Using a mortgage broker can increase your chances of mortgage approval by 2.5 times if you have a low deposit. Many first home buyers and borrowers with complex financial situations struggle to navigate New Zealand’s mortgage market alone. This guide explains what mortgage brokers do, how they help secure better loan terms, and why they’re especially valuable for those with low deposits or bad credit.

Table of Contents

- The Role Of Mortgage Brokers In New Zealand

- How Mortgage Brokers Help First Home Buyers And Those With Low Deposits

- Supporting Borrowers With Bad Credit Or Complex Financial Histories

- Common Misconceptions About Mortgage Brokers In New Zealand

- How Mortgage Brokers Negotiate Better Mortgage Terms

- The Mortgage Application Process With A Broker

- Making The Most Of Your Mortgage Broker Relationship

- Discover Expert Mortgage Advisers To Guide Your Home Loan

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Wide lender access | Brokers connect you to over 50 lenders including banks and non-bank providers. |

| Higher approval rates | First home buyers with low deposits see 2.5 times better approval odds through brokers. |

| Better rates | Brokers negotiate 0.1% to 0.3% lower mortgage rates compared to direct applications. |

| No borrower fees | Most brokers are paid by lenders, not you. |

| Bad credit support | Brokers identify flexible lenders and guide credit improvement strategies. |

The role of mortgage brokers in New Zealand

Mortgage brokers act as intermediaries between you and a broad panel of lenders. They assess your financial profile to match loan options that suit your unique circumstances, whether you’re a first home buyer, self-employed, or managing complex finances.

Brokers access over 50 lenders including major banks and non-bank lenders. This broad reach means they can find products that traditional banks might not offer directly to you.

What brokers do for you:

- Evaluate your deposit size, income sources, and credit history to identify suitable lenders

- Search their entire lender panel for products matching your needs

- Handle complex paperwork and documentation requirements

- Present multiple loan options with clear comparisons

- Negotiate terms on your behalf using their industry relationships

Understanding the role of mortgage brokers in NZ helps you recognise why working with them simplifies the mortgage process. The best mortgage brokers in New Zealand maintain strong lender relationships that translate into better outcomes for borrowers.

Brokers provide personalised advice considering your specific situation. They don’t push a single lender’s products because their success depends on finding the right fit for you.

How mortgage brokers help first home buyers and those with low deposits

First home buyers face unique challenges securing mortgage approval, especially with limited deposits. Brokers know exactly which lenders accept low deposit applications and what criteria they use.

First home buyers with low deposits achieve 2.5 times higher approval rates using brokers. This dramatic difference comes from brokers’ expertise in packaging applications to highlight your strengths.

How brokers boost approval chances:

- Identify lenders with flexible low deposit criteria

- Guide you through government schemes like Welcome Home Loan

- Structure your application to emphasise stable income and savings discipline

- Reduce documentation errors that delay or jeopardise approval

- Coordinate timing between multiple lenders for comparison

Brokers also educate you about deposit requirements, LVR restrictions, and strategies to strengthen your position. A mortgage broker explained for first home buyers shows how professional guidance transforms challenging applications into approved loans.

Pro tip: Start working with a broker 3 to 6 months before you plan to buy. Early engagement gives you time to improve your financial position and access more lender options when you’re ready to apply.

The right broker understands that low deposit borrowers need creative solutions. They’ll explore guarantor options, non-bank lenders, and specialty products that banks rarely advertise.

Supporting borrowers with bad credit or complex financial histories

Bad credit doesn’t automatically disqualify you from homeownership. Brokers specialise in finding lenders willing to look beyond credit scores to assess your current financial capacity.

Brokers identify lenders willing to consider bad credit and advise on rehabilitation steps. They maintain relationships with non-bank lenders who evaluate applications more holistically than major banks.

Steps brokers take to support bad credit borrowers:

- Request and review your credit report to identify specific issues

- Match your profile with lenders offering flexible assessment criteria

- Advise on improving your credit score before application submission

- Coordinate documentation proving your current financial stability

- Follow up with lenders to address concerns and negotiate terms

Your broker might recommend delaying your application by six months to improve your credit position. This honest advice saves you from rejected applications that further damage your credit score.

Mortgage brokers for complicated mortgages understand that past financial difficulties don’t define your future. They focus on demonstrating your ability to service a loan today.

Complex situations like self-employment, contract work, or variable income also benefit from broker expertise. They know which lenders accept alternative income verification and how to present your finances effectively.

Common misconceptions about mortgage brokers in New Zealand

Several myths prevent borrowers from seeking broker assistance. Understanding the truth helps you make informed decisions about professional mortgage support.

Most mortgage brokers are paid by lenders, not borrowers. Lenders compensate brokers through commissions when loans settle, so you typically pay nothing directly.

Clearing up common myths:

- Myth: Brokers only work with limited lenders. Reality: Brokers access 50+ lenders including banks and specialists.

- Myth: Using a broker delays approval. Reality: Brokers often speed up the process through efficient application management.

- Myth: Brokers push expensive products. Reality: Their reputation depends on finding suitable, competitive solutions.

- Myth: You get better deals going direct to banks. Reality: Brokers negotiate rates banks don’t advertise publicly.

- Myth: Brokers charge hidden fees. Reality: All fees must be disclosed upfront by law.

Understanding benefits of mortgage brokers in NZ dispels fears about cost and quality. Transparent broker relationships benefit everyone involved.

Some borrowers worry brokers favour certain lenders. Professional brokers maintain diverse relationships and prioritise matching you with the right product, not maximising their commission.

How mortgage brokers negotiate better mortgage terms

Brokers leverage volume and relationships to secure mortgage rates and terms you can’t access directly. Their negotiating power comes from bringing lenders consistent business.

Broker negotiated rates are typically 0.1% to 0.3% lower than direct applications. Over a 30-year mortgage, even 0.2% saves thousands of dollars in interest.

| Factor | Broker negotiation | Direct application |

|---|---|---|

| Interest rate | 0.1% to 0.3% lower on average | Standard advertised rate |

| Product range | Access to 50+ lenders | Limited to one institution |

| Special deals | Exclusive broker only offers | Public promotions only |

| Approval flexibility | Broker advocates for exceptions | Rigid automated criteria |

| Fee waivers | Often negotiated | Rarely available |

Brokers also access exclusive products unavailable to retail customers. Home loan options that banks can’t provide directly include specialty low deposit schemes and construction finance packages.

Pro tip: Ask your broker about lender specials or discounts available through their panel. These limited time offers can significantly reduce your borrowing costs.

Your broker’s existing relationship with lenders means they know exactly who to approach for your situation. This targeted strategy wastes no time on lenders unlikely to approve your application.

Smaller rate differences compound dramatically over loan terms. A 0.2% reduction on a $500,000 mortgage saves approximately $20,000 over 30 years.

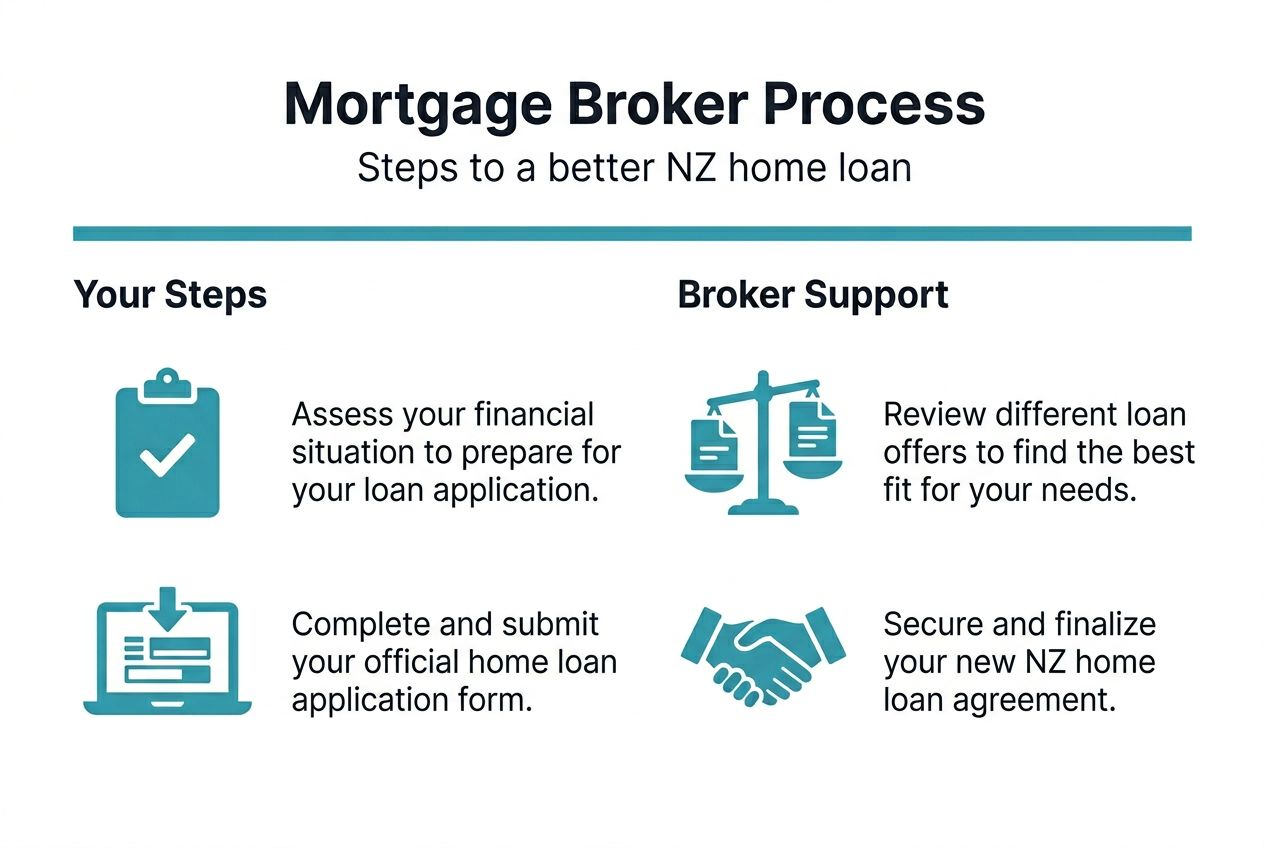

The mortgage application process with a broker

Working with a broker follows a clear process designed to minimise your effort while maximising approval chances. Understanding each step helps you prepare effectively.

Brokers handle paperwork and liaise with lenders to streamline applications. This coordination reduces delays and prevents common errors that derail approvals.

The broker application journey:

- Initial consultation: Discuss your financial situation, goals, and timeline with complete transparency.

- Document gathering: Your broker provides a checklist of required paperwork including income proof, bank statements, and identification.

- Lender matching: The broker searches their panel to identify suitable products and creates a shortlist.

- Application preparation: Your broker prepares your application with supporting documentation and submits to selected lenders.

- Lender liaison: The broker manages communication, answers lender queries, and advocates for your approval.

- Offer presentation: Your broker explains each loan offer, compares terms, and recommends the best option.

- Settlement coordination: Once you accept an offer, your broker guides you through final conditions and settlement.

This structured approach typically takes 2 to 4 weeks from initial consultation to formal approval. Understanding why use mortgage brokers in NZ shows how professional management accelerates outcomes.

Your broker acts as your advocate throughout the process. They translate lender requirements into plain language and ensure you understand every decision point.

Making the most of your mortgage broker relationship

Maximising broker value requires selecting the right professional and maintaining open communication. These practical tips help you build an effective working relationship.

Strategies for working effectively with brokers:

- Choose brokers with proven NZ market knowledge and strong lender relationships

- Be completely transparent about your finances, including debts and credit issues

- Understand broker compensation models to avoid surprises

- Respond promptly to document requests to prevent application delays

- Ask questions about anything you don’t understand

- Maintain regular contact during the application process

Selecting how to choose a mortgage broker in NZ involves checking credentials, reading reviews, and interviewing potential brokers about their experience with situations like yours.

Broker transparency and open communication lead to better mortgage outcomes. The more your broker understands your situation, the more effectively they can match you with suitable lenders and negotiate favourable terms.

Your broker should explain how they’re paid, which lenders they work with, and their approach to finding your best option. Professional brokers welcome these questions and provide clear answers.

Remember that your broker works for you, not the lender. They succeed when you secure a mortgage that serves your long term financial interests.

Discover expert mortgage advisers to guide your home loan

Ready to experience the benefits of professional mortgage guidance? Expert brokers simplify your home loan journey by connecting you with tailored solutions across New Zealand’s entire lending market.

Mortgage advisers act as your personal shoppers for home loans, comparing products and negotiating terms you can’t access alone. Whether you’re a first home buyer with a low deposit or managing complex finances, specialist advisers match your situation with suitable lenders.

If you’re in Auckland, find a mortgage broker in Auckland who understands local market conditions and maintains strong lender relationships. Professional advisers provide personalised service aligned with your financial goals.

Pro tip: Contact expert mortgage advisers and brokers today to access exclusive lender rates and accelerate your approval process.

Frequently asked questions

What does a mortgage broker do exactly?

A mortgage broker assesses your financial situation and matches you with suitable lenders from their panel of 50+ institutions. They handle application paperwork, negotiate terms on your behalf, and guide you through the entire mortgage process from initial consultation to settlement.

Do I pay mortgage broker fees in New Zealand?

Most mortgage brokers in New Zealand are paid by lenders through commissions, so you typically pay nothing directly. Any fees charged to borrowers must be disclosed upfront by law, and many brokers offer completely free services funded entirely by lender commissions.

Can a mortgage broker help if I have bad credit?

Yes, brokers specialise in finding lenders willing to consider bad credit applications. They assess your credit report, identify specific issues, and match you with non-bank lenders offering flexible criteria. Brokers also advise on improving your credit score before applying to maximise approval chances.

How quickly can a broker get my mortgage approved?

Mortgage approval through a broker typically takes 2 to 4 weeks from initial consultation to formal approval. Brokers often accelerate this timeline by submitting error-free applications, responding promptly to lender queries, and leveraging relationships to prioritise your application.

Are mortgage brokers independent or tied to specific lenders?

Most New Zealand mortgage brokers are independent, meaning they work with multiple lenders rather than representing a single institution. This independence allows them to compare products across their entire panel and recommend the best option for your specific circumstances without bias.