TL;DR:

- Nearly 12% of New Zealanders are in credit arrears, affecting mortgage eligibility.

- Negative credit events include defaults, court judgments, and insolvencies, staying on reports for up to 5 years.

- While a default impacts home loan chances, specialist lenders may offer options if recent and settled.

Nearly 12% of credit-active New Zealanders are currently in arrears, yet a surprising number of people have no clear idea what actually counts as a negative credit event, or what it means for their chances of owning a home. If you’ve missed payments, faced a debt collection notice, or wondered why a lender turned you away, you’re not alone. This guide will walk you through exactly what negative credit events are in a New Zealand context, how they affect your home loan eligibility, and the practical steps you can take to move forward with confidence.

Table of Contents

- What are negative credit events in New Zealand?

- How negative credit events affect home loan eligibility

- Trends and statistics: Negative credit events in New Zealand

- Recovering from negative credit events: Steps and strategies

- Our perspective: What most Kiwis miss about negative credit events

- How we can help with negative credit events

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Types of negative events | Defaults, court judgments, insolvencies, and debt repayment orders all count as negative credit events in New Zealand. |

| Impact on home loans | Negative events remain visible for four to five years and can limit home loan approval, but specialist options exist. |

| Steps to recover | Checking your credit report, settling debts, and demonstrating positive behaviour can help you recover. |

| Current trends | Over 11% of credit-active New Zealanders are in arrears, so you are not alone in facing these challenges. |

What are negative credit events in New Zealand?

Now that you understand why this matters, let’s define exactly what negative credit events are in a New Zealand context. A negative credit event is any recorded incident on your credit file that signals to lenders you’ve had difficulty meeting financial obligations in the past. These events are logged by credit reporting agencies such as Centrix, Equifax, and illion, and they can significantly shape how lenders perceive your application.

According to Centrix’s credit file guide, negative credit events include credit defaults, court judgments, insolvencies, and debt repayment orders. Each of these carries its own weight and duration on your credit report.

Here’s a clear summary of the main event types, what they mean, and how long they stay on your file:

| Event type | What it means | How long it stays on your file |

|---|---|---|

| Credit default | A debt that went unpaid after the lender made contact | 5 years from date of default |

| Court judgment | A court-ordered debt repayment | 5 years from date of judgment |

| Insolvency (bankruptcy) | A formal legal process for unmanageable debt | 4 years from date of discharge |

| No asset procedure (NAP) | A simplified insolvency for those with no assets | 4 years from date of discharge |

| Debt repayment order | A court-managed repayment plan | 4 years from completion |

Understanding these categories is the first step toward taking control. Each event tells a different story to a lender, and knowing which applies to you helps you respond strategically.

Here’s what each event can mean for your day-to-day financial life:

- Credit default: You may struggle to open new credit accounts, get mobile phone contracts, or rent a property.

- Court judgment: Lenders view this as a serious red flag, and it can affect your ability to access credit for the full five-year period.

- Insolvency: This is the most severe event and typically prevents standard bank lending until discharge and often beyond.

- Debt repayment order: While less severe than bankruptcy, it still signals significant financial difficulty to lenders.

Pro Tip: You’re entitled to request a free copy of your credit report from any of New Zealand’s credit reporting agencies. Make a habit of monitoring your credit at least once a year so you’re never caught off guard by what’s on your file.

How negative credit events affect home loan eligibility

Knowing what negative credit events are is one thing. Understanding how they influence your lending options is another. The impact on your home loan application depends on the type of event, how recent it is, whether it’s been paid or resolved, and which type of lender you approach.

As Centrix confirms, defaults stay on your credit file for 5 years even if paid, court judgments remain for 5 years, and insolvencies for 4 years from discharge. This means the event doesn’t disappear the moment you settle the debt. It stays visible, though it can be marked as paid, which does make a difference.

Here’s how different lenders typically respond to each event type:

| Event type | Main bank reaction | Specialist lender reaction | Non-bank lender reaction |

|---|---|---|---|

| Paid default (minor) | Likely declined | May consider with conditions | Often willing to assess |

| Unpaid default | Almost always declined | Assessed case by case | May consider with higher rate |

| Court judgment (resolved) | Likely declined | May consider after 2+ years | Often willing with explanation |

| Insolvency (discharged) | Declined until clear | Assessed after discharge | May consider with strong deposit |

| Debt repayment order | Likely declined | May consider after completion | Assessed individually |

The gap between what a main bank will accept and what a specialist lender will consider is significant. If you’ve been turned away by a bank, that doesn’t mean the door is closed entirely. Exploring mortgage options with credit defaults through a specialist lender or non-bank lender can open up paths that most people don’t realise exist.

When assessing your application after a negative credit event, lenders typically look for the following:

- Time elapsed since the event: The older the event, the less weight it carries. Lenders feel more confident when a negative event is two or more years in the past.

- Whether the debt has been settled: A paid default is viewed more favourably than an unpaid one, even though both remain on your file.

- Stability of income: Consistent, verifiable income reassures lenders that past difficulties are behind you.

- Deposit size: A larger deposit reduces the lender’s risk and can tip the balance in your favour.

- Overall credit behaviour since the event: New positive credit activity, such as on-time payments and responsible credit use, demonstrates recovery.

Pro Tip: When qualifying for a mortgage with defaults, prepare a brief written explanation of what caused the negative event and what you’ve done since to address it. Lenders respond well to transparency and accountability.

Trends and statistics: Negative credit events in New Zealand

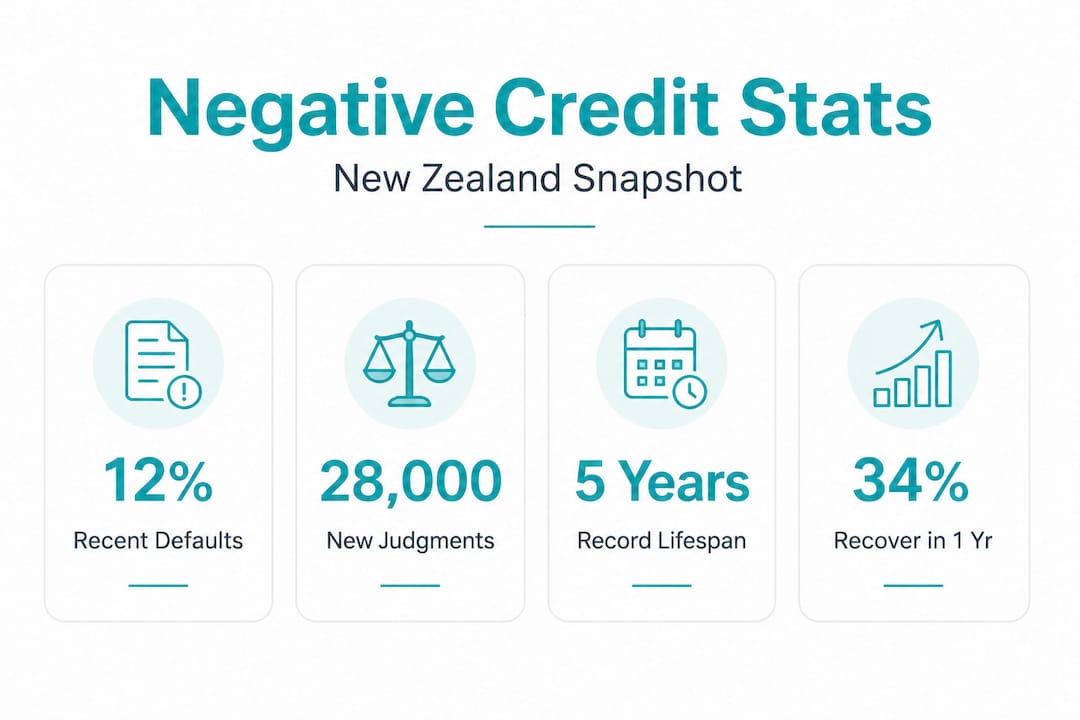

To show how common these issues are, let’s look at the latest data on negative credit events and defaults in New Zealand. The numbers paint a picture that’s both sobering and reassuring. Sobering because the scale is significant. Reassuring because it confirms you’re far from alone.

The November 2025 Centrix data shows that consumer arrears sat at 11.83%, mortgage arrears were at 1.35%, and consumer defaults were up 4% year-on-year but showing signs of stabilising. Here’s a snapshot of the key figures:

| Indicator | November 2025 figure | Year-on-year change |

|---|---|---|

| Consumer arrears rate | 11.83% | Elevated but stabilising |

| Mortgage arrears rate | 1.35% | Slight increase |

| Consumer defaults | Up 4% YoY | Stabilising trend |

Nearly 1 in 8 credit-active New Zealanders is currently in arrears. If you’re among them, you’re navigating a challenge that hundreds of thousands of Kiwis are facing right now.

These numbers matter for anyone seeking a home loan. Here’s what they imply for the average applicant:

- Lenders are seeing more applications with credit issues, which means specialist lenders are increasingly experienced in assessing complex cases.

- Stabilising default rates suggest the worst of recent economic pressure may be easing, which could translate into more flexible lending conditions over time.

- Mortgage arrears remain relatively low at 1.35%, meaning most homeowners are managing their repayments, which can work in your favour if you can demonstrate similar stability.

- The volume of affected Kiwis means there is growing demand for, and availability of, products designed for people with imperfect credit histories.

Understanding the broader landscape helps you see your situation in context. The mortgage defaults explained resource on our website can help you understand how these trends affect your specific circumstances. And if you’re actively working toward a home loan, knowing that specialist lenders are well-versed in qualifying with adverse credit is genuinely encouraging.

Recovering from negative credit events: Steps and strategies

If you’ve experienced a negative credit event, there are tangible steps you can take to recover and improve your chances with lenders. Recovery isn’t instant, but it is absolutely achievable. The key is being methodical and consistent.

As the Centrix November 2025 report confirms, defaults and negative events remain visible for up to 5 years, with some insolvency-related events clearing after 4 years. But being marked as paid changes how lenders interpret what they see. Action matters.

Here are the core steps to take after a negative credit event:

- Check your credit report immediately. Request a free copy from Centrix, Equifax, or illion. Confirm that all information is accurate and identify every negative item listed.

- Settle any outstanding debts. Even if a default remains on your file, paying it off allows it to be marked as paid, which signals responsibility to lenders.

- Contact the creditor to update the record. Once a debt is paid, ask the creditor to notify the credit reporting agency so the status is updated promptly.

- Demonstrate consistent positive financial behaviour. Pay all current bills on time, every time. Avoid applying for multiple credit products in a short period, as each application leaves a footprint on your file.

- Seek advice from a mortgage adviser. A specialist adviser can assess your specific situation and identify lenders who are genuinely open to your circumstances.

The path to rebuilding credit for a mortgage is rarely a straight line, but every positive step you take builds the case for a lender to say yes. There are also bad credit home loan options available right now, even if your credit file isn’t perfect yet.

Pro Tip: When applying for a home loan with a negative credit event on your file, include a brief cover letter with your application. Explain the circumstances clearly and factually, describe what you’ve done to resolve the situation, and highlight the positive financial steps you’ve taken since. This kind of transparency can be a real turning point in how a lender views your application.

Ongoing habits that protect and improve your credit standing include:

- Paying bills before the due date, not just on the due date, to avoid any processing delays that could register as late.

- Keeping credit card balances low relative to your credit limit, ideally below 30% of the available limit.

- Avoiding unnecessary credit applications, especially in the months leading up to a home loan application.

- Reviewing your credit file annually to catch any errors or unexpected entries early.

- Building savings consistently, even in small amounts, to demonstrate financial discipline to lenders.

These habits, practised over time, can meaningfully improve your home loan eligibility even while a negative event is still technically on your file.

Our perspective: What most Kiwis miss about negative credit events

Beyond the technical details, our experience working with clients reveals a few hidden truths about negative credit events that most people simply don’t know.

The biggest misconception we encounter is that a negative credit event is a permanent verdict. It isn’t. It’s a chapter in your financial story, not the whole book. We’ve worked with clients who assumed they’d never qualify for a mortgage because of a default from several years ago, only to find that a specialist lender was genuinely willing to assess their application based on the full picture of their finances.

What most people overlook is the power of documentation and transparency. Lenders aren’t just looking at numbers. They’re assessing risk, and a well-documented explanation of what happened, paired with evidence of recovery, can shift that risk assessment meaningfully. Gathering bank statements, proof of settled debts, and a clear written account of your circumstances is often the difference between an approval and a decline.

Another truth that surprises many clients is that consistency in positive financial behaviour often carries more weight than a single negative event, particularly as time passes. A lender reviewing your application two or three years after a default will look at everything that’s happened since. If that period shows steady income, on-time payments, and responsible credit use, the negative event begins to fade into the background of the story.

Our strong advice is to seek guidance early, before you apply. Exploring adverse credit mortgage options with a specialist adviser means you approach lenders strategically, not speculatively. Going to the right lender with the right preparation is far more effective than applying broadly and collecting declines, which themselves can further affect your credit file.

How we can help with negative credit events

If you’re ready to explore your home loan options after a negative credit event, here’s how we can help. At Mortgage Managers, we work with Kiwis across Auckland and throughout New Zealand who are navigating exactly these kinds of challenges. We know which lenders are genuinely open to complex credit histories, and we know how to present your application in the strongest possible light.

Our home loan experts take the time to understand your full financial picture before recommending any course of action. We’re not here to judge your past. We’re here to help you build your future. Whether you’re dealing with a paid default, a discharged insolvency, or a court judgment that’s a few years old, there may be more options available to you than you think. Reach out to our team today and let’s look at your situation together. Our adverse credit mortgage help service is designed for people exactly like you.

Frequently asked questions

How long do defaults stay on my credit file in New Zealand?

Defaults remain on your credit report for five years from the date of default, even if you pay them off before that period ends.

What counts as a negative credit event for home loan applications?

In New Zealand, negative credit events include defaults, court judgments, insolvencies such as bankruptcy, no asset procedures, and debt repayment orders.

Can I still get a mortgage after a negative credit event?

Yes, specialist lenders and experienced mortgage advisers offer home loan products specifically for applicants with poor or complex credit histories, so a negative event doesn’t automatically close the door.

Do paid defaults improve my ability to get a home loan?

Paid defaults are marked as such on your credit file and are viewed more favourably by lenders, though they still remain visible for the full five-year period from the date of default.