TL;DR:

- Preparing complete documents early can significantly speed up your mortgage approval process in New Zealand. Using the Kāinga Ora First Home Loan scheme through participating lenders allows eligible buyers to purchase with minimal deposits and no mortgage insurance. Staying organized, prompt in responding to lenders, and leveraging digital tools ensure a smooth, efficient home loan experience.

An easy mortgage application is a well-prepared one: gather your documents early, understand what lenders need, and use government-backed support like the Kāinga Ora First Home Loan to reduce complexity from the start. For first home buyers in New Zealand, the home loan process can feel like a maze of paperwork and waiting. It does not have to be. With the right preparation and a clear understanding of how participating lenders, KiwiSaver withdrawals, and digital application tools work together, you can move from enquiry to pre-approval with confidence and far less stress than you might expect.

What you need to prepare before you apply for a mortgage

The single biggest factor in a quick mortgage approval is document readiness. Lenders evaluate income, employment stability, credit score, debt-to-income ratio, and assets when approving home loans, and any gap in your paperwork triggers delays. Think of your application as a job interview: showing up prepared tells the lender you are a serious, low-risk borrower.

The Consumer Financial Protection Bureau recommends assembling a paperwork packet before you even start shopping for homes. This approach maps directly onto New Zealand mortgage protocols and gives you a real head start. When your documents are ready before you need them, the process shifts from reactive to proactive.

Here is what your packet should include:

- Valid photo ID: Passport or New Zealand driver’s licence for all applicants

- Proof of income: Three months of recent payslips, plus your two most recent tax returns if you are self-employed

- Bank statements: Three to six months of statements showing regular savings and spending patterns

- KiwiSaver documentation: Confirmation of your balance and a withdrawal application if you plan to use KiwiSaver as part of your deposit

- Existing debt details: Current balances and repayment schedules for any personal loans, car finance, or credit cards

- Employment confirmation: A signed letter from your employer confirming your role, salary, and length of service

KiwiSaver withdrawal timing deserves special attention. Plan your withdrawal at least 10 to 15 working days before your settlement date to avoid last-minute coordination issues with your lender. Missing this window is one of the most common and easily avoidable delays first home buyers face.

Your credit profile matters just as much as your paperwork. Check your credit report through Centrix or Equifax New Zealand before you apply, and address any errors or outstanding defaults. A strong credit profile reduces underwriting scrutiny and can cut approval time from the typical 30 to 45 days down to as little as 21 days in some cases.

Pro Tip: Set up a dedicated folder on your computer or in Google Drive labelled “Home Loan Documents.” As you gather each item, drop it in. When your adviser or lender asks for something, you can share it in seconds rather than hunting through emails.

How does the Kāinga Ora First Home Loan work?

The Kāinga Ora First Home Loan is a government-backed scheme that allows eligible buyers to purchase a home with as little as a 5% deposit, without paying lender mortgage insurance. This is a significant financial advantage. Lender mortgage insurance can add thousands of dollars to your upfront costs, so removing it from the equation makes the simple mortgage process considerably more affordable.

Eligibility is based on three main criteria:

| Criteria | Requirement |

|---|---|

| Income cap (single buyer) | Up to $95,000 gross per year |

| Income cap (two or more buyers) | Up to $150,000 gross combined |

| Minimum deposit | 5% of the purchase price |

| Property price cap (Auckland) | $875,000 |

| Property price cap (other regions) | Varies by location |

You do not apply to Kāinga Ora directly. Instead, you apply through a participating lender, who submits the guarantee application on your behalf. This is the detail that surprises most first home buyers. The lender handles the bureaucratic coordination internally, which means your job is simply to submit complete, accurate documentation to them.

Pre-approval under this scheme typically takes 3 to 7 business days once your documentation is complete, and the pre-approval is valid for 60 to 90 days. That window gives you a realistic timeframe to find a property and make an offer without the pressure of an expiring approval hanging over you.

Pro Tip: Ask your mortgage adviser to confirm which lenders on their panel are Kāinga Ora-approved before you commit to a lender. Not all banks and non-bank lenders participate in the scheme, and choosing a non-participating lender means starting the process again.

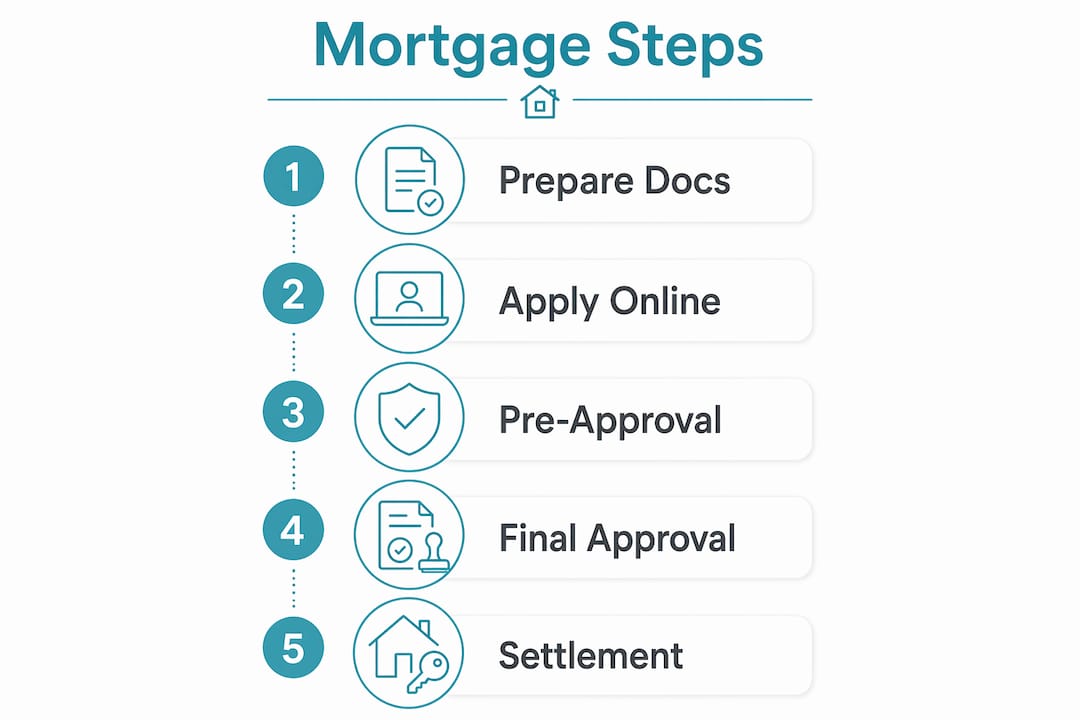

Step-by-step: how to submit your application and avoid delays

A fast mortgage application follows a clear sequence. Skipping steps or submitting incomplete information is the primary cause of drawn-out approvals. Follow this order and you give yourself the best chance of a smooth, no-hassle mortgage experience.

- Get pre-approval first. Pre-approval before house hunting strengthens your buying position and tells you exactly how much you can borrow. Sellers and real estate agents take pre-approved buyers more seriously.

- Submit your full document packet. Use your lender’s secure online portal or provide physical copies if preferred. Incomplete submissions are the number one cause of processing delays.

- Respond to lender requests within 24 hours. Lenders often need clarification on specific transactions or additional payslips. A slow response from you pauses the clock on your approval.

- Avoid new credit activity. Do not apply for new credit cards, take out personal loans, or make large purchases while your application is being assessed. New credit lines during applications trigger re-checks that slow approval and can change your debt-to-income ratio.

- Do not change jobs. Employment stability is a core lender requirement. A job change mid-application can require a full reassessment of your income.

- Confirm your KiwiSaver withdrawal timeline. If you are using KiwiSaver funds, make sure your withdrawal request is lodged well ahead of your settlement date.

Treat pre-approval as a milestone that reflects document completeness and lender confidence, not an inevitable waiting period. Timely, complete submissions directly determine how fast you move through the process.

The digital application tools offered by major lenders in 2026, including e-signatures, document uploads, and digital bank verification, mean you rarely need to visit a branch in person. This makes the easy home loan process genuinely accessible from your kitchen table.

What online tools make your mortgage application faster?

Digital tools have transformed the online mortgage application experience for New Zealand buyers. You no longer need to print, sign, and courier documents to a bank branch. Most major lenders now offer secure portals where you upload, sign, and track your application in real time.

Here is how to use these tools to your advantage:

- Borrowing power calculators: Use your lender’s or adviser’s online calculator before you apply. Tools like the Mortgagemanagers borrowing calculator give you a realistic figure based on your income, expenses, and deposit, so you are not guessing when you start the formal process.

- Secure document upload portals: Most NZ banks and non-bank lenders accept PDF uploads of payslips, bank statements, and ID. Label your files clearly (e.g., “Payslip_March2026”) to speed up verification.

- Automated credit checks: Many lenders run automated credit assessments as part of the digital application process, which reduces the back-and-forth of manual underwriting.

- E-signature platforms: DocuSign and Adobe Sign are widely accepted for signing loan documents, removing the need for in-person appointments.

- Pre-approval apps: Some lenders offer mobile app-based pre-approval that can return a conditional decision within hours of submission, provided your documents are complete.

For a structured overview of what to prepare at each stage, the mortgage application checklist from Mortgagemanagers walks you through every document and step in the New Zealand context. Pairing that with your lender’s digital portal creates a genuinely fast mortgage application experience.

The key insight here is that technology speeds up the process only when your documents are ready. A digital portal cannot compensate for missing payslips or an unsigned employment letter. Preparation and technology work together, not independently.

Key takeaways

An easy mortgage application in New Zealand requires complete documentation, strategic use of the Kāinga Ora First Home Loan scheme, and consistent responsiveness throughout the lender’s assessment process.

| Point | Details |

|---|---|

| Prepare documents early | Gather ID, payslips, bank statements, and KiwiSaver paperwork before you start house hunting. |

| Use Kāinga Ora strategically | Apply through a participating lender who manages the guarantee process on your behalf. |

| Get pre-approval first | Pre-approval takes 3 to 7 business days and is valid for 60 to 90 days, giving you a clear buying window. |

| Avoid financial changes mid-application | New credit, large purchases, or job changes during assessment can delay or derail your approval. |

| Leverage digital tools | Secure portals, e-signatures, and automated credit checks reduce paperwork delays significantly. |

What I have learned helping first home buyers get approved

Working with first home buyers across Auckland and the wider New Zealand market, the pattern I see most often is this: the buyers who find the process stressful are almost always the ones who started without a complete picture of what lenders actually need. They gather documents reactively, one request at a time, and each gap adds days to the timeline.

The buyers who sail through are not necessarily in a stronger financial position. They are simply more organised. They arrive with a complete packet, they respond to lender queries the same day, and they have already spoken to a mortgage adviser who has told them exactly what to expect. That preparation is the real difference between a drawn-out ordeal and a smooth, confident experience.

My honest advice: do not wait until you find a property you love to start your application. By then, you are already behind. Start the home loan preparation process three to six months before you plan to buy. Use that time to build your savings record, check your credit report, and get your KiwiSaver balance confirmed. When the right property comes along, you will be ready to move quickly.

The Kāinga Ora First Home Loan is genuinely one of the most underutilised tools available to eligible New Zealand buyers. Many first home buyers assume the government scheme adds complexity. It does the opposite. Your lender handles the guarantee application. You just need to meet the eligibility criteria and submit complete paperwork. That is it.

— Stuart

Ready to make your mortgage application simple?

Getting your first home loan does not have to feel overwhelming. At Mortgagemanagers, our advisers act as your personal shoppers for a home loan, comparing lenders, handling paperwork, and guiding you through the Kāinga Ora First Home Loan process from start to finish. Based in Hobsonville and servicing buyers across Auckland, the North Shore, West Auckland, and remotely throughout New Zealand, we know the local lending market inside out.

Whether you are just starting to think about buying or you are ready to apply today, our team is here to make the process clear, fast, and as stress-free as possible. Reach out to Mortgagemanagers and take the first step toward your new home with a team that genuinely knows how to get first home buyers across the line.

FAQ

What documents do I need for a mortgage application in NZ?

You need valid photo ID, three months of payslips, three to six months of bank statements, KiwiSaver documentation, and details of any existing debts. The Consumer Financial Protection Bureau recommends assembling these documents before you start shopping for homes.

How long does mortgage pre-approval take in New Zealand?

Pre-approval typically takes 3 to 7 business days once your documentation is complete. Under the Kāinga Ora First Home Loan scheme, pre-approval is valid for 60 to 90 days, giving you a clear window to find a property.

Can I apply for a mortgage online in New Zealand?

Yes. Most major NZ lenders offer secure online portals for document uploads, e-signatures, and application tracking. Digital bank verification and automated credit checks mean many buyers complete the entire process without visiting a branch.

What is the minimum deposit for a Kāinga Ora First Home Loan?

The minimum deposit is 5% of the purchase price. The scheme removes the need for lender mortgage insurance, which makes it a cost-effective option for eligible first home buyers with smaller deposits.

What slows down a mortgage application?

Incomplete documentation, new credit activity during the assessment period, and slow responses to lender queries are the most common causes of delays. Maintaining financial stability and responding promptly to lender requests keeps your application moving forward.