TL;DR:

- A second mortgage is a loan secured against a property with an existing mortgage, allowing access to home equity without refinancing. It ranks behind the first mortgage and involves higher interest rates due to increased risk. Borrowers should carefully compare options, understand the risks, and work with advisers to make confident decisions.

A second mortgage is a loan secured against a property that already has an existing mortgage, giving you access to your home equity without replacing your original loan. The second mortgage sits behind your first mortgage in priority order, which is why lenders charge a higher interest rate to offset their increased risk. For New Zealand homeowners and property investors, this structure creates a practical way to fund renovations, consolidate debt, or finance an investment without disturbing a favourable first mortgage rate. Understanding the mechanics, costs, and risks upfront is the clearest path to making a confident borrowing decision.

How does a second mortgage work in New Zealand?

A second mortgage works by placing a second lien on your property, ranking behind your first mortgage in repayment priority. If you default and the property is sold, the first mortgage lender gets paid first. The second mortgage lender recovers whatever remains, which is why second mortgage lenders charge higher rates than first mortgage lenders.

Lenders assess your combined loan-to-value ratio (CLTV) before approving a second mortgage. This figure adds your existing mortgage balance to the new loan amount, then divides the total by your property’s current value. CLTV limits typically sit at 80%–85%, meaning you need at least 15%–20% equity remaining after both loans are counted. That equity buffer protects the lender and sets the ceiling on how much you can borrow.

The application process follows a clear sequence:

- Request a property appraisal. A registered valuer confirms your home’s current market value. This figure drives your CLTV calculation and determines your borrowing limit.

- Gather your financial documents. Lenders require recent payslips or tax returns, bank statements, proof of your existing mortgage balance, and a current credit report.

- Submit your application. Your lender or mortgage adviser lodges the application with supporting documents.

- Lender assessment. The lender reviews your credit score, debt-to-income ratio, and CLTV. This stage can involve a formal credit inquiry, which temporarily lowers your credit score.

- Settlement. Once approved, funds are released. The full process from application to closing typically takes 2–4 weeks.

Pro Tip: Request a copy of your credit report before you apply. Correcting errors in advance can improve your rate and reduce the chance of delays.

Second mortgage lenders hold real legal power. They can initiate foreclosure independently from the first mortgage lender if there is enough equity in the property to cover their losses. This right is rarely exercised, but it is a genuine risk you need to factor into your decision.

What types of second mortgages are available?

Two main products fall under the second mortgage umbrella: home equity loans and home equity lines of credit (HELOCs). Choosing between them depends on how you plan to use the funds and how comfortable you are with variable repayments.

Home equity loans deliver a fixed lump sum at a fixed interest rate, with set monthly repayments over an agreed term. This structure suits borrowers who need a defined amount for a specific purpose, such as a kitchen renovation or a deposit on an investment property. You know exactly what you owe each month, which makes budgeting straightforward.

HELOCs work more like a credit card secured against your home. You draw funds as needed up to an approved limit, repay, and draw again. The interest rate is variable, so your repayments shift with the market. New Zealand lenders offer revolving credit facilities that function similarly. You can read more about how revolving credit works and whether it suits your situation.

| Feature | Home equity loan | HELOC / revolving credit |

|---|---|---|

| Funds structure | Lump sum, paid upfront | Draw as needed, up to limit |

| Interest rate | Fixed | Variable |

| Repayments | Set monthly amount | Varies with balance drawn |

| Best suited for | One-off, defined expenses | Ongoing or staged costs |

| Repayment risk | Predictable | Payment shock possible |

The HELOC structure carries a specific risk worth noting. Many products include an interest-only draw period, after which principal repayments begin. That shift can cause payment shock if you have not planned for the higher repayment amount.

Pro Tip: If your renovation will happen in stages, a revolving credit facility lets you draw only what you need and reduces the total interest you pay.

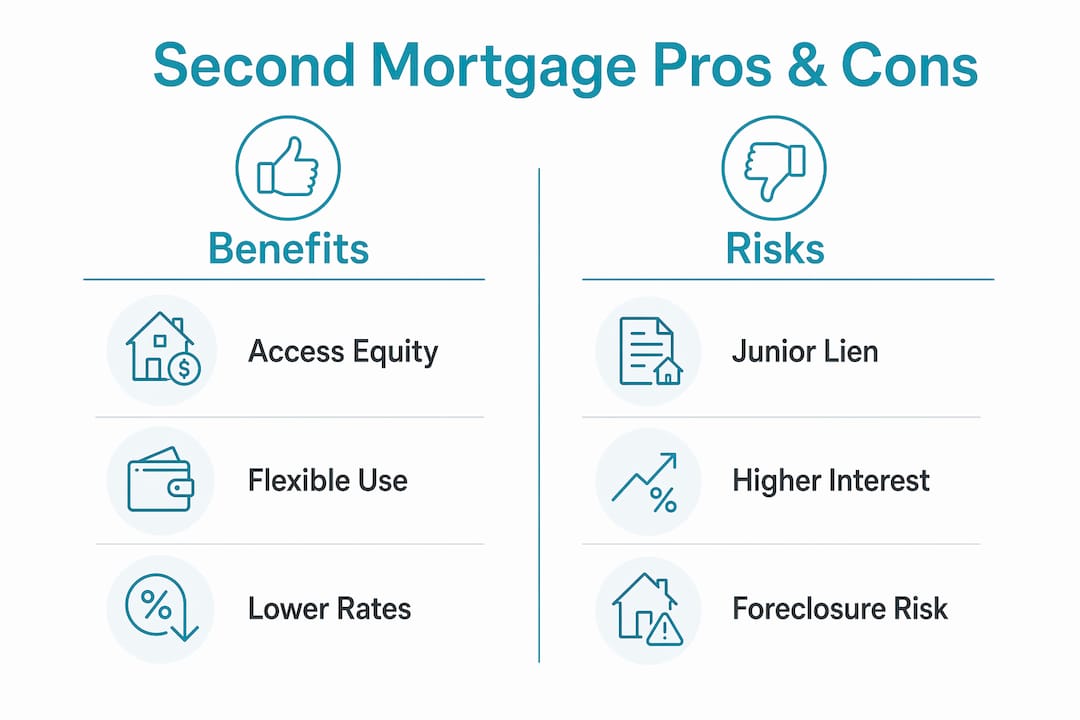

What are the benefits and risks of a second mortgage?

A second mortgage gives you access to equity you have already built, without forcing you to refinance your first mortgage. That matters most when your first mortgage carries a low fixed rate you do not want to break. Homeowners often prefer second mortgages precisely to preserve those favourable primary rates while still accessing funds.

Benefits

- Access to equity without refinancing. You keep your existing mortgage terms intact and borrow separately against your equity.

- Flexible use of funds. Common uses include debt consolidation and home improvements, both of which can improve your financial position over time.

- Potentially lower rates than unsecured debt. Because the loan is secured against your property, rates are generally lower than personal loans or credit cards.

- Investment funding. Property investors use second mortgages to fund deposits on additional properties without liquidating existing assets.

Risks

- Higher interest rates than your first mortgage. The junior lien position means lenders price in extra risk. That premium adds to your total borrowing cost.

- Increased foreclosure exposure. A second mortgage lender can move to foreclose independently if equity conditions allow. Falling property values shrink that buffer quickly.

- Greater debt burden. Two mortgage repayments reduce your monthly cashflow. A change in income can make both harder to service.

- Credit score sensitivity. Your credit score directly affects the rate you receive. Errors on your credit report can cost you significantly over the life of the loan.

- Break costs and fees. Early repayment fees, establishment fees, and valuation costs add to the total expense of the loan.

The junior lien position is the defining risk. In a falling property market, the equity buffer protecting the second mortgage lender can disappear quickly, increasing pressure on both lender and borrower.

How to qualify for a second mortgage in New Zealand

Qualifying for a second mortgage requires meeting specific financial thresholds across credit, income, and equity. Preparing each area before you apply improves both your approval chances and the rate you receive.

- Check your credit score. Most lenders require a minimum score of 620, with the best rates reserved for scores above 720. A score below 620 will likely result in a declined application.

- Review your credit report for errors. Credit report inaccuracies can push your rate higher or trigger a decline. Request a free report from a credit bureau and dispute any errors before you apply.

- Calculate your CLTV. Add your existing mortgage balance to the amount you want to borrow. Divide that total by your property’s current value. If the result exceeds 80%–85%, you may need to reduce the loan amount or wait until your equity grows.

- Assess your debt-to-income ratio. Lenders want to see that your total debt repayments remain manageable relative to your income. Paying down other debts before applying strengthens this ratio.

- Commission a professional appraisal. A registered valuation confirms your property’s market value and supports your application. Budget for this cost as part of your preparation.

- Organise your documents. Gather payslips or tax returns for the past two years, three to six months of bank statements, your current mortgage statement, and proof of identity.

- Work with a mortgage adviser. A qualified adviser knows which lenders are most likely to approve your profile and can present your application in the strongest possible way. Mortgagemanagers specialises in exactly this kind of guidance for New Zealand homeowners. You can find a detailed walkthrough of the NZ second mortgage process on the Mortgagemanagers website.

Pro Tip: Avoid applying for any new credit in the months before your second mortgage application. Each hard inquiry reduces your score slightly and signals financial pressure to lenders.

Key takeaways

A second mortgage gives New Zealand homeowners structured access to home equity, but the junior lien position, higher interest rates, and foreclosure risk make careful preparation non-negotiable.

| Point | Details |

|---|---|

| Lien priority drives cost | Second mortgages rank behind first mortgages, so lenders charge higher rates to offset their risk. |

| CLTV limits your borrowing | Most lenders cap combined loans at 80%–85% of property value, requiring at least 15%–20% equity. |

| Two main product types | Home equity loans offer fixed lump sums; HELOCs provide flexible, variable-rate revolving credit. |

| Credit score is critical | A score above 720 secures the best rates; below 620 typically results in a declined application. |

| Professional advice pays off | A mortgage adviser can match your profile to the right lender and improve your approval outcome. |

Stuart’s view on using second mortgages wisely

The most common mistake I see is borrowers treating a second mortgage like free money. It is not. It is a secured debt that puts your home at greater risk than your first mortgage alone ever did.

The question I always ask clients first is: why not refinance? If your first mortgage rate is no longer competitive, a cash-out refinance can be cheaper overall than adding a second loan at a higher rate. The maths does not always favour a second mortgage, and too many borrowers skip that comparison entirely. Homeowners who preserve a genuinely low fixed rate have a strong reason to keep their first mortgage untouched. But if that rate is average or above, refinancing deserves a serious look before you add another layer of debt.

I have also seen borrowers underestimate how much a second mortgage tightens their monthly cashflow. Two repayments feel manageable until income drops or rates rise. The borrowers who handle it best are those who stress-test their budget at a rate two percentage points higher than their current offer before they sign anything.

New Zealand lenders in 2026 are applying tighter debt-to-income scrutiny than in previous years. That means your income documentation needs to be thorough and your existing debts need to be as low as possible before you apply. Working with an adviser who understands current bank lending criteria is not optional at this stage. It is the difference between a smooth approval and a frustrating decline.

— Stuart

Mortgagemanagers can help you find the right second mortgage

Accessing equity through a second mortgage is a significant financial decision. Getting the structure right from the start saves you money and protects your property.

Mortgagemanagers is a locally owned Auckland mortgage advisory business based in Hobsonville, serving homeowners across West Auckland, the North Shore, and remotely throughout New Zealand. The team works with a wide panel of lenders to find second mortgage products that match your equity position, credit profile, and financial goals. Whether you are funding a renovation, consolidating debt, or building a property portfolio, Mortgagemanagers acts as your personal mortgage adviser, comparing options and negotiating on your behalf so you get the right outcome.

FAQ

What is a second mortgage?

A second mortgage is a loan secured against a property that already has an existing mortgage, ranking behind the first mortgage in repayment priority. It lets you borrow against your home equity without replacing your original loan.

How does a second mortgage differ from a home equity loan?

A home equity loan is one type of second mortgage that delivers a fixed lump sum at a fixed rate. The term “second mortgage” covers any junior lien on a property, including both home equity loans and revolving credit facilities like HELOCs.

What credit score do I need for a second mortgage in New Zealand?

Most lenders require a minimum credit score of 620, with the best interest rates reserved for borrowers with scores above 720. Checking and correcting your credit report before applying is the fastest way to improve your position.

Is a second mortgage worth it?

A second mortgage is worth it when you need to access equity without disturbing a favourable first mortgage rate and you can comfortably service both repayments. If your first mortgage rate is no longer competitive, a cash-out refinance may be a cheaper alternative.

How long does a second mortgage application take in New Zealand?

The process from application to settlement typically takes 2–4 weeks, depending on how quickly you can provide documentation and how long the property appraisal takes to complete.