TL;DR:

- Credit checks assess your financial behaviour to determine mortgage eligibility and interest rates.

- Regularly reviewing and improving your credit report can significantly boost approval chances.

- Approaching credit issues proactively and understanding how they influence lenders can help first home buyers succeed.

Your credit file might feel like a mystery, but it doesn’t have to be. For first home buyers in New Zealand, understanding how credit checks work is one of the most practical steps you can take towards securing a home loan. Many people assume that a past financial hiccup permanently closes the door on homeownership, but that’s simply not the case. Recent positive behaviour on your credit file carries more weight than old mistakes. This guide walks you through everything you need to know, from what a credit check actually involves to how you can use it as a tool to improve your mortgage prospects.

Table of Contents

- What is a credit check and why does it matter?

- The credit check process step-by-step

- What impacts your credit score and report the most?

- How credit checks affect your home loan application

- Our take: why credit checks should empower, not scare, first home buyers

- Get expert help with your mortgage journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Recent actions matter most | Lenders place higher value on your recent payment behaviour than old mistakes. |

| Know the process | Understanding how credit checks work gives you more control over your mortgage application. |

| Get your free report | You can request a free annual credit report in New Zealand to stay informed. |

| Credit checks shape loan offers | Your credit history directly influences the rate, approval and options you receive when buying a home. |

What is a credit check and why does it matter?

A credit check is a review of your financial history, conducted by a lender or authorised party to assess how reliably you manage money. In New Zealand, this information is held by credit bureaus such as Centrix, Equifax, and Illion. When you apply for a home loan, your lender will request a copy of your credit report to get a clear picture of your financial behaviour over time.

Lenders use credit checks to assess risk before offering a home loan. They want confidence that you’ll meet your repayment obligations every month for potentially 25 to 30 years. Your credit report gives them a window into your financial past, and what they find shapes their decision.

Here’s what typically appears on a New Zealand credit report:

- Payment history: Whether you’ve paid bills, loans, and credit cards on time

- Credit defaults: Any accounts sent to collections or formally recorded as unpaid

- Credit enquiries: How many times you’ve applied for credit recently

- Current credit accounts: Balances, limits, and account types you hold

- Public records: Bankruptcies or court judgements related to debt

Understanding why lenders reject applications often comes back to these very items. A pattern of late payments or multiple recent credit applications can signal financial stress to a lender, even if your income looks healthy on paper.

“Your credit file is not a verdict on your character. It’s a snapshot of your financial habits, and snapshots can change.”

The good news is that your credit score and home loans are more connected than most first home buyers realise. A stronger score doesn’t just improve your approval odds; it can also influence the interest rate you’re offered, which affects your repayments for decades.

Pro Tip: Pull your credit report before you start house hunting. Knowing where you stand gives you time to address any issues well before a lender sees your file.

The credit check process step-by-step

Now you understand why credit checks matter, let’s walk through what actually happens during the process. Knowing each stage removes the uncertainty and helps you feel prepared.

Here’s how a mortgage credit check typically unfolds in New Zealand:

- You apply for a home loan with a bank or lender, either directly or through a mortgage adviser.

- You provide consent for the lender to access your credit information. This is a legal requirement in New Zealand.

- The lender contacts a credit bureau such as Centrix, Equifax, or Illion to request your report.

- Your credit report is generated, showing your full credit history including defaults, enquiries, and payment behaviour.

- The lender assesses your report alongside your income, expenses, and deposit to make a lending decision.

- You receive an outcome: approval, conditional approval, or a decline with reasons you can act on.

You don’t have to wait for a lender to see your file first. Our credit assessment guide walks you through how to review your own position before applying. And if you find something concerning, there’s real guidance on how to fix your credit before you approach a lender.

One important right every New Zealander has is access to a free annual credit report from each registered bureau. This is mandated under New Zealand law and costs you nothing.

| Credit bureau | Free report available | Report request method |

|---|---|---|

| Centrix | Yes, annually | Online via centrix.co.nz |

| Equifax | Yes, annually | Online via equifax.co.nz |

| Illion | Yes, annually | Online via illion.co.nz |

Requesting your own report is classified as a “soft enquiry” and does not affect your credit score. Only applications for credit, known as “hard enquiries,” leave a mark on your file.

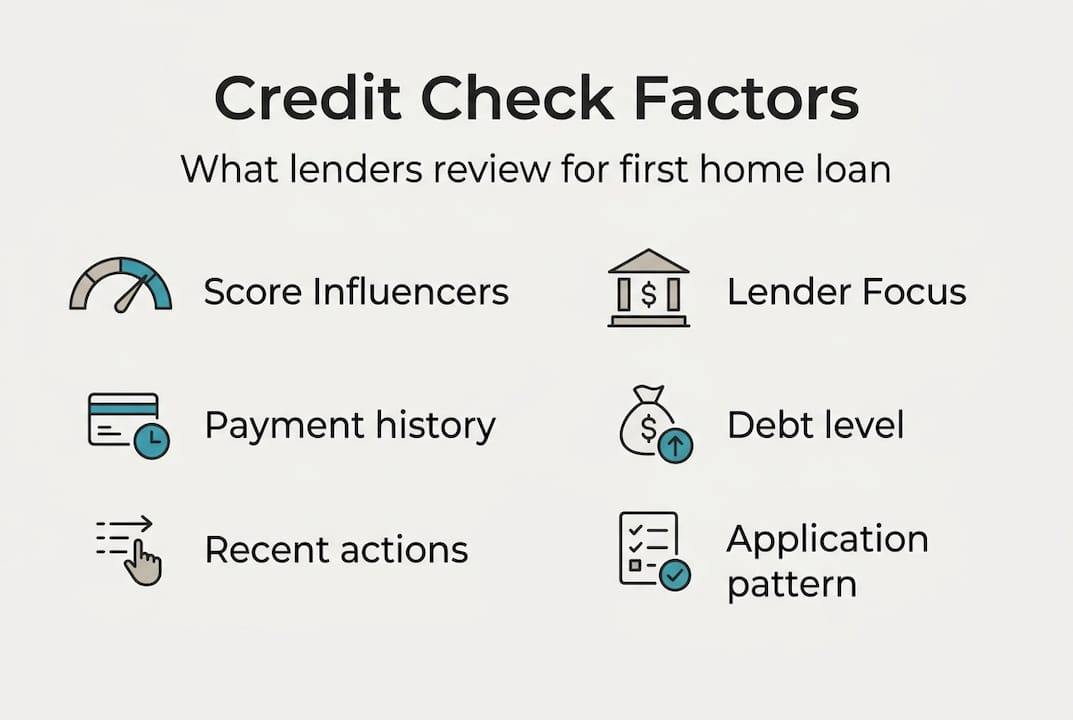

What impacts your credit score and report the most?

Having covered the process, it’s essential to know which factors have the biggest effect on your credit profile. Not all credit behaviours carry the same weight, and understanding this can help you focus your energy where it counts most.

Payment history dominates your score, and recent positive behaviour counts more than older negatives. This is genuinely encouraging news for first home buyers who may have had a rough patch a few years ago.

| Factor | Impact level | What it includes |

|---|---|---|

| Payment history | Very high | On-time vs. late payments across all accounts |

| Credit defaults | Very high | Unpaid debts, collections, court judgements |

| Recent credit enquiries | Moderate | Number of applications in the past 12 months |

| Credit utilisation | Moderate | How much of your available credit you’re using |

| Length of credit history | Lower | Age of your oldest and newest accounts |

Here’s what this means in practice for your credit score improvement:

- Paying every bill on time, even small ones like utilities, builds a positive pattern quickly

- Reducing your credit card balance below 30% of its limit signals responsible usage

- Avoiding multiple credit applications in a short period prevents a cluster of hard enquiries

- Keeping older accounts open, even if unused, supports the length of your credit history

Pro Tip: Set up automatic payments for recurring bills. One forgotten payment can take months to recover from, but automation makes it nearly impossible to miss a due date.

Understanding why credit history matters goes beyond just the score itself. Lenders look at the story your file tells. A consistent record of responsible behaviour, even over just 12 to 18 months, can shift the narrative significantly in your favour.

How credit checks affect your home loan application

With a strong grasp of credit score factors, you can now see exactly how these affect your chance of approval. The impact is real, and it touches more than just whether you get a yes or a no.

Lenders assess the risk of missed repayments and defaults based on your credit file. A clean, consistent file signals low risk. A file with gaps, defaults, or frequent enquiries signals higher risk, which lenders price accordingly.

Here’s how your credit profile directly influences your mortgage outcome:

- Approval likelihood: A strong credit file significantly increases the chance a lender says yes

- Loan amount: Lenders may offer a smaller loan to borrowers with weaker credit profiles

- Interest rate: Higher perceived risk can mean a higher rate, costing you more over the life of the loan

- Loan conditions: Some approvals come with conditions, such as a larger deposit requirement

- Lender choice: Borrowers with excellent credit have access to a wider range of lenders and products

“A lower credit score is not a full stop. It’s often a comma, with more of your financial story still to be written.”

Some buyers worry that past mistakes make homeownership impossible. The reality is more nuanced. If you’re exploring getting a home loan with bad credit, there are lenders who consider the full picture, including your employment stability, savings history, and the reasons behind any past defaults.

For buyers in Auckland and surrounding areas, understanding credit scores for Auckland buyers in the context of local property prices adds another layer of relevance. The higher the loan amount you need, the more scrutiny your credit file will face, which makes preparation even more worthwhile.

Recent improvements to your credit file genuinely matter. A lender reviewing your file in 2026 is far more interested in what you’ve done in the past 12 months than what happened four years ago.

Our take: why credit checks should empower, not scare, first home buyers

Here’s something we’ve observed working with first home buyers across Auckland and beyond: the fear of a credit check often does more damage than the credit check itself. Buyers delay applying, avoid seeking advice, and talk themselves out of opportunities because they assume their file is worse than it actually is.

Most buyers dramatically overestimate the permanence of a bad credit record. Credit files are living documents. They evolve with your behaviour, and lenders know this. The buyer who had a default three years ago but has since paid every bill on time, reduced their debt, and built a savings habit is a very different risk proposition than someone whose problems are current.

Our advice is straightforward: treat your credit file like a fitness tracker, not a report card. Check it regularly, act on what you find, and use any setbacks as information rather than judgement. Preparing your bank statements alongside your credit file gives you a complete picture of how a lender will see you. Buyers who approach the process proactively are always better positioned than those who wait and hope.

Get expert help with your mortgage journey

Understanding credit checks is a powerful first step, but navigating the full mortgage process is where personalised support makes a real difference.

At Mortgage Managers, we work with first home buyers across Auckland, West Auckland, the North Shore, and remotely throughout New Zealand to make the mortgage process feel manageable. We can review your credit position, explain what lenders are looking for, and help you put your best foot forward before you apply. Our apply for a mortgage guide is a great place to start, and our team of personalised mortgage advisers is ready to walk alongside you every step of the way. Reach out today for an obligation-free conversation.

Frequently asked questions

How long do credit checks stay on my report in New Zealand?

Credit enquiries typically remain on your report for up to five years, but their influence fades over time as recent behaviour is weighted higher than older negatives.

Will one missed payment stop me from getting a home loan?

One missed payment rarely prevents approval, particularly if you’ve demonstrated consistent, positive behaviour since the incident occurred.

Where can I get my free credit report in New Zealand?

You’re entitled to one free annual report from each of New Zealand’s registered credit bureaus, including Centrix, Equifax, and Illion.

Can I fix errors on my credit report?

Yes. If you find inaccurate information, you should contact the relevant credit bureau directly to dispute and correct the entry, as errors can affect your score unfairly.

Do all lenders use the same credit score?

No. Different lenders may access different bureaus or apply their own internal scoring models, meaning each lender’s assessment criteria can vary considerably.