In times of crisis a mortgage holiday seems like a great idea.

The Government have announced that the banks will be offering a 6-month mortgage holiday to home owners to help them survive financially through the COVID-19 crisis and it was received well by the public.Of course, for many families the mortgage repayments are one of the biggest regular expenses so the thought of not having to make that payment definitely is appealing and in some cases almost essential.

Kiwis are concerned about their finances.

A mortgage holiday seems like a gift … but is it really?

How Mortgage Holidays Work

Firstly, we would point out that while mortgage holidays can seem like a gift the banks are not actually giving away anything. In fact, the way mortgage holidays work will see the banks earn more money from you.

With a mortgage you would generally be paying principal and interest so over time the money that you owe the bank reduces.

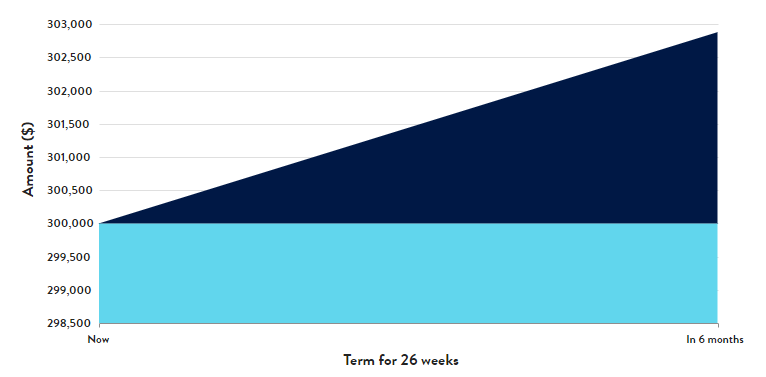

Consider this;

You have a $300,000 mortgage at 3.99% and your weekly repayment would be $344 over a 30-year loan term. The interest that you pay is $230 of that, meaning you will reduce your loan by $114 in that week. The interest that you pay to the bank is what they make from you, less what they pay someone for that money.

If you did not make that weeks payment because the bank gave you a “mortgage holiday” then your loan balance would increase by $230 and so when you make a payment the next week your loan balance has increased to $300,230 and therefore your repayment has increased to $345.

It seems like a small increase, but over time this grows exponentially.

In 6-months your loan has increased by $2,880.29 or an average of just over $110 weekly.

A mortgage holiday can be expensive.

In the example here your mortgage has increased by over $110 every week.

That means you have increased your mortgage and will have to repay that money again with interest.

What Are Your Options?

If your income has been severely limited then you may not have a lot of options, but if you still have a secure job and income then you do have choices.

Speak to your mortgage adviser and they can explain all the options.

Yes, a mortgage holiday may be the best option but you should consider what suits you rather than just taking the “easy option” that is being offered.

You should be considering your overall financial position including any other debt and your future income when you are able to return to work.

If you have other debt then a top up will leave you in a better financial position.

If your income is continuing then you would be better to reduce your repayments or switch to paying just interest only.

Switching to the lower home loan interest rates on offer now may be better, or refinancing to a more suitable home loan.

Don’t just default to a mortgage holiday before speaking to an adviser and considering all options.