Saving for your first home in Auckland can feel like a marathon, especially when every dollar counts toward your dream of ownership. A bigger deposit means more than just reaching the usual twenty percent—it shows banks you are a strong candidate and can actually lower your mortgage interest rates slightly, typically by 0.10% to 0.30% according to local experts. This introduction explains why your deposit size matters and clears up the common myths many buyers believe.

Table of Contents

- Defining Bigger Deposit And Common Myths

- Deposit Variations And Qualifying Criteria

- How Deposit Percentages Work

- Qualifying Criteria Lenders Actually Assess

- Why Your Circumstances Shape Everything

- How Deposit Size Impacts Mortgage Approval

- Interest Costs, LMI And Long-Term Savings

- Risks With Small Deposits And Alternatives

Key Takeaways

| Point | Details |

|---|---|

| Bigger deposits improve mortgage terms | Contributing more than 20% as a deposit reduces lender risk, consequently leading to better interest rates and terms. |

| Debunking myths about deposits | A larger deposit does not guarantee mortgage approval, nor do all lenders provide discounts for them. |

| Risks of small deposits | Small deposits increase financial vulnerability, exposing homeowners to negative equity and higher monthly repayments. |

| Professional advice is essential | Consult a mortgage adviser early to identify the optimal deposit level that will enhance your financial position. |

Defining bigger deposit and common myths

A bigger deposit simply means contributing more than the traditional 20% down payment when purchasing a property in Auckland. Rather than putting down the minimum required amount, you’re investing significantly more of your own capital into the home purchase from day one.

Why does this matter? Banks and lenders view larger deposits as a sign of financial stability and reduced risk. When you have more money invested in the property, you have more incentive to maintain payments and protect your investment.

What counts as a bigger deposit?

Deposits typically fall into these categories:

- 20–30%: Standard larger deposit that improves your position with most lenders

- 30–40%: Strong deposit that opens doors to better rates and terms

- 40%+: Exceptional deposit that gives you maximum negotiating power

Each percentage point above 20% strengthens your application and can reduce mortgage interest rates slightly, typically by 0.10% to 0.30% depending on the lender.

Busting the common myths

There’s plenty of misinformation about larger deposits floating around Auckland property circles. Let’s clear up what’s actually true.

Myth 1: All banks automatically give discounts for bigger deposits. This isn’t accurate. Whilst larger deposits do improve your position, banks don’t always publicly advertise these discounts. Lender policies vary considerably, and you need to ask directly about rate reductions available to you.

Myth 2: A bigger deposit guarantees your mortgage will be approved. Having substantial savings is excellent, but it’s not the only factor lenders examine. Your income, employment history, credit score, and debt-to-income ratio all matter significantly. A larger deposit helps, but it’s not a golden ticket.

Myth 3: You must save 20% to avoid lender’s mortgage insurance. Technically true for most conventional lending, but the relationship between deposit size and costs goes deeper. The real benefit of a bigger deposit is avoiding lender’s mortgage insurance (LMI) altogether and securing better rates throughout your loan term.

Myth 4: A bigger deposit means you pay less overall. Partially true. Lower interest rates do reduce total repayment costs, but you’re also tying up more capital upfront. The financial benefit depends on your personal situation and what you could earn with those funds elsewhere.

The real advantages worth considering

When you bring a larger deposit to the table in Auckland’s competitive market, several practical benefits emerge:

- Lower monthly repayments: Borrowing less means smaller regular payments

- Avoiding LMI costs: Deposit above 20% eliminates mortgage insurance fees

- Better interest rates: Lenders reward lower risk with improved pricing

- Stronger negotiating position: Sellers and lenders take you more seriously

- Faster equity building: You own more of the property immediately

A bigger deposit isn’t just about having more money—it’s about reducing your financial risk and improving the terms available to you throughout the entire loan.

Pro tip: Before saving aggressively for a larger deposit, speak with a mortgage adviser to understand what deposit level actually improves your specific situation. Different lenders have different thresholds where rates shift, and your circumstances matter more than chasing a particular percentage.

Deposit variations and qualifying criteria

Deposits aren’t one-size-fits-all in Auckland’s property market. Different lenders have different expectations, and your personal circumstances determine what deposit level actually works for you. Understanding these variations helps you avoid wasting time chasing unrealistic targets.

The home deposit requirements across New Zealand vary based on property value, location, and lender policies. What one bank accepts at 10% down, another might require at 15% or 20%.

How deposit percentages work

Deposit amounts are calculated as a percentage of the property’s purchase price, not the mortgage amount. Here’s what that means practically:

- 10% deposit: Minimum for many first-home buyers; usually requires lender’s mortgage insurance

- 15% deposit: Sweet spot for some lenders; still often requires LMI but improves terms

- 20% deposit: Traditional benchmark; avoids mandatory insurance for most conventional loans

- 25% and above: Excellent position; strongest rates and terms available

For example, buying a $600,000 property with a 15% deposit means putting down $90,000. With a 20% deposit, that’s $120,000. The difference significantly impacts your borrowing capacity and monthly repayments.

Here’s how common deposit sizes impact key mortgage outcomes in Auckland:

| Deposit Size | Typical LVR | Likely Interest Rate | LMI Requirement | Overall Cost over 25 Years |

|---|---|---|---|---|

| 10% ($60k on $600k) | 90% | Higher (~5.85%) | Required (costly) | Highest—interest plus LMI |

| 15% ($90k on $600k) | 85% | Medium-high (~5.70%) | Often required | Lower than 10%, still high |

| 20% ($120k on $600k) | 80% | Lower (~5.55%) | Not required | Much lower; best for most |

| 25%+ ($150k+) | 75% or less | Lowest (may be <5.55%) | Not required | Lowest—maximises savings |

Qualifying criteria lenders actually assess

Your deposit is just one piece of the puzzle. Lenders examine multiple factors before approving your mortgage:

Income and employment stability matter enormously. Banks want to see steady income over at least two years, ideally in the same field or employer. Self-employed applicants face stricter scrutiny and typically need to provide tax returns and accountant letters.

Credit history and debt-to-income ratios reveal your financial reliability. Your existing debts—car loans, credit cards, student loans—affect how much additional mortgage debt lenders will allow you to carry. Most lenders cap total debt at 80-85% of your gross income.

Savings history and deposit source matter more than you’d think. Lenders prefer seeing consistent savings patterns over time, not sudden large transfers. If you’re gifted money from family, you may need a statutory declaration confirming it’s a gift, not a loan requiring repayment.

Property value and location influence lending decisions. Some lenders are more cautious about certain Auckland suburbs or property types. Investment properties typically require larger deposits than owner-occupied homes.

The following table summarises how lender criteria affect your ability to qualify for different deposit levels:

| Lender Criteria | High Impact with Small Deposit | Low Impact with Large Deposit |

|---|---|---|

| Income stability | Critical for approval | Still reviewed, less critical |

| Credit history | Minor issues can block loan | Minor issues more tolerated |

| Source of deposit | Scrutinised closely | Fewer questions asked |

| Employment status | Strict for self-employed | Guidelines more flexible |

Why your circumstances shape everything

Two buyers with identical 20% deposits might receive vastly different mortgage offers based on their individual situations. One with stable employment and clean credit gets premium rates. Another with irregular income or recent defaults faces higher interest charges or deposit requirements.

Your deposit is powerful, but it’s your complete financial picture that determines whether you qualify and what rate you’ll actually receive.

This is why speaking with a mortgage adviser early matters. They understand which lenders suit your specific circumstances and can identify the deposit level that genuinely improves your position.

Pro tip: Rather than saving aggressively toward a specific deposit percentage, focus first on strengthening your overall application—pay down existing debts, maintain stable employment, and build your savings history. A smaller deposit with excellent qualifying criteria often beats a larger deposit with weak financial standing.

How deposit size impacts mortgage approval

Your deposit size directly influences whether lenders approve your mortgage application and on what terms. A larger deposit signals reduced risk to banks, which translates into faster approvals, better interest rates, and access to more competitive loan products.

When you apply for a mortgage, lenders assess your loan-to-value ratio (LVR). This is simply your loan amount divided by the property’s value. A 20% deposit means an 80% LVR—your mortgage covers 80% of the property cost. A 10% deposit creates a 90% LVR, which carries higher risk in the lender’s eyes.

Why deposit size changes approval chances

Larger deposits improve approval odds because they reduce lender exposure:

- Lower LVR = lower risk: Banks lend less relative to property value, so they’re protected if property values drop

- Automatic mortgage insurance removal: At 20% deposit, you avoid lender’s mortgage insurance entirely, which streamlines approval

- Easier qualification: Lenders relax income and credit requirements for larger deposits

- Multiple lender options: More lenders compete for your business when you have a strong deposit

- Faster processing: Applications with larger deposits typically move through underwriting quicker

Think of it this way: if a property worth $500,000 drops 10% in value, a buyer with a 10% deposit is underwater immediately. A buyer with 25% deposit still has equity cushion. Banks remember market downturns and price their risk accordingly.

The approval difference in practice

A smaller deposit doesn’t automatically mean rejection, but it does create hurdles. You’ll face stricter scrutiny on income documentation, credit history, and savings patterns. Lenders might also impose conditions—such as requiring a specific insurance product or additional financial reserves.

The role of deposit in home buying extends beyond simple approval odds. A larger deposit can mean the difference between multiple competitive offers and a single limited offer.

With a 10% deposit, you might qualify with one lender at 5.95% interest. With 20%, five lenders compete for your business at 5.65%. That 0.30% difference compounds over 25 years into tens of thousands of dollars.

Conditional approvals and deposit requirements

Some lenders issue conditional approvals tied to specific deposit levels. They’ll say: “Approved at 15% deposit, but not at 10%.” This forces you to save more or walk away from the property.

Other lenders have tiered approval systems. Your application strength determines whether you need 15%, 20%, or 25%. Self-employed applicants, contract workers, and recent migrants often find themselves in higher deposit brackets regardless of income stability.

A larger deposit isn’t just about approval likelihood—it’s about approval certainty and the financial terms you’ll actually receive.

Understanding how your specific deposit level affects your application requires knowing which lenders suit your circumstances. This is where professional guidance matters significantly.

Pro tip: Before settling on a deposit target, ask a mortgage adviser exactly which deposit level unlocks the best rates from lenders who specialise in your situation. Sometimes moving from 15% to 20% saves more than you’d expect; other times, the rate jump happens at 25% or 30%.

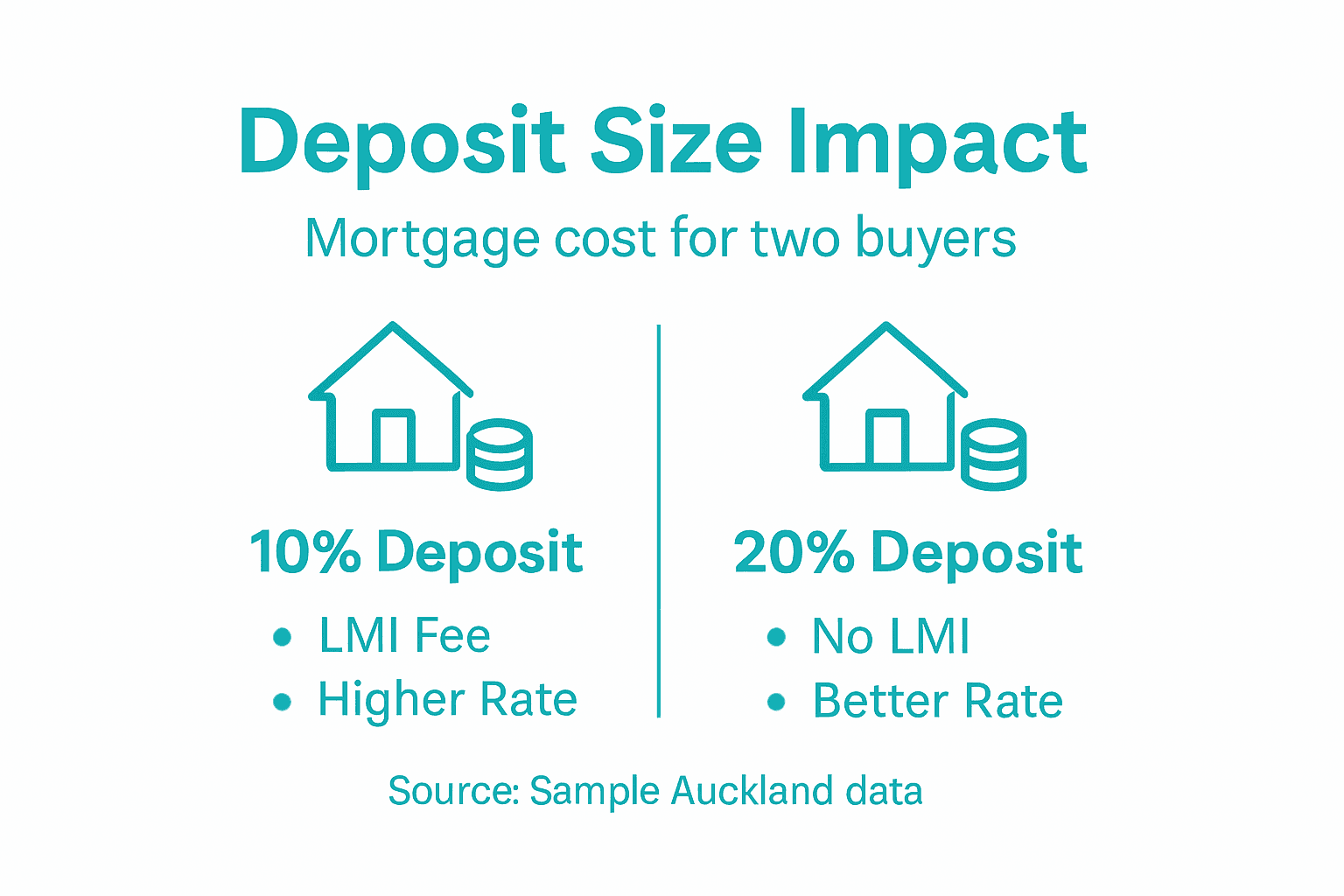

Interest costs, LMI and long-term savings

The real cost of a smaller deposit isn’t just the deposit amount itself. It’s the compound interest, insurance fees, and higher rates that follow you throughout your entire loan term. Over 25 years, these costs dwarf the initial deposit difference.

Consider two Auckland buyers, each purchasing a $600,000 property. Buyer A puts down 10% ($60,000) and borrows $540,000. Buyer B saves 20% ($120,000) and borrows $480,000. The deposit difference is $60,000. But that’s only the beginning of the cost disparity.

How lender’s mortgage insurance drains your money

Lender’s mortgage insurance (LMI) is a fee you pay when your deposit falls below 20%. It protects the lender if you default, not you. This insurance can cost 2-5% of your loan amount depending on your LVR and lender.

For Buyer A, LMI on a $540,000 loan might cost $16,200. This fee gets added to the loan, so you’re now borrowing $556,200 instead of $540,000. You’ll pay interest on the insurance cost for 25 years.

That $16,200 becomes approximately $35,000 in total interest once compounded. Buyer B pays nothing.

Interest rates and the deposit advantage

Banks reward larger deposits with better interest rates. A buyer with 10% deposit might receive 5.85% interest, whilst a 20% deposit holder gets 5.55%. That 0.30% difference might seem small, but it’s enormous over time.

On Buyer A’s $556,200 loan at 5.85% over 25 years, total interest paid is approximately $428,000. On Buyer B’s $480,000 loan at 5.55%, total interest paid is approximately $365,000. The difference is $63,000 in interest alone.

Add the LMI cost, and Buyer A has paid roughly $98,000 more than Buyer B—despite the initial deposit gap being just $60,000.

The lifetime cost picture

Understanding lifetime cost of mortgages helps first-time buyers grasp why deposit size matters so profoundly. Your deposit choice today echoes through every monthly payment for decades.

These calculations assume interest rates remain constant, which they don’t. During rate cycles, the compounding effect becomes even more dramatic. A buyer with a larger deposit entering a rising rate environment suffers less because they’re borrowing less capital.

The savings timeline

When does the larger deposit “pay for itself”? Usually within 5-7 years. After that, every month saved on interest compounds your financial advantage.

Key savings points across the loan:

- Year 5: Savings offset most deposit difference

- Year 10: Savings dramatically exceed initial deposit gap

- Year 15: Savings become substantial wealth differences

- Year 25: Total advantage reaches $100,000+

A bigger deposit isn’t an expense—it’s an investment that pays dividends every single month for the next 25 years through lower interest costs and eliminated insurance fees.

This is why property experts consistently recommend saving as much deposit as reasonably possible. The long-term financial impact dwarfs short-term convenience.

Pro tip: Calculate your actual interest savings using your specific loan amount and rate quotes from different lenders. Many advisers can show you projections revealing exactly how much extra you’ll pay with a smaller deposit—seeing the number often motivates the final push to save more.

Risks with small deposits and alternatives

Small deposits expose you to financial vulnerability that extends far beyond your initial home purchase. When you borrow 90% of a property’s value, you’re operating without a safety net if circumstances change unexpectedly.

The primary risk is negative equity. If property values drop even 10%, you owe more than your home is worth. This traps you in the property, unable to sell without financial loss, and prevents refinancing to better rates.

The real dangers of minimal deposits

Small deposits create cascading problems:

- Vulnerability to rate rises: Borrowing more means rate increases devastate your repayments. A 1% rate rise on a $540,000 loan costs roughly $5,400 annually more than on a $480,000 loan

- Forced selling in downturns: Job loss or health issues force distressed sales when you’ve borrowed heavily, often at severe losses

- LMI adds borrowed debt: You’re paying interest on insurance that protects the lender, not you, for years

- Limited refinancing options: Future lenders view high LVR as risky, restricting your ability to switch to better rates

- Stress and financial strain: Monthly repayments consume more of your income, leaving little buffer for unexpected costs

These risks compound during economic cycles. Auckland has experienced property corrections before, and buyers with minimal equity often suffer the most.

Alternatives to rushing into small-deposit mortgages

Low deposit mortgages do exist, but they’re not your only path forward. Consider these strategic alternatives before settling for high-risk borrowing.

Delay and save longer. It feels frustrating, but reaching 15-20% deposit takes financial pressure off and improves every term you’ll receive. Each additional percentage point saved dramatically strengthens your position.

Explore first-home buyer programs. Some lenders offer schemes specifically designed for first buyers with smaller deposits but strong financial profiles. These may include rate discounts or waived insurance fees unavailable through standard lending.

Consider property alternatives. A less expensive property in an emerging suburb might let you achieve your deposit goal faster than stretching for premium locations. You can always upgrade later.

Partner with family strategically. If relatives can gift or loan deposit funds (with proper documentation), it strengthens your application without requiring you to carry additional debt.

Build your financial profile first. Pay down existing debts, establish solid employment history, and demonstrate consistent savings. A smaller deposit with excellent fundamentals often beats a larger deposit with weak finances.

Small deposits create risk that spreads across decades. The temporary convenience of buying sooner often costs far more than the extra months or years spent saving.

Pro tip: Before accepting a low-deposit mortgage, ask your adviser what happens to your repayments if interest rates rise 2%. If the answer makes you uncomfortable, that’s your signal to save more deposit instead of stretching your borrowing capacity.

Maximise Your Deposit Power with Expert Mortgage Advice

Struggling to understand how saving a bigger deposit shapes your mortgage impact in Auckland? The challenge is real. A larger deposit not only lowers your interest rates but also helps you avoid costly lender’s mortgage insurance and builds stronger equity faster. If concepts like LVR, mortgage approval odds, and interest savings seem overwhelming, you are not alone. Many Auckland buyers face the same confusion and financial stress when deciding how much deposit to save.

Let Mortgage Managers guide you through these critical decisions with personalised advice from local experts based in Hobsonville. We specialise in helping Aucklanders navigate the complexities of deposit requirements, lender criteria, and interest costs to find solutions that truly fit your unique financial situation. Don’t risk higher costs or approval hurdles by guessing your deposit target. Act now and connect with trusted advisers who understand the market inside out. Discover how to turn your deposit into a powerful advantage at Mortgage Managers. Start your journey today by visiting our homepage and find the best mortgage options tailored for you. Learn more about the role of deposits in home buying and strategies for low deposit home loans that can make a real difference.

Frequently Asked Questions

What is considered a ‘bigger deposit’ when buying a property?

A bigger deposit typically refers to putting down more than the conventional 20% of the property’s purchase price. Contributions of 20–30% are standard, while deposits above 30% improve loan terms significantly.

How does a bigger deposit impact my mortgage interest rates?

With a larger deposit, lenders may offer lower interest rates, typically ranging from 0.10% to 0.30% reduction, which can save you substantial money over the loan term.

Will a bigger deposit guarantee my mortgage approval?

While a bigger deposit improves your chances of approval, it’s not a guarantee. Lenders also consider your income, credit score, employment history, and debt-to-income ratio before making a decision.

What are the long-term financial benefits of saving for a bigger deposit?

Saving for a bigger deposit can lower your monthly repayments, eliminate lender’s mortgage insurance (LMI), and increase your equity in the property faster, ultimately leading to savings on interest costs over the life of the loan.