TL;DR:

- Your deposit size fundamentally influences your loan options, interest rates, and approval likelihood.

- Knowing your LVR enables you to choose suitable schemes and lenders, saving you time and money.

- A strategic deposit, combined with financial preparation and expert advice, maximizes your borrowing power.

Many first home buyers assume that any deposit will open the same doors when applying for a home loan. The reality is quite different. The size of your deposit doesn’t just influence how much you can spend on a home; it fundamentally determines which loan products you can access, what interest rates banks will offer you, and how many hoops you’ll need to jump through before getting approved. Understanding this connection early can save you thousands of dollars and months of frustration.

Table of Contents

- Why deposit size matters: the basics explained

- How much deposit you need: standard, low, and edge cases

- Deposit size and its impact on borrowing power

- Weighing the pros and cons of smaller versus larger deposits

- What most buyers miss about deposit size (and how to think smarter)

- Get expert support for your first home loan deposit decision

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Deposit size equals leverage | The money you put down determines your loan options, rates, and how much you can borrow as a first home buyer. |

| 10–19% is possible | Many FHBs succeed with deposits below 20%, but you must navigate more hoops and lender restrictions. |

| Schemes help but don’t solve all | Government-backed loans like Kāinga Ora allow just 5%, but income and serviceability limits still apply. |

| Bigger deposit, bigger advantage | Saving more unlocks lower rates, more lender choice, and higher long-term security for your home. |

Why deposit size matters: the basics explained

Your deposit is far more than a show of good faith to a lender. It’s the single most powerful variable in your mortgage application. Here’s why: the amount you put down sets your loan-to-value ratio, or LVR, which banks use to classify your application as either standard or high risk.

Understanding LVR is genuinely one of the most important things you can do as a first home buyer. LVR is calculated by dividing your loan amount by the property value. So if you buy a $700,000 home with a $140,000 deposit, your LVR is 80%. That 80% threshold is significant.

According to the Reserve Bank of New Zealand, standard deposit requirements for first home buyers sit at 20%, which achieves an LVR of 80% or lower. This is the sweet spot where banks treat your application as standard lending, offer their most competitive rates, and face no restrictions on how many loans like yours they can approve.

Drop below that 20% deposit, and you enter high-LVR territory. That’s where things get more complicated.

“Your deposit percentage isn’t just a number—it’s a signal to your lender about how much risk they’re taking on. The more you contribute upfront, the more comfortable banks feel offering you their best terms.”

Here’s a quick summary of why deposit size is so pivotal:

- LVR below 80% (20%+ deposit): Standard lending, competitive rates, no quota restrictions

- LVR between 80% and 90% (10–19% deposit): High-LVR category, limited by Reserve Bank quotas

- LVR above 90% (less than 10% deposit): Highly restricted, mostly only accessible through government-backed schemes

The Reserve Bank places firm limits on how many high-LVR loans banks can issue at any given time. This means even if you meet all other criteria, a bank might simply not have room in its high-LVR quota to approve your application.

Pro Tip: Before you start home hunting, check the NZ deposit requirements that apply to your situation. Knowing your LVR position ahead of time means fewer surprises when you’re sitting across from a bank manager.

With the big picture set, let’s break down how different deposit sizes map to your options.

How much deposit you need: standard, low, and edge cases

Now that you know deposit size is the gatekeeper, let’s match common deposit levels to the options available. The table below gives you a clear snapshot of where different deposit amounts place you.

| Deposit amount | LVR | Loan type available | Key restrictions |

|---|---|---|---|

| 20% or more | 80% or below | Standard bank lending | None for LVR; best rates apply |

| 10–19% | 81–90% | High-LVR lending | Subject to Reserve Bank quotas |

| 5% | 95% | Kāinga Ora First Home Loan | Income caps, eligibility criteria |

| Less than 5% | Above 95% | Extremely rare | Family gifts, new builds only |

The Kāinga Ora First Home Loan is a genuine game-changer for eligible buyers. This government-backed scheme allows first home buyers to purchase with as little as a 5% deposit, sitting outside the standard Reserve Bank LVR restrictions. To qualify, you need to be a genuine first home buyer, earn no more than $95,000 as an individual or $150,000 as a household, and meet the scheme’s property price caps. These thresholds vary by region, so it’s worth checking current limits for your area.

What about deposits under 10% outside of government schemes? According to LVR restrictions data, low deposit options under 10% are rare without Kāinga Ora involvement, a qualifying family gift, or purchasing a new build. These edge cases come with stricter criteria and carry higher risk in the eyes of lenders.

Here are the most common edge cases where less than 10% can still get you into a home:

- Family gift or contribution: A gifted deposit from immediate family can supplement your savings, though banks will verify it’s a genuine gift and not a loan.

- New build exemptions: New builds often sit outside standard LVR restrictions, meaning some lenders will consider lower deposits for properties still under construction or recently completed.

- Welcome Home or regional schemes: Some local and regional programmes occasionally offer additional support for eligible buyers.

The government’s first home buying guide confirms that Kāinga Ora remains the primary pathway for buyers with only 5%, and that income and first-time buyer status are both checked carefully before approval.

If you’re exploring low deposit lender options, the landscape can feel like a maze. Not every bank participates in every scheme, and availability changes based on quotas and market conditions. This is exactly where professional guidance pays off.

Deposit size and its impact on borrowing power

After mapping loan options, let’s connect deposit size with the all-important question: how much you can actually borrow.

A common misconception is that meeting the minimum deposit automatically means you’ll borrow as much as you need. In practice, lenders run two separate tests on your application. The first is the LVR test, which checks your deposit size against the property value. The second is the serviceability or affordability test, which checks whether your income is sufficient to comfortably repay the loan.

Here’s a step-by-step look at how banks calculate your maximum borrowing capacity:

- Determine your deposit and LVR: Your deposit establishes the upper boundary of the property price you can access and the loan category you fall into.

- Apply income and expense analysis: Banks look at your gross income, existing debts, regular expenses, and dependants to calculate your net disposable income.

- Stress test your repayments: Lenders add a buffer of typically 2–3% above the current interest rate to see if you could still afford repayments if rates rose.

- Apply DTI limits: The debt-to-income ratio caps how much total debt you can hold relative to your annual income, typically no more than six times your gross income under current Reserve Bank guidance.

- Arrive at maximum borrowing: The lowest figure produced by the LVR, serviceability, and DTI tests becomes your approved limit.

According to the Reserve Bank, LVR classification determines whether you access standard unlimited lending or quota-limited high-LVR lending, directly affecting how many lenders are willing and able to approve you. A larger deposit doesn’t just lower your loan amount; it opens up more lenders, more competitive rates, and stronger negotiating power.

The impact of LVR on borrowing is worth understanding before you set a price target. Buyers with 20% deposits are dealing with far more lenders willing to compete for their business, which can mean meaningfully better rates over the life of a 25 or 30 year loan.

Canstar’s research into borrowing capacity confirms that even with a low deposit accessed through a scheme like Kāinga Ora, the DTI and serviceability stress tests can become the real limiting factor, particularly for buyers with moderate to higher incomes and existing financial commitments.

| Deposit | LVR | Lender options | Rate competitiveness | Risk of quota rejection |

|---|---|---|---|---|

| 20% or more | 80% or below | All major banks | Best available | None |

| 10–19% | 81–90% | Selected lenders | Moderate | Moderate to high |

| 5% (Kāinga Ora) | 95% | Scheme participants only | Limited | Scheme-based |

Pro Tip: Run your numbers before you fall in love with a property. Use an online borrowing calculator to estimate your range, then speak to a mortgage adviser who can stress-test those numbers against real lender criteria.

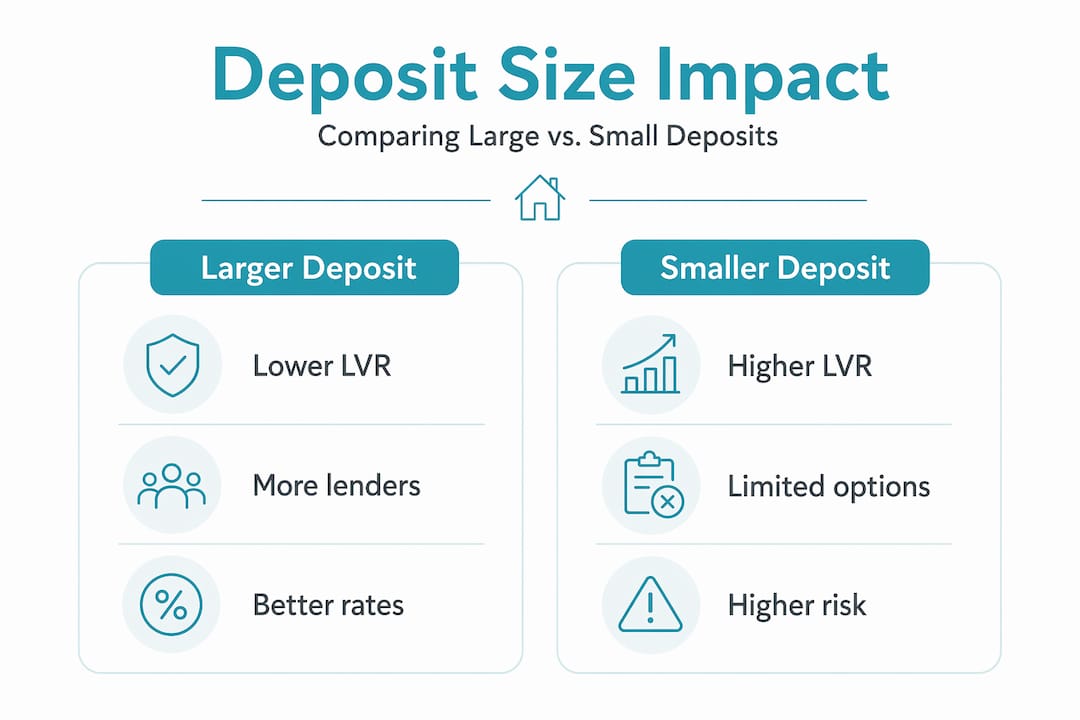

Weighing the pros and cons of smaller versus larger deposits

Trade-offs matter. Let’s compare the real impact of deposit decisions and look at shifting trends in the New Zealand market.

Saving a 20% deposit can feel like a marathon, especially in Auckland and other high-demand areas where property prices remain elevated. It’s understandable to ask whether it’s worth waiting, or whether buying sooner with a smaller deposit is the smarter move.

Benefits of a 20%+ deposit:

- Access to the full range of lenders and loan products

- Lowest available interest rates, which can save tens of thousands over the loan term

- No exposure to Reserve Bank quota restrictions

- A stronger equity buffer if property values shift

- No need to navigate complex eligibility criteria or scheme income caps

Downsides of buying with a minimum deposit:

- Limited to quota-based high-LVR lending, which can mean rejections even when you meet financial criteria

- Higher interest rates applied by lenders to compensate for increased risk

- Potential for a low-equity premium or fee added to your loan

- Narrower choice of lenders means less room to negotiate

According to recent RNZ reporting on first home buyers, New Zealand first home buyers are increasingly entering the market with deposits between 10% and 19%, using high-LVR quota allocations to get in. The trend shows that waiting for 20% isn’t always the path buyers choose, but 20% remains the optimal threshold for rates and equity protection.

When buying sooner with a smaller deposit might make sense:

- Property values in your target area are rising faster than you can save

- You have strong, stable income and can comfortably service the loan

- You qualify for Kāinga Ora or another scheme that removes some of the extra cost burden

- You have a family gift or KiwiSaver funds ready to support your deposit

Learning how to boost your deposit before you apply is one of the best investments of your time. Even moving from 10% to 15% can meaningfully change your lender options and rate outcomes.

What most buyers miss about deposit size (and how to think smarter)

After comparing pros and cons, here’s a fresh take on how to approach your deposit strategy.

Most first home buyers treat deposit saving as a hurdle to clear as quickly as possible. They ask: “What’s the minimum I need?” Then they target that figure and stop. This framing, while understandable, misses something important.

Your deposit is not just a barrier; it’s actually a lever. The more you can contribute, the more negotiating power you hold. Banks compete for well-capitalised borrowers. If your LVR is 75% rather than 90%, you’re a fundamentally different risk proposition in the eyes of a lender, and they’ll price their products accordingly.

Here’s the counter-intuitive insight that many buyers miss: for some higher-income first home buyers, the deposit is not the hardest part of the equation at all. The DTI ratio and serviceability test are. If you earn $120,000 a year and have student debt, car finance, and a credit card balance, your borrowing power can be capped well below what a 20% deposit alone would suggest. In these cases, clearing existing debt before applying can do more for your borrowing capacity than adding another $10,000 to your deposit.

Don’t let the 20% rule paralyse you. Many buyers enter the market successfully at 10 to 19%, particularly when they’ve prepared their finances carefully and worked with a knowledgeable mortgage adviser to find lenders with available high-LVR quota allocations. The key is preparation, not perfection.

The smarter approach is to work backwards. Ask yourself what monthly repayments you can comfortably afford, then work out what loan size that supports, then figure out what deposit you need to unlock that loan from the widest possible pool of lenders. If you’re eligible for the First Home Grant, factoring that into your deposit calculation can also shift the picture materially.

Deposit strategy is ultimately about finding the right balance between what you have now, what the market demands, and what your income can genuinely sustain over decades.

Get expert support for your first home loan deposit decision

Navigating deposit thresholds, LVR classifications, government schemes, and DTI limits is genuinely complex, and making the wrong call can cost you more than you realise. The good news is that you don’t have to work through it alone.

At Mortgage Managers, our expert mortgage advisers work with first home buyers across Auckland, the North Shore, West Auckland, and throughout New Zealand to make sense of exactly these decisions. We’ll help you understand your LVR position, identify which lenders have quota availability, assess your eligibility for schemes like Kāinga Ora, and model your borrowing power against real repayment scenarios. Understanding the mortgage adviser’s role in your journey means you’ll have a trusted guide in your corner when it matters most. Reach out to our team today for a no-pressure conversation about your deposit situation and what’s genuinely possible for you.

Frequently asked questions

Is it better to wait to save a 20% deposit before buying your first home in New Zealand?

While a 20% deposit unlocks the best rates and broadest lender options, many first home buyers successfully enter the market with 10 to 19% if they’re prepared for additional requirements. According to recent data on FHB deposits, this trend is growing, though 20% remains the optimal threshold for rates and equity protection.

Can you really buy a home with less than 10% deposit in NZ?

It is possible through Kāinga Ora loans, a qualifying family gift, or purchasing a new build, but these pathways are uncommon and carry stricter criteria. LVR restriction data confirms that sub-10% deposits outside government schemes come with significantly higher scrutiny from lenders.

What is LVR and why does it matter for deposit size?

LVR stands for loan-to-value ratio, which compares your loan amount to the property’s value and tells lenders how much risk they’re carrying. The Reserve Bank’s LVR rules use this ratio to set lending restrictions, making it the most direct way your deposit size shapes your borrowing options.

If I qualify for a Kāinga Ora loan, does deposit size still matter?

Yes, absolutely. While Kāinga Ora allows you to buy with as little as 5%, your income, existing debts, and repayment capacity still determine how much you can borrow. Serviceability testing data shows that DTI and stress-tested repayments can cap your borrowing even when your deposit meets the scheme’s requirements.