TL;DR:

- A mortgage loan in New Zealand is a secured long-term debt where your property acts as collateral.

- Choosing the right loan structure, such as fixed, floating, or split, affects your financial flexibility over decades.

A mortgage loan is a secured loan where your property acts as collateral, giving the lender the legal right to sell it if you stop making repayments. In New Zealand, this is the standard mechanism for buying a home, and understanding how it works puts you in a far stronger position before you sign anything. The term “mortgage” and “home loan” are used interchangeably in everyday conversation, but the mortgage is technically the legal security registered against the property title, while the loan is the debt itself. Knowing that distinction matters when you read your loan documents.

What is a mortgage loan and how does it work in New Zealand?

A mortgage loan in New Zealand is structured as a table loan, meaning each repayment is the same dollar amount throughout the loan term. What changes is the split between interest and principal inside each payment. Early in the loan, most of your repayment covers interest. As the years pass and your principal reduces, more of each payment chips away at the actual debt.

Standard loan terms in NZ run 25–30 years. That long timeframe keeps weekly or fortnightly repayments manageable, but it also means you pay a significant amount of interest over the life of the loan. A borrower who makes extra repayments early reduces the principal faster, which cuts the total interest paid considerably.

Interest is calculated on the outstanding balance, so every dollar you pay off the principal saves you future interest. This is why financial advisers consistently recommend making lump sum payments when you can, even small ones.

The lender holds a registered mortgage over your property title for the duration of the loan. If you default, the lender has the legal right to initiate a mortgagee sale, selling the property to recover the debt. That legal security is what allows banks to lend large sums at relatively low interest rates compared to unsecured personal loans.

- You borrow a set amount and the lender registers a mortgage over the property.

- You make regular repayments covering both principal and interest.

- The interest portion shrinks over time as the principal reduces.

- Once the loan is fully repaid, the mortgage is discharged from the title.

Pro Tip: Making even one extra repayment per year on a 25-year loan can shave years off your term. Ask your adviser to model this before you settle on a repayment frequency.

What types of mortgage loans are available in New Zealand?

Common mortgage structures in NZ include fixed-rate, floating, split, offset, and revolving credit facilities. Each suits a different financial situation, and choosing the wrong structure can cost you flexibility or money.

Fixed-rate loans

A fixed-rate loan locks your interest rate for a set period, typically 6 months to 5 years. Your repayments stay the same regardless of what the Reserve Bank of New Zealand does with the Official Cash Rate. This gives you certainty for budgeting, which is particularly valuable for first-time buyers adjusting to homeownership costs. The trade-off is that break fees apply if you want to exit the fixed term early.

Floating (variable) rate loans

A floating rate moves with market conditions. When the Official Cash Rate drops, your rate and repayments can fall too. When it rises, so do your costs. Floating loans typically allow unlimited extra repayments without penalty, making them attractive for borrowers who want to pay down debt aggressively.

Split, offset, and revolving credit

| Loan type | How it works | Best suited to |

|---|---|---|

| Split loan | Part fixed, part floating | Borrowers wanting rate certainty with some flexibility |

| Offset mortgage | Savings balance offsets loan balance, reducing interest | Borrowers with significant savings |

| Revolving credit | Functions like a large overdraft against your home equity | Disciplined borrowers managing variable cash flow |

- Split loans let you fix a portion for certainty while keeping the rest floating for flexibility.

- Offset mortgages are powerful for borrowers with savings sitting in a transaction account, as those funds reduce the interest-bearing balance daily.

- Revolving credit facilities require strong financial discipline. Without it, the easy access to funds can slow debt repayment significantly.

Pro Tip: Fixed vs floating is not a one-size-fits-all decision. Read the fixed vs floating rate breakdown before committing to a structure, especially if rates are moving.

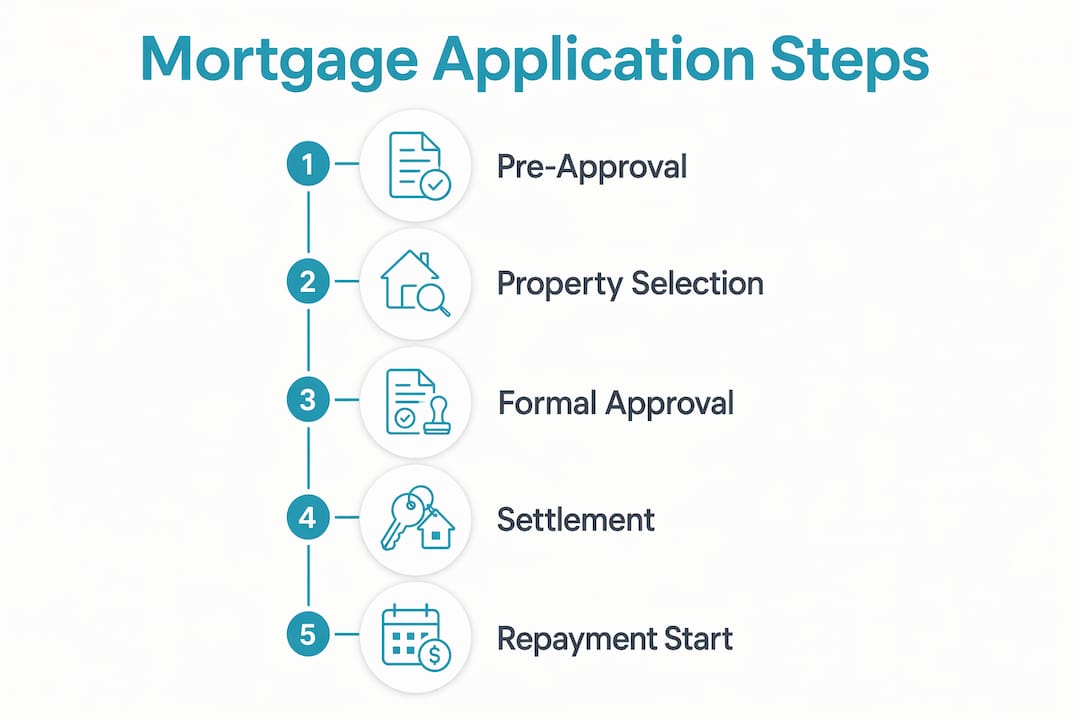

How does the mortgage loan application process work?

The full home buying cycle, from starting your mortgage application to settlement, typically takes 3–6 months in New Zealand. That timeline includes pre-approval, property search, due diligence, formal approval, and settlement. Understanding each stage prevents costly mistakes.

Step-by-step: from pre-approval to settlement

- Prepare your finances. Gather payslips, bank statements, KiwiSaver details, and a list of existing debts and expenses. Lenders review 3–6 months of bank statements to assess your spending habits and financial discipline.

- Apply for pre-approval. Pre-approval gives you a borrowing limit before you start making offers. Pre-approval typically takes 3–10 working days.

- Find a property and make an offer. Your offer should be conditional on finance, building inspection, and a LIM report. Never make an unconditional offer without formal mortgage approval in place.

- Complete due diligence. During the conditional period, arrange your building inspection, review the LIM report from the local council, and get a registered valuation if the lender requires one.

- Secure formal mortgage approval. Once you have chosen a property, formal approval takes an additional 3–5 working days. Your solicitor will review the sale and purchase agreement at this stage.

- Go unconditional. This is the legal point of no return. Going unconditional legally obliges you to complete the purchase. Severe financial penalties apply if you cannot settle.

- Settlement. Your solicitor transfers funds to the vendor. The mortgage is registered on the title and you receive the keys.

Key documents you will need:

- Recent payslips or proof of income (self-employed borrowers need two years of financial statements)

- Three to six months of bank statements

- KiwiSaver account details if using a first home withdrawal

- Identification documents

- Details of existing debts, credit cards, and hire purchase agreements

Pro Tip: Read the full mortgage approval process guide before your first lender meeting. Knowing what documents to bring saves days of back-and-forth.

Practical tips for first-time mortgage borrowers in New Zealand

The biggest mistake first-time borrowers make is focusing almost entirely on the interest rate and ignoring loan structure. Rate matters, but structure determines your financial flexibility for the next 25 years. A slightly higher rate on a floating loan may cost less overall if it lets you make unlimited extra repayments and pay off the debt years earlier.

Banks scrutinise your expenses as closely as your income. Lenders assess 3–6 months of bank statements, and patterns like frequent gambling transactions, high credit card balances, or irregular savings can trigger a decline even when your income looks strong. Preparing your finances at least six months before applying gives you time to clean up your spending record.

Key pitfalls to avoid:

- Going unconditional without full approval. If your finance falls through after going unconditional, you can lose your deposit and face legal action.

- Underestimating due diligence costs. Building inspections, LIM reports, and valuations add up. Budget $1,500–$2,500 for these before making offers.

- Ignoring interest rate stress testing. Banks assess your ability to repay at rates higher than the current rate. Make sure you can genuinely afford repayments if rates rise.

- Overlooking KiwiSaver. Eligible first home buyers can withdraw KiwiSaver contributions toward a deposit. Confirm your eligibility early in the process.

Working with a mortgage adviser in New Zealand gives you access to multiple lenders and structures, not just the one bank where you hold your everyday account. That comparison can make a material difference to your loan terms.

Key takeaways

A mortgage loan in New Zealand is a secured, long-term debt where your property is the lender’s security, and the structure you choose shapes your repayments and financial flexibility for decades.

| Point | Details |

|---|---|

| Mortgage loan definition | A secured loan against property, typically structured as a table loan over 25–30 years. |

| Repayment mechanics | Early repayments are mostly interest; the principal share grows as the balance reduces. |

| Loan structure choice | Fixed, floating, split, offset, and revolving credit each suit different financial situations. |

| Application timeline | Pre-approval takes 3–10 working days; the full buying cycle averages 3–6 months. |

| Unconditional risk | Going unconditional without formal mortgage approval creates serious legal and financial exposure. |

What I have learned watching borrowers navigate mortgages in New Zealand

After years of working with home buyers across Auckland and beyond, one pattern stands out clearly. Borrowers spend enormous energy comparing interest rates across lenders, sometimes agonising over a difference of 0.1%, while paying almost no attention to loan structure. That is the wrong priority.

I have seen borrowers lock into a five-year fixed rate because it felt safe, only to find themselves unable to make extra repayments when their income grew. The break fee to exit that fixed term wiped out the rate saving entirely. A split loan or a shorter fixed term would have served them far better.

The conditional period is another area where I see real stress. Buyers underestimate how much coordination is required to get a building inspection, LIM report, and valuation completed within a 10-day conditional window. Booking those services the moment your offer is accepted is not optional. It is the only way to meet the timeframe without panicking.

The borrowers who come through the process with the least stress are the ones who prepared their finances six months out, chose their loan structure deliberately, and worked with an adviser who could explain the trade-offs clearly. Rate is just one variable. Structure, flexibility, and preparation are the ones that actually determine your outcome.

— Stuart

How Mortgagemanagers can help you find the right home loan

Choosing a mortgage is one of the largest financial decisions you will make. Getting it right means comparing lenders, understanding structures, and knowing which product fits your situation, not just the one your bank happens to offer.

Mortgagemanagers acts as your personal shopper for home loans, comparing options across multiple lenders to find the structure and rate that suits your goals. Based in Hobsonville and servicing Auckland, the North Shore, West Auckland, and clients across New Zealand remotely, the team brings local knowledge and lender relationships that a single bank simply cannot match. Whether you are buying your first home or refinancing an existing loan, Mortgagemanagers guides you through every step with clarity and confidence.

FAQ

What is the mortgage loan definition in simple terms?

A mortgage loan is a secured loan where the property you are buying acts as collateral for the debt. If you stop repaying, the lender has the legal right to sell the property to recover what is owed.

What is the difference between a mortgage and a home loan?

The terms are used interchangeably in New Zealand, but technically the mortgage is the legal security registered on the property title, while the home loan is the debt itself. Both terms refer to the same borrowing arrangement.

How long does mortgage approval take in New Zealand?

Pre-approval typically takes 3–10 working days. Formal approval after selecting a property takes an additional 3–5 working days, and the full home buying process averages 3–6 months from start to settlement.

What does a mortgage loan cover?

A mortgage loan covers the purchase price of a residential property, minus your deposit. It does not cover legal fees, building inspections, LIM reports, or moving costs, so budget for those separately.

Can I pay off my mortgage loan early in New Zealand?

Yes, but the rules depend on your loan structure. Floating rate loans allow unlimited extra repayments without penalty. Fixed rate loans typically charge break fees if you repay early or restructure before the fixed term ends.