TL;DR:

- Most Kiwi homeowners view fixed rate choices as one-time decisions at purchase, but in reality, borrowers refix every one to three years, affecting multiple points over a 25-year mortgage. Proper management of rollover, break fees, and splitting loans can save thousands, with strategic preparation essential for optimizing outcomes and avoiding costly floating rates. Working with mortgage experts helps navigate fixed periods, negotiate better rates, and build a system to monitor each decision point effectively.

Most Kiwi homeowners think of choosing a fixed rate as a one-off decision when they buy. The reality is quite different. With borrowers refixing every one to three years, a typical 25-year mortgage involves dozens of separate rate decisions across its life. Getting fixed rate periods explained properly from the start means you understand not just what you are signing up for today, but the full cycle of decisions ahead. This guide covers how fixed periods work, what happens at rollover, break fees, and how to manage the whole process without losing money through inaction.

Table of Contents

- Key takeaways

- How fixed rate periods work in NZ

- What happens when your fixed term ends

- Breaking a fixed rate early: what it costs

- Fixed vs floating vs split loans

- Practical strategies for managing your rate rollovers

- My take on the cycle most borrowers underestimate

- Let Mortgagemanagers handle your next refix

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Fixed terms lock your rate | NZ fixed periods run from 6 months to 5 years, keeping repayments stable regardless of OCR changes. |

| Rollover inaction is costly | Doing nothing at term end usually triggers a floating rate up to 2.5% higher than fixed, adding thousands in annual interest. |

| Break fees can be significant | Early exit costs depend on rate differentials and remaining balance, and can range from zero to over $30,000. |

| Splitting your loan reduces risk | Staggering fixed terms across loan portions spreads rollover dates and smooths refinancing exposure. |

| Proactive refixing saves money | Setting reminders 30 to 45 days before expiry gives you time to compare offers and negotiate a better rate. |

How fixed rate periods work in NZ

A fixed rate period is a set timeframe during which your home loan interest rate stays the same, regardless of what happens in financial markets. Your lender locks in a rate at the start of the term, and your repayments remain constant until the period ends.

NZ fixed rate home loans are typically available across the following terms:

- 6 months for short-term certainty or rate positioning

- 1 year the most popular choice among Kiwi borrowers

- 2 years offering a balance of certainty and flexibility

- 3 years suited to those wanting longer-term stability

- 5 years the longest standard fixed period in New Zealand

During your fixed term, the Reserve Bank of New Zealand can lift or cut the Official Cash Rate as much as it likes, and your repayments will not move. That protection is the core appeal of fixing. Your repayments are calculated based on the fixed interest rate, your loan balance, and the remaining loan term, using standard amortisation. This means each payment covers interest first, with the remainder reducing your principal.

The certainty fixed periods offer makes budgeting far more manageable, particularly if you are a first-time buyer stretching your finances. You know exactly what you are paying for the entire term. That said, understanding fixed rate loans means accepting a trade-off. Certainty comes at the cost of flexibility, and that flexibility question becomes much more pressing when your term ends.

What happens when your fixed term ends

This is where a lot of borrowers get caught out. When your fixed period expires, your loan does not simply continue at the same rate. Three things can happen: your lender moves your loan onto their floating rate, you refix for a new term, or you refinance with a different lender.

The trap most borrowers fall into is option one. If you take no action, your bank will typically roll your loan onto its standard floating rate. Floating rates in NZ run roughly 1.5 to 2.5 percentage points above recent fixed rates. On a $500,000 mortgage, that difference can add more than $8,000 in extra interest per year. That is money you could have saved simply by being organised.

Banks do give you a window to act. Most NZ lenders allow you to lock in a new fixed rate 30 to 90 days before your current term expires. This rate-lock window is your opportunity to compare the market, negotiate with your current lender, and potentially refinance before the rollover happens.

Here is how to manage the rollover process well:

- Record your expiry date when you first take out or refix your loan, and set a calendar reminder 60 days before.

- Check current market rates from multiple lenders a few weeks before that reminder triggers.

- Contact your existing lender and ask what rate they can offer for your next fixed term.

- Get competing offers from other lenders, either directly or through a mortgage adviser.

- Decide and lock in your preferred rate before expiry to avoid any gap on a higher floating rate.

Pro Tip: Banks rarely offer their best rate automatically at rollover. You almost always need to ask, compare, or bring in a competitor’s offer to get a better deal. Silence tends to favour the bank, not you.

Breaking a fixed rate early: what it costs

Sometimes life changes. You might sell your home, want to refinance to a lower rate, or need to restructure your loan mid-term. When you exit a fixed rate period before it ends, your lender will typically charge a break fee.

Break fees compensate the bank for the interest it expected to receive for the remainder of your fixed term. The calculation is based on the difference between your contracted fixed rate and the current wholesale swap rate for the remaining term, applied to your outstanding balance.

| Scenario | Rate situation | Likely break fee |

|---|---|---|

| Rates have risen since you fixed | Current rates above your fixed rate | Zero or near zero |

| Rates have fallen slightly | Small drop in current rates | Low to moderate fee |

| Rates have fallen significantly | Large drop in current rates | High fee, potentially $10,000 to $30,000+ |

| Selling property and repaying loan | Depends on rate movements | Variable, request estimate from lender |

Break fees can range from zero to over $30,000 depending on how much rates have moved since you fixed. If rates have risen above your fixed rate, you might actually pay nothing to break because the bank can relend those funds at a higher rate. If rates have fallen considerably, the bank takes a real financial hit and passes that cost to you.

One critical point most guides miss: break fees use wholesale swap rates, not retail interest rates, in their calculation. This means the final number is unpredictable until you ask your lender for a written estimate. You must request this estimate before making any decision to break. Do not assume the number is manageable. Get it in writing first.

Pro Tip: If you are considering breaking a fixed term to chase a lower rate, request the break fee estimate and then calculate whether the interest savings over the new term actually outweigh the upfront cost. The break fee needs to be recovered before you are genuinely better off.

For a detailed breakdown of how these costs apply in Auckland and across New Zealand, the team at Mortgagemanagers has covered break fee mechanics in depth.

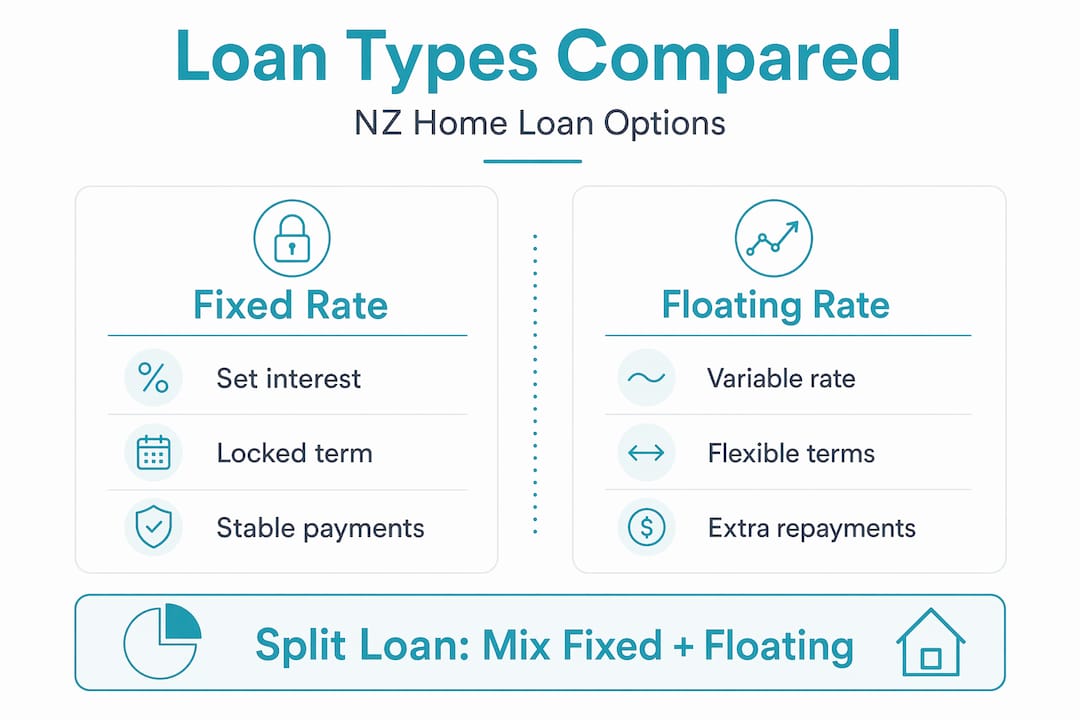

Fixed vs floating vs split loans

The fixed rate vs variable rate question is one of the most debated topics in New Zealand mortgage planning, and there is no universal right answer. The best choice depends on your financial situation, your risk tolerance, and what you think might happen with interest rates.

Fixed rate loans tend to offer lower rates than floating options historically in New Zealand, but they come with break fee risk and limited ability to make large extra repayments. Floating loans move with market conditions, which can work in your favour when rates are falling but creates uncertainty in rising markets. Floating loans do allow unlimited extra repayments, which can significantly reduce your loan term.

Key considerations when choosing between fixed and floating:

- How long do you plan to stay in the property?

- Do you want the ability to make large lump sum payments?

- How would a sudden repayment increase affect your budget?

- What is your view on the likely direction of NZ interest rates?

A practical solution many Kiwi borrowers use is splitting their mortgage into portions, each on a different fixed term. For example, you might fix $300,000 on a one-year term and $200,000 on a two-year term. This staggered fixed terms approach is sometimes called a mortgage ladder. When the first portion rolls over, you are not exposed to refixing your entire balance at once. You have staggered your exposure and retained some flexibility.

The current NZ rate environment in 2026 adds another layer. With the Reserve Bank having moved through a significant rate cycle, borrowers who understand fixed mortgage terms can position themselves more deliberately. Shorter fixed terms make sense when you expect rates to fall further. Longer terms provide peace of mind if you believe rates have bottomed out.

Practical strategies for managing your rate rollovers

The most valuable advantage you can give yourself as a NZ borrower is not guessing where rates are headed. It is being prepared when your rollover moment arrives.

- Set your reminders early. Proactive refixing starts with knowing your expiry date. Put a reminder in your calendar for 60 days before and another for 30 days before.

- Compare lender offers, not just your bank’s. Your current lender has an incentive to retain your business, but not necessarily to offer you their most competitive rate without prompting. Shopping around creates leverage.

- Consider staggered terms. If your loan is large enough, splitting it across two fixed periods with different maturity dates reduces the stress of refixing everything at once and spreads rollover risk across different market conditions.

- Model the numbers before breaking. If you are considering breaking a fixed term early, do the maths properly. Get the break fee in writing, calculate your interest saving over the new term, and see how long it takes to break even.

- Keep a rate watch habit. You do not need to obsess over daily movements, but checking in on the direction of fixed rates every few months keeps you informed without consuming your time.

Pro Tip: Borrowers rolling into a lower fixed rate sometimes keep their repayments at the old, higher amount. This quietly reduces your principal faster and can cut loan duration significantly without requiring any discipline because the repayment is already built into your budget.

My take on the cycle most borrowers underestimate

I have worked with a lot of Kiwi homebuyers over the years, and the pattern I see most consistently is this: people are highly engaged at purchase, less engaged at their first refix, and almost passive by the third or fourth rollover. That progressive disengagement is exactly when the costly mistakes happen.

What I have found is that borrowers who treat each rollover as a fresh decision point tend to do significantly better than those who just accept whatever their bank sends them in the mail. The reality is that each refix cycle is a genuine opportunity. A one-year fixed term on a $500,000 loan means you are making this decision roughly 25 times over your mortgage’s life. Even small improvements at each rollover compound meaningfully over time.

My honest advice is to stop thinking of your fixed rate as a set-and-forget arrangement. It is a recurring decision with real financial consequences. The borrowers who come to me having missed rollover windows and defaulted onto floating rates are not careless people. They are busy people who did not build a system for monitoring their mortgage. Build the system. Set the reminders. And do not refix in isolation when a second set of eyes on the numbers costs you nothing.

— Stuart

Let Mortgagemanagers handle your next refix

Knowing what fixed rate periods are is one thing. Getting the best possible outcome at every rollover is another. Mortgagemanagers works as your personal mortgage shoppers, comparing fixed rate options across multiple lenders, negotiating on your behalf, and helping you time your refix to avoid costly default floating rates. Whether you are approaching your first rollover or your fifth, having expert guidance in your corner reduces risk and saves real money.

If your fixed term is coming up in the next few months, or if you are unsure when your current term ends, get in touch with the team at Mortgagemanagers early. The best refix outcomes go to borrowers who prepare, and preparation starts with a conversation.

FAQ

What is a fixed rate period on a NZ home loan?

A fixed rate period is a set term during which your home loan interest rate stays the same, protecting you from market movements. NZ terms typically range from 6 months to 5 years.

What happens if I do nothing when my fixed term ends?

Your lender will usually roll your loan onto its standard floating rate, which can be 1.5 to 2.5 percentage points higher than current fixed rates. On a $500,000 loan, this can cost more than $8,000 in extra interest annually.

How are break fees calculated in New Zealand?

Break fees are based on the rate differential between your contracted fixed rate and current wholesale swap rates, multiplied by your remaining balance and time left on your term. Always request a written estimate from your lender before making any decision to break.

Is it better to fix for a shorter or longer term in 2026?

It depends on your financial goals and the rate environment. Shorter terms offer more flexibility to refix at potentially lower rates, while longer terms provide repayment certainty. A split loan across different terms is a common middle ground for NZ borrowers.

Can a mortgage adviser help with fixed rate decisions?

Yes. Mortgage advisers compare rates across multiple lenders, help you time rollovers, and model break fee scenarios so you can make informed decisions at every stage of your mortgage.