TL;DR:

- Securing an investment property mortgage in New Zealand requires larger deposits, stricter LVR, and careful DTI management due to tighter lending rules. Accurate assessment of your deposit, credit profile, income, and rental income is vital for approval, especially as rules tighten further in 2026. Understanding recent tax changes, such as full interest deductibility from April 2025, is essential to maximize investment returns and avoid costly mistakes.

Securing a mortgage for an investment property in New Zealand is a different ball game compared to buying your own home. Lending rules are tighter, deposits are larger, and tax changes have rewritten the rules on what you can claim. If you’ve been navigating rising interest rates, shifting DTI (Debt-to-Income) limits, and updated interest deductibility rules all at once, you’re not alone in feeling the pressure. This guide walks you through every critical step, from understanding the updated eligibility requirements to locking in a mortgage structure that genuinely works for your portfolio.

Table of Contents

- Investment property mortgage basics: what’s changed in 2026?

- Step-by-step guide to qualifying for an investment mortgage

- Navigating NZ tax rules: interest deductibility and ring-fencing

- Avoiding costly pitfalls: common mistakes NZ investors make

- Why a tailored mortgage strategy is essential for NZ property investors

- Speak to NZ mortgage experts for bespoke investment advice

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Higher deposit needed | Investment property mortgages require a larger deposit than owner-occupier loans in New Zealand. |

| DTI constraints apply | Both owner-occupier and investment loans are capped at six times gross income. |

| Interest deductibility restored | From April 2025, 100% mortgage interest can be claimed for eligible NZ investment properties. |

| Eligibility matters | Interest deductibility depends on property use and compliance with IRD rules. |

| Custom adviser support | A tailored mortgage approach is crucial to maximise investment returns and compliance. |

Investment property mortgage basics: what’s changed in 2026?

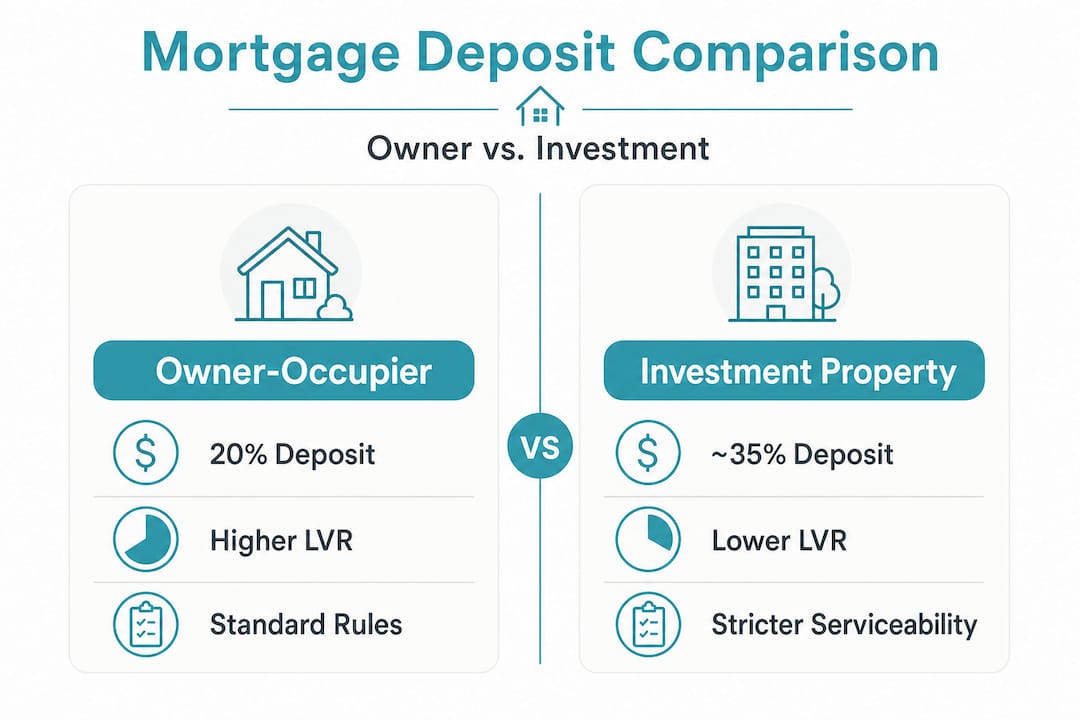

The gap between owner-occupier mortgages and investment property mortgages has never been wider. Banks and lenders treat these two loan types very differently, and knowing exactly what separates them is the first step to building a winning strategy.

The most immediate difference you’ll notice is the deposit requirement. For an owner-occupied home, most lenders accept a 20% deposit. For an investment property, you’re generally looking at a minimum of 35%, which means a higher loan-to-value ratio (LVR) restriction of 65% rather than the 80% available to owner-occupiers. This isn’t just a small hurdle. On a $900,000 Auckland property, that’s a difference of $135,000 in required capital upfront.

As investment-property lending confirms, stricter serviceability rules apply across the board, including higher deposit and LVR requirements alongside DTI-based constraints. Understanding the investment loan basics NZ framework helps you position your application before you even speak to a bank.

Here’s a quick comparison to put it in perspective:

| Feature | Owner-occupier | Investment property |

|---|---|---|

| Minimum deposit | 20% | ~35% |

| Maximum LVR | 80% | ~65% |

| DTI cap | 6× gross income | 6× gross income |

| Interest deductibility | Not applicable | Up to 100% (conditions apply) |

| Rental income counted | No | Yes (at a shade, typically 75%) |

The DTI cap is one area where both loan types now sit equally. Lenders assess your total debt across your entire portfolio against your gross income, so if you already carry existing mortgages, this can significantly limit your additional borrowing capacity.

Useful property investment tips NZ suggest reviewing your DTI position across all properties before making any offer, not after. Getting this calculation right early can save you from the frustration of conditional approvals that fall apart at the final hurdle.

Pro Tip: Ask your mortgage adviser to run a full portfolio DTI calculation before you make any offer. A single miscalculation can derail your entire application timeline.

Key points for 2026:

- Investment LVR cap sits at approximately 65%, meaning your equity or deposit must be at least 35%

- The 6× gross income DTI cap applies to your entire property portfolio, not individual loans

- Lenders assess rental income at a discounted rate, so your actual borrowing capacity may be lower than expected

- Recent regulatory updates have tightened scrutiny on interest-only loans for investment properties

Step-by-step guide to qualifying for an investment mortgage

Knowing the criteria is one thing. Knowing exactly how to meet them is where most investors find real clarity. Follow these steps sequentially, and you’ll walk into your lender meeting prepared and confident.

1. Assess your deposit position

Calculate whether you have at least 35% of the target property’s purchase price available, either in savings, existing equity, or a combination. Many investors use equity from their primary residence to fund this. If your equity is borderline, speak to a mortgage adviser before assuming you qualify.

2. Check your credit profile

Your credit score matters more than many investors realise. Obtain a free credit report and review it for errors or missed payments. Lenders want to see a clean repayment history, particularly across existing mortgages and credit facilities. Address any issues before you apply.

3. Compile your income documentation

Lenders need a complete picture of your income. This means recent payslips or financial accounts if self-employed, tax returns for the past two years, and evidence of any existing rental income. The mortgage steps NZ process outlines exactly what each lender category expects, which can vary significantly.

4. Calculate your DTI ratio accurately

Your DTI is calculated by dividing your total debt (across all properties and loans) by your gross annual income. The DTI lending constraints applied in New Zealand set this at a maximum of 6× gross income for both owner-occupiers and investors when assessed across a combined portfolio. If you earn $120,000 gross per year, your total permissible debt load sits at $720,000.

5. Get a property appraisal

Lenders will conduct their own valuation, but having an independent appraisal gives you a baseline and can prevent surprises. For high-value Auckland properties in particular, valuations can shift significantly from purchase price.

6. Consider non-bank lenders if mainstream options fall short

If your application doesn’t fit a major bank’s criteria, non-bank lenders offer more flexible assessment frameworks. They often accept more complex income structures or properties that fall outside standard categories. Rates may be higher, but the access they provide can be worth it.

7. Submit a complete application

A complete application means every document requested upfront, no gaps, no follow-ups. Incomplete submissions slow approvals significantly and can result in declined applications at busy lending periods.

Here’s what lenders typically assess:

| Assessment factor | What lenders look for |

|---|---|

| Deposit/equity | Minimum 35% for investment properties |

| Rental income | Typically assessed at 75% of market rent |

| Existing debt | Full portfolio reviewed for DTI compliance |

| Employment/income | Stable income for minimum 2 years |

| Credit history | Clean record, no defaults or arrears |

| Property type | Standard residential preferred; some restrictions on apartments |

The Auckland investment property guide outlines specific considerations for Auckland-based purchases, where valuations and competition add additional complexity to the process.

Pro Tip: Document every dollar of rental income and outgoings across your entire portfolio before applying. Lenders love clarity, and a well-organised financial picture can mean the difference between approval and a lengthy back-and-forth.

Navigating NZ tax rules: interest deductibility and ring-fencing

Getting your mortgage approved is a milestone. But understanding the tax landscape is what separates a good investment from a great one. The rules changed significantly in recent years, and 2025 brought a particularly meaningful shift.

From 1 April 2025, as confirmed by IRD’s guidance, you can claim 100% of interest you incur for residential rental property, subject to other deductibility rules and ring-fencing provisions. This is a welcome shift after a period of phased reductions that frustrated many landlords. But there’s a catch: eligibility is not automatic.

“From 1 April 2025 you can claim 100% of the interest you incur for residential rental property (subject to other deductibility rules/ring-fencing).” IRD, Property interest rules

The interest deductibility rules apply broadly. IRD’s ring-fencing rules cover almost any property with a dwelling, including long-term rentals, short-stay accommodation, and even vacant properties. Private use of a property, however, is excluded. If you use the property personally for any period, you need to apportion interest accurately.

Here’s what you need to confirm before relying on full deductibility:

- Purpose of the loan: The interest must relate directly to the income-earning use of the property. Personal use portions are not deductible.

- Property type: The rules cover residential properties with a dwelling, but specific exclusions apply. Confirm with IRD or your adviser.

- Ring-fencing: Rental losses can generally only offset other rental income, not your personal income. Losses may carry forward, but they don’t freely reduce your overall tax bill.

- Exclusions: Certain properties and loan structures are excluded. If your property is mixed-use, you’ll need to calculate the deductible portion carefully.

Understanding how interest rates impact your overall return is essential alongside these tax rules. A small movement in your mortgage rate can undo months of careful tax planning if you haven’t stress-tested your numbers.

Pro Tip: Don’t assume that because your property is rented out, all interest is fully deductible. Confirm your specific eligibility with IRD or a tax-aware mortgage adviser before filing your return.

Avoiding costly pitfalls: common mistakes NZ investors make

Every year, NZ investors lose thousands of dollars to avoidable mistakes. Some errors happen at the mortgage application stage; others creep in during tax time. Knowing where others stumble helps you stay on track.

Misjudging your deposit requirement

One of the most common early-stage mistakes is underestimating how much capital you need upfront. The minimum deposit sits at approximately 35% for most investment properties. Investors who plan based on owner-occupier rules and then scramble to find extra funds often end up missing purchase opportunities entirely.

Calculating DTI incorrectly

Your DTI calculation must account for all debt, not just the new loan you’re applying for. Investors who focus only on the target property’s mortgage, and overlook credit card limits, personal loans, or other mortgages, routinely find their application pulled back at assessment stage. Use a mortgage repayment calculator alongside a DTI review to stress-test your numbers before applying.

Assuming all rental interest is deductible

As IRD makes clear, interest deductibility is conditional on purpose, eligibility, and property type, with ring-fencing and exclusion rules limiting actual claims in many situations. Assuming you can deduct everything without checking the conditions is a costly mistake. Always verify your specific situation.

Failing to separate private and rental use

If you use your investment property personally at any point during the year, that portion of interest is not deductible. Investors who fail to accurately log private versus rental use find themselves facing IRD adjustments and penalties that erode their returns significantly.

Overlooking lender-specific criteria

Not all lenders assess investment mortgages the same way. Some count rental income more generously; others apply stricter stress-test rates. Submitting to the wrong lender wastes time and can result in a hard credit inquiry that affects your profile.

Key mistakes to avoid:

- Applying without a complete documentation package

- Relying on estimated rather than actual rental income figures

- Ignoring how existing debt affects your DTI cap

- Failing to reconfirm deductibility each tax year as your circumstances change

- Not seeking specialist mortgage advice before making an offer

Pro Tip: Reconfirm your deductibility position with IRD or your tax adviser each year, especially if your property use, loan structure, or income mix changes. What was eligible last year may have shifted.

Why a tailored mortgage strategy is essential for NZ property investors

Here’s an uncomfortable truth that many investors learn the hard way: a mortgage that worked perfectly two years ago may actively be working against you today. Rules change. Interest rates move. Tax policies shift. And a generic mortgage strategy built around yesterday’s conditions can leave real money on the table.

We’ve seen investors come to us after locking in structures that no longer aligned with updated DTI caps or post-2025 interest deductibility rules. The financial cost of misalignment isn’t always obvious until tax time or when they try to refinance and find their options are far narrower than expected.

A tailored mortgage strategy integrates three things most generic approaches ignore: your current tax position, your full portfolio lending capacity under today’s rules, and your medium-term investment goals. These three elements interact constantly. A loan structure that minimises your repayments today might limit your ability to access equity tomorrow.

Revisiting your mortgage structure annually, not just at loan approval, is where seasoned investors gain a genuine edge. As IRD confirms, full interest deductibility eligibility isn’t just time-based from 1 April 2025. It’s conditional on ongoing usage, property type, and exclusion checks. An annual review catches changes before they become expensive surprises.

The investors who thrive long-term follow property success tips NZ that go beyond simply securing the lowest rate. They treat their mortgage as a living part of their investment plan, one that needs active management, not just a set-and-forget approach. That’s the mindset shift that separates average portfolios from excellent ones.

Speak to NZ mortgage experts for bespoke investment advice

Navigating investment property finance alone is like driving in an unfamiliar city without a map. You might eventually reach your destination, but the detours are expensive and time-consuming.

At Mortgage Managers, our Auckland-based team of mortgage advisers works with NZ investors to build mortgage strategies that align with both their lending position and their long-term financial goals. We’re locally owned, based in Hobsonville, and well positioned to serve investors across Auckland, the North Shore, West Auckland, and remotely throughout New Zealand. Whether you’re building your first investment portfolio or refinancing an existing one, we help you cut through the complexity and make confident, well-informed decisions. Visit Mortgage Managers to speak with an adviser who understands the NZ investment landscape from the inside.

Frequently asked questions

What is the minimum deposit required for investment property mortgages in New Zealand?

A minimum deposit of around 35% is typically required for investment property mortgages, compared to 20% for owner-occupier loans. This higher threshold reflects the increased risk lenders associate with investment lending.

Can I claim 100% mortgage interest as a deduction on investment property in NZ?

From 1 April 2025, you can generally deduct 100% of interest on eligible residential rental properties, provided you meet IRD’s conditions around property use, loan purpose, and ring-fencing rules.

Does mortgage interest deductibility apply to short-term rentals and vacant properties?

Yes, IRD’s rules extend to various rental uses including short-stay accommodation and vacant properties with a dwelling, though interest relating to private use is excluded from deductibility.

What is the DTI ratio for investment property mortgages?

The DTI (Debt-to-Income) limit is generally 6× gross income applied across your combined portfolio of owner-occupier and investment loans, not on a property-by-property basis.