TL;DR:

- Interest rates in New Zealand are influenced by decisions made by the Reserve Bank, global economic conditions, and bank-specific strategies, ultimately affecting borrowers’ monthly repayments. Understanding this chain allows homeowners to negotiate better rates, time their fixed terms strategically, and save thousands over their mortgage’s lifetime. Active comparison and timely actions, especially during OCR shifts, empower borrowers to navigate interest rate fluctuations effectively.

Most people assume banks simply decide what interest rate to charge you on a whim, or that a board meeting somewhere determines your mortgage repayments. The reality is far more layered, and far more fascinating. Interest rates in New Zealand are shaped by a chain of decisions, economic forces, and global events that ultimately land on your doorstep as a monthly repayment figure. Understanding this process is not just interesting — it can genuinely save you thousands of dollars over the life of your home loan.

Table of Contents

- The foundations: What interest rates really are

- Who sets interest rates in New Zealand?

- Banks and lenders: How rates are applied to your mortgage

- International and market influences: Beyond local policy

- Practical steps: What you can do to get the best rates

- Our take: What most guides miss about interest rates

- Find the right mortgage advice for your rate strategy

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| RBNZ sets the benchmark | The Reserve Bank of New Zealand sets the Official Cash Rate, influencing all mortgage interest rates. |

| Banks use OCR as a base | NZ banks start with the OCR but adjust final mortgage rates according to market, competition, and risk. |

| Global forces play a role | International events and investor sentiment can indirectly shift NZ interest rates. |

| Comparing rates saves money | Negotiating and shopping between lenders helps Kiwi homeowners secure the best mortgage deals. |

| Expert advice accelerates results | Working with mortgage advisers gives you an edge in understanding, negotiating, and timing your home loan decisions. |

The foundations: What interest rates really are

An interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. For homeowners, it is the figure that determines how much you pay on top of the principal amount you borrowed. Think of it as the price tag on credit. The higher the rate, the more expensive your loan becomes over time.

In New Zealand, home loans generally come in two main forms. A fixed rate locks in your interest rate for a set term, usually between six months and five years, giving you certainty about your repayments. A variable rate (also called a floating rate) moves up and down with the market, meaning your repayments can change at any time. Each has advantages depending on your financial situation and where rates are heading.

To put this in real terms, consider a $500,000 mortgage over 25 years. At 6%, your monthly repayments would be approximately $3,222. Bump that rate to 7%, and you are looking at around $3,534 per month. That is a difference of $312 every single month, or nearly $3,750 per year. Over the life of the loan, that gap becomes enormous.

Understanding the impact of interest rates NZ on your borrowing capacity and repayments is the first step toward making smarter mortgage decisions.

Pro Tip: If you are on a fixed rate coming up for renewal, start researching your options at least 60 days before your term ends. Rates can shift quickly, and being prepared puts you in a much stronger position to negotiate.

Who sets interest rates in New Zealand?

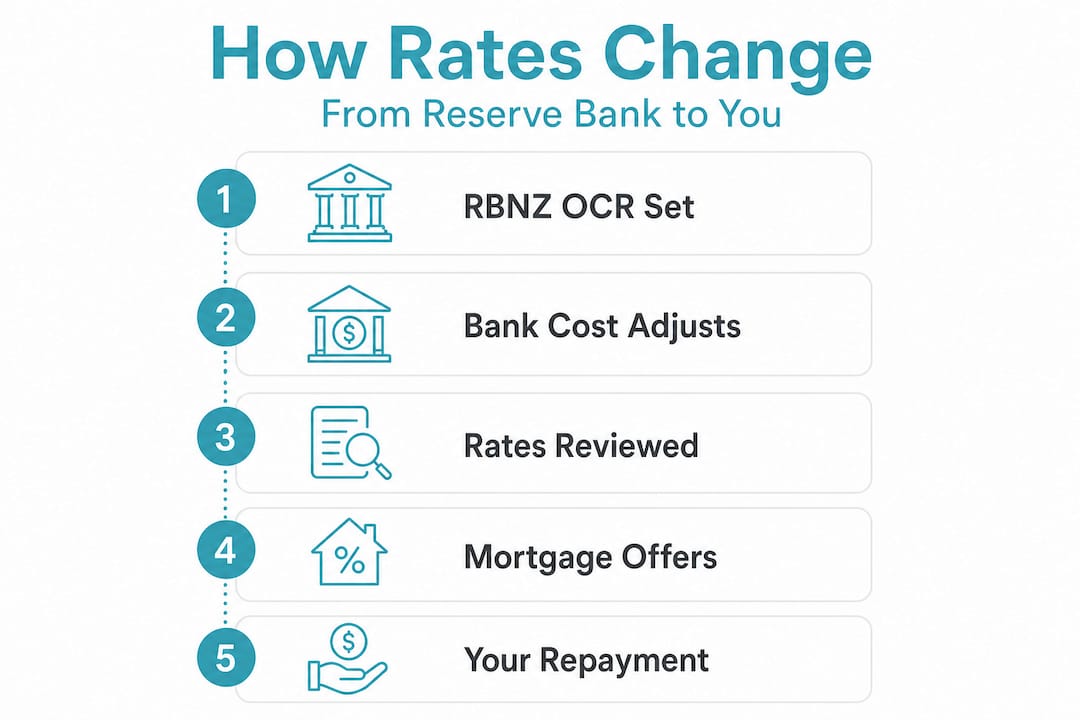

Here is where most people’s understanding stops short. Banks do not set interest rates in isolation. They take their lead from a far more powerful institution: the Reserve Bank of New Zealand (RBNZ).

The RBNZ is New Zealand’s central bank, and it uses monetary policy tools to keep the economy stable. Its most powerful lever is the Official Cash Rate, or OCR. The OCR is the interest rate at which commercial banks borrow and lend money to each other overnight. When the RBNZ adjusts this rate, it sends a ripple effect through the entire banking system, influencing everything from savings account returns to home loan rates.

The Reserve Bank and mortgages relationship is fundamental. As the role of Reserve Bank in New Zealand’s financial system makes clear, the RBNZ’s primary goal is to control inflation and maintain price stability. When inflation rises too quickly, the RBNZ lifts the OCR to make borrowing more expensive, which slows spending and cools the economy. When the economy is struggling, it cuts the OCR to encourage borrowing and stimulate growth.

Here is a snapshot of recent OCR movements and their broad effects on mortgage rates:

| Year | OCR movement | General effect on home loans |

|---|---|---|

| 2021 | 0.25% (historic low) | Record low mortgage rates, strong buyer activity |

| 2022 | Rose sharply to 3.50% | Mortgage rates climbed significantly |

| 2023 | Peaked near 5.50% | High borrowing costs, reduced buyer demand |

| 2024 | Began cutting cycle | Rates started easing, buyer confidence returning |

| 2025 | Continued cuts | More competitive lending environment |

“The OCR has been cut roughly 60% since its 2023 peak, signalling a significant shift in New Zealand’s borrowing landscape and providing meaningful relief to homeowners on variable and short-term fixed rates.”

The key takeaway here is that why mortgage rates change is directly tied to RBNZ decisions. When you hear about an OCR announcement, it is not background noise. It is a signal that directly affects your mortgage.

Key reasons the RBNZ adjusts the OCR:

- Rising or falling inflation pressures

- Changes in employment and economic growth

- Global financial conditions and offshore interest rate movements

- The housing market’s impact on household debt and spending

Banks and lenders: How rates are applied to your mortgage

The OCR is not the rate you see advertised on a bank’s website. It is the starting point. Commercial banks use the OCR as a baseline, then layer on their own costs, risk assessments, and profit margins before arriving at the rates they offer borrowers.

How lenders set rates involves several key factors beyond just the OCR. These include the bank’s cost of raising funds in wholesale and international markets, the competitive landscape with other lenders, and the individual risk profile of the borrower.

Banks adjust mortgage rates after OCR announcements, but not always by the same amount or at the same speed. One bank might pass on a 0.25% OCR cut in full within days. Another might wait weeks or pass on only part of the reduction. This is exactly why shopping around matters so much.

Here is a simplified comparison of how fixed and variable rates tend to behave:

| Rate type | How it’s set | Best suited for |

|---|---|---|

| Fixed (1 year) | OCR expectations plus lender margin | Certainty seekers in rising markets |

| Fixed (2-3 years) | Wholesale rate forecasts plus margin | Medium-term budget planning |

| Variable/floating | OCR plus lender margin, adjusts freely | Flexible borrowers expecting rate drops |

The factors affecting mortgage rates include more than just the OCR. Your deposit size, credit history, income stability, and loan-to-value ratio (LVR) all influence what rate a lender will offer you personally. A borrower with a 40% deposit and strong income will typically receive a better rate than someone with a 10% deposit and irregular earnings.

Understanding why higher rates are sometimes necessary helps put these figures in context too. Higher rates are a tool to prevent runaway inflation, which ultimately protects the purchasing power of your money and the stability of the housing market.

Pro Tip: Do not accept the first rate a bank offers you. Lenders compete for your business, and a simple phone call mentioning that a competitor has offered a lower rate can sometimes prompt a better deal on the spot. A mortgage adviser can do this comparison work for you across many lenders at once.

International and market influences: Beyond local policy

Even when the RBNZ holds the OCR steady, your mortgage rate can still shift. Global events affect New Zealand interest rates indirectly, and this is a reality that many first-home buyers do not fully appreciate until it catches them off guard.

New Zealand is a small, open economy. We borrow significant amounts of money from international markets to fund our banking system. When the cost of that offshore borrowing rises, banks face higher expenses which can flow through to mortgage rates. When global investors see New Zealand as a riskier place to park capital, the premium on that borrowing goes up further.

The three main international factors that influence New Zealand mortgage rates are:

- US Federal Reserve decisions: Because the US dollar underpins global finance, US rate changes affect the cost of borrowing for institutions worldwide, including New Zealand banks.

- Australian monetary policy: Given the close economic ties between New Zealand and Australia, decisions by the Reserve Bank of Australia (RBA) can influence investor sentiment and funding costs here.

- Global risk appetite and investor confidence: During periods of global uncertainty such as financial crises, pandemics, or geopolitical tension, investors demand higher returns to lend money, which raises costs throughout the system.

Beyond these three pillars, the demand for mortgage-backed securities in international markets also plays a role. When investors are confident, they buy these products willingly and at lower yields, keeping funding costs down for banks. When confidence wavers, yields rise and banks eventually pass those costs on.

“Global bond market movements have become increasingly influential on New Zealand fixed mortgage rates, sometimes creating key factors affecting mortgage rates that diverge from what you might expect based on local OCR decisions alone.”

This is why you might sometimes see banks raise their fixed rates even when the RBNZ has not moved the OCR. The global market has spoken first.

If you are serious about securing cheapest home loan rates possible, staying across both local and international financial news becomes genuinely useful.

Practical steps: What you can do to get the best rates

Knowledge is only useful if it leads to action. Now that you understand the forces shaping your interest rate, here are the practical moves that can make a real difference to your mortgage outcome.

Monitor OCR announcements. The RBNZ publishes a schedule of its OCR review dates well in advance. Mark these dates in your calendar. When an OCR cut is expected or announced, it is a good time to review your mortgage structure, especially if you are approaching the end of a fixed term.

Compare lenders actively. Not all banks respond to rate changes at the same speed or by the same amount. Checking cheapest loan rates NZ across multiple institutions gives you leverage and insight into where the market is sitting.

Strategies to help you negotiate a better rate:

- Review your loan-to-value ratio. If your property has increased in value, you may qualify for a better rate tier.

- Consolidate your banking. Having your main accounts with your mortgage lender can sometimes unlock relationship discounts.

- Consider splitting your loan between fixed and variable portions to hedge against rate movements.

- Time your fixed rate renewals strategically, ideally when rates are at or near a cycle low.

- Ask your lender directly about any cashback offers or rate specials that may not be publicly advertised.

Understanding why you should compare home loans NZ goes beyond just finding the lowest number. Loan features, flexibility, offset accounts, and repayment terms all factor into the true cost of your mortgage.

Comparing loan offers and negotiating is one of the most effective ways to save money on your home loan. Even a 0.20% reduction on a $600,000 mortgage saves you around $1,200 per year. Over five years, that is $6,000 back in your pocket.

Pro Tip: Use a mortgage adviser as your market intelligence tool. They have access to multiple lenders, understand which institutions are competing aggressively for new business, and can match your financial profile to the right product. This can save you not just money but enormous amounts of time and stress.

Our take: What most guides miss about interest rates

Most articles on this topic stop at listing current rates or explaining what the OCR is. That surface-level coverage misses the most valuable insight available to you as a borrower: understanding the chain from RBNZ decision to your repayment figure transforms you from a passive recipient of rates into an active negotiator.

We work with homeowners and buyers across Auckland and beyond, and the single biggest difference we see between people who secure great rates and those who do not is timing. Rates do not wait for you to feel ready. After an OCR cut cycle begins, the best fixed rate deals can appear and disappear within weeks as banks compete briefly before settling into a new normal.

There is also a dangerous assumption we see constantly: that loyalty to one bank equals a better deal. In reality, your existing bank has little incentive to offer you their sharpest rate unless they believe you are genuinely considering going elsewhere. Competition is your leverage. Using it requires preparation, which means knowing what the market is offering before you walk into any conversation.

The deeper lesson is this: interest rates are not something that happens to you. With the right knowledge and support, they are something you can navigate with confidence. Tracking RBNZ announcements, understanding how global markets feed into local rates, and working with an adviser who knows the current lending landscape can genuinely alter your financial future. The difference between a well-timed, well-negotiated mortgage and a default offer accepted without question can run into tens of thousands of dollars across the life of a loan.

Find the right mortgage advice for your rate strategy

Understanding how interest rates are set is genuinely empowering. But turning that understanding into a better mortgage outcome takes more than knowledge alone. It takes access to the right lenders at the right time.

At Mortgage Managers, our team of expert mortgage advisers is based in Hobsonville and works with homeowners and buyers across Auckland, the North Shore, West Auckland, and remotely throughout New Zealand. We help you make sense of OCR movements, compare real offers from multiple lenders, and time your decisions to align with market conditions. Whether you are buying your first home or refinancing an existing loan, explore our mortgage advisers home loan services, or check the latest current home loan rates to see where the market stands today.

Frequently asked questions

What is the Official Cash Rate (OCR) and why does it matter?

The OCR is the benchmark interest rate set by the Reserve Bank of New Zealand, and it directly influences what banks charge for home loans. A lower OCR generally means cheaper borrowing costs, as the RBNZ’s OCR decisions flow through to mortgage rates across the market.

Can banks offer different mortgage rates to the same borrower?

Yes, banks assess borrower risk and compete for business differently, meaning rates can vary between lenders even for the same financial profile. This is why banks adjust rates after OCR changes at different speeds and by different amounts, making it worthwhile to compare multiple offers.

How often does the Reserve Bank change the OCR?

The Reserve Bank reviews the OCR approximately every six weeks, though it does not change the rate at every review. Decisions depend on inflation, employment data, and economic conditions, as the OCR impact on borrowing costs is significant and adjustments are made carefully.

Do international events impact New Zealand mortgage rates?

Yes, global economic shifts and central bank decisions overseas can affect the cost of funds for New Zealand banks, which can flow through to your mortgage. The key factors affecting mortgage rates include US Federal Reserve policy, Australian rate movements, and global investor confidence.

What’s the best way to secure a lower interest rate?

Comparing multiple lenders, timing your application around OCR announcements, and working with a mortgage adviser are the most effective strategies. As outlined in guidance on getting a better interest rate, negotiating actively rather than accepting the first offer can lead to meaningful savings over the life of your loan.