Most australian homebuyers are surprised to learn that the average deposit needed in New Zealand now sits between 10 percent and 20 percent of a property’s price. For many, understanding the rules, fees, and risks tied to a home loan can be one of the toughest steps when buying a home across the Tasman. This guide breaks down the essentials so you can approach the New Zealand property market with clarity and confidence.

Table of Contents

- Home Loans Explained In New Zealand

- Types Of Home Loans Available

- Eligibility Criteria And Application Process

- Repayments, Interest Rates And Fees

- Risks, Pitfalls And Common Mistakes

Key Takeaways

| Point | Details |

|---|---|

| Home Loan Fundamentals | A home loan allows borrowers to purchase property by borrowing from lenders, typically requiring a 10% to 20% deposit and repayment over 15 to 30 years. |

| Types of Home Loans | Key loan types in New Zealand include fixed-rate, floating-rate, split, interest-only, and construction loans to accommodate varying borrower needs. |

| Eligibility Criteria | Prospective borrowers typically need to be at least 18 years old, demonstrate stable income, maintain a good credit history, and provide a suitable deposit. |

| Common Pitfalls | Borrowers should avoid common mistakes such as overestimating borrowing capacity and neglecting to budget for additional homeownership costs. |

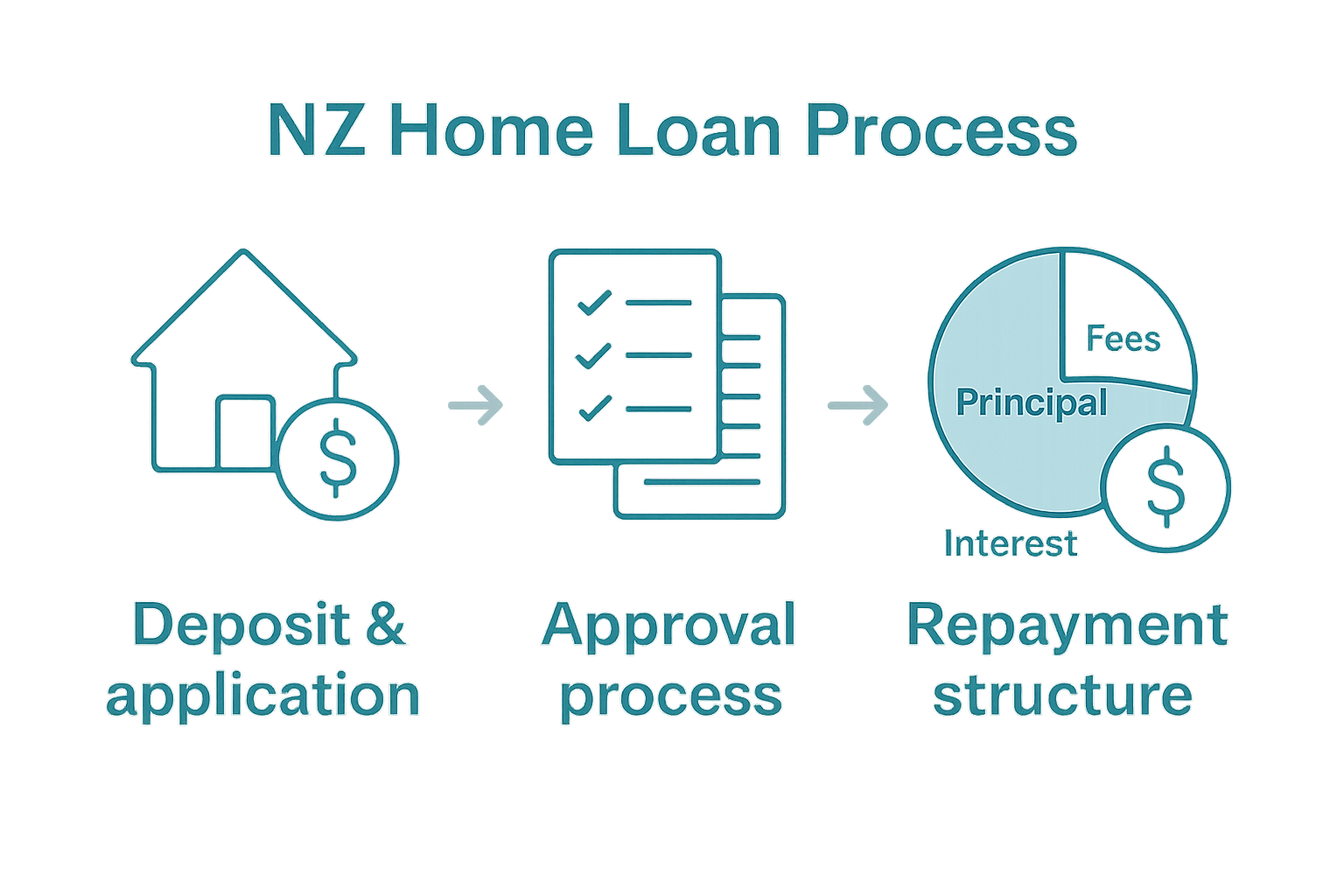

Home Loans Explained In New Zealand

A home loan is a specialised financial agreement that enables Kiwis to purchase property by borrowing money from a lender, typically a bank or financial institution. According to Consumer Protection, lenders have specific responsibilities to ensure loans remain suitable and affordable for borrowers.

The core mechanics of a home loan involve several critical components. Borrowers receive a substantial sum to purchase property, which they then repay with interest over an agreed timeframe, usually between 15 to 30 years. Reserve Bank of New Zealand highlights that loan-to-value ratio (LVR) restrictions play a crucial role in maintaining financial system stability by limiting high-risk mortgage lending.

Typically, home loans in New Zealand require borrowers to provide a deposit, which demonstrates financial commitment and reduces the lender’s risk. Most lenders expect a minimum deposit of 10% to 20% of the property’s total value. Key factors influencing loan approval include:

- Credit history

- Current income

- Employment stability

- Existing financial obligations

- Property valuation

Navigating home loans can be complex, which is why many Kiwis seek guidance from mortgage advisers who understand the intricacies of local lending standards. Their expertise helps borrowers select the most appropriate loan structure for their unique financial circumstances.

Types Of Home Loans Available

New Zealand offers several distinct home loan types designed to meet diverse financial needs and homebuyer circumstances. Kāinga Ora provides specialised First Home Loans, which help eligible first-time buyers enter the property market with lower deposit requirements.

The primary home loan categories in New Zealand include:

- Fixed-Rate Loans: Interest rates remain constant for a predetermined period

- Floating-Rate Loans: Interest rates fluctuate with market conditions

- Split Loans: Combination of fixed and floating rate portions

- Interest-Only Loans: Borrowers pay only interest for a specific timeframe

- Construction Loans: Specifically designed for building new properties

New Zealand Government also highlights innovative options like top-up loans and reverse mortgages, which allow homeowners to borrow against their property’s existing equity. These specialised loan types provide financial flexibility for different life stages and investment strategies.

Understanding the nuances of each loan type is crucial. Some loans offer lower initial rates but might have stricter conditions, while others provide more flexibility but potentially higher long-term costs.

Consulting with mortgage advisers who specialise in local lending standards can help you navigate these complex options and select the most suitable loan for your unique financial situation.

Eligibility Criteria And Application Process

Securing a home loan in New Zealand requires meeting specific eligibility criteria that vary depending on the loan type and individual lender requirements. Kāinga Ora provides clear guidelines for First Home Loans, highlighting key eligibility factors for prospective homeowners.

General eligibility criteria typically include:

- Minimum Age: Must be 18 years or older

- Income Requirements: Demonstrable, stable income

- Credit History: Good credit score and financial history

- Deposit: Minimum deposit usually between 10% to 20%

- Residency Status: New Zealand citizen or permanent resident

Consumer Protection emphasises that lenders must thoroughly assess loan suitability, ensuring borrowers can realistically manage their financial obligations. The application process typically involves several key steps:

- Initial financial assessment

- Document preparation

- Loan application submission

- Credit and background checks

- Property valuation

- Loan approval and offer

Prospective borrowers should be prepared to provide comprehensive documentation, including proof of income, bank statements, identification, and detailed information about existing financial commitments.

IMAGE:descriptive_key_1] [Mortgage advisers who understand local lending standards can provide invaluable guidance throughout this complex process, helping you navigate the intricate requirements and improve your chances of successful loan approval.

Repayments, Interest Rates And Fees

Home loan repayments form the core financial commitment for New Zealand homeowners, involving complex interactions between principal amounts, interest rates, and ongoing fees. Consumer Protection highlights the critical importance of understanding these financial components before entering any loan agreement.

Typical home loan fees and charges may include:

- Application Fees: Initial loan setup costs

- Establishment Fees: One-time charges for processing the loan

- Monthly Service Fees: Ongoing administrative charges

- Valuation Fees: Costs associated with property assessment

- Legal Fees: Charges for legal documentation and processing

- Early Repayment Penalties: Potential charges for closing loans before term

Healthcare Plus emphasises that strategic repayment approaches can significantly reduce overall loan costs. Making additional repayments or choosing more frequent payment schedules can potentially shorten loan terms and minimise total interest paid.

Interest rates play a pivotal role in determining your total repayment amount. Borrowers can choose between fixed and floating rates, each with unique advantages. Mortgage advisers who understand local lending standards can help you navigate these complex decisions, ensuring you select a repayment strategy that aligns with your long-term financial goals and current economic conditions.

Risks, Pitfalls And Common Mistakes

Consumer Protection warns that home loan borrowers frequently encounter significant financial risks when approaching mortgage lending without proper preparation and understanding. Navigating the complex landscape of home loans requires careful consideration and strategic planning to avoid potentially devastating financial missteps.

Common home loan risks and mistakes include:

- Overestimating Borrowing Capacity: Taking on loans beyond personal financial capabilities

- Ignoring Additional Costs: Overlooking insurance, maintenance, and property-related expenses

- Failing to Build Emergency Funds: Not maintaining financial buffer for unexpected circumstances

- Neglecting Comparison Shopping: Accepting first loan offer without thorough market research

- Poor Credit Management: Failing to maintain a strong credit profile

Reserve Bank of New Zealand emphasises the critical importance of understanding loan-to-value (LVR) restrictions as a key mechanism for mitigating high-risk lending practices. These restrictions help prevent borrowers from overextending themselves financially and protect both lenders and homeowners from potential economic instability.

Financial experts recommend working closely with mortgage advisers who understand local lending standards to develop a comprehensive strategy that addresses potential risks. This approach involves careful financial planning, realistic budgeting, and a thorough understanding of your long-term financial goals and current economic conditions.

Take Control of Your Home Loan Journey with Expert Support

Understanding the complexities of New Zealand home loans can feel overwhelming. With terms like loan-to-value ratio, fixed and floating rates, and eligibility criteria, you need more than just information – you need guidance tailored to your unique financial situation. Whether you are a first home buyer trying to navigate deposit requirements or a homeowner seeking the best repayment strategy, aligning with trusted mortgage advisers can make all the difference.

At Mortgage Managers, we specialise in local lending standards and provide personalised advice designed to reduce financial stress and avoid common mortgage mistakes. Serving Hobsonville, Auckland, and all of New Zealand remotely, we help you unlock the right home loan options and repayment plans. Start your path to smarter borrowing today by visiting Mortgage Managers or explore how mortgage advisers who understand local lending standards can guide you through the application process. Secure the future you deserve with professional support from Mortgage Managers. Make your move now before rates or lending conditions change.

Frequently Asked Questions

What is a home loan?

A home loan is a financial agreement that allows individuals to borrow money from a lender to purchase property, which they repay with interest over a set period, usually between 15 to 30 years.

What factors affect my eligibility for a home loan?

Eligibility for a home loan typically depends on your age, income, credit history, deposit amount (usually between 10% to 20% of the property’s value), and residency status.

What types of home loans are available in New Zealand?

Common types of home loans include fixed-rate loans, floating-rate loans, split loans, interest-only loans, and construction loans. Each type caters to different financial needs and circumstances.

How can I lower my home loan repayments?

To lower your home loan repayments, consider making additional repayments, opting for a more frequent payment schedule, or consulting with mortgage advisers to choose the most suitable repayment strategy.

Recommended

- Types of Home Loans NZ: Complete 2024 Guide | Mortgage Managers

- What Is a Mortgage? Complete NZ Home Loan Guide

- Mortgage Approval Process Guide NZ Home Loans – Mortgage Managers

- Basic 101 On How To Apply For A Home Loan

- How to Qualify for a Mortgage: Step-by-Step Guide for Buyers – Craigburn Capital