TL;DR:

- Guarantors legally commit to cover mortgage repayments if the borrower defaults, risking their assets.

- Risks include reduced borrowing capacity, potential property sale, and long-term financial and relational impacts.

- Always negotiate limited guarantees and seek independent legal advice to protect all parties involved.

Understanding a guarantor’s role for your first home in NZ

Buying your first home in New Zealand is exciting, but let’s be honest: the deposit hurdle alone can feel impossible. Many first home buyers look to a guarantor as the answer, assuming it is a simple, low-risk arrangement that unlocks the door to homeownership. The reality is far more layered. Guarantor agreements carry genuine legal weight, significant financial exposure for the person stepping in to help, and consequences that can ripple through family relationships for years. This guide will walk you through exactly what a guarantor does, what the real risks look like for everyone involved, and what options you might explore before signing anything.

Table of Contents

- What is a guarantor and how do they help first home buyers?

- Key risks and responsibilities for guarantors

- Understanding limited vs unlimited guarantees and legal protections

- Alternatives to guarantors: Exploring other ways to secure your home loan

- Our perspective: Why real transparency matters for home loan guarantors

- Need help navigating guarantor home loans in New Zealand?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Guarantors boost home loan chances | Having a guarantor can help first home buyers in New Zealand borrow more or with a smaller deposit. |

| Risks can be significant | Guarantors are legally responsible if the borrower defaults and may risk their own financial stability. |

| Limit guarantees where possible | Negotiating a limited guarantee and seeking independent legal advice is critical for protection. |

| Alternatives exist | Cash gifts, loans, and joint ownership can also help home buyers secure a loan without a guarantor. |

What is a guarantor and how do they help first home buyers?

A guarantor is a person who formally agrees to cover your mortgage repayments if you are unable to meet them yourself. In legal terms, they are putting their own financial position on the line so that your lender feels confident enough to approve your loan. Think of it like a safety net beneath a tightrope walker: the guarantor is not doing the walking, but they are the one who catches the fall if things go wrong.

In New Zealand, this arrangement most commonly involves parents using the equity in their own home as security for their child’s mortgage. Rather than needing a full 20% deposit, a first home buyer might only need a small deposit or none at all, because the guarantor’s property effectively tops up the security offered to the bank. This can be a genuine game-changer for buyers who have strong income and repayment ability but simply haven’t had enough time to save a large deposit.

There are different types of guarantors you can explore, and understanding the distinctions matters greatly. Here is what a guarantor arrangement can typically help you achieve:

- Access the property market sooner by covering the shortfall in your deposit

- Avoid paying Lenders Mortgage Insurance (LMI), which can add thousands of dollars to your loan costs

- Borrow a higher amount relative to your deposit, giving you more purchasing power

- Secure more competitive interest rates because the lender views the loan as less risky with added security

- Demonstrate stronger loan serviceability to lenders who might otherwise decline your application

NZ banks have specific requirements for guarantor agreements. They will generally assess the guarantor’s financial position independently, check their own mortgage obligations, and confirm they have sufficient equity. The bank wants to be certain the guarantor genuinely has the capacity to cover the debt if called upon.

Pro Tip: Before approaching a family member to act as guarantor, speak to a mortgage adviser about your complete home loan options first. You may qualify for more than you think, and a guarantor might not even be necessary.

It is also worth noting that risks of guaranteeing a home loan extend well beyond the obvious. If you default, the bank can pursue the guarantor first, sell their property to recover the debt, and impact their borrowing capacity. Alternatives such as cash gifts, parental loans, deposit top-ups, and joint ownership arrangements are often worth exploring before committing to a formal guarantee.

Key risks and responsibilities for guarantors

After laying out the positives and how guarantors can help, it is essential to address the real risks and responsibilities involved. This is where many families make costly assumptions, believing that agreeing to be a guarantor is largely symbolic or a formality. It is not.

Here are the major risks every guarantor must understand before signing:

- Legal liability comes first. Banks have the legal right to pursue the guarantor for repayment before they even chase the primary borrower. You could be responsible for debt that is not technically yours to begin with.

- Your own borrowing capacity is reduced. Once you sign a guarantee, lenders treat that obligation as an existing debt on your record. This can severely limit your ability to refinance, take out new loans, or even increase your own mortgage.

- Your property can be sold. In a worst-case default scenario, the bank can pursue the guarantor and sell the guarantor’s property to recover the outstanding loan balance. This is not a theoretical risk; it happens.

- Chain guarantees multiply your exposure. If you sign an unlimited guarantee and the borrower has other debts with the same lender, you may find yourself liable for far more than just the home loan.

- Your credit history can be damaged. Long-term financial reputation and credit scores may suffer if the borrower defaults and recovery action is taken against you.

Important: Guaranteeing a loan is a serious legal commitment. Before signing, every guarantor must understand that they are not simply lending their name. They are pledging their financial security, their assets, and potentially their retirement savings.

The relationship dimension is also worth considering. Even when both parties have the best of intentions, financial stress has a way of straining even the closest family relationships. Missed repayments, lifestyle changes, or a shift in the borrower’s circumstances can create tension and resentment that outlasts the loan itself.

You should also consider risks of going guarantor carefully if you are the parent being asked to help. Your own financial future, including retirement planning and future property purchases, may be affected in ways that are not immediately obvious. The key takeaway: get a clear, honest picture of the borrower’s financial stability and repayment capacity before agreeing to anything.

Financially speaking, guarantors should also map out what happens at various stages. What if the borrower loses their job? What if interest rates rise significantly? What if the property value falls and the loan goes into negative equity? These are not catastrophising scenarios; they are planning questions every prudent guarantor must answer before committing.

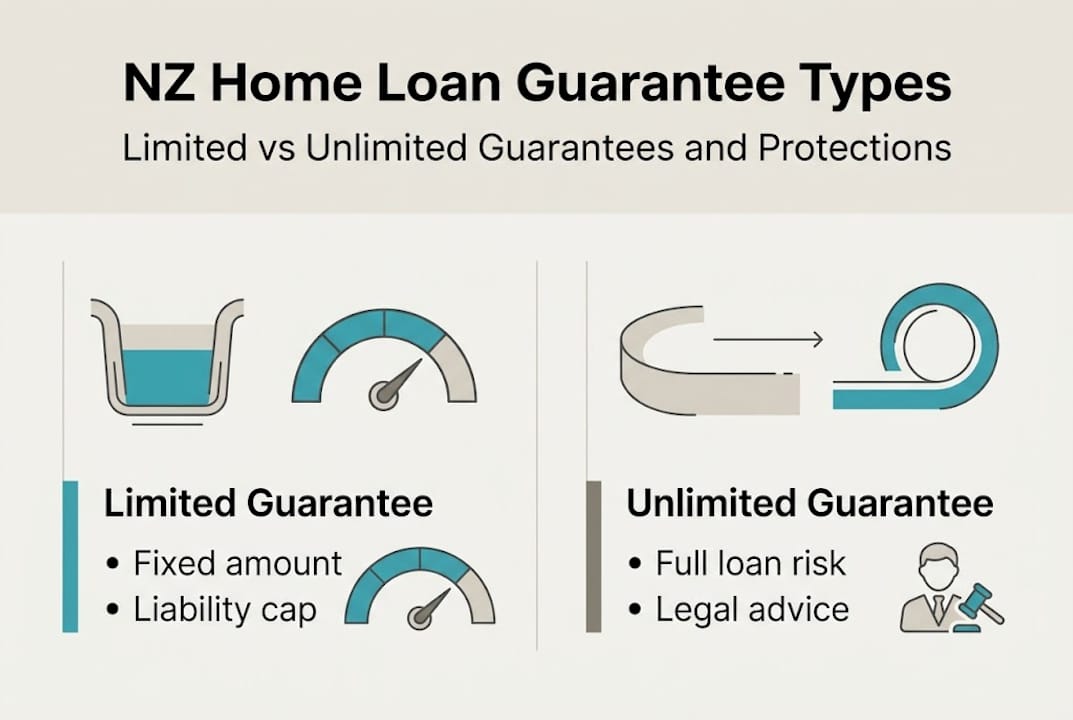

Understanding limited vs unlimited guarantees and legal protections

Having reviewed the risks, let’s clarify what kinds of guarantees exist and how you can shield yourself or your guarantor from unnecessary danger. Not all guarantees are created equal, and choosing the right structure can be the difference between a manageable obligation and a financial catastrophe.

A limited guarantee caps the guarantor’s liability at a specific dollar amount. For example, if a buyer needs a $100,000 top-up to reach their deposit threshold, the guarantor’s liability might be limited to exactly that amount, plus interest. Once the borrower pays down enough of the loan to cover that shortfall from their own equity, the guarantee is released.

An unlimited guarantee, by contrast, exposes the guarantor to the full loan balance plus any associated costs, fees, and interest. The hidden danger here is chain guarantees. If the same lender holds multiple debts from the borrower, an unlimited guarantee could theoretically cover all of them, not just the home loan.

Here is a clear comparison to help you understand the difference:

| Feature | Limited guarantee | Unlimited guarantee |

|---|---|---|

| Liability cap | Yes, fixed amount | No, full loan balance |

| Chain guarantee risk | Low | High |

| Release conditions | Clearer and defined | Often more complex |

| Recommended? | Yes, strongly | Avoid if possible |

| Common with NZ banks? | Increasingly preferred | Less common post-reform |

NZ lending reforms have made unlimited guarantees harder to arrange, but they have not eliminated them entirely. This is why it remains critical to negotiate limited guarantee terms from the outset rather than accepting whatever the lender presents.

Independent legal advice (ILA) is not just a recommendation; in most NZ guarantee arrangements, it is mandatory. Banks require guarantors to seek independent legal advice and sign a certificate confirming they have done so. This protects both parties: the guarantor cannot later claim they did not understand what they signed, and the lender is protected from legal challenge.

Pro Tip: Always insist on a limited guarantee rather than an unlimited one. If the lender or borrower pushes back, treat that as a warning sign and consult your lawyer or mortgage adviser immediately.

The importance of ILA cannot be overstated. A qualified lawyer will walk through the exact nature of the obligation, explain the release conditions, and ensure the guarantor fully understands what they are committing to. This conversation alone has saved many families from devastating financial mistakes.

Alternatives to guarantors: Exploring other ways to secure your home loan

While guaranteeing is one route, it is worth understanding your other options before making a commitment. The good news is that there are several practical pathways that can help you secure your first home without placing someone else’s property at risk.

Here is a comparison of the most common alternatives:

| Option | How it works | Key consideration |

|---|---|---|

| Cash gift | Parent or family member gives you money outright | Not repayable; may have gift duty implications |

| Parental loan | Family member lends you the deposit | Repayable; lender may treat as existing debt |

| Deposit top-up | Combining KiwiSaver, savings, and other funds | Requires planning; reduces loan-to-value ratio |

| Joint ownership | You and a family member buy together | Shared liability; legal agreements essential |

| First Home Grant | Government support for eligible buyers | Income and purchase price caps apply |

According to advisers, alternatives to formal guarantees such as gifts, loans, deposit top-ups, and joint ownership arrangements have become increasingly favoured, particularly since recent lending reforms have made formal guarantees more complex to arrange.

Here is what you need to know about each option:

- Cash gifts are the cleanest option in terms of ongoing liability. Once the money is given, it is yours to use as a deposit. However, some lenders may ask for a statutory declaration confirming the gift is not repayable.

- Parental loans can work, but lenders will typically factor the repayments into your debt servicing calculations. This might actually reduce how much you can borrow, partially offsetting the benefit.

- Deposit top-ups through KiwiSaver First Home Withdrawal and the First Home Grant can be surprisingly powerful when combined with disciplined savings. Many buyers underestimate how much these programmes can contribute.

- Joint ownership gives parents a formal share in the property, which can feel more equitable but introduces complications around future sale, capital gains, and family dynamics.

Brokers increasingly note that post-lending reform, cash gifts and parental loans are often easier to facilitate than formal guarantees. This is worth weighing when you compare home loan options with a qualified adviser.

You should also consider loans for house deposits as a potential bridge strategy, though always assess repayment obligations carefully before proceeding. The right choice depends entirely on your personal financial situation, family dynamics, and long-term goals.

Our perspective: Why real transparency matters for home loan guarantors

Bringing together all these threads, what really separates safe, successful outcomes from costly mistakes? In our experience working with first home buyers across Auckland and greater New Zealand, the answer is almost always transparency and preparation.

Most families enter into guarantor arrangements with genuinely good intentions. Parents want to help. Children want to get into the market. But good intentions alone do not protect anyone from poorly structured agreements. We have seen situations where a parent signs an unlimited guarantee without fully realising the chain liability risk, only to find years later that their own refinancing plans are blocked or their retirement savings are at risk.

Negotiating a limited guarantee and insisting on independent legal advice are not bureaucratic box-ticking exercises. They are acts of genuine care for everyone involved. Open and honest conversations about what happens if repayments become difficult, or if circumstances change, are just as important as the paperwork itself.

Our honest advice: do not just sign the documents because the bank puts them in front of you. Understand every clause, every obligation, and every exit condition. The first home buyer deserves a solid start, and the guarantor deserves to know exactly what they are agreeing to.

Need help navigating guarantor home loans in New Zealand?

If everything you have read so far feels a little overwhelming, you are not alone. Guarantor arrangements and the alternatives around them can be genuinely complex, and the stakes are high for everyone involved. That is exactly why speaking to an experienced mortgage adviser early in your journey makes such a difference.

At Mortgage Managers, we work with first home buyers every day, helping them understand their options clearly and confidently. Whether you are weighing up a guarantor arrangement or exploring alternatives like gifts or joint ownership, we can help you find a mortgage adviser who understands the NZ lending landscape. You can talk to a mortgage broker from our Hobsonville base, servicing West Auckland, the North Shore, and beyond. Ready to take the next step? Apply for a home loan today and let us guide you forward.

Frequently asked questions

Can a guarantor be released from a home loan in New Zealand?

A guarantor can typically be released from a guarantee once the borrower has built enough equity or demonstrated consistent repayment behaviour, but the lender must formally approve the change. The timeline varies depending on property value growth and how quickly the borrower reduces the loan balance.

Does acting as a guarantor affect your own ability to borrow?

Yes. Banks treat guarantee obligations as existing debts, which directly reduces your borrowing capacity for any future loans you may need. This is one of the most commonly overlooked consequences of agreeing to be a guarantor.

What happens if the main borrower defaults on a loan with a guarantor?

The lender may pursue the guarantor for repayment and can even sell the guarantor’s property to recover the outstanding debt. This can happen before the lender takes action against the primary borrower.

Are there statistics on default rates for guarantor loans in New Zealand?

There are no specific published figures for NZ guarantor loans, but comparable Australian schemes showed default rates dropping from around 15% to 8% over time, suggesting that structured support programmes can meaningfully reduce risk when properly designed.

Should a guarantor always get legal advice before signing?

Yes, independent legal advice is strongly recommended and often required by NZ lenders to ensure all parties genuinely understand their obligations before the guarantee is formalised. Skipping this step is one of the most avoidable and costly mistakes a guarantor can make.