TL;DR:

- Construction loans in NZ fund building projects through staged drawdowns with interest-only payments during construction.

- Low-deposit options like Kāinga Ora schemes enable eligible buyers with as little as 5% deposit, mostly for turn-key contracts.

- Borrowers should prepare detailed documentation, consider scheme eligibility, and account for extra costs and delays in the building process.

Many New Zealanders assume construction lending is reserved for experienced builders or those with deep pockets. The reality is quite different. Low-deposit options, including Kāinga Ora-backed schemes with as little as 5% deposit, have opened doors for first-time home builders and modest-income buyers. But accessibility comes with nuance. Eligibility criteria, contract types, and lender policies can catch people off guard if they’re not prepared. This guide breaks down everything you need to know about construction lending in New Zealand, from what it actually is, to who qualifies, how the process works, and what traps to avoid along the way.

Table of Contents

- What is construction lending?

- Eligibility and deposit requirements for construction loans

- How construction loans work in New Zealand

- Common challenges and tips for construction lending applicants

- The overlooked realities of construction lending in NZ

- Get expert guidance for your construction loan journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Lower deposit options | Eligible buyers can build with as little as 5% deposit using Kāinga Ora schemes. |

| Eligibility criteria matter | Income caps, property type, and occupancy status determine your construction loan access. |

| Loan type affects process | Turn-key contracts suit low deposit buyers; progressive loans require staged drawdowns. |

| Preparation prevents delays | Secure builder contracts and check lender requirements early to avoid setbacks. |

What is construction lending?

Construction lending is a type of home loan specifically designed to finance the building of a new home or a major renovation. It works differently from a standard mortgage, where the full loan amount is provided upfront to purchase an existing property. With construction lending, funds are released in stages, called drawdowns, as building work progresses.

This staged release structure is one of the most important things to understand. You typically pay interest only on the funds that have been drawn down to date, not on the full loan amount. That means your repayments start smaller and grow as more money is released. It’s a practical approach that reflects the reality of how building projects unfold over months.

For owner-occupiers building new homes, the standard deposit is 10% of the total project cost, which includes both land and build costs. This is notably lower than the 20% typically required for purchasing an existing home. That difference alone makes new builds an attractive pathway for buyers who are still growing their savings.

When preparing for a home loan for construction, it helps to understand the two main loan structures available:

- Progressive drawdown loans: Funds are released in stages aligned with build milestones such as slab, frame, roof, and lock-up.

- Turn-key loans: The full loan amount is released in a single payment once the build is complete and you take possession.

- Interest-only period: During construction, you pay interest only on funds drawn, reducing early financial pressure.

- Fixed-price build contracts: Most lenders require a fixed-price contract with a registered builder before approving a construction loan.

- Valuation requirements: Lenders will require an independent valuation of the completed property before approving finance.

| Feature | Construction loan | Standard home loan |

|---|---|---|

| Deposit required | From 10% (new build) | Typically 20% |

| Funds released | In stages (drawdowns) | Upfront lump sum |

| Repayments during build | Interest only | Full principal and interest |

| Loan purpose | Build or major renovation | Purchase existing property |

| Contract requirement | Fixed-price build contract | Purchase and sale agreement |

Eligibility and deposit requirements for construction loans

Now that you’re clear on what construction lending is, let’s look at who qualifies and what deposit you’ll need. The answer depends heavily on which loan type you’re pursuing and whether you meet specific scheme criteria.

Standard lenders generally require a 10% deposit for new construction loans. That’s a meaningful advantage over the 20% needed for an existing home, but it still represents a significant sum for many buyers. First-time builders often need to combine savings, KiwiSaver withdrawals, and in some cases family gifting to reach that threshold.

For eligible buyers, the Kāinga Ora First Home Loan is a genuine game-changer. According to Kāinga Ora eligibility criteria, you may qualify with just a 5% deposit if you meet the right conditions. Understanding those conditions is critical.

The key eligibility requirements for the Kāinga Ora First Home Loan include:

- You must be a New Zealand citizen or permanent resident.

- Your income must not exceed $95,000 per year if you’re single with no dependants, or $150,000 for couples or those with dependants.

- Your deposit, which can include KiwiSaver and gifted funds, must be at least 5% of the purchase price.

- The property must be owner-occupied, meaning you intend to live in it.

- Some approved lenders permit new builds under this scheme, but usually only for turn-key packages rather than progressive construction contracts.

| Loan type | Minimum deposit | Income cap | Build type allowed |

|---|---|---|---|

| Standard construction loan | 10% | No cap | Progressive or turn-key |

| Kāinga Ora First Home Loan | 5% | $95k / $150k | Typically turn-key only |

For more detail on accessing these options, the Kāinga Ora First Home Loan details page at Mortgage Managers walks through how the scheme works in practice. You can also compare low deposit lenders to understand what flexibility different banks and non-bank lenders offer.

Pro Tip: Not all lenders allow progressive drawdown payments under a 5% deposit loan. If you’re building rather than buying a completed home, confirm with your adviser whether a turn-key or progressive contract applies to your situation before signing anything with your builder.

How construction loans work in New Zealand

Having clarified eligibility, let’s step through what actually happens with a construction loan from application to your finished home. The process has more moving parts than a standard mortgage, but it’s very manageable once you know what to expect.

- Get your documents in order. Before applying, you’ll need signed build plans, a fixed-price contract with a licensed building practitioner, and a full cost breakdown. Lenders won’t proceed without these.

- Submit your loan application. Your lender assesses your income, deposit, and the viability of your build project. This includes a registered valuation of the completed property based on the plans.

- Loan approval is issued. Approval typically includes conditions, such as confirmation of builder insurance, consent approvals, and review of the fixed-price contract.

- Drawdowns are released in stages. As each stage of the build is completed, you request a drawdown. The lender may require an inspection or statutory declaration to confirm progress before releasing funds.

- Interest-only repayments apply. During construction, you pay interest only on the funds drawn. This keeps repayments manageable while the build is underway.

- Final drawdown and full loan activation. Once the build is complete and a code compliance certificate is issued, the final drawdown is made and your loan converts to standard principal and interest repayments.

If you’re using a Kāinga Ora First Home Loan with a 5% deposit, be aware that you’ll typically be limited to turn-key contracts, where the full loan is released upon completion rather than in stages. Understanding the first home loan process in full will help you plan timelines and avoid surprises.

Pro Tip: Talk to your mortgage adviser before signing your build contract. The contract type, whether turn-key or progressive, must align with what your chosen lender will actually fund under your deposit level.

For those newer to home ownership, our guide on how to get a mortgage in NZ covers the foundations clearly and helps you frame the bigger picture.

Common challenges and tips for construction lending applicants

Understanding the loan process is only half the battle. Here’s what most people get caught out on, and how to come out ahead.

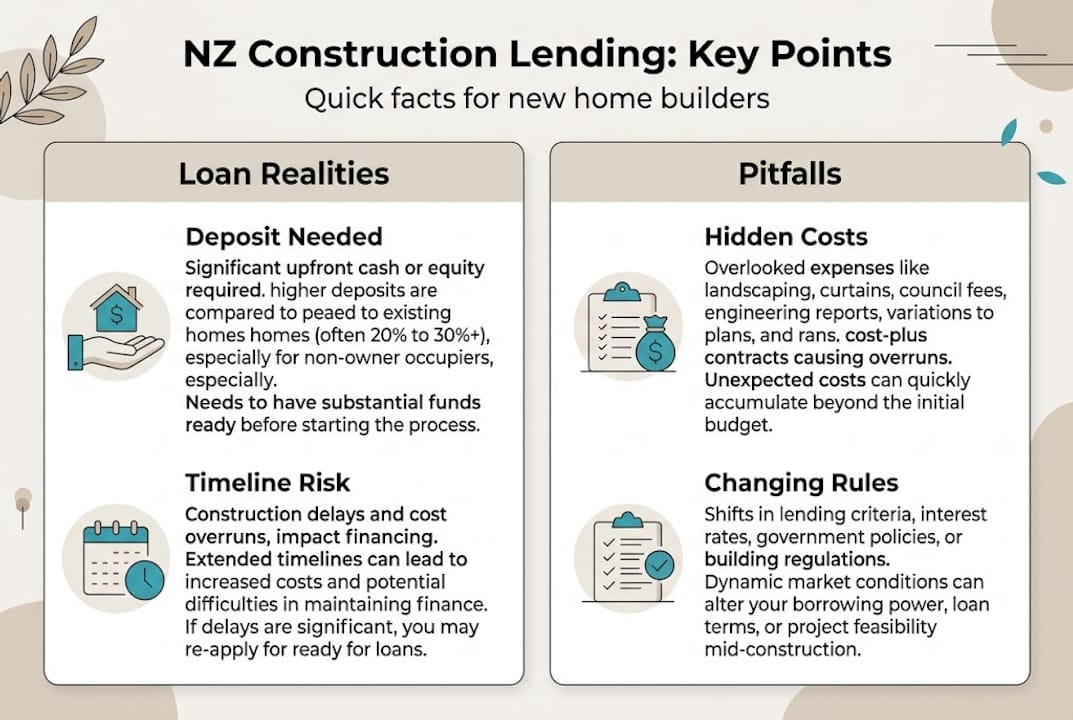

Construction lending comes with a unique set of friction points that standard home purchases simply don’t have. Budget blowouts are probably the most common. Fixed-price contracts offer protection, but variations, upgrades, or unexpected site conditions can add costs that your loan won’t automatically cover.

Common challenges to watch for:

- Progress payment mismatches: Your lender’s drawdown schedule may not align perfectly with when your builder wants payment. Clarify this early.

- Valuation shortfalls: If the completed valuation comes in lower than expected, your lender may reduce the approved loan amount, requiring more deposit from you.

- Lender restrictions for low deposits: As Kāinga Ora guidance confirms, low-deposit schemes favour turn-key builds to avoid the complexity of interim payments, which limits your builder options.

- Limited lender choice: Fewer lenders offer construction loans for borrowers with a 5% deposit, giving you less room to shop around.

- Delays affecting interest costs: Build delays extend your interest-only period, which affects your total borrowing costs even if repayments feel manageable in the short term.

“Low-deposit options via Kāinga Ora enable entry for modest-income first buyers, but strict criteria around income caps and owner-occupancy contrast with the flexibility of a standard 10% deposit loan. For first-time builders, turn-key contracts are generally preferred to avoid the complexity of progress payments under a lower deposit structure.” — Kāinga Ora Homes and Communities

For a practical starting point, our low deposit home loan guide outlines realistic strategies and lender options for buyers working with smaller deposits.

Tips to stay ahead:

- Build a contingency buffer of at least 10% on top of your projected build cost.

- Withdraw KiwiSaver early in the process so funds are confirmed before your application.

- Get independent legal advice before signing any fixed-price build contract.

- Work with a mortgage adviser who has specific experience with construction lending in NZ.

The overlooked realities of construction lending in NZ

After guiding you through the process and pitfalls, here’s what experience in the NZ market really teaches. Most guides focus on the pathway in. Far fewer talk honestly about what happens once you’re on it.

The biggest gap between expectation and reality isn’t the deposit requirement. It’s the timeline. Construction loan approvals take longer than standard mortgages. Lenders scrutinise build contracts, valuations, and builder credentials in detail, and any gap in documentation sends applications back to the start. Clients who arrive prepared with a complete builder contract and current valuations move significantly faster than those who try to assemble documents after applying.

Another underappreciated reality is that scheme policies change. Kāinga Ora eligibility criteria, income caps, and which lenders participate in the First Home Loan scheme are updated regularly. What worked for your colleague 18 months ago may not apply today. That’s why working with advisers who stay current with the best Kāinga Ora options is genuinely valuable, not just a nice-to-have.

There’s also a tendency to underestimate hidden costs. Consent fees, soil reports, engineering assessments, and connection costs for services like water and power can add tens of thousands to a project that looked affordable on a builder’s quote. Planning for those from day one is what separates a smooth build from a stressful one.

Get expert guidance for your construction loan journey

Ready to take the next step with confidence? Construction lending is one of the more complex areas of home finance, but you don’t have to navigate it alone. The right mortgage adviser can act as your financial GPS through every stage, from choosing the right loan structure to aligning your contract type with your lender’s requirements.

At Mortgage Managers, our team of Auckland mortgage brokers specialises in helping first-time builders and low-deposit borrowers find the right construction loan pathway. Whether you’re weighing up a turn-key package or planning a progressive build, our personal mortgage advisers will match your situation to the most suitable lenders and current schemes available in 2026. Get in touch today and take the guesswork out of your construction loan journey.

Frequently asked questions

What is the minimum deposit for a construction loan in New Zealand?

The standard minimum is 10% of the total project cost for owner-occupiers building new homes, but eligible first home buyers may access Kāinga Ora-backed loans with just a 5% deposit for qualifying new builds.

Can I use my KiwiSaver savings for a construction loan deposit?

Yes, eligible borrowers can put KiwiSaver funds toward their deposit, and KiwiSaver and gifted funds can count toward the 5% minimum required under the Kāinga Ora First Home Loan scheme.

What is the difference between a turn-key and a progressive drawdown construction loan?

A turn-key loan releases the full loan amount in one payment when the build is finished and handed over to you, while a progressive drawdown loan releases funds in stages as each phase of construction is completed, such as slab, frame, and roof.

How strict are income limits for low-deposit construction loans?

Kāinga Ora caps income at $95,000 for single buyers with no dependants, and at $150,000 for couples or buyers with dependants, to qualify for the 5% deposit First Home Loan scheme.