TL;DR:

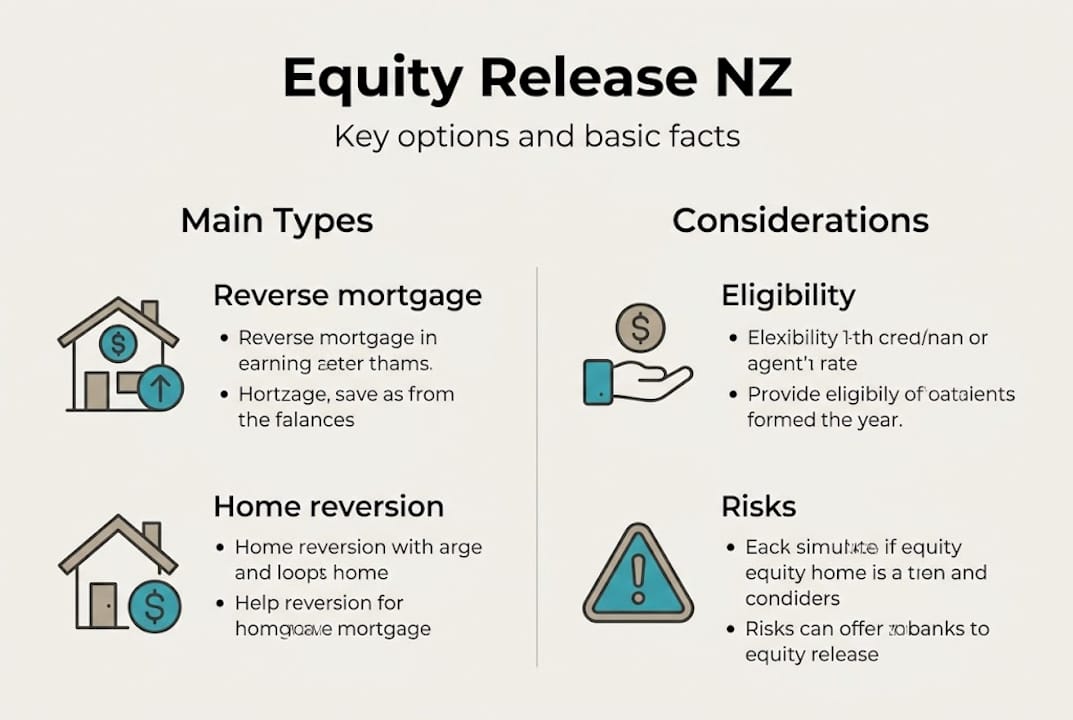

- Equity release allows homeowners aged 60 and over to access home value without selling.

- Main options include reverse mortgages with accumulating interest and home reversion schemes selling part of the home.

- Important to consult advisers to weigh risks, benefits, and impacts on inheritance and government support.

Your home is likely your most valuable asset, yet for many New Zealanders aged 55 and over, that wealth feels completely out of reach until the day you sell up and move on. That assumption is understandable, but it is not entirely accurate. Equity release in New Zealand allows homeowners aged 60 and over to access home equity without selling, primarily through reverse mortgages or home reversion schemes. This guide walks you through what equity release actually means, who qualifies, the main types available, the risks to consider, and the practical steps to get started with confidence.

Table of Contents

- Understanding equity release in New Zealand

- Types of equity release: Reverse mortgages vs. home reversion

- Eligibility and key considerations for New Zealanders

- Risks, benefits, and alternatives to equity release

- Steps to apply for equity release in New Zealand

- Our perspective: The unseen realities of equity release in New Zealand

- Explore your equity release options with expert help

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Access funds without selling | Equity release lets you unlock home value for retirement, staying in your own home. |

| Two main options | Reverse mortgages and home reversion schemes both offer unique pros and cons. |

| Careful planning is crucial | Understand eligibility, impacts, and alternatives before making a decision. |

| Professional advice helps | Discussing with mortgage advisers ensures you choose the option best suited to your needs. |

Understanding equity release in New Zealand

Equity release is, at its core, a way of converting part of the value locked inside your home into usable cash, without requiring you to pack up and leave. You remain in your property while accessing funds that can meaningfully improve your quality of life in retirement. Think of it as a financial tap connected to your home’s value, one that you can turn on when you need it most.

The equity release details available in New Zealand have grown more accessible in recent years, and eligibility typically begins at age 60. Some providers, however, do offer options for homeowners as young as 55, which is worth knowing if you are planning ahead.

People use equity release for a wide range of reasons:

- Supplementing NZ Superannuation to cover everyday living costs

- Funding home renovations or accessibility upgrades

- Travelling or pursuing retirement goals

- Helping adult children with a first home deposit

- Managing unexpected medical or care expenses

Funds can be delivered in several ways, depending on the product and provider. You might receive a single lump sum, regular income-style payments, or a line of credit you draw on as needed. Each delivery method suits different financial situations, so it pays to think carefully about what matches your lifestyle and goals.

“Equity release gives you options. Instead of watching your wealth sit in bricks and mortar while your day-to-day budget feels tight, you can access what you have already built.”

Understanding home equity basics is the first step before exploring any product. The more clearly you understand how much equity you hold and how it works, the better positioned you will be to make a decision that genuinely serves your retirement.

Types of equity release: Reverse mortgages vs. home reversion

The two main options in New Zealand are reverse mortgages and home reversion schemes, and they work quite differently from one another. Choosing between them is not just a financial calculation. It is a deeply personal decision shaped by your goals, your family, and your comfort with debt.

| Feature | Reverse mortgage | Home reversion (e.g. Lifetime Home) |

|---|---|---|

| How it works | Borrow against your equity | Sell a share of your home |

| Repayment | On sale or departure | No debt, share sold at below market value |

| Interest | Compounds over time | None |

| Ownership | You retain full ownership | Partial ownership transferred |

| Right to stay | Guaranteed | Guaranteed |

| Best for | Flexible access to funds | Avoiding debt entirely |

A reverse mortgage guide will show you that this product lets you borrow against the equity in your home, with no repayments required while you live there. The loan, plus accumulated interest, is repaid when you sell, move into care, or pass away. This flexibility is attractive, but the compounding interest means the amount owed can grow significantly over time.

Home reversion schemes, such as the equityNow programme, work differently. You sell a percentage of your home to a provider at a discounted rate in exchange for a lump sum. You keep the right to live there for life, but you no longer own that portion of the property. There is no debt and no interest, but you are giving up future capital growth on that share.

Common options in New Zealand are reverse mortgages and the Lifetime Home home reversion scheme, and each carries distinct trade-offs worth examining carefully.

Pro Tip: If leaving a full inheritance to your children is a priority, a home reversion scheme may feel less comfortable than a reverse mortgage, since you are permanently transferring ownership of a portion of your home. Talk it through with your family before deciding.

Key stat: Interest on a reverse mortgage compounds annually, meaning a loan of $100,000 at 8% interest could more than double within nine years if no repayments are made.

Eligibility and key considerations for New Zealanders

Before you explore products in detail, it helps to know whether you are likely to qualify. Most lenders require applicants to be 60 and over and to own most or all of their home outright. Some providers extend eligibility to age 55, particularly for certain products.

Here are the core eligibility factors to consider:

- Age: Typically 60 and over, though some products accept applicants from 55

- Property type: Must be your primary residence, not a rental or investment property

- Property condition: Lenders usually require the home to meet minimum valuation and condition standards

- Equity level: The more equity you hold, the more you can potentially access

- Existing mortgage: Some lenders allow equity release if a small mortgage remains, provided there is sufficient equity

The amount you can access is influenced by your age, the value of your home, and the specific lender’s policies. Generally, older applicants can access a higher percentage of their home’s value.

There are also important downstream considerations that many people overlook. Releasing equity can affect your eligibility for government benefits such as the Accommodation Supplement. It may also reduce the value of the estate you leave behind, which is something to discuss openly with your family. Future aged care costs are another factor. If you need residential care in later years, having less equity available could limit your options.

Pro Tip: Before applying, speak with a financial adviser and a solicitor separately. Improving your eligibility and understanding your full financial picture beforehand can save you from costly surprises down the track.

Now that you understand the requirements, it is time to look at the broader picture of benefits, risks, and alternatives.

Risks, benefits, and alternatives to equity release

Equity release is not a one-size-fits-all solution, and it is important to weigh both sides honestly before making any commitment.

The benefits:

- Access to tax-free cash without selling your home

- No monthly repayments required during your time in the property

- Financial breathing room to enjoy retirement more fully

- Flexibility in how funds are received and used

The risks:

Equity release offers flexibility but comes with the risk of eroding home equity over time. Compounding interest is the most significant concern with reverse mortgages. The longer you hold the loan, the more it grows, and the less equity remains for your estate or future needs.

“Equity release is a powerful tool, but like any tool, it works best when used with care and a clear plan in mind.”

Here is a simple checklist to help you weigh your priorities:

- How much cash do I genuinely need, and for what purpose?

- Do I have other assets or income sources I have not fully explored?

- How important is leaving an inheritance to my family?

- What are my likely aged care needs in the next 10 to 15 years?

- Have I spoken to an independent financial adviser and a lawyer?

Alternatives worth considering:

| Alternative | How it works | Key trade-off |

|---|---|---|

| Downsizing | Sell and buy smaller | Requires moving |

| Taking in a boarder | Rent a room for income | Less privacy |

| Government grants | Apply for support schemes | Limited availability |

| Remortgaging | Access equity via new loan | Requires repayments |

Exploring bank alternatives and remortgaging for equity may suit homeowners who still have income and can manage repayments. These options preserve more of your equity over time.

Steps to apply for equity release in New Zealand

Applying for equity release usually involves property valuation, legal advice, and a formal lender application process. Here is a practical roadmap to help you move forward with clarity.

- Research your options. Understand the difference between reverse mortgages and home reversion schemes, and consider which aligns with your goals.

- Seek independent advice. Talk to a mortgage adviser and a solicitor before approaching any lender. This step alone can save you from costly mistakes.

- Get a property valuation. Lenders will require a current valuation of your home to determine how much equity you can access.

- Submit your application. Once you have chosen a lender, complete the formal application with all required documents.

- Review the offer carefully. Read every condition, fee, and interest rate before accepting. Compare at least two or three providers.

- Complete legal checks. Your solicitor will review the contract and ensure your rights are protected.

- Receive your funds. Once all checks are complete, your funds are released in the agreed format.

Documents you will typically need include proof of identity, recent property rates notices, and details of any existing mortgage. Timelines vary but most applications take between four and eight weeks from initial enquiry to settlement.

Pro Tip: Use a mortgage repayment calculator to model different loan amounts and interest scenarios. Seeing the numbers play out over time helps you make a more grounded decision. Also consider refinancing options as a comparison point before committing to equity release.

Fees can include application costs, valuation fees, legal fees, and early repayment charges. Always ask for a full fee schedule upfront so there are no surprises.

Our perspective: The unseen realities of equity release in New Zealand

Most guides focus on the mechanics of equity release. But in our experience working with New Zealand homeowners, the real challenges are rarely about the numbers alone.

Equity release decisions are often made under financial pressure, and that pressure can cloud judgement. Families sometimes have strong opinions, and those opinions do not always align with what is best for the homeowner. Emotional stress is a real factor that deserves acknowledgement.

What we see less often discussed is the significant variation between lenders. Two reverse mortgages might look similar on the surface, but the fine print around interest rate structures, early exit conditions, and fee schedules can produce vastly different outcomes over a decade. The role of a mortgage adviser is to surface those differences before you sign, not after.

We also see regret most commonly among people who did not plan for aged care costs. Releasing a large portion of equity early can leave you with fewer options if residential care becomes necessary later. Equity release works best as a considered, strategic step, not a quick fix for a tight month.

Explore your equity release options with expert help

Taking the first step towards equity release can feel like standing at a crossroads without a map. That is exactly where a trusted mortgage adviser becomes your financial GPS, helping you compare products, understand the fine print, and avoid the pitfalls that catch many homeowners off guard.

At Mortgage Managers, we specialise in personalised mortgage advice for New Zealanders navigating complex financial decisions, including equity release. Based in Hobsonville and servicing clients across Auckland, the North Shore, West Auckland, and remotely throughout New Zealand, our team is ready to help you find the right solution for your retirement. Visit Mortgage Managers today to start the conversation.

Frequently asked questions

Can I release equity from my home if I am under 60 in New Zealand?

Some lenders offer equity release to homeowners as young as 55, but most lenders require applicants to be at least 60 and to own most or all of their home outright.

Does releasing home equity affect my New Zealand pension or benefits?

Releasing equity can affect your entitlement to government benefits, so always check with an independent adviser before you apply to avoid unexpected changes to your financial support.

What happens to my home after I use equity release?

You retain the right to stay in your home for life or until you move out, after which the property is typically sold to repay the released equity amount.

Are there risks to equity release in New Zealand?

Yes, key risks include compounding interest reducing your estate, possible impacts on government benefits, and eroding home equity over time. Always seek independent legal and financial advice before signing anything.