You will have heard media and our Reserve Bank talk about inflation and how inflation must be controlled in 2022.

Inflation has hit a 30-year high and we’re told that it’s not good, but many people we speak to do not understand why most people are so concerned and yet some seem not to be.

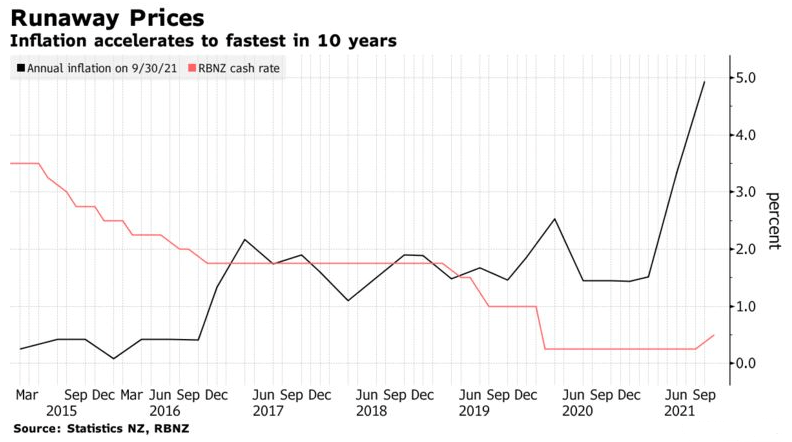

Understanding Inflation

Inflation in economic terms is the rate of increase in prices over a given period of time. In New Zealand we use the consumers price index (CPI) as a measure of inflation.

What is inflation?

In simple economic terms inflation is the rate of increase in prices over a given period of time. In most cases inflation gets reported in annual terms.

It gives a good indication of price increases and is used by the Reserve Bank as a key indicator for managing the economy.

What is the measure of inflation in New Zealand

The consumers price index (CPI) is a measure of inflation for New Zealand households which measures the percentage change in the price of a basket of goods and services consumed by households over a period of time. There are 11 CPI groups and they include food, housing and household utilities, health, recreation and culture, education, communication, clothing and footwear, transport, alcoholic beverages and tobacco, household contents and services and the last is miscellaneous goods and services.

Some inflation is good as it typically shows a growing economy, but high inflation is also bad as it means that money is losing its value.

For the past twenty or so years inflation has been relatively low and as a nation we have become used to the economic stability that comes with low inflation. It’s been an economy where prices have been increasing, but in most cases incomes have increased too.

Since 2000 New Zealand CPI (Consumers Price Index) inflation has averaged around 2.15 percent and this compares with averages of 2.40 percent in the 1990’s.

But it was not always as low as this. Older New Zealanders will remember inflation back in the 1970’s and 1980’s when the average inflation was 11.6 percent and when (at this rate) it would take only six years for prices to double. Incomes did not keep up with inflation during these years and there was high unemployment and finally some harsh economic reforms were needed.

Over the longer term the inflation rate in New Zealand has averaged 4.61 percent from 1918 until 2022, reaching an all time high of 44.00 percent in the third quarter of 1918 and a record low of -15.30 percent in the first quarter of 1923.

Many of us thought that we could resign high inflation to history, but maybe we were being naïve.

The Cause Of This New Inflation Increase

With the announcements and acceptance that we have the highest inflation for the last 30-years we need to try and understand what caused it to jump up so fast, and by doing so we may figure out how we will ne able to reign it in again.

Of course some of this was signaled during our COVID response when the Government borrowed heavily to prop up the economy and jobs. Whenever you (the Government or us personally) borrow money for consumption rather than investment there will become a time in the future when that debt needs to be repaid. In a personal sense that means a concentrated effort with limited spending is needed which nobody really enjoys, and the Government should be no different as it’s not Government money it is our money.

Unfortunately we are seeing the finance minister Grant Robinson denying responsibility and saying that it’s global issues, such as the war in Ukraine and disrupted shipping and supply lines because of Covid-19 as the main factors in rising inflation. These are major contributing factors, but he can also look to address the domestic pressures on inflation.

You just need to look at the public sector.

The public sector (including both central and local government) have grown into big organisations and now over 5 percent of people are employed within the public sector and in roles that do not earn New Zealand any income. Instead the public sector have been forced to increase their staff levels, salaries and costs to carry out Government policy on climate change, health and safety, water and carbon emissions. Furthermore we see a lot of inefficiencies and waste within many parts of the public sector as they are not exposed to the realities of business or any competition.

While there is no denying the need for a public sector, there needs to be some accountability and control on the runaway spending.

Increasing Prices Hurt People and Economies

None of us really enjoy seeing prices skyrocket, especially with everyday items that we cannot avoid.

The food trolley is getting expensive to fill and of course fuel prices have gone through the roof recently too, but maybe this is just the start of those price increases?

Then there are the home loan interest rates – they have increased significantly and quickly and the Reserve Bank is making no secret that they will have to keep increasing too.

We can accept some inflation and increased interest rates when our income is also increasing, but this time around many of us are still recovering from the impact of COVID and are now being hit with increases in both inflation and interest rates.

We should all be concerned with the recent inflation results and especially if the Government and Reserve Bank cannot get it under control quickly preferably by doing more than just lifting interest rates.

What Can We Do Individually?

As individuals we cannot control everything, and inflation is one of those things that we have very little control over but that doesn’t mean we can ignore it either.

The higher the inflation goes the less value our money (our income) has and if home loan interest rates or rent are increased then this hits our pockets even harder.

We therefore should be looking at all of our costs that we can control and see if there is any way we can do things more efficiently, plus we can look at our income and investments to see if there is any way to enhance those too.

Review Financials Costs – there are some costs that you cannot control, but others that you can review and possibly reduce. We always suggest that you start with some of the more obvious costs and gradually work through the other costs. Of course short-term debts like credit cards, car loans and hire purchase is often expensive and savings can be made quite easily. With insurances there are sometimes discounts available if you pay things like insurances annually, and it’s always a good idea to review what levels of cover you have.

Review Your Income – most people don’t believe that they can increase what they earn, but sometimes it’s worth having a closer look. A lot of employers will consider offering a pay increase or bonus if you can offer to help them with some extra hours or by being more efficient. Many people are also doing something as a part-time business or job and there are a number of options that you can consider.

The main thing that we suggest is review what you are doing on a regular basis. Often you can improve things by making a few small changes rather than trying to find that magic bullet that is expected to change your life.

"*" indicates required fields