TL;DR:

- Offset accounts reduce mortgage interest by linking savings directly to the loan principal.

- They offer high flexibility and tax advantages over redraw facilities and savings accounts.

- Consistent use and strategic management maximize long-term savings and shorten loan terms.

Most Kiwi homebuyers assume their mortgage interest is simply a fixed cost of borrowing, something to endure rather than manage. But that assumption can cost you tens of thousands of dollars over the life of your loan. Offset accounts quietly change the rules, allowing your everyday savings to work directly against your mortgage interest. Whether you’re buying your first home in Auckland or refinancing an investment property on the North Shore, understanding how offset accounts function could be one of the most valuable financial moves you make. This guide breaks down everything you need to know, in plain language, so you can decide if an offset account belongs in your mortgage strategy.

Table of Contents

- Defining an offset account

- Offset vs redraw vs savings: What’s the difference?

- Who should use an offset account?

- Making the most of your offset account

- The truth about offset accounts most Kiwis miss

- How a mortgage adviser can help you leverage offset accounts

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| What offset accounts do | An offset account reduces the interest you pay on your home loan by using your savings to offset the mortgage principal. |

| Who can benefit | Homebuyers with savings or steady income streams can cut years off their loan with disciplined offset usage. |

| Common confusions | Offset accounts are distinct from redraw facilities and regular savings accounts—with unique features and access rules. |

| Making it work | Regularly moving every spare dollar into your offset and keeping spending separate maximises your interest savings. |

Defining an offset account

Before we get into strategies, it’s important to strip back the jargon and pin down what an offset account actually is.

An offset account is a savings or transaction account that is formally linked to your home loan. The balance sitting in that account is used to reduce the portion of your loan on which interest is calculated. So if your home loan balance is $500,000 and you have $30,000 in your offset account, you only pay interest on $470,000. That difference adds up significantly over a 25 to 30 year mortgage.

Offset accounts operate by offsetting the savings account balance against the home loan principal, rather than crediting interest to your savings. This is a crucial distinction. You don’t earn interest on the money in your offset account. Instead, that money reduces the interest you owe. The net effect is the same as earning interest, but the mechanism is different, and the tax implications are friendlier.

Here’s how it plays out day to day:

- Your salary lands in your offset account on payday

- Your full account balance immediately reduces your loan’s interest calculation

- As you spend throughout the month, your balance drops and your interest offset reduces slightly

- Even on days when your balance is lower, every dollar is still working for you

- At the end of the month, your interest charge reflects the average daily balance in your offset account

This is why offset accounts are popular with homebuyers who want full access to their cash without locking it away. Your money stays liquid, available for groceries, school fees, or emergencies, while simultaneously chipping away at your mortgage interest every single day.

Pro Tip: Route all regular income, including your salary, rental income, or freelance payments, into your offset account first. Even if the money only sits there for a week before you spend it, every day it reduces your loan interest.

The beauty of this structure is its simplicity. You don’t need to make extra repayments or restructure your loan to benefit. You simply keep your money in the right place, and the maths does the rest for you.

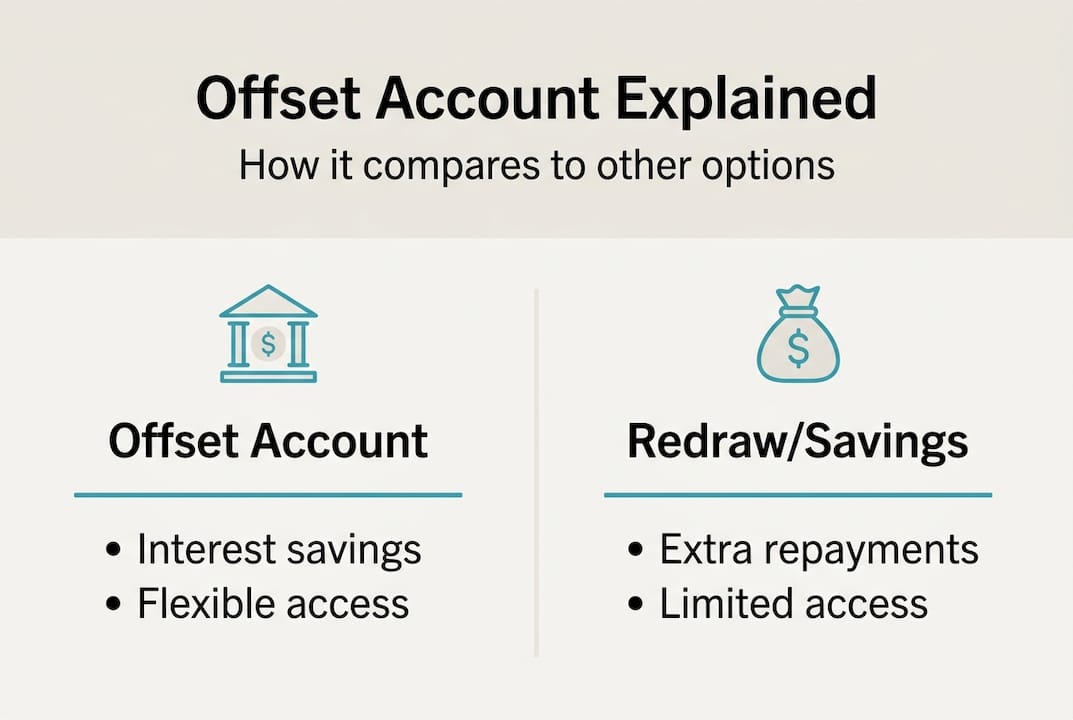

Offset vs redraw vs savings: What’s the difference?

Having established what an offset account is, it’s natural to wonder how it stacks up against similar-sounding home loan features.

Many borrowers confuse offset accounts with redraw facilities and regular savings accounts. They’re genuinely different tools, and choosing the wrong one for your situation can cost you money or flexibility. Understanding the offset mortgage benefits compared to alternatives helps you make a much smarter decision.

Here’s a clear side-by-side comparison:

| Feature | Offset account | Redraw facility | Savings account |

|---|---|---|---|

| Reduces mortgage interest | Yes | Yes (via extra repayments) | No |

| Instant access to funds | Yes | Sometimes delayed | Yes |

| Interest earned on balance | No | No | Yes |

| Tax on interest | No | No | Yes (on interest earned) |

| Flexibility | High | Moderate | High |

A redraw facility allows you to make extra repayments on your mortgage and then withdraw that money later if you need it. The key difference is access. Some lenders place restrictions on how quickly you can redraw funds, and some charge fees for each withdrawal. With an offset account, your money is always fully accessible, just like a regular bank account.

A regular savings account does earn interest, which sounds appealing. But that interest is taxable income in New Zealand. With an offset account, the interest you save is not taxable, because you’re not technically earning anything. You’re simply reducing a cost. Over a 25 year loan, that tax advantage compounds into a meaningful difference.

Here’s a numbered breakdown of how to think through the decision:

- If you want maximum flexibility and daily access, an offset account suits you best

- If you’ve already made extra repayments and want a safety net, a redraw facility is useful

- If you’re building a separate emergency fund outside your mortgage, a savings account makes sense

- If you’re focused on minimising total interest paid over the long term, an offset account typically wins

Many borrowers benefit from using a combination of these features, but the offset account is usually the centrepiece of a smart mortgage strategy.

Who should use an offset account?

Now you understand how offset accounts work and compare, let’s see who can make the most of these features.

Offset accounts aren’t a one-size-fits-all solution, but they suit a surprisingly wide range of Kiwi borrowers. The benefits of offset mortgages are especially powerful for homebuyers who carry meaningful savings or receive regular, predictable income.

Consider these typical profiles:

| Borrower type | Typical offset balance | Estimated annual interest saving |

|---|---|---|

| Young professional, $15,000 savings | $15,000 | $900 at 6% interest |

| Family with $40,000 in accounts | $40,000 | $2,400 at 6% interest |

| Investor with $80,000 cash flow | $80,000 | $4,800 at 6% interest |

These figures grow dramatically over time. A family maintaining $40,000 in their offset account over 25 years could save well over $50,000 in interest and shave years off their loan term. That’s a holiday fund, a children’s education, or a meaningful boost to retirement savings.

Borrowers with seasonal income, such as those in construction, tourism, or agriculture, also benefit strongly. During high-income months, their offset balance swells and their interest drops sharply. During quieter months, the balance may reduce, but the structure still works harder than a standard loan.

- Professionals with steady salaries who can keep balances consistently high

- Families consolidating multiple accounts into one offset structure

- Investors managing rental income alongside a home loan

- Self-employed borrowers with variable but healthy cash flow

- First-home buyers who want flexibility as their financial situation evolves

Even modest balances make a real difference. If you explore the best offset loan options available in New Zealand, you’ll find lenders who cater to a range of borrower types. And if you’re serious about speed, pairing an offset account with a plan to pay your mortgage off faster can produce remarkable results.

Pro Tip: On payday, transfer your entire salary into your offset account before moving spending money to a separate everyday account. Those extra days of a higher offset balance accumulate into real interest savings over the year.

Making the most of your offset account

Once you know if you’re a good fit, you need to make your offset account work as hard as possible.

Having an offset account and using it well are two very different things. Many borrowers set one up and then leave money scattered across multiple accounts, which dilutes the benefit. Here’s how to get the most from your structure:

- Consolidate all household funds into the offset account. The more money sitting in the account, the greater your interest reduction. Combine savings, emergency funds, and even short-term money you’re setting aside for bills.

- Keep a separate spending account with only what you need. Transfer your weekly or fortnightly budget to a separate account for daily expenses. This keeps your offset balance as high as possible for as long as possible.

- Review your lender’s fees and rules regularly. Some banks charge monthly account fees that can erode your savings. Make sure the interest saved outweighs any costs associated with maintaining the account.

- Avoid using your offset account as a redraw. Withdrawing large lump sums defeats the purpose. If you need to access funds, plan ahead and replenish the account quickly.

- Automate where possible. Set up automatic salary credits and automatic transfers for bills so your offset balance stays predictable and high.

Consistent higher balances in offset accounts can shave years off a home loan and save tens of thousands in interest over the full loan term. That’s not a small win. It’s a life-changing financial outcome for many Kiwi families.

“If a borrower maintains $20,000 in an offset account consistently over a 25 year mortgage at 6% interest, they could save more than $25,000 in interest and reduce their loan term by over two years. The discipline to keep that balance high is the real secret to making offset accounts perform.” — Mortgage Managers

You can also explore the offset loan mechanics in more detail to understand how your specific lender calculates daily interest, which can vary slightly between banks.

Pro Tip: Set a calendar reminder every six months to review your offset account balance, your lender’s fees, and whether your current structure still suits your financial situation.

The truth about offset accounts most Kiwis miss

Even equipped with facts and tips, many Kiwis overlook a few truths about how offset accounts affect real-world finances.

Here’s our honest perspective after working with hundreds of New Zealand homebuyers: an offset account is only as powerful as the habits behind it. We’ve seen borrowers set up a well-structured offset loan and then gradually let balances slip as spending creeps up, redraw gets used too freely, and the original discipline fades. The maths stops working in your favour the moment your balance drops.

The other thing most people miss is that offset accounts reward consistency, not perfection. You don’t need to maintain a huge balance every single day. You just need to be thoughtful and intentional about where your money lives. Regular reviews matter more than most borrowers realise.

Working with a trusted financial adviser can make an enormous difference here. An adviser doesn’t just help you choose the right loan. They help you build the cashflow habits that make an offset account genuinely transformative over the long term.

How a mortgage adviser can help you leverage offset accounts

If you want a shortcut to expert implementation and a tailored offset plan, working with a trusted adviser is your next step.

Choosing the right offset loan structure is more nuanced than it might appear. Lenders differ in how they calculate interest, what fees apply, and how flexible their offset arrangements are. A knowledgeable mortgage adviser can compare these options across multiple lenders and match you with a structure that fits your income, savings habits, and long-term goals.

At Mortgage Managers, we work with first-home buyers, growing families, and property investors across Auckland and throughout New Zealand. We understand that offset accounts are only valuable when they’re set up correctly and used with intention. Our team is here to guide you through every step, from choosing the right lender to building the cashflow strategy that makes your offset account perform at its best.

Frequently asked questions

Are offset accounts available with all New Zealand banks?

Not every bank offers offset accounts, so it’s important to compare lenders carefully. There are bank and non-bank lenders with different offset offerings worth exploring.

Is interest on offset accounts taxable in New Zealand?

No tax is paid on interest saved through an offset account, unlike interest earned on a regular savings account. This tax treatment advantage is one of the strongest reasons to choose an offset structure.

Can you access money in an offset account whenever you want?

Yes, in most cases your funds remain fully accessible for everyday spending, just like a regular transaction account. Offset accounts provide transaction flexibility that redraw facilities often cannot match.

What’s the main risk of using an offset account incorrectly?

Letting your offset balance fall too low means you miss out on meaningful interest savings. Maintaining healthy balances is the single most important factor in making an offset account work effectively for you.