TL;DR:

- Loan-to-value ratio determines how much of a property you’re borrowing versus owning outright.

- Exemptions like new builds and Kāinga Ora loans allow higher LVRs for first home buyers.

- Building a larger deposit improves approval chances, rates, and long-term financial stability.

If you’ve ever felt your eyes glaze over when a bank mentions “LVR,” you’re not alone. Loan-to-value ratio is one of those mortgage terms that sounds deceptively simple but carries enormous weight in your home buying journey. For first home buyers in New Zealand, understanding LVR isn’t just helpful, it’s the difference between getting approved and walking away empty-handed. This guide breaks down exactly what LVR means, how the Reserve Bank’s rules affect you, which exemptions could work in your favour, and how to position yourself for the best possible outcome when you apply for your first home loan.

Table of Contents

- What is loan-to-value ratio and why does it matter?

- Understanding LVR restrictions and exemptions in New Zealand

- How LVR affects your deposit and loan approval

- Kāinga Ora and other LVR exemption paths for first home buyers

- Common LVR mistakes and how to avoid them

- Our take: What first home buyers really need to know about LVR

- Ready to take action? Expert help for New Zealand home buyers

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| LVR affects loan approval | Understanding and optimising your LVR can boost your chances of mortgage approval and better loan terms. |

| Special exemptions exist | First home buyers can access low-deposit paths through government schemes and new build exemptions. |

| Avoid common pitfalls | Watch out for valuation surprises and plan for the total cost of buying, not just the deposit. |

| Expert guidance helps | A good mortgage adviser can help you navigate complex LVR rules and choose the right solution. |

What is loan-to-value ratio and why does it matter?

LVR stands for loan-to-value ratio. It’s the percentage of a property’s value that you’re borrowing from a lender. In plain terms, it tells the bank how much of the property you own outright versus how much they’re funding.

The formula is straightforward:

LVR = (Loan Amount ÷ Property Value) x 100%

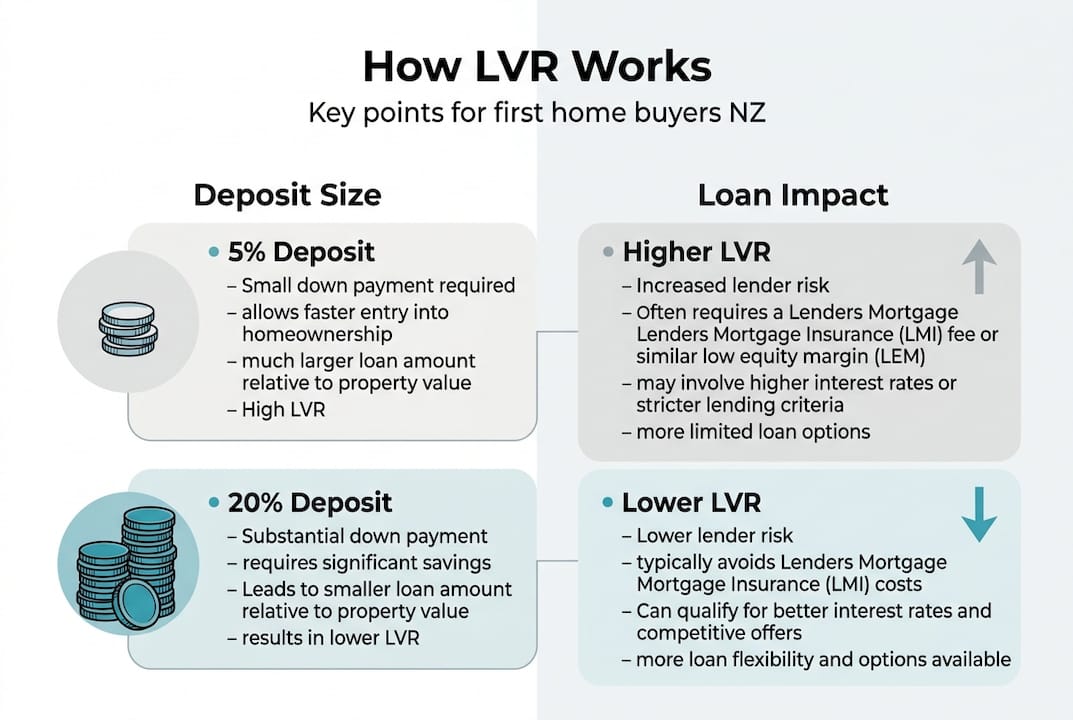

So if you’re buying a home worth $500,000 and you have a $50,000 deposit, your loan amount is $450,000. That gives you an LVR of 90%. Simple enough, but the implications are significant.

Here’s why lenders and the Reserve Bank of New Zealand pay close attention to LVR:

- Risk management: A higher LVR means the bank is exposed to more risk if property values fall.

- Borrower resilience: Lower deposits often correlate with tighter household budgets, increasing default risk.

- Market stability: The Reserve Bank uses LVR restrictions as a tool to prevent overheating in the property market.

| Deposit amount | Property value | Loan amount | LVR |

|---|---|---|---|

| $50,000 | $500,000 | $450,000 | 90% |

| $100,000 | $500,000 | $400,000 | 80% |

| $150,000 | $500,000 | $350,000 | 70% |

As the table shows, a larger deposit dramatically reduces your LVR. And that matters because lower LVR improves approval odds, rates, and equity access. Aiming for below 80% means you avoid the premiums and restrictions that come with high-LVR lending. It’s a goal worth working towards, even if it takes a little longer to save.

With the importance of LVR established, it’s crucial to grasp how banks and regulators view your mortgage application.

Understanding LVR restrictions and exemptions in New Zealand

Now that you know why LVR matters, let’s break down the rules and exceptions that could affect your home buying journey.

The Reserve Bank of New Zealand sets limits on how much high-LVR lending banks can do. These rules are called LVR restrictions, and they change periodically based on market conditions. As of late 2025 and into 2026, RBNZ eased LVR rules for owner-occupiers, allowing banks to extend up to 25% of new lending above the 80% LVR threshold. That’s a meaningful shift that opens more doors for buyers with smaller deposits.

Here’s a comparison of standard limits versus exemption cases:

| Borrower type | Standard LVR limit | Exemption available |

|---|---|---|

| Owner-occupier | 80% (20% deposit) | Up to 95% with Kāinga Ora |

| Residential investor | 65% (35% deposit) | Limited exemptions |

| New build buyer | Exempt from standard rules | Higher LVR accessible |

Key exemptions that first home buyers should know about:

- New builds: Properties being built or recently completed are generally exempt from standard LVR rules, giving buyers access to higher LVR lending.

- Kāinga Ora First Home Loan: This government-backed scheme allows eligible buyers to borrow with a much smaller deposit. Kāinga Ora loans have different LVR treatment compared to standard mortgages.

- Welcome Home Loan successors: Various government initiatives continue to support first home buyers in accessing the market.

Understanding which exemptions apply to your situation can be the difference between buying now or waiting years longer to save a bigger deposit.

Pro Tip: Banks always use the lower of the purchase price or the independent valuation when calculating your LVR. If a property is valued below what you’ve agreed to pay, your effective deposit shrinks instantly. Always get a valuation before going unconditional. You can learn more about LVR impact on first home buyers and how these rules play out in practice.

How LVR affects your deposit and loan approval

With a handle on LVR rules and exemptions, let’s see how your deposit directly affects your loan options.

The size of your deposit is the single biggest lever you can pull on your LVR. And the threshold that matters most for standard bank lending is 20%. Here’s what happens at each stage:

- Below 10% deposit (LVR above 90%): Very limited options outside of specific exemption schemes. Most mainstream banks won’t lend here without a government-backed guarantee.

- 10% to 20% deposit (LVR 80 to 90%): Some lenders will consider this, but you’re in the high-LVR zone. Expect stricter criteria, higher interest rates, and possible low equity margins.

- 20% deposit (LVR at 80%): This is the standard threshold for most bank lending. You unlock more lender options and better rates.

- Above 20% deposit (LVR below 80%): You’re in the strongest position. More lenders compete for your business, rates improve, and approval is more straightforward.

First home buyers often access higher LVRs of 90 to 95% through exemptions like new builds and Kāinga Ora, but strict income and property criteria apply. It’s not a free pass. You still need to demonstrate solid financial habits and meet specific eligibility requirements.

If you’re exploring ways to boost mortgage eligibility, small changes like reducing credit card limits or paying down personal debt can make a real difference to how lenders assess your application. And if a 5% deposit sounds appealing, it’s worth checking your eligibility for 5% deposit loans before assuming you qualify.

Pro Tip: Even if you qualify with a low deposit, budget carefully for other upfront costs including legal fees, building inspections, insurance, and moving expenses. These can add $5,000 to $15,000 on top of your deposit, and they won’t be covered by your mortgage.

Kāinga Ora and other LVR exemption paths for first home buyers

For even more accessible home loan options, let’s look at government assistance and special exemptions for Kiwi first home buyers.

The Kāinga Ora First Home Loan is arguably the most powerful tool available to eligible first home buyers in New Zealand. Here’s what it offers:

- 5% deposit required: You don’t need the standard 20%, making it far more accessible for many buyers.

- No lenders mortgage insurance (LMI): Unlike some overseas equivalents, this scheme doesn’t load you up with extra insurance premiums.

- Primary residence only: Kāinga Ora requires you to occupy the home as your primary residence. Investors need not apply.

- Income caps (2026): Single applicants must earn under $95,000 annually. Couples or multiple buyers must earn under $150,000 combined.

- House price caps: These vary by region, so a property that qualifies in Palmerston North may not qualify in central Auckland.

For those considering building, the new build exemption is equally powerful. Buying or building a new property allows you to access higher LVR lending without falling under standard restrictions. This is a genuine game-changer for buyers who are flexible about property type.

You can explore your options through Kāinga Ora First Home Loan info and also look into Kāinga Ora shared ownership if full ownership feels out of reach right now. For those who want to understand which product suits them best, comparing the best Kāinga Ora loan option is a smart starting point. You can also get a clear picture of the NZ first home loan process from application through to settlement.

Pro Tip: Always check both the income cap and the regional house price cap before assuming you qualify. Many buyers are surprised to discover the price ceiling in their target suburb rules them out, even if their income is within range.

Common LVR mistakes and how to avoid them

Understanding the special pathways is helpful, but new buyers often make avoidable mistakes. Here’s how to sidestep the most frequent LVR traps.

- Calculating deposit based on purchase price alone: Many buyers assume their deposit covers the LVR calculation. But banks use the lower amount of either the purchase price or the independent valuation. If the valuation comes in low, your LVR jumps and your approval may be at risk.

- Ignoring exemptions that could apply: New builds and Kāinga Ora loans are often overlooked by buyers who assume they need a 20% deposit. Don’t rule out options before checking the criteria.

- Forgetting additional costs: Legal fees, building reports, insurance, and moving costs all come out of your savings. If these eat into your deposit, your LVR worsens before you’ve even applied.

- Not checking lender-specific criteria: Each bank interprets LVR rules slightly differently. Some are more flexible than others, especially for first home buyers with strong income profiles. Reviewing lender criteria for home loans before you apply saves time and protects your credit record.

- Going unconditional without a valuation: This is the most costly mistake. If the valuation comes in below the purchase price after you’ve gone unconditional, you’re locked into a deal with a higher LVR than planned.

Pro Tip: Always factor in a possible valuation shortfall of 5 to 10% when planning your deposit. Building that buffer into your savings target means you won’t be caught short at the worst possible moment.

Our take: What first home buyers really need to know about LVR

Here’s what most guides won’t tell you about thriving as a first home buyer in New Zealand.

We see it regularly. A buyer scrapes together the minimum 5% or 10% deposit, celebrates getting approved, and then spends the next few years under real financial pressure. The loan is approved, yes. But the higher interest rate, the tighter monthly budget, and the lack of equity buffer make the journey far more stressful than it needs to be.

The uncomfortable truth is that meeting the minimum LVR requirement is not the same as being in a strong financial position. A lower LVR gives you access to better rates, more lender competition, and the ability to tap into equity if life throws you a curveball. It also makes refinancing far easier if market conditions shift.

Real home loan resilience comes from building genuine buffers, not just clearing the entry bar. We encourage every buyer to look at why LVR matters for buyers beyond just the approval question. Sometimes waiting six to twelve months longer to build a stronger deposit is the most powerful financial decision you can make. A trusted mortgage adviser can help you model both scenarios and choose the path that sets you up for long-term stability, not just short-term approval.

Ready to take action? Expert help for New Zealand home buyers

Understanding LVR is a fantastic first step, but applying that knowledge to your specific situation is where things get real.

At Mortgage Managers, we specialise in helping first home buyers navigate LVR rules, access exemptions, and find the right loan product for their circumstances. Whether you’re ready to apply for a mortgage in Auckland or simply want to understand your options, our personal mortgage advisers are here to guide you through every step. We’re locally based in Hobsonville and work with buyers across Auckland, the North Shore, West Auckland, and remotely throughout New Zealand. Let us help you move from confusion to confidence.

Frequently asked questions

What is a good LVR for a first home loan in New Zealand?

An LVR of 80% or less is ideal, as lower LVR improves approval odds and helps you avoid extra restrictions and higher rates. Aiming for this threshold gives you the widest range of lender options.

Can I buy a first home in NZ with less than a 20% deposit?

Yes, exemptions like the Kāinga Ora First Home Loan allow eligible buyers to purchase with just a 5% deposit, provided you meet income and property price criteria.

Do new builds really have LVR exemptions?

Yes. New builds and Kāinga Ora loans receive different LVR treatment, meaning buyers can access higher LVR lending that wouldn’t be available for existing properties under standard rules.

What does the bank use to calculate LVR if the valuation is lower than the purchase price?

Banks use the lower amount of either the independent valuation or the purchase price when determining your LVR, so a low valuation can significantly affect your effective deposit.

How can I check if I qualify for a low-deposit exemption?

Review your income, property type, and first home buyer status against the criteria for Kāinga Ora and new build exemptions. First home buyers accessing higher LVRs of 90 to 95% must meet strict income and eligibility requirements, so speaking with a mortgage adviser is the fastest way to confirm your options.