a bridging loan in New Zealand?

Most bridging loans in NZ last from a few weeks up to 12 months, though shorter terms are far more common and interest accrues throughout the entire bridging period, making a swift sale financially important.

Do bridging loans require payments on both homes?

Yes, during the bridging period you’ll typically make interest payments on both your existing mortgage and the bridging loan, which creates short-term dual costs that can significantly increase your monthly financial commitments until the sale settles.

Are bridging loans more expensive than regular home loans?

Bridging loans carry higher interest rates than standard home loans, with floating rates ranging from 6% to 11.95% per annum, often sitting around 1.5% above what you’d pay on a typical fixed-rate mortgage.

What happens if I don’t sell my current house in time?

If your property doesn’t sell within the bridging loan term, you may face extension fees, higher holding costs, or the need to refinance urgently, which is why backup plans are essential and expert advice before committing is so important.