Many New Zealand homeowners confuse refinancing with restructuring, often using the terms interchangeably when discussing mortgage changes. This misunderstanding can lead to costly financial decisions that don’t align with your actual needs or circumstances. Refinancing and restructuring are fundamentally different approaches to managing your home loan, each suited to distinct situations and goals. This guide clarifies both options in practical terms, helping you understand which path fits your financial situation and how to make an informed choice that protects your investment.

Table of Contents

- Key takeaways

- What is refinancing and how does it work?

- What is restructuring and when is it the better choice?

- Comparing refinance and restructure: key differences and eligibility

- How to decide between refinancing and restructuring your mortgage

- How mortgage managers can help with refinancing and restructuring

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

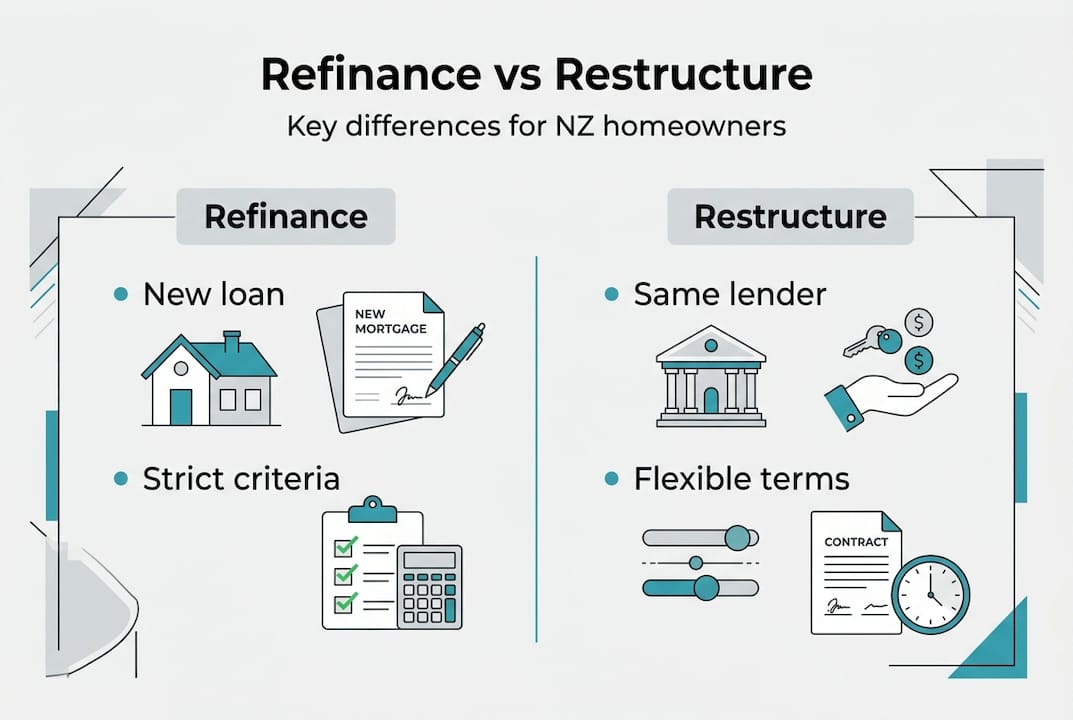

| New loan replacement | refinancing means replacing your existing mortgage with a new loan, often with different terms or a different lender. |

| Existing loan tweaks | restructuring modifies the current loan without taking out a new loan or changing lenders. |

| Break even calculation | Calculate your break even point by dividing total upfront costs by monthly savings to judge if refinancing is worth it. |

| Choose by goals and credit | The right option depends on your financial goals and your credit situation. |

What is refinancing and how does it work?

Refinancing lets homeowners replace their current mortgage with a completely new loan, often featuring different terms, rates, or even a different lender altogether. Think of it as trading in your existing mortgage for a fresh start that better aligns with your current financial position and goals. The new loan pays off your old mortgage entirely, and you begin making payments under the new agreement.

New Zealand homeowners typically refinance for several compelling reasons. Lower interest rates top the list, as even a small rate reduction can save thousands over your loan’s lifetime. Many also refinance to access home equity for renovations, investments, or debt consolidation. Better loan features like offset accounts or flexible repayment options attract others, whilst some simply want to escape restrictive terms or poor service from their current lender.

The refinancing process involves several clear steps. You start by evaluating current market rates and loan products, comparing what’s available against your existing mortgage. Next comes the application phase, where your new lender assesses your financial situation, credit history, and property value. Be prepared for costs including application fees, valuation fees, legal fees, and potentially break fees if you’re leaving a fixed-rate term early. Once approved, settlement occurs where the new loan pays out the old one, and you transition to your new repayment schedule.

Refinancing offers genuine advantages beyond rate savings. You gain flexibility to restructure your loan term, potentially shortening it to build equity faster or extending it to reduce monthly payments. Consolidating high-interest debts into your mortgage can simplify finances and reduce overall interest costs. Access to equity unlocks opportunities for property improvements that increase home value or investments that generate returns.

Pro Tip: Calculate your break-even point before refinancing by dividing total upfront costs by monthly savings. If you plan to stay in your home longer than this break-even period, refinancing likely makes financial sense. If you’re moving soon, the costs may outweigh benefits.

What is restructuring and when is it the better choice?

Restructuring modifies existing mortgage terms to better suit your current financial situation without taking out a new loan or changing lenders. Your lender adjusts the conditions of your existing agreement, offering relief or flexibility whilst maintaining the fundamental loan relationship. This approach proves particularly valuable when you’re facing temporary challenges or need breathing room without the complexity and cost of refinancing.

Common restructuring options provide various forms of relief. Extending your loan term reduces monthly payments by spreading repayments over more years, though you’ll pay more interest overall. Changing repayment frequency from monthly to fortnightly can align better with your income schedule and slightly reduce interest through more frequent payments. Switching temporarily to interest-only payments dramatically lowers immediate obligations, giving you time to stabilise finances, though you’re not reducing the principal during this period. Some lenders also allow payment holidays for genuine hardship situations.

Restructuring suits homeowners experiencing specific circumstances. Payment difficulties due to job loss, reduced hours, or unexpected expenses make restructuring a lifeline that prevents default. Income fluctuations from seasonal work or contract positions benefit from flexible repayment structures. Short-term relief needs, such as covering medical costs or supporting family, become manageable without the stress of maintaining full mortgage payments. Business owners facing temporary cash flow challenges often restructure rather than risk their home.

Potential downsides deserve honest consideration. Extending your loan term means paying significantly more interest over the life of your mortgage, potentially adding years to your debt. Most lenders charge fees for restructuring, though these typically cost less than refinancing. Your credit file may show the restructuring, particularly if you’ve formally entered a hardship arrangement, which could affect future borrowing. Interest-only periods delay equity building, leaving you with the same principal debt when they end.

Pro Tip: Contact your lender at the first sign of payment trouble, well before missing any payments. Banks prefer proactive borrowers and offer more options when you approach them early. Waiting until you’ve missed payments limits your choices and damages your credit record, making future refinancing much harder.

Comparing refinance and restructure: key differences and eligibility

Refinancing and restructuring differ significantly in eligibility requirements, costs, and ultimate impact on your mortgage terms. Understanding these distinctions helps you identify which option suits your situation and whether you’ll qualify for your preferred approach.

| Factor | Refinancing | Restructuring |

|---|---|---|

| Process complexity | High: new application, credit check, valuation | Low: internal adjustment with existing lender |

| Typical costs | $2,000-$5,000+ (fees, valuations, legal) | $200-$500 (administration fees) |

| Interest rate impact | Can secure lower market rates | Usually maintains current rate |

| Credit requirements | Good to excellent credit score needed | More lenient, considers circumstances |

| Timeframe | 4-8 weeks from application to settlement | 1-3 weeks for approval and implementation |

| Equity requirements | Usually need 20% equity minimum | No additional equity required |

Eligibility requirements create the most significant distinction between these options. Refinancing demands strong financial credentials including a good credit score, stable employment history, and sufficient income to service the new loan. Lenders assess you as a new customer, scrutinising your entire financial picture. You’ll need adequate equity in your property, typically at least 20% to avoid lenders mortgage insurance, though some lenders accept less with additional costs. Your debt-to-income ratio must fall within acceptable limits, usually below 40% of gross income.

Restructuring takes a more flexible approach to eligibility. Your existing lender already knows your payment history and circumstances, giving them confidence to work with you through challenges. Credit score matters less than your demonstrated commitment to meeting obligations and your reasons for needing adjustment. Employment stability still counts, but temporary disruptions don’t automatically disqualify you if you can show a path back to normal payments. Equity levels don’t factor into restructuring decisions since you’re not borrowing additional funds.

Common financial goals align differently with each option. Refinancing serves homeowners seeking to capitalise on better market conditions, access equity for specific purposes, or consolidate expensive debts into lower-rate mortgage debt. It suits those with strong financial positions wanting to optimise their mortgage structure. Restructuring serves homeowners needing temporary relief from payment pressure, time to recover from setbacks, or adjustments to match changed income patterns. It suits those facing challenges but committed to keeping their home.

Advantages and disadvantages balance differently for each approach. Refinancing offers potential long-term savings, better loan features, and the opportunity to shop competitors for best terms, but comes with substantial upfront costs, lengthy approval processes, and strict eligibility hurdles. Restructuring provides quick relief, minimal costs, and maintains your existing lender relationship, but typically doesn’t improve your interest rate, may extend your debt period, and offers less dramatic financial improvement than refinancing.

How to decide between refinancing and restructuring your mortgage

Choosing between refinancing and restructuring depends on your specific financial goals, credit profile, and capacity to manage the process and costs involved. Several key factors should guide your decision.

Interest rates form the foundation of your analysis. If market rates have dropped significantly since you took your mortgage, refinancing becomes attractive. Calculate potential savings by comparing your current rate against available rates, factoring in all costs. Even a 0.5% reduction saves substantial money over a 25-year loan. Conversely, if rates have risen or remained stable, restructuring makes more sense for gaining flexibility without rate risk.

Loan terms and features matter beyond just rates. Review your current mortgage restrictions, penalties, and features. Are you locked into a fixed term with high break fees? Does your loan lack offset accounts or flexible repayment options you now want? Refinancing lets you access modern features and remove restrictive conditions. If your current loan already offers good features and you simply need payment relief, restructuring avoids unnecessary change.

Fees and costs require honest calculation. Total all refinancing expenses including application fees, valuation costs, legal fees, and any break fees for leaving your current loan early. Compare this against restructuring fees, typically much lower. Calculate how long you need to recoup refinancing costs through savings. If you’re planning to sell within a few years, high upfront costs may never pay off.

Credit score and financial position determine feasibility. Check your credit report before deciding. A strong score above 700 opens refinancing options with competitive rates. Scores below 600 make refinancing difficult and expensive, pushing you toward restructuring. Consider your employment stability, income level, and existing debts. Lenders scrutinise these factors heavily during refinancing but less so for restructuring.

Follow these steps to evaluate your situation systematically:

- Review your current mortgage statement, noting your interest rate, remaining term, balance, and any fixed-period end dates.

- Research current market rates from multiple lenders, comparing against your existing rate to identify potential savings.

- Check your credit score and report, addressing any errors before applying for refinancing if that’s your likely path.

- Calculate total refinancing costs including all fees, break costs, and legal expenses to understand your upfront investment.

- Estimate monthly savings from refinancing or restructuring, projecting these over your expected time in the property.

- Assess your financial stability, considering job security, income trends, and ability to manage application processes.

- Consult a mortgage adviser or broker who can access multiple lenders and provide personalised analysis of your options.

Seek professional mortgage advice when facing complex decisions. Brokers understand current lender policies, eligibility requirements, and can negotiate on your behalf. They access products unavailable directly to consumers and save you time shopping multiple banks. Their expertise proves especially valuable if you have credit challenges, complex income sources, or unique property situations.

Warning signs indicate when restructuring is safer than refinancing. If you’ve recently missed payments, faced employment disruption, or seen your credit score drop, restructuring with your current lender who knows your history makes more sense than facing rejection from new lenders. If you need immediate relief within weeks rather than months, restructuring’s faster timeline suits urgent situations. When you’re confident your financial challenge is temporary and you’ll return to normal payments soon, restructuring provides a bridge without the commitment and cost of refinancing.

Conversely, refinancing makes more sense when you have strong credit, stable income, and clear long-term savings from better rates or terms. If you’re accessing equity for value-adding renovations or investments, refinancing provides the structure and funding. When your current lender offers poor service or inflexible terms, refinancing lets you vote with your feet.

Pro Tip: Use online mortgage calculators to model different scenarios before committing. Calculate total interest costs over your full loan term for refinancing options versus your current loan. Factor in all fees to see true costs. Many broker websites offer these tools free, and advisers can provide detailed comparisons showing exactly how each option affects your finances over time.

How mortgage managers can help with refinancing and restructuring

Navigating mortgage decisions becomes significantly easier with expert guidance tailored to your unique circumstances. After understanding the differences between refinancing and restructuring, the practical challenge is executing your choice effectively whilst securing the best possible terms.

Mortgage Managers bring specialised knowledge of New Zealand’s lending landscape, helping you identify which lenders suit your situation and which products align with your goals. Professional advisers act as your personal shoppers, comparing options across multiple banks and non-bank lenders to find optimal solutions you might miss researching independently. They handle complex paperwork, liaise with lenders on your behalf, and negotiate terms using their established relationships and market insight.

Whether you’re considering refinancing for better rates or need restructuring to manage temporary challenges, expert mortgage advisers simplify the process whilst maximising your financial outcome. Their service typically costs you nothing, as lenders pay adviser commissions, yet you gain professional representation and access to wholesale rates often unavailable directly.

Frequently asked questions

What is the main difference between refinancing and restructuring?

Refinancing replaces your entire mortgage with a new loan, often involving a different lender and fresh terms including potentially lower rates. Restructuring modifies your existing loan’s conditions with your current lender without replacing the underlying mortgage. This fundamental distinction affects costs, timeframes, eligibility requirements, and the outcomes you can achieve through each approach.

Can I refinance my mortgage with bad credit in New Zealand?

Refinancing with bad credit is challenging but possible with specialised brokers or lenders familiar with non-bank mortgages. You’ll likely face higher interest rates, need larger deposits, and have fewer lender options. Working with experienced advisers who understand which lenders consider applications from borrowers with credit challenges significantly improves your chances of approval and helps you access the most competitive rates available for your situation.

How does refinancing affect my home loan interest rate?

Refinancing can secure lower rates if market conditions have improved since your original mortgage or if your credit profile has strengthened. The new rate depends on current market conditions, your credit score, loan-to-value ratio, and the lender’s assessment of your financial position. Even modest rate reductions of 0.5-1% translate to significant savings over a typical 25-30 year mortgage term, potentially saving tens of thousands of dollars.

How long does refinancing take compared to restructuring?

Refinancing typically takes 4-8 weeks from initial application through to settlement, involving credit checks, property valuations, legal work, and formal approval processes. Restructuring moves much faster, usually completing within 1-3 weeks since you’re working with your existing lender who already holds your information and security. If you need urgent payment relief, restructuring’s shorter timeframe often makes it the only practical option.

Will restructuring my mortgage affect my credit score?

Restructuring itself doesn’t automatically damage your credit score if you maintain payments under the new arrangement. However, if you’ve entered a formal hardship programme or missed payments before restructuring, these events appear on your credit file. Proactive restructuring before missing any payments protects your credit record whilst giving you needed flexibility. Always communicate with your lender early to explore options before payment difficulties become defaults.