A lot of Kiwis have not heard of the co ownership concept with property, but it’s quite common in other places and is becoming more popular here too.

The concept of co-ownership provides a way to buy into your first home when your deposit is less than what the banks will accept.

Traditionally you may have entered into a co-ownership agreement with a family member (typically a parent) where the other party may have the equity to enable you to buy a property, and their reward is to share in the gain of the value.

As New Zealand mortgage advisers we have been helping people get into their first home using this option, but often a family member is not able to assist so the good news is shared ownership can now be sourced from companies that offer this as a financial product … a formal co ownership agreement.

Key Features For Qualification

Firstly you probably want to know if you qualify.

The criteria is easier than what the banks apply for low deposit lending.

The key criteria is;

-

- You must have a minimum of 5% deposit – this can include your KiwiSaver withdrawal, any First Home Grant and of course any savings that you have. You can have some gifted deposit too, but they really want to see that you have been able to save your deposit yourself.

- You need to be able to afford the repayments – your adviser can help with working this out. The funding is done with a non-bank lender and therefore the criteria is not as tough as the banks, but there is still a responsibility to ensure that you can afford the repayments. Of course this will be important to you as well.

- You can have some blemishes on your credit check and other debts too, but these are assessed on a case by case basis. The adviser will be able to help present this to the lender and we have had good success with some poor credit, poor account conduct and people with quite a lot of short-term debt.

Your application will need to be assessed before an approval can be given, but the criteria is not as difficult as many people think.

How Do The Numbers Work For Co-Ownership?

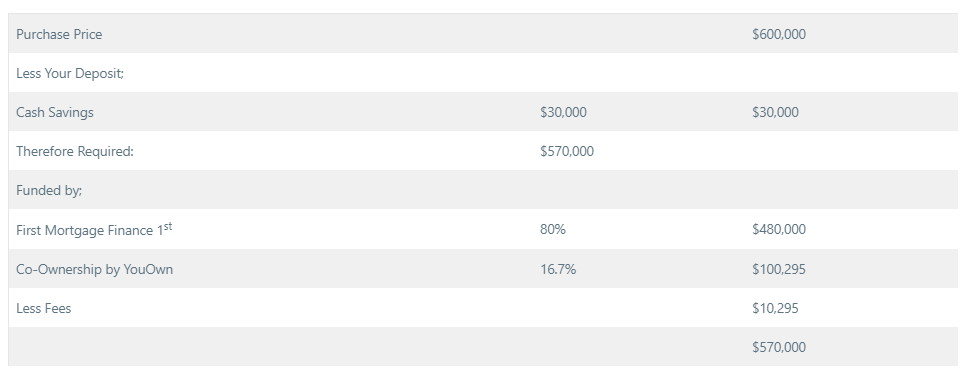

To show you how the numbers work we have used a real example here – this is a scenario that we sent to someone recently who only had a 5% ($30,000) deposit but wanted to buy their first home.

So you have a deposit of $30,000 and therefore with borrowing of 95% you could purchase for $600,000

Unfortunately at the moment the banks and even non-banks are not lending to 95% but we have an option with one lender and shared ownership.

This is how the finances work;

This is funded using a 1st mortgage provided by a non-bank mortgage provider and a co-ownership by YouOwn.

The interest rate for the non-bank mortgage provider is about 6.75% and YouOwn have an equity charge of 4.95%

That means the repayments will be approx. $815 per week.

This is made up of the non-bank mortgage provider at approx. $720 weekly and YouOwn at $95 weekly.

Like any first home buyer you need to consider the costs of home ownership and balance this with the desire to have your own home.

Let’s Compare To Bank Funding?

Let’s compare to what a bank could offer, if only they could approve the loan.

- ASB currently have a 2-year rate of 2.69% (as at 16th October 2020) plus add a low equity margin of 1.30% so if you chose this fixed term you would be paying 3.99%

- The repayments for a 95% loan ($570,000) would be approx. $630 per week.

Bank finance is the cheapest option.

The problem is the bank criteria can be quite difficult, especially if you do not have a large deposit or if you have other debt.

Co-Ownership Is More Expensive … BUT

As you can see the co-ownership concept that we have provided will be more expensive than what a bank could offer, but it is a solution.

If a bank will approve your home loan then that should be the preferred option.

You could always speak to a non bank broker too and see what other options might be available too.

The co ownership concept is often the best option when you have a smaller deposit, and it may be your only viable option.

Compare this to waiting and saving, especially with house prices increasing as they are.

When You Want 100% Ownership

Also you need to be aware that with co-ownership you will want to buy the remaining share from YouOwn in the future.

This is generally done after 5-years, and they make their money from the expected increase in value.

In this scenario they have a 16.7% share of the property worth $600,000 so YouOwn’s share = $100,295

If the value of the property is worth ‘say’ $800,000 in 5-years then the YouOwn share is now worth $133,600 (16.7%) so an increase of $33,305

Of course your share (83.3%) has increased by $166,600 too!

Co-Ownership May Be A Good Option For You

If you can get a mortgage with a bank or a non bank lender then that is most likely going to be your best option; however in many cases this is not possible.

There are four main reasons for this;

- You Have A Low Deposit – if you have not been able to save a big enough deposit then the banks and non-bank lender might not be prepared to give you a mortgage.

It’s Hard to Prove All Your Income – the banks criteria for proving income can be tough especially for self-employed people. Some non banks are better but they tend to require a larger deposit which you may not have. - Too Much Short-Term Debt – the banks do not like to see too much short term debt when they are assessing an application. You may have great repayment history and be quite okay with affording the payments, but the banks have rules on how much debt you can have and they also need to factor on those repayments plus the new mortgage repayments. We can sometimes consolidate some debts into the mortgage when we do co-ownership arrangements, depending on the deposit that you have available from your KiwiSaver, any First Home Grant and of course your savings too.

- Some Credit Issues – sometimes past credit issues will mean that the banks cannot approve your mortgage. Again, some non bank lenders are not quite so strict, but they will still need your application presented to them well.

Banks are not looking to provide finance for everyone, and if you don’t fit the standard criteria then they may very likely say “no” to you.

You may be quite comfortable with the repayments and they may even be comparable to the rent that you are paying too. Owning a house is not always more expensive than renting, but many people may struggle to meet the banks criteria.

Around the world these types of arrangements have been quite popular. In the UK they have had shared ownership schemes for some time now. These are Government backed schemes and they have helped a lot of first home buyers there. READ HERE about what they offer in the UK.

They are not a new concept at all.

Co-Ownership Is Just One More Option

As mortgage advisers we know that this is not the best option for all people, but it is a viable option that can help people get into a home where otherwise they may need to save for another year or two.

Waiting and watching the house values increasing can be frustrating too.

It may be smarter for first home buyers to get on the property ladders sooner.

Often the values will increase at a faster rate than you could save!

That’s when you really do see the value in buying a home with a co-ownership arrangement.

It may allow you to buy into the market now at the current house prices. Using the example about you are taking most of the ownership, but getting help with 16.7%.

You can live in the house and treat it as your own.

By agreement you are able to buy that 16.7% share at a later date when you are in a better financial position, and of course when the value has increased your equity in the house which allows you to get a good bank mortgage at lower interest rates.

You have missed out on the increased value on the 16.7% share, but you have got the gains from the 83.3%.

Speak To An Adviser To See If This Could Work For You

The best thing to do is to contact an adviser that can look at this for you.

Very few New Zealand mortgage advisers have the knowledge and access to this co ownership concept, but the team at Mortgage Managers can help.

What is the difference between joint and co ownership?

In simplistic terms Joint owners is when two people have equal (or sometimes unequal) ownership in a property. This is most often spouses or partners, but it’s now common for the extended family with parents and children. The term “co-ownership” is used in property where that another person or entity has ownership of a percentage of the property and with residential property that may be a company or Government entity that holds a smaller ownership to assist in particular first home buyers to enable then to purchase a home.

What is co ownership of a house?

Co-ownership of a house generally means you are buying your house with someone else. This is an alternative way of buying a house when traditional options are not available to you. Instead of owning 100% of your home, you may be able to own 75% or 85% of the property with a mortgage, but have a shortfall meaning you cannot buy 100% at this stage. Instead you have a co owner that provides the extra equity and for that you pay a monthly equity fee to that third party. You can buy the co owners share of the house at a later time when you can afford it, and then take full 100% ownership.