More than half of australian and New Zealand homebuyers feel overwhelmed by complicated mortgage terms and servicing rules. Deciding on a first home in Hobsonville or West Auckland brings not just excitement but a maze of finance options that can be difficult to understand. Knowing how mortgage servicing works lets you take control, avoid costly mistakes, and make long-term choices with more confidence and financial clarity.

Table of Contents

- Mortgage Servicing Explained For Homebuyers

- Types Of Mortgage Structures In New Zealand

- How Lenders Assess Loan Serviceability

- Key Costs, Risks And Mistakes To Avoid

- Tips For Improving Mortgage Approval Chances

Key Takeaways

| Point | Details |

|---|---|

| Understanding Mortgage Servicing | Mortgage servicers manage crucial aspects of home loans, including payment processing and customer support, ensuring smooth financial transactions. |

| Evaluating Mortgage Structures | New Zealand offers diverse mortgage types, including principal and interest, interest-only, and revolving credit, tailored to different financial needs. |

| Loan Serviceability Assessment | Lenders assess several factors, such as income stability and existing debts, to determine a borrower’s ability to manage loan repayments effectively. |

| Avoiding Common Mistakes | First-home buyers should be aware of additional ownership costs and choose suitable loan structures to avoid financial strain and ensure long-term stability. |

Mortgage Servicing Explained For Homebuyers

Mortgage servicing represents the operational backbone that keeps your home loan functioning smoothly throughout its lifecycle. When you secure a home loan, the mortgage servicer becomes your primary point of contact, managing critical financial transactions and administrative tasks that ensure your property remains securely financed. These professionals handle everything from processing monthly payments to maintaining crucial loan documentation.

The fundamental role of mortgage servicing involves collecting and distributing your regular loan payments, which typically include principal, interest, property taxes, and potentially homeowners insurance. Your servicer tracks every dollar, ensuring funds are allocated correctly and maintaining accurate financial records. Understanding mortgage repayments helps first-time homebuyers comprehend exactly how their monthly contributions support their overall financial commitment.

Mortgage servicers also manage several behind-the-scenes responsibilities that most homebuyers never see. This includes managing escrow accounts, processing insurance and tax payments, handling potential loan modifications, and providing critical customer support when financial challenges arise. They act as intermediaries between borrowers and lenders, maintaining transparent communication channels and helping homeowners navigate complex financial landscapes.

Pro tip: Always maintain open communication with your mortgage servicer and keep detailed records of all interactions and payments to protect your financial interests and ensure smooth loan management.

Types Of Mortgage Structures In New Zealand

New Zealand’s mortgage market offers several distinct loan structures designed to accommodate diverse financial needs and borrowing strategies. Mortgage structures vary widely, providing homebuyers with flexible options to match their unique financial circumstances and long-term property investment goals.

The primary mortgage types in New Zealand include standard principal and interest loans, interest-only loans, and revolving credit facilities. Principal and interest loans represent the most traditional structure, where borrowers steadily reduce their loan balance through regular payments that cover both the original borrowed amount and accruing interest. Interest-only loans offer short-term flexibility by allowing borrowers to pay only the interest portion for a specified period, which can be beneficial for investors or those experiencing temporary financial constraints.

Revolving credit facilities provide a unique approach to home financing, functioning similarly to an advanced overdraft account. These structures allow borrowers to blend their everyday banking with mortgage management, potentially reducing overall interest payments by applying incoming funds directly to the loan balance. Borrowers can often access additional funds while maintaining the ability to make variable payments that suit their changing financial situations.

Here is a comparison of common mortgage structures available in New Zealand:

| Mortgage Type | How Repayments Work | Typical Borrower | Key Benefit |

|---|---|---|---|

| Principal & Interest | Reduces loan balance monthly | First-home buyers, families | Gradual equity growth |

| Interest-Only | Pays only interest for set period | Investors, short-term budget relief | Lower initial repayment amounts |

| Revolving Credit Facility | Flexible repayments, acts like overdraft | Borrowers with variable income | Lower interest paid if managed well |

Pro tip: Consider consulting a mortgage adviser to understand which loan structure best matches your specific financial profile and long-term property ownership objectives.

How Lenders Assess Loan Serviceability

Lenders employ a comprehensive approach to evaluating loan serviceability, scrutinising multiple financial dimensions to determine a borrower’s capacity to manage mortgage repayments. Lenders focus intensely on your income as the primary indicator of financial stability and repayment potential. This assessment goes far beyond simply examining your current salary, diving deep into your overall financial health, income consistency, and future earning prospects.

The loan serviceability assessment typically involves a detailed analysis of several key financial factors. Lenders carefully examine your gross income, taking into account not just your base salary but also additional revenue streams like bonuses, overtime, rental income, and investment returns. They simultaneously evaluate your existing financial commitments, including credit card limits, personal loans, car payments, and other recurring expenses. This comprehensive review helps them calculate your debt-to-income ratio, which critically determines your ability to take on and manage a new mortgage.

Beyond financial metrics, lenders also consider your employment stability, credit history, and overall financial behaviour. They look for consistent employment patterns, preferring borrowers with steady jobs and predictable income streams. Your credit score plays a significant role, with a strong history of timely bill payments and responsible credit management significantly improving your loan serviceability assessment. Lenders will typically request detailed bank statements, tax returns, and employment verification to build a comprehensive picture of your financial reliability.

Below is a summary of key factors lenders review during the loan serviceability assessment:

| Factor | What Lenders Evaluate | Example Questions Considered |

|---|---|---|

| Income | Stability and diversity of sources | How stable is your salary? |

| Existing Debt | Credit cards, personal loans | What current obligations exist? |

| Employment History | Length and reliability of job | Have you had steady roles? |

| Credit Behaviour | Timely payments, responsible use | Is your credit report positive? |

Pro tip: Before applying for a mortgage, conduct a thorough review of your financial documents, reduce unnecessary expenses, and ensure your bank statements reflect responsible financial management.

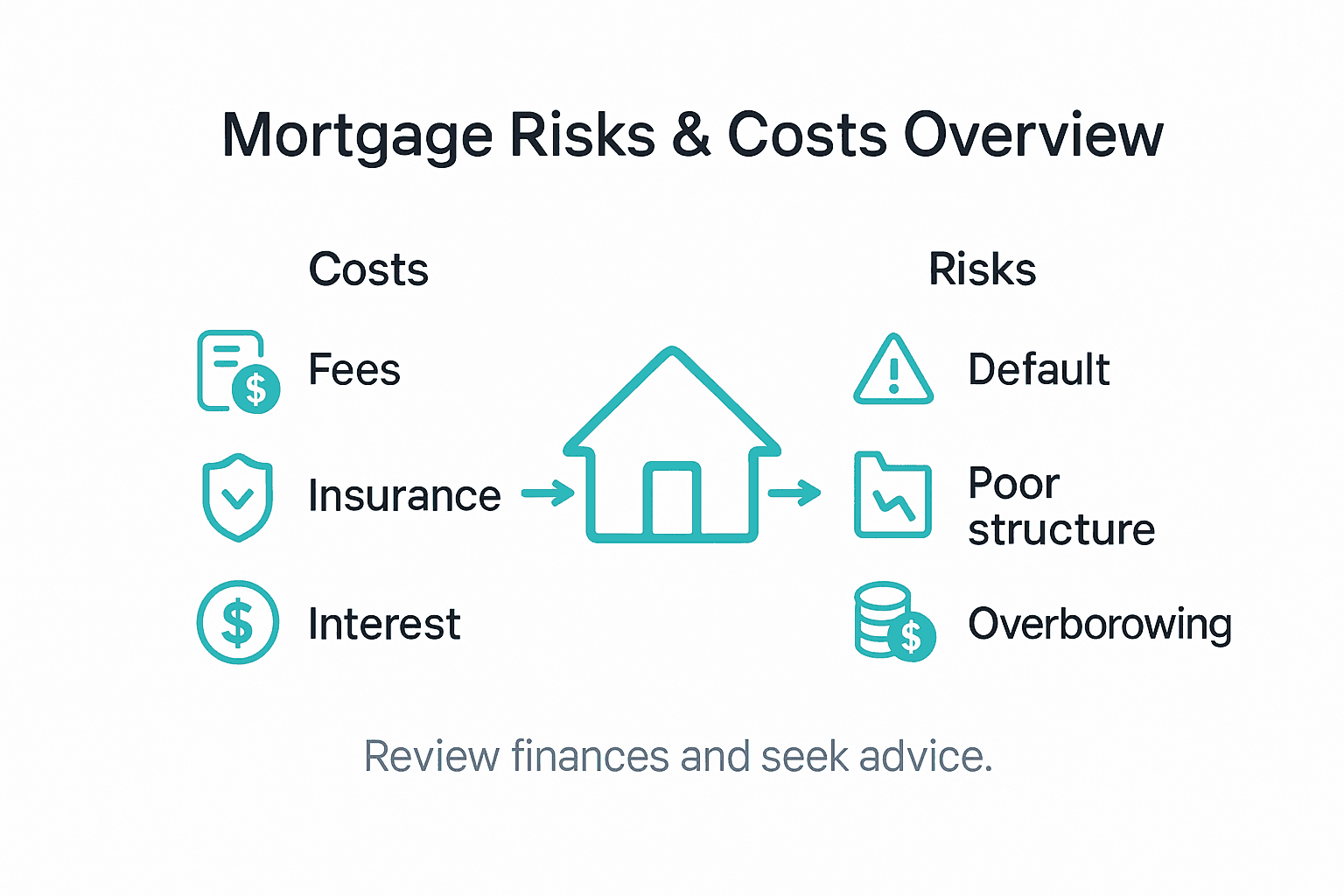

Key Costs, Risks And Mistakes To Avoid

First-home buyers must navigate a complex landscape of potential financial pitfalls when securing a mortgage, with several critical mistakes that can significantly impact long-term financial stability. Understanding these risks is crucial for making informed decisions and protecting your financial future.

One of the most significant risks involves misunderstanding the total cost of homeownership. Beyond the mortgage principal and interest, first-time buyers often underestimate additional expenses such as property maintenance, insurance, council rates, and potential renovation costs. Many new homeowners fail to budget for these ongoing expenses, which can create substantial financial strain. Lenders typically recommend maintaining an emergency fund equivalent to 3-6 months of mortgage payments to buffer against unexpected financial challenges.

Another critical area of risk involves selecting inappropriate loan structures and terms. Borrowers frequently make costly mistakes by choosing variable interest rates without fully understanding potential market fluctuations or selecting loan terms that stretch their financial capacity too thin. Some first-home buyers become overly optimistic about their future earning potential, committing to mortgage repayments that become unsustainable during economic downturns or personal financial setbacks. Careful consideration of loan flexibility, potential interest rate changes, and realistic income projections is essential for long-term financial security.

Pro tip: Conduct a comprehensive financial review with a professional mortgage adviser to identify potential risks and develop a strategic approach that aligns with your unique financial circumstances.

Tips For Improving Mortgage Approval Chances

Securing mortgage approval requires strategic financial planning and a comprehensive understanding of lenders’ expectations. Home loan eligibility demands careful preparation and proactive management of your financial profile to demonstrate reliability and repayment capacity.

First-time buyers can significantly enhance their mortgage approval prospects by maintaining a clean credit history and demonstrating consistent financial responsibility. This involves several key strategies: keeping credit card balances low, avoiding unnecessary credit applications, and ensuring all existing financial obligations are paid punctually. Lenders scrutinise bank statements for evidence of stable income, consistent savings patterns, and responsible spending habits. Reducing existing debts, particularly high-interest consumer loans and credit card balances, can substantially improve your debt-to-income ratio and make you a more attractive borrower.

Documentation plays a critical role in mortgage approval processes. Prospective homebuyers should compile a comprehensive financial portfolio that includes recent payslips, tax returns, bank statements, proof of employment, and detailed records of any additional income sources. Lenders prefer applicants who can provide clear, consistent evidence of financial stability. This means maintaining the same employment for at least six months to a year, avoiding frequent job changes, and being prepared to explain any irregular income patterns or financial history complexities.

Pro tip: Obtain a copy of your credit report at least six months before applying for a mortgage, allowing time to address any potential issues or discrepancies that might negatively impact your loan application.

Take Control of Your Mortgage Servicing With Expert Guidance

Navigating mortgage servicing can feel overwhelming for first-home buyers especially when managing repayments, understanding loan structures or preparing for lender assessments. At Mortgage Managers, we understand these critical challenges and provide personalised advice to help you avoid costly mistakes, improve your loan serviceability and choose the best mortgage structure to suit your unique financial situation. Our Auckland-based mortgage advisers are ready to guide you through every step, making complex mortgage terms simple and empowering you with clear options.

Don’t let uncertainty hold you back from securing your dream home. Visit Mortgage Managers now to benefit from expert support tailored to first-home buyers. Discover how you can improve your mortgage approval chances and protect your financial future with our trusted advice. Start your journey today by exploring our loan serviceability insights and choosing the right mortgage structure. Take confident steps towards homeownership with Mortgage Managers.

Frequently Asked Questions

What is mortgage servicing, and why is it important for first-home buyers?

Mortgage servicing refers to the management of home loans, including collecting payments, managing escrow accounts, and providing customer support. It is crucial for first-home buyers as it ensures their loans are handled properly throughout the mortgage term, helping them maintain financial stability.

How do mortgage servicers handle monthly payments?

Mortgage servicers collect and distribute monthly payments, which typically cover the principal, interest, property taxes, and insurance. They track each dollar to ensure accurate allocation and maintain proper financial records for transparent loan management.

What should first-home buyers look for in a mortgage servicer?

First-home buyers should look for a mortgage servicer that offers effective communication, transparency in fees, reliable customer support, and a strong reputation for managing loans properly. Establishing good communication can aid in financial problem-solving when challenges arise.

How can first-home buyers protect their financial interests during the mortgage servicing process?

Homebuyers can protect their interests by maintaining open communication with their servicer, keeping detailed records of all interactions and payments, and understanding their mortgage terms and potential risks involved. Regularly reviewing loan documents can also enhance financial awareness.