TL;DR:

- Bankruptcy significantly impacts your credit file in New Zealand, restricting access to loans and rentals for several years. Understanding reporting timelines and lender risk appetites is crucial in strategically rebuilding your creditworthiness for future homeownership. Proactive financial discipline and expert guidance can improve your prospects despite a challenging credit history.

Bankruptcy leaves a mark that many New Zealanders underestimate when they begin thinking about homeownership again. It is not just about a few months of reduced credit access. Insolvency procedures affect your credit rating and can restrict your ability to access credit for a house or even rent a property, sometimes for years after the event itself. If you are wondering whether a path back to homeownership exists after bankruptcy, the honest answer is yes, but only if you understand the landscape clearly and take deliberate, strategic steps.

Table of Contents

- How bankruptcy changes your borrowing power in New Zealand

- Timeline: How long bankruptcy stays on your credit record

- Borrowing options after bankruptcy: What lenders really see

- Steps to rebuild credit and improve borrowing prospects

- Beyond the credit file: Why real-world borrowing after bankruptcy is more nuanced

- Find tailored support for your home loan journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Bankruptcy impacts credit | Your credit rating is restricted for at least four years after bankruptcy discharge in New Zealand. |

| Duration varies by procedure | Bankruptcy and No Asset Procedures stay on your file for four years, Debt Repayment Orders for five years. |

| Lenders review multiple factors | Approval depends on time since discharge, improved credit history, and lender risk appetite. |

| Rebuilding credit matters | Taking steps to repair your credit and seeking expert advice can boost your borrowing chances post-bankruptcy. |

| Specialist advice helps | Mortgage advisers experienced in complex credit situations can increase your odds of loan approval. |

How bankruptcy changes your borrowing power in New Zealand

From establishing bankruptcy’s impact, let us examine how these changes play out in real borrowing scenarios. Bankruptcy is not simply a paperwork event that disappears when the process is over. It sends a powerful signal to every lender who looks at your credit file, and that signal does not fade quickly.

When a lender considers your home loan application, their first question is always about risk. A bankruptcy record tells them that at some point you were unable to meet your financial obligations. Even if your circumstances have changed completely, that historical record shapes how they interpret your application today.

Here is what bankruptcy directly affects when you try to borrow:

- Home loan eligibility: Most mainstream banks require a clean or near-clean credit history and will decline applications with recent insolvency events.

- Rental access: Finding a landlord willing to rent to you becomes harder because many landlords run credit checks before approving tenancy applications.

- Car finance and personal loans: These are often declined or offered at significantly higher interest rates to account for perceived risk.

- Hire purchase and credit accounts: Retailers offering buy-now-pay-later or store credit will also see the bankruptcy record.

- Utility and phone contracts: Some providers check credit files before offering post-pay arrangements.

“Insolvency affects your credit rating and can make it difficult to find a money lender willing to give you credit to buy things like a car or house, and to find landlords willing to rent to you.”

— New Zealand Insolvency and Trustee Service

Understanding these consequences helps you plan rather than be surprised. For a broader picture of how negative credit events affect your borrowing profile in New Zealand, it is worth familiarising yourself with the full range of issues that lenders assess.

The important thing to recognise is that bankruptcy does not make borrowing permanently impossible. It makes it harder for a defined period, and that period is manageable if you know what you are working with.

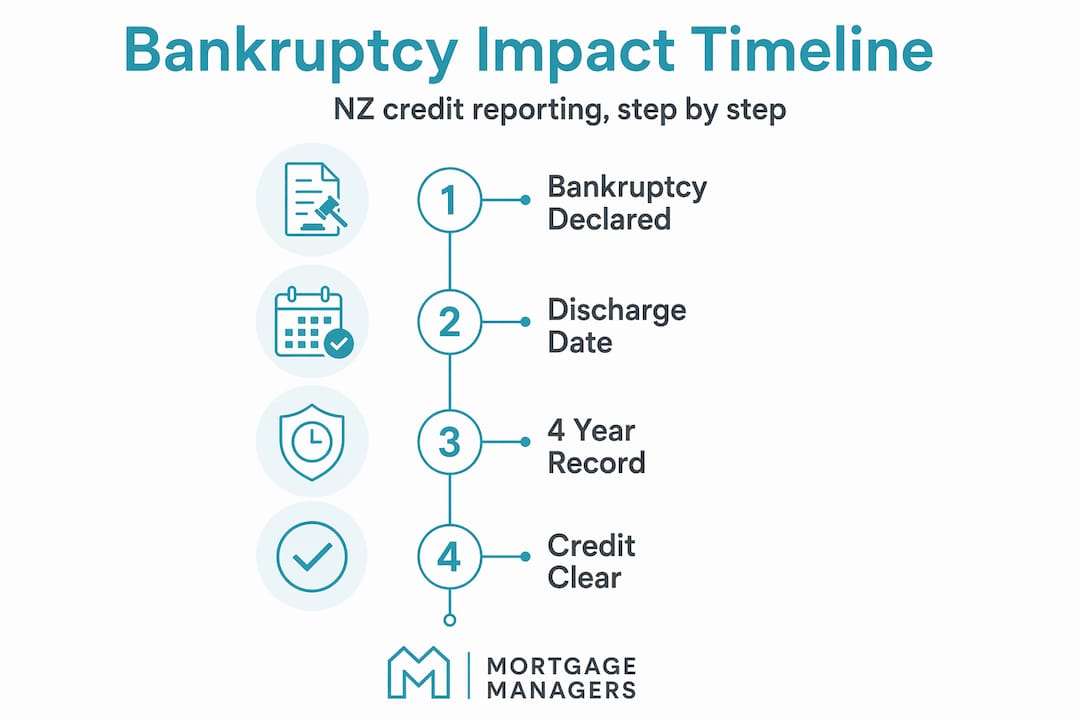

Timeline: How long bankruptcy stays on your credit record

Now that we understand bankruptcy’s impact, let us break down the reporting timelines and their practical consequences. One of the most common misconceptions is that bankruptcy “falls off” your credit file the moment you are discharged. That is not how it works in New Zealand.

Your discharge date is the starting point for a new countdown, not the finish line. Credit reporting agencies maintain insolvency information for several years after discharge, and different types of insolvency procedures have different reporting periods.

| Insolvency type | Reporting duration | Counted from |

|---|---|---|

| Single bankruptcy | 4 years | Date of discharge |

| No Asset Procedure (NAP) | 4 years | Date of discharge |

| Debt Repayment Order | 5 years | Date of order |

According to Centrix credit file documentation, a single bankruptcy is reportable for 4 years from the date of discharge, while a Debt Repayment Order remains visible for 5 years from the date of the order itself. This distinction matters enormously depending on which insolvency path you went through.

For New Zealanders who experienced bankruptcy or a No Asset Procedure, credit reporting is generally kept for a further 4 years after discharge. That means if you were discharged in early 2022, the record could remain visible to lenders until early 2026.

Key figures to keep in mind:

- Bankruptcy discharge typically occurs 3 years after the adjudication date in New Zealand, unless discharged earlier.

- The 4-year credit reporting period begins after discharge, not after adjudication.

- Total potential credit file visibility from adjudication to removal can therefore span 7 years or more in practice.

Pro Tip: Request a copy of your own credit file from a New Zealand credit reporting agency before you apply for any loan. Knowing exactly what lenders will see puts you in a far stronger position to address concerns proactively.

The timeline has real consequences beyond just mortgage applications. Landlords checking your credit file during that 4-year window will see the bankruptcy record. So will utility companies and phone plan providers. Understanding how long different credit events last in NZ helps you map out a realistic plan for when and how to approach different types of borrowing.

If you are seriously exploring getting a mortgage after bankruptcy, timing your application strategically around these reporting windows can make a meaningful difference to your approval prospects.

Borrowing options after bankruptcy: What lenders really see

Understanding timelines helps, but you need to know how lenders interpret those records in real-world borrowing decisions. Not all lenders respond to a bankruptcy record in the same way, and this is where many borrowers either give up too early or apply to entirely the wrong lenders.

Official documentation confirms that lending outcomes are determined by individual lenders’ risk appetite and lending criteria, not simply by the existence of a bankruptcy record. That is a genuinely important insight. There is no universal rule that says “no mortgage for 4 years after discharge.” Each lender makes their own assessment.

Here is how different lenders tend to approach post-bankruptcy applications:

| Lender type | Typical stance | Key considerations |

|---|---|---|

| Major trading banks | Generally conservative | May require 4+ years clear of all insolvency events |

| Non-bank lenders | More flexible | Will often lend sooner but at higher interest rates |

| Specialist credit providers | Case by case | Focus on current income and repayment behaviour |

| Building societies | Varies | Some more community-focused in their assessment |

The factors that most influence a lender’s decision after bankruptcy include:

- Time since discharge: The further you are from your discharge date, the more comfortable most lenders become. Even 12 to 18 months of post-discharge good behaviour can shift a lender’s perception.

- Repayment history since discharge: Consistent, on-time repayments on any subsequent credit accounts are powerful evidence that your financial behaviour has changed.

- Stable, verifiable income: Lenders want to see that you can service the loan. Documented income from employment or a well-established business is critical.

- Savings and deposit size: A larger deposit reduces a lender’s risk exposure. If you can present a genuine savings history alongside a healthy deposit, it speaks volumes about your discipline.

- Reasons for the original bankruptcy: Not all bankruptcies stem from reckless spending. A medical crisis, job loss, or relationship breakdown is viewed differently to a pattern of financial mismanagement.

Pro Tip: When preparing your application, write a clear and honest explanation of what led to your bankruptcy and what has changed since. Lenders who take a case-by-case approach respond well to borrowers who demonstrate self-awareness and a plan.

If your credit has other complications alongside the bankruptcy record, understanding how to qualify for a mortgage with defaults in New Zealand will give you a clearer picture of the full landscape. It is also worth knowing that refinancing your non-bank mortgage is a realistic path for borrowers who started with a specialist lender and want to move to a more competitive rate once their credit profile improves.

If you are working on improving your overall home loan eligibility, taking a structured approach over 12 to 24 months can genuinely shift where you sit on a lender’s risk scale.

Steps to rebuild credit and improve borrowing prospects

With context on lender behaviour, here is how you can proactively rebuild your borrowing profile. The mechanics of post-bankruptcy borrowing in New Zealand revolve around two things: the timeline of what is visible to lenders, and the quality of your financial behaviour within that timeline.

The discharge date determines how long the record is typically kept, generally 4 years after discharge. But what you do during those 4 years shapes whether a lender sees a risk or a recovery story.

Here are the most effective strategies for rebuilding your credit and borrowing profile:

- Check your credit file regularly: Know exactly what is on your file and dispute any inaccuracies immediately. Errors on credit files are more common than people realise.

- Make every repayment on time: Even small credit commitments like a mobile phone plan or a low-limit credit card help build a positive payment pattern.

- Avoid multiple credit applications in a short period: Each application leaves a footprint on your file, and multiple enquiries in a short window signal financial distress to lenders.

- Build genuine savings: A consistent savings pattern demonstrates financial discipline. Many lenders want to see at least three to six months of regular savings deposits before approving a home loan.

- Reduce existing debt: High levels of existing debt relative to your income make lenders nervous. Paying down balances before applying strengthens your application considerably.

- Document your income carefully: Self-employed borrowers or those with variable income should keep thorough financial records. Two years of tax returns and financial statements can make a strong case.

- Work with a mortgage adviser: A specialist adviser who understands post-bankruptcy lending in New Zealand can identify the right lenders, structure your application strategically, and help you avoid wasting credit enquiries on applications likely to fail.

Pro Tip: Start your credit rebuilding process the day after your discharge, not the year before you want to buy a home. The earlier you build positive credit history, the stronger your profile will be when you are ready to apply.

For a structured approach to rebuilding your credit after bankruptcy, understanding the specific steps that New Zealand lenders value most is essential. If you want to start with the fundamentals, fixing your credit before buying a home is a practical place to begin. You can also explore credit repair basics for home loan success and credit score improvement tips for first home buyers in 2026.

Beyond the credit file: Why real-world borrowing after bankruptcy is more nuanced

Let us close with a reality check that helps you move beyond the paperwork and see what really matters to lenders. There is a tendency to treat the credit file as the final word on your borrowing prospects. It is not.

Here is an insight that many people miss: credit reporting retention differs by procedure type. Two people who went through insolvency at the same time, but via different procedures, will have records visible for different durations. Someone who went through a Debt Repayment Order may carry a visible record for 5 years from the date of the order, while someone who was discharged from bankruptcy faces a 4-year post-discharge window. This is an edge case that most borrowers and even many advisers overlook. Knowing your specific procedure type matters when you are planning your application timeline.

The broader point is this: official guidelines describe what can appear on your credit file and for how long. They do not describe how individual lenders will interpret that information. A lender with a conservative credit policy might automatically decline any application showing insolvency within the last 4 years. Another lender might look at the same file, see 2 years of clean repayment history post-discharge, a stable income, and a 20% deposit, and approve the loan.

We have seen borrowers who assumed they were completely ineligible, when in reality they just needed to be matched with the right lender at the right time. We have also seen borrowers who applied too early, accumulated multiple declined applications, and damaged their credit file further in the process. Strategic action and expert credit rebuilding advice can genuinely tip the odds in your favour.

The question of mortgage approval after bankruptcy is not a yes or no question. It is a question of timing, preparation, and knowing which lenders to approach. That is where specialist guidance becomes genuinely transformative.

Find tailored support for your home loan journey

Navigating borrowing after bankruptcy in New Zealand is complex, but it is absolutely manageable with the right support. Knowing the timelines, understanding what lenders look for, and taking systematic steps to rebuild your credit profile are the foundations of a strong application.

At Mortgage Managers, we work with New Zealanders who are navigating exactly these kinds of complex credit situations. Our team of Auckland-based mortgage advisers understands how to structure applications for borrowers with challenging credit histories, and we know which lenders are genuinely open to post-bankruptcy applicants. Whether you are in Hobsonville, the North Shore, West Auckland, or anywhere in New Zealand, we can help you build a clear, realistic path toward homeownership. Find a mortgage broker who will treat your situation as an opportunity, not an obstacle. Think of us as your personal mortgage adviser, here to shop the market on your behalf and find the right solution for your unique circumstances.

Frequently asked questions

How long does bankruptcy affect my ability to borrow in New Zealand?

Bankruptcy information is reportable for 4 years from the date of discharge, meaning lenders can see this record and may factor it into their decision throughout that period.

Can I get a home loan after bankruptcy in New Zealand?

It is possible, but approval depends on how long ago you were discharged, your current credit behaviour, and the specific risk appetite of each lender you approach.

Will bankruptcy affect my ability to rent in New Zealand?

Yes. Bankruptcy can make it difficult to find landlords willing to rent to you, because many landlords run credit checks as part of their standard tenancy application process.

Are all insolvency events treated the same by lenders?

No. Credit reporting retention differs by procedure type, so bankruptcy and No Asset Procedures carry a 4-year post-discharge window, while Debt Repayment Orders are visible for 5 years from the date of the order.

How can I improve my chances of getting a loan after bankruptcy?

Focus on building a consistent repayment history, save regularly to demonstrate financial discipline, check your credit file for errors, and seek support from a specialist mortgage adviser who understands post-bankruptcy lending in New Zealand.