TL;DR:

- A loan term is the total duration to repay the full mortgage, up to 30 years in NZ.

- Fixed-rate periods are short-term rate locks, separate from the overall loan term.

- Shorter loan terms reduce total interest paid but require higher monthly repayments.

Many New Zealanders confuse ‘loan term’ with their fixed-rate period, and this mix-up can quietly cost thousands of dollars over the life of a mortgage. These two concepts are closely related but serve very different purposes in your mortgage planning. Understanding the difference is not just a technical exercise. It is the foundation of every smart borrowing decision you will make. In this guide, we break down what a loan term actually means in New Zealand, how it compares to fixed-rate periods, and how you can use this knowledge to structure your home loan with confidence.

Table of Contents

- What does ‘loan term’ mean in New Zealand?

- Loan term vs. fixed-rate period: Key differences

- How loan term length impacts repayments and total interest

- NZ loan term strategies: Short vs long, fixed vs floating

- A perspective: Why focusing on the loan term, not just the rate, pays off

- Get expert help to optimise your loan term

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Loan term shapes costs | How long you take to repay your mortgage directly impacts your monthly repayments and total interest paid. |

| Fixed period ≠ loan term | The fixed-rate period only sets your interest for a short time—your total loan term is usually much longer. |

| Shorter terms save money | If you can manage higher repayments, opting for a shorter loan term greatly reduces total interest costs. |

| Pick strategy carefully | Mix loan terms and fixed periods to suit your goals, budget, and market conditions. |

What does ‘loan term’ mean in New Zealand?

Let’s start with the most basic but most misunderstood question.

A loan term in New Zealand is the total duration you agree to repay the full principal and interest on your home loan. Think of it as the entire length of your mortgage journey, from the day you draw down funds to the day you make your final repayment. It is the big picture timeframe, not a short window within it.

Standard home loan terms in NZ run up to 30 years for table loans, which are the most common loan structure used by Kiwi borrowers. A table loan means your repayments stay consistent throughout the term, though the proportion going to interest versus principal shifts over time. In the early years, most of your repayment covers interest. As the years pass, more of each payment chips away at the principal.

Here is what your loan term shapes:

- Total interest paid over the life of the loan

- Monthly repayment amount and how much budget pressure you carry

- Equity build-up and how quickly you own more of your home

- Borrowing eligibility, since lenders assess your age and income against the full term

- Financial flexibility when life circumstances change

It is worth noting that your loan term is not the same as your fixed-rate period. Many borrowers assume that when their two-year fixed rate ends, their loan is somehow reset or renegotiated from scratch. It is not. Your loan term keeps running in the background, regardless of how many times you re-fix or switch to a floating rate. Explore the full range of NZ home loan types to understand how different structures interact with your term.

Pro Tip: If you are 35 years old and take out a 30-year loan, you will be 65 before it is fully repaid. Choosing a 25-year term instead could mean entering retirement with no mortgage at all.

The loan term you choose at the start is one of the most consequential decisions in your entire mortgage journey. It deserves just as much attention as the interest rate.

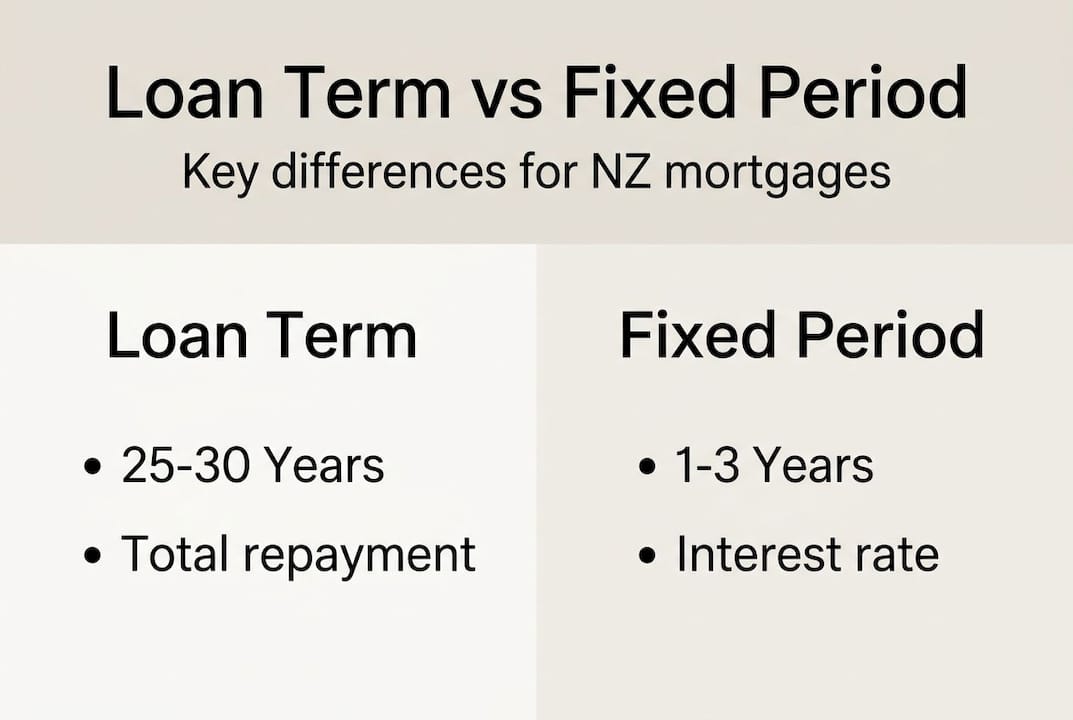

Loan term vs. fixed-rate period: Key differences

With the full loan term now defined, it is crucial to see how it fits alongside fixed and floating rate choices.

Loan terms must be distinguished from fixed-rate periods. A fixed-rate period is a short window, typically 6 months to 5 years, during which your interest rate is locked in and cannot change. Your overall loan term, by contrast, can be up to 30 years. These two things run on completely different clocks.

| Feature | Loan term | Fixed-rate period |

|---|---|---|

| Duration | 25 to 30 years | 6 months to 5 years |

| Purpose | Full repayment timeline | Rate certainty window |

| Changes at end | Loan is repaid | Re-fix, float, or restructure |

| Affects repayments | Yes, significantly | Yes, when rate changes |

| Affects total interest | Yes, major impact | Yes, moderate impact |

When your fixed-rate period ends, you have options. You can re-fix at a new rate, switch to a floating rate, or restructure your loan entirely. None of these actions change your original loan term unless you specifically refinance to a new term. Your repayment options at this stage are worth reviewing carefully.

Historically, shorter fixed terms of 1 to 2 years have been cheaper in total interest than longer fixed terms of 3 to 5 years. That said, longer fixed periods offer predictability, which has real value when budgeting for a family or managing a tight cash flow. The impact on interest rates of your chosen fix length is something worth modelling before you commit.

For a deeper look at this decision, the fix vs float comparison from Consumer NZ is a solid reference.

Pro Tip: When you are approaching the end of a fixed period, start reviewing your options at least 6 to 8 weeks before rollover. Lenders often allow you to lock in a new rate ahead of time, which can protect you from sudden rate rises.

Understanding these two concepts as separate but connected levers gives you real control over your mortgage.

How loan term length impacts repayments and total interest

Now that you know the terms, let’s see how length really changes your financial picture.

Longer loan terms mean lower monthly repayments but significantly higher total interest, because early repayments are weighted heavily toward interest rather than principal. This is the trade-off at the heart of every mortgage decision.

Consider this real-world NZ scenario using a $500,000 loan at a 6.5% interest rate:

| Loan term | Monthly repayment | Total repaid | Total interest paid |

|---|---|---|---|

| 30 years | $3,160 | $1,137,600 | $637,600 |

| 25 years | $3,370 | $1,011,000 | $511,000 |

| 20 years | $3,730 | $895,200 | $395,200 |

The difference between a 30-year and 20-year term on this loan is over $242,000 in total interest. That is a significant sum. For just $570 more per month, you could save nearly a quarter of a million dollars over the life of your loan.

Here is how to think about the key trade-offs:

- Shorter terms mean higher monthly repayments but dramatically lower total interest

- Longer terms ease monthly cash flow but cost far more over time

- Extra repayments on a longer-term loan can bridge the gap if your income grows

- Refinancing to a shorter term later is possible but comes with fees and reassessment

Some borrowers also consider interest-only periods, where you pay only the interest for a set time and none of the principal. Interest-only periods reduce repayments short-term but increase long-term costs, and owner-occupiers face stricter eligibility criteria. They can suit investors managing cash flow, but they are rarely the right fit for first home buyers. Learn more about the interest-only loan pros and cons before considering this path.

Use a repayment calculator to calculate your repayments across different scenarios so you can see the numbers clearly before you commit.

NZ loan term strategies: Short vs long, fixed vs floating

Armed with these insights, how should Kiwis actually structure their loans for best results?

The honest answer is that there is no single right answer. But there are principles that hold up well across most situations.

Choosing a shorter overall term is the most effective way to minimise total interest, provided you can manage the higher repayments comfortably. A 20-year term is not out of reach for many dual-income households, and the long-term savings are substantial.

When it comes to fixed periods, floating rates allow extra repayments with no penalty, which makes them ideal for borrowers who receive bonuses or irregular income. Fixed periods, on the other hand, offer peace of mind against rate rises and make budgeting predictable.

Here are the most common strategies Kiwi borrowers use:

- Short term, short fix: Maximise interest savings and stay nimble with rate changes. Best for financially stable borrowers with strong income.

- Long term, short fix: Keep repayments manageable while still benefiting from competitive short-term rates. Common for first home buyers.

- Split structure: Fix half your loan for certainty and keep the other half floating for flexibility. A popular middle-ground approach.

- Long term, long fix: Lock in certainty for 3 to 5 years. Useful when rates are expected to rise, though historically more expensive overall.

“The best loan structure is the one that fits your life, not just the current rate environment. Revisit your structure every time your fixed period ends.”

Pro Tip: Review your mortgage repayment strategies annually, not just at rollover. Your income, expenses, and goals change, and your loan structure should keep pace with them.

For first home buyers, understanding the loan features available can make a real difference to how you structure your first mortgage. And if you want to compare loan structures side by side, a step-by-step guide can help you visualise your options clearly.

A perspective: Why focusing on the loan term, not just the rate, pays off

Here is something we see again and again working with borrowers across Auckland and throughout New Zealand. People spend enormous energy chasing the best interest rate, sometimes moving lenders for a difference of 0.1%. Yet those same people rarely stop to ask what would happen if they simply shortened their loan term by five years.

The maths is confronting. On a $500,000 loan, five fewer years can mean over $100,000 in savings, depending on the rate environment. That is not a marginal gain. It is a life-changing sum.

Mortgage statements do not make this easy to see. The compounding effect of term length is buried in the fine print, and lenders rarely volunteer the comparison. This is where having a trusted adviser becomes genuinely valuable.

If you can afford slightly higher repayments today, treating that extra commitment as an investment in future equity and security is one of the most powerful financial moves available to you. Rates matter, but time in the loan matters more. Start by understanding how to prepare for a home loan so you can enter the conversation with lenders from a position of strength.

Get expert help to optimise your loan term

Choosing the right loan term and structure is one of the most impactful financial decisions you will make. It deserves more than a quick online comparison.

At Mortgage Managers, our advisers work through the numbers with you, comparing scenarios across multiple lenders to find the structure that genuinely suits your goals. Whether you are buying your first home in Auckland or refinancing a property anywhere in New Zealand, personal home loan help from an experienced adviser can mean the difference between paying off your loan years early or carrying unnecessary debt into retirement. Visit Mortgage Managers to connect with a local adviser who will guide you every step of the way.

Frequently asked questions

What is the typical loan term for a NZ home loan?

Most New Zealand home loans have terms between 25 and 30 years, with 30 years as the usual maximum for table loans offered by most lenders.

Can you change your loan term after taking out a mortgage?

Yes, you can refinance to a shorter or longer term at any point, though this may affect your repayments, total interest paid, and may involve break fees or application costs.

Does a longer loan term mean lower repayments?

A longer loan term does reduce your monthly repayments, but total interest paid increases significantly because you are borrowing for a longer period.

How often do you need to re-fix your interest rate in New Zealand?

Most fixed-rate periods last from 6 months to 5 years, though 1 to 3 years is most common, meaning you typically re-fix every couple of years while your overall loan term continues running.

Is it better to choose a shorter fixed period for your mortgage?

Shorter fixed terms of 1 to 2 years have generally been more cost-effective over time, though the right choice depends on current rates, your financial goals, and your tolerance for rate uncertainty.