Many first-time homebuyers in New Zealand face confusion about subprime mortgages when their limited credit history blocks standard loan approvals. Subprime mortgages offer loans to borrowers with poor credit, but they come with higher costs and significant risks that demand careful consideration. This guide explains what subprime mortgages are, examines the risks through lessons from overseas crises, and highlights practical alternatives and strategies to improve your chances of securing a home loan in New Zealand’s regulated lending environment.

Table of Contents

- What Subprime Mortgages Are And How They Work

- Subprime Mortgage Risks And Criticism: Lessons From Overseas And Relevance To New Zealand

- Alternatives To Subprime Mortgages For First-Time New Zealand Homebuyers

- Comparing Loan Options: Subprime Mortgages Versus Regulated Nz Home Loans

- How Mortgage Advisers Can Help First-Time Buyers With Credit Challenges

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Subprime targets poor credit | These mortgages serve borrowers with credit scores typically between 580 and 669, charging higher interest rates to offset lender risk. |

| NZ offers safer alternatives | Government-backed schemes like Kāinga Ora and guarantor options provide regulated pathways for first-home buyers with credit challenges. |

| Credit improvement matters | Building your credit score and understanding loan terms significantly increase your mortgage approval chances and reduce borrowing costs. |

| Professional advice helps | Mortgage advisers navigate complex eligibility criteria and match buyers to suitable lenders beyond standard banks. |

What subprime mortgages are and how they work

Subprime mortgages are home loans designed for borrowers with poor credit scores, typically ranging from 580 to 669. These loans exist because traditional lenders reject applicants who don’t meet standard creditworthiness criteria. Lenders offset the higher default risk by charging elevated interest rates, requiring larger down payments, and structuring loans with adjustable rates or extended terms.

The key features distinguish subprime mortgages from prime loans. Interest rates can run 2 to 5 percentage points higher than standard mortgages, significantly increasing your total repayment amount over the loan term. Down payment requirements often reach 15 to 25 percent of the property value, compared to the 5 to 10 percent typical for prime borrowers. Many subprime products use adjustable rate mortgages where your interest rate can increase after an initial fixed period, creating payment uncertainty.

These loan characteristics reflect how lenders manage risk when extending credit to borrowers with payment defaults, high debt levels, or insufficient credit history. The higher costs compensate lenders for the statistical likelihood that some subprime borrowers will struggle with repayments or default entirely. Understanding mortgage features for first-time buyers helps you compare these products against standard options.

Pro Tip: Before pursuing any subprime product, calculate the total interest you’ll pay over the loan term, not just the monthly payment, to understand the true cost difference.

New Zealand’s lending market differs substantially from American subprime lending that dominated headlines during the 2008 financial crisis. Kiwi banks operate under stricter regulatory oversight through the Reserve Bank, and the subprime mortgage category remains far less prevalent here. Most NZ lenders focus on prime borrowers, with alternative options like guarantor arrangements or specialist bad credit loans filling the gap for those with credit challenges.

Key differences between prime and subprime mortgages:

- Credit score requirements: Prime loans require scores above 670, while subprime accepts 580 to 669

- Interest rate premiums: Subprime rates typically 2 to 5 percentage points higher

- Down payment demands: Subprime often requires 15 to 25 percent versus 5 to 10 percent for prime

- Loan terms: Subprime may include adjustable rates or balloon payments that prime loans avoid

“Subprime lending serves borrowers who can’t access traditional financing, but the higher costs and risks require careful evaluation of whether homeownership through this route makes financial sense for your situation.”

Subprime mortgage risks and criticism: lessons from overseas and relevance to New Zealand

The 2008 global financial crisis exposed catastrophic flaws in subprime lending practices, particularly in the United States. Empirical research shows US subprime mortgages peaked at 20 percent of loan originations in 2006, with delinquency rates exceeding 11.7 percent. The securitisation of these risky loans, where lenders bundled and sold them to investors, led to 10 to 25 percent higher default rates because originators had little incentive to screen borrowers carefully.

Lax lending standards created a perfect storm. Borrowers received loans without income verification, minimal down payments, and teaser rates that reset to unaffordable levels. When property values stopped rising, millions of homeowners found themselves owing more than their homes were worth, triggering mass defaults that collapsed financial institutions and devastated economies worldwide.

New Zealand’s experience differs markedly due to tighter regulation and conservative lending practices. The Reserve Bank enforces responsible lending codes and loan-to-value ratio restrictions that limit high-risk lending. While NZ data shows 14 percent subprime personal loan approval rates in 2025, these figures reflect personal lending rather than mortgages, where standards remain stricter.

Comparison of US and NZ subprime lending:

| Metric | United States (2006 peak) | New Zealand (2026) |

|---|---|---|

| Subprime share of originations | 20 percent | Less than 2 percent |

| Delinquency rates | 11.7 percent plus | Below 5 percent |

| Regulatory oversight | Minimal pre-crisis | Strict RBNZ standards |

| Securitisation impact | Widespread, high risk | Limited, controlled |

Criticisms of subprime lending centre on predatory practices and borrower exploitation. Critics argue these loans trap vulnerable buyers in unaffordable debt, with adjustable rates and balloon payments creating payment shocks that lead to foreclosure. The high costs extract wealth from borrowers who can least afford it, while lenders profit from fees and interest regardless of whether borrowers succeed.

Pro Tip: If a lender offers you a loan that seems too good to be true with low initial payments, ask exactly when and how much those payments will increase before signing anything.

New Zealand’s approach emphasises regulated alternatives over high-risk subprime products. Government schemes like Kāinga Ora provide low-deposit options with consumer protections, while guarantor arrangements let family members support your application without the predatory features of American-style subprime lending. Understanding bad credit home loans NZ options reveals safer pathways to homeownership.

Key risks of subprime mortgages:

- Payment affordability: Higher interest rates strain your budget and increase default risk

- Rate adjustments: Adjustable rate mortgages can spike your payments unexpectedly

- Equity building: Higher costs mean less of your payment reduces the principal balance

- Refinancing difficulty: Poor credit and high loan-to-value ratios limit your ability to refinance to better terms

“The 2008 crisis taught us that subprime lending without proper safeguards destroys wealth for borrowers and destabilises entire economies, reinforcing why New Zealand’s regulated approach better protects first-time buyers.”

Alternatives to subprime mortgages for first-time New Zealand homebuyers

New Zealand offers several regulated alternatives that provide safer pathways to homeownership for buyers with limited credit history. Kāinga Ora First Home Loan stands out as a government-backed option requiring only a 5 percent deposit, with the government guaranteeing up to 15 percent of the loan value. However, this programme requires solid credit history, stable employment, debt-to-income ratios under 6 times your annual income, and income caps of $95,000 for singles or $150,000 for couples.

Bad credit often disqualifies applicants from Kāinga Ora despite the low deposit requirement, because lenders still assess your ability to service the loan responsibly. This highlights why improving your credit position before applying significantly increases your chances of approval. Other regulated options include guarantor arrangements where a family member with good credit and equity guarantees your loan, reducing the lender’s risk without requiring you to have perfect credit yourself.

Alternative home loan options for limited credit buyers:

- Guarantor loans: Family member guarantees part of your loan, allowing lower deposits and better rates despite your credit challenges

- Specialist bad credit lenders: Some non-bank lenders offer bad credit home loans with higher rates but more flexible credit criteria

- Joint applications: Applying with a partner or family member who has stronger credit can improve approval odds

- Larger deposits: Saving 15 to 20 percent deposit reduces lender risk and may offset credit concerns

Pro Tip: Start working with a mortgage adviser 6 to 12 months before you want to buy, giving you time to improve your credit and financial position based on their specific recommendations.

Improving your credit score and financial profile dramatically increases your mortgage options and reduces borrowing costs. Follow these practical steps to strengthen your application:

- Check your credit report for errors and dispute any inaccuracies that damage your score

- Pay all bills on time for at least six months before applying, as recent payment history weighs heavily

- Reduce existing debts, particularly high-interest credit cards and personal loans that inflate your debt-to-income ratio

- Avoid new credit applications in the months before your mortgage application, as multiple inquiries lower your score

- Build savings to demonstrate financial discipline and increase your deposit amount

- Maintain stable employment, as lenders prefer at least 12 months in your current role

Income stability and employment history matter as much as credit scores for New Zealand lenders. Contract workers and self-employed applicants face additional scrutiny, often needing two years of accounts to prove consistent income. Understanding how to rebuild credit for mortgage NZ provides detailed strategies tailored to Kiwi lending requirements.

Experienced mortgage advisers navigate complex eligibility criteria across multiple lenders, finding options that mainstream banks might miss. They understand which lenders accept specific credit issues, how to structure applications to highlight your strengths, and when to wait versus apply immediately. This expertise proves invaluable when your credit history doesn’t fit standard lending boxes.

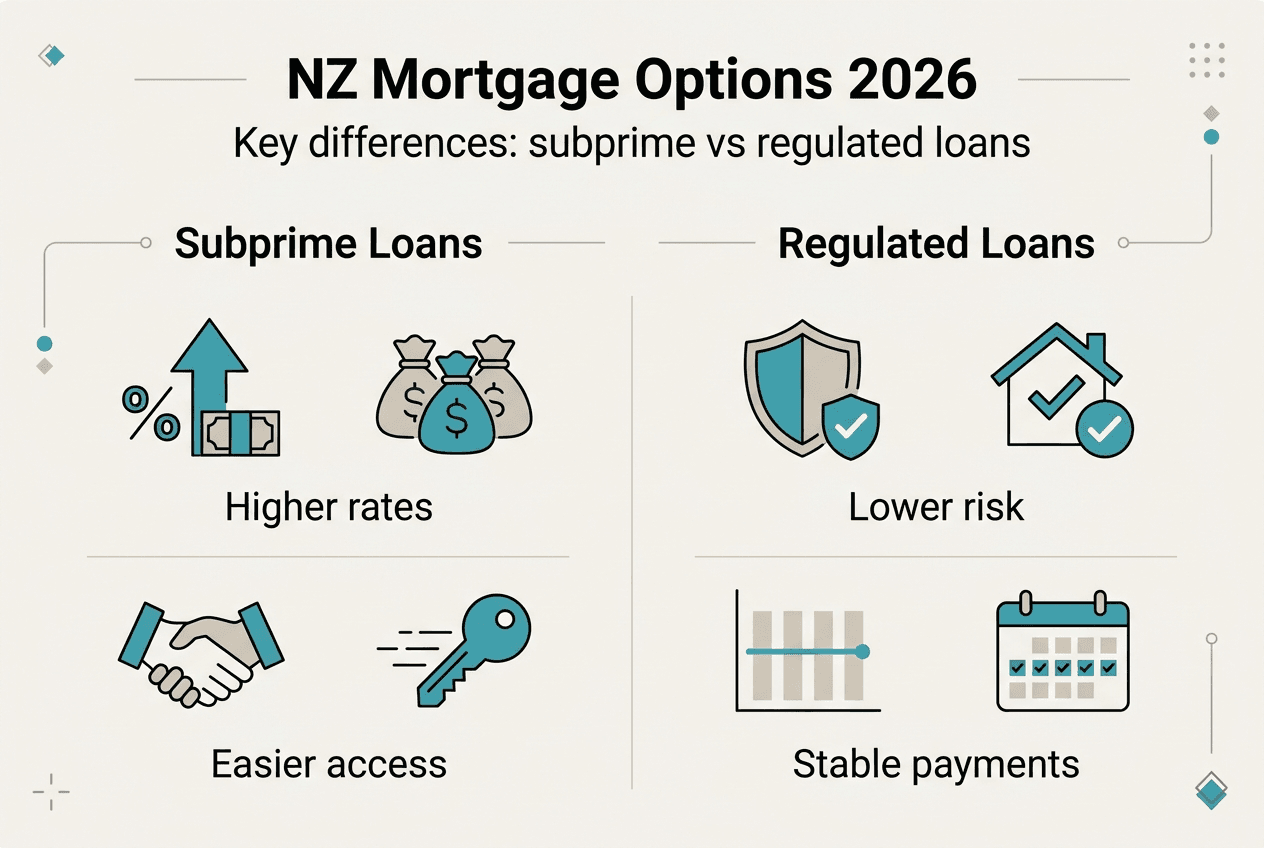

Comparing loan options: subprime mortgages versus regulated NZ home loans

Directly comparing subprime mortgages against New Zealand’s regulated alternatives clarifies which route suits your situation and financial capacity. The table below contrasts key features to help you evaluate trade-offs between higher-risk subprime products and safer government-backed or guarantor options.

Loan option comparison:

| Feature | Subprime mortgages | Kāinga Ora First Home | Guarantor loans | Bad credit specialists |

|---|---|---|---|---|

| Minimum deposit | 15 to 25 percent | 5 percent | 10 to 15 percent | 10 to 20 percent |

| Interest rates | 3 to 5 percent above standard | Standard market rates | Standard to 1 percent above | 1 to 3 percent above standard |

| Credit requirements | Poor credit accepted | Good credit required | Flexible with guarantor | Poor credit considered |

| Income caps | None typically | $95k single, $150k couple | Varies by lender | None typically |

| Key risks | High costs, payment shocks | Strict eligibility | Family relationship strain | Higher long-term costs |

Contrasting perspectives show subprime enables homeownership for credit-impaired borrowers but faces criticism for predatory terms and lax screening that contributed to the 2008 crisis. New Zealand’s focus on regulated alternatives like guarantors and low-deposit schemes provides inclusion without the extreme risks that characterised American subprime lending.

Pro Tip: Calculate the total interest paid over your full loan term for each option, not just monthly payments, to understand the true cost difference between choices.

Pros and cons of each loan type:

Subprime mortgages pros: Access to homeownership despite poor credit, potential to refinance later after building equity and improving credit. Subprime mortgages cons: Significantly higher costs, risk of payment increases with adjustable rates, potential for predatory terms, limited consumer protections.

Regulated NZ alternatives pros: Government backing or family support reduces risk, standard market rates keep costs manageable, consumer protections prevent predatory practices, opportunity to build credit for future refinancing. Regulated NZ alternatives cons: Stricter eligibility requirements, income caps may exclude higher earners, guarantors assume financial risk, limited lender options for bad credit.

Guarantor and low-deposit options help you build equity and improve your credit profile over time, positioning you to refinance to better terms once you’ve demonstrated responsible repayment. This creates a pathway from limited credit to mainstream lending that subprime mortgages often fail to provide due to their high costs consuming your income.

Understanding loan terms fully protects you from predatory pitfalls. Read all documentation carefully, ask questions about anything unclear, and never sign under pressure. Legitimate lenders give you time to review terms and seek independent advice. If a lender rushes you or discourages getting professional guidance, consider it a red flag.

Mortgage advisers personalise loan selection by matching your specific situation to suitable lenders and products. They explain trade-offs between options, help you understand what different terms mean for your finances, and advocate for you during the application process. This support proves especially valuable when navigating mortgage features NZ first-time buyers need to understand before committing to a 25 or 30 year loan.

How mortgage advisers can help first-time buyers with credit challenges

Navigating home loans with limited or poor credit requires expertise that most first-time buyers lack. Mortgage advisers specialise in matching clients to suitable lenders, including options beyond mainstream banks that consider your full financial picture rather than just credit scores. They understand which lenders accept specific credit issues, how recent your credit problems need to be to matter, and how to structure applications to maximise approval chances.

Mortgage Managers brings deep knowledge of New Zealand’s lending landscape, connecting Auckland and nationwide clients to appropriate loan products regardless of credit challenges. Their advisers work as mortgage advisers your personal shoppers for a home loan, researching options across multiple lenders to find solutions that fit your situation. This personalised approach identifies opportunities you’d miss applying directly to banks.

Expert guidance proves invaluable when improving your borrowing position. Advisers provide specific recommendations on paying down debts, timing applications, and building savings to strengthen your profile. They help you understand realistic timeframes for achieving mortgage approval based on your current credit status. Starting this conversation early, ideally 6 to 12 months before you want to buy, gives you time to implement their suggestions and maximise your options.

Whether you’re exploring bad credit home loans or need strategies to rebuild credit for mortgage NZ applications, professional advice tailored to your circumstances increases your chances of homeownership success while avoiding costly mistakes.

Frequently asked questions

What credit score defines a subprime borrower?

Subprime borrowers typically have credit scores between 580 and 669, though exact thresholds vary by lender and loan type. Scores below 580 often result in loan rejection entirely, while scores above 670 generally qualify for prime lending with standard rates. Your credit score reflects your payment history, debt levels, credit utilisation, and length of credit history, with recent behaviour weighing most heavily in lending decisions.

Can first-time Kiwi buyers with poor credit get a home loan?

Yes, but options are more limited and often require additional support or higher deposits. Guarantor arrangements where family members back your loan provide the most common pathway, allowing you to access standard rates despite credit challenges. Some specialist lenders offer bad credit home loans with higher interest rates but more flexible credit criteria. Government schemes like Kāinga Ora typically require good credit despite low deposit requirements, making them unsuitable for poor credit applicants.

What are the key risks of subprime mortgages in New Zealand?

Higher interest rates significantly increase your total repayment amount and monthly payment burden, raising the risk of financial stress and default. Adjustable rate mortgages common in subprime lending can see your payments spike when rates reset, potentially making your loan unaffordable. Limited consumer protections compared to regulated loan products leave you more vulnerable to predatory terms. The combination of high costs and payment uncertainty makes subprime mortgages risky for buyers already facing financial challenges.

How can mortgage advisers support those with limited credit?

Advisers identify suitable lenders and loan products that consider your full financial situation beyond just credit scores, accessing specialist lenders that don’t advertise publicly. They explain complex loan terms in plain language, helping you understand exactly what you’re committing to and how different features affect your finances. Advisers provide credit rebuilding strategies specific to mortgage lending requirements, giving you actionable steps to improve your position. Their lender relationships and application expertise often secure approvals that direct applications would miss.