TL;DR:

- Mortgage rates in New Zealand are influenced by the OCR, swap rates, and individual borrower profiles.

- Understanding these factors helps borrowers negotiate better rates and choose suitable mortgage structures.

Mortgage rates are the interest percentages lenders charge on home loans, and they determine how much you pay on top of the amount you borrow. In New Zealand, understanding what are mortgage rates means understanding the difference between paying $500,000 for a home and paying well over $800,000 by the time your loan is repaid. The Reserve Bank of New Zealand (RBNZ) sets the Official Cash Rate (OCR), which is the single biggest driver of where rates sit at any given time. Whether you are buying your first home in Auckland or refinancing an existing loan, knowing how rates work puts you in a far stronger position at the negotiating table.

What factors affect mortgage rates in New Zealand?

Mortgage rates in New Zealand are shaped by a mix of national policy, global financial markets, and your own financial profile. No single factor controls the number you see on a bank’s website.

The RBNZ’s OCR is the most direct lever. The OCR is reviewed eight times yearly and reflects the cost banks pay for overnight funds. When the OCR rises, banks pay more to borrow money, and they pass that cost on to you. When it falls, floating rates tend to follow within weeks.

Fixed mortgage rates work differently. They are priced off wholesale swap rates, which are market instruments that reflect where traders expect the OCR to be in the future. This is why fixed rates can fall before the RBNZ officially cuts the OCR. The market prices the expectation, not the announcement.

Beyond the OCR and swap rates, your own profile matters significantly. Lenders assess:

- Loan-to-value ratio (LVR): A lower deposit means higher risk for the bank, which often means a higher rate.

- Credit history: A clean repayment record signals reliability and can unlock better pricing.

- Income stability: Salaried borrowers typically receive more favourable terms than self-employed applicants.

- Loan size: Larger loans can sometimes attract better rates because the bank earns more in absolute dollar terms.

Bank funding costs and profit margins also play a role. Banks source money from depositors, wholesale markets, and overseas lenders. When those costs rise, mortgage rates follow. Understanding key factors affecting mortgage rates helps you see why two borrowers can receive different rates from the same bank on the same day.

Pro Tip: Do not wait for an OCR announcement to act on a fixed rate. Swap rates price expected changes weeks or months earlier, so the best fixed rate may already be gone by the time the RBNZ makes its move.

What are the types of mortgage rates and how do they differ?

New Zealand borrowers choose from three main rate structures: fixed, floating, and split. Each suits a different financial situation, and choosing the wrong one can cost you thousands.

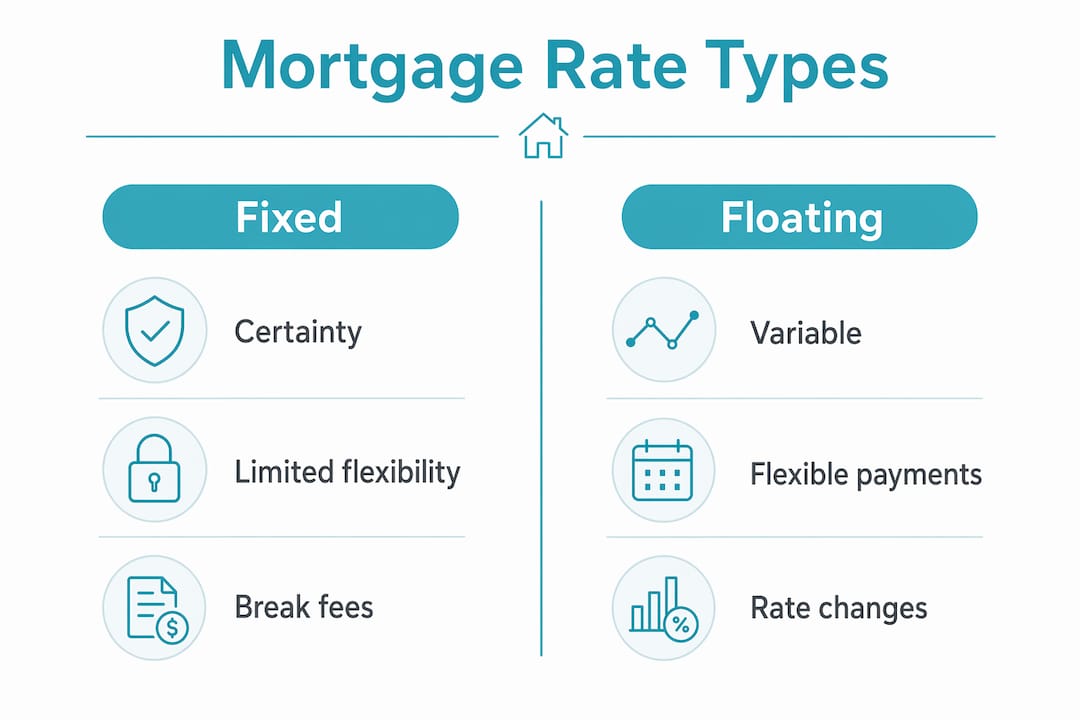

Fixed rates

A fixed mortgage rate locks your interest rate for a set term, typically 6 months to 5 years. Your repayments stay the same for the entire term, which makes budgeting straightforward. The trade-off is that fixed loans limit extra repayments to $5,000–$10,000 per year, and breaking the loan early triggers a break fee that can run into thousands of dollars. Fixed rates suit borrowers who value certainty and plan to stay in their home for the foreseeable future.

Floating rates

A floating rate (also called a variable rate) moves with market conditions, particularly the OCR. You can make unlimited extra repayments and exit the loan without a break fee. The cost of that flexibility is real: floating rates currently sit around 6.99%–7.09%, compared to mid-4% to mid-5% for competitive fixed terms. That gap of 1%–2% adds up quickly on a large loan. Floating rates suit borrowers who expect to sell, refinance, or make large lump-sum repayments in the near term.

Split loans

Split loans combine fixed and floating portions and are the most common mortgage structure in New Zealand. You fix the bulk of your loan for rate certainty, while keeping a smaller portion floating for flexibility. This structure reduces your exposure to rate rises while still allowing extra repayments on the floating portion. For borrowers considering property upgrades or extensions, a knock down rebuild can also affect how you structure your loan, since construction finance often requires a floating or revolving component during the build phase.

| Rate type | Certainty | Flexibility | Break fees | Best for |

|---|---|---|---|---|

| Fixed | High | Low | Yes | Stable budgeters |

| Floating | Low | High | No | Short-term holders |

| Split | Medium | Medium | Partial | Most borrowers |

Pro Tip: If you are unsure which structure suits you, start with a split loan. It gives you the safety of a fixed rate on most of your debt while keeping a floating portion available for lump-sum payments.

How do current mortgage rate trends affect borrowing in 2026?

The rate environment in 2026 is meaningfully better for borrowers than it was two years ago, but it still rewards careful decision-making. As of april 2026, major New Zealand banks offer short-term fixed rates ranging from approximately 4.49% to 6.20%, while floating rates sit between 6.99% and 7.09%.

The difference between a 5.5% and a 6.5% rate on a $700,000 loan is approximately $130 per month, or $46,800 over a 30-year term. That is not a rounding error. It is a car, a renovation, or years of retirement savings.

Recent OCR cuts have pulled floating rates down from their 2023 peaks, but floating still carries a significant premium over the best fixed terms. Borrowers who locked into longer fixed terms at peak rates in 2022 and 2023 are now rolling off those terms and finding a much more competitive market waiting for them.

What should you watch for in the current environment?

- Short-term fixed rates (6 months to 2 years) are currently the most competitive, reflecting market expectations of further OCR movement.

- Longer fixed terms (3–5 years) offer less certainty about whether you are locking in at a good level, since swap markets are harder to predict over longer horizons.

- Floating rates remain expensive relative to fixed options and are best used tactically, not as a default.

- Rollover timing is critical. At fixed term expiry, your loan rolls onto a higher default floating rate if you do not act. That rollover moment is your best opportunity to negotiate.

The risk of waiting for rates to fall further is real. Market swap rates reflect expected future OCR changes and are already priced into fixed mortgage rates. Borrowers who wait for official cuts often find the fixed rates have already moved before the announcement.

How can borrowers find and negotiate better mortgage rates?

Getting a better rate is not luck. It is preparation, timing, and knowing where to look. Here is a practical approach:

- Check carded rates, then go further. Advertised rates are a starting point, not the final offer. Broker discounts of 0.25%–0.75% are often available through mortgage advisers, depending on your LVR and credit profile. These discounts are not publicly listed.

- Use a mortgage adviser. Advisers have direct relationships with multiple lenders and access to rates that are not available to the general public. They negotiate on your behalf and know which lenders are most competitive for your specific situation.

- Act at rollover. The end of a fixed term is your strongest negotiating position. Banks prefer to retain borrowers rather than lose them to a competitor, which means they will often sharpen their offer if you signal you are shopping around.

- Improve your LVR before applying. If your deposit is close to a key LVR threshold (typically 20%), paying down a little more before applying can move you into a lower-risk bracket and unlock a better rate.

- Consider a split structure. Splitting your loan across two or more fixed terms reduces the risk of locking everything in at the wrong moment. If one term proves too high, the other portion rolls over sooner and can be renegotiated.

For borrowers thinking about property investment or dual occupancy, understanding dual occupancy home benefits can also inform how you structure your borrowing, since rental income from a second dwelling affects your serviceability assessment.

Pro Tip: Ask your adviser specifically about broker rates versus carded rates. The difference is rarely advertised, but it is almost always available. A good adviser will show you both numbers side by side.

For more practical guidance, the Mortgagemanagers resource on how to get a better rate walks through the negotiation process in plain language.

Key takeaways

Understanding mortgage rates in New Zealand means knowing that the OCR, swap rates, your LVR, and your timing at rollover are the four levers that most directly determine what you pay.

| Point | Details |

|---|---|

| OCR drives floating rates | The RBNZ reviews the OCR eight times yearly; floating rates move with it directly. |

| Swap rates drive fixed rates | Fixed rates price expected future OCR changes, often before official announcements. |

| Rate type choice matters | Floating rates sit 1%–2% above the best fixed terms; choose based on your timeline. |

| Rollover is your best opportunity | Act at fixed term expiry to negotiate; defaulting to floating costs you significantly. |

| Broker rates beat carded rates | Advisers access discounts of 0.25%–0.75% not available to the public. |

My honest view on timing the mortgage market

After working with borrowers across Auckland and wider New Zealand, the single most common mistake I see is waiting. Borrowers watch the news, track OCR announcements, and hold off fixing their rate because they believe rates will drop further next month. Sometimes they are right. More often, they are not.

The reason is simple. Fixed mortgage rates are priced off wholesale swap rates, not the OCR itself. By the time the RBNZ cuts, the swap market has already moved. The fixed rate you could have locked in three months ago may be higher than what is available today, but the one you are waiting for next quarter may already be priced in right now. Waiting for certainty in a market that prices expectations is a losing strategy.

What I tell every borrower is this: focus on what you can control. Your LVR, your credit profile, your timing at rollover, and your choice of adviser all have a direct impact on the rate you receive. The OCR is outside your control. Your preparation is not.

The borrowers who consistently get the best outcomes are the ones who act at rollover, use an adviser to access broker rates, and structure their loan thoughtfully rather than defaulting to whatever the bank offers. That is not sophisticated financial strategy. It is just paying attention at the right moment.

— Stuart

Mortgagemanagers can help you find the right rate

Knowing the theory is one thing. Getting the best rate for your specific situation is another. Mortgagemanagers is a locally owned Auckland-based team of mortgage advisers who work across West Auckland, the North Shore, Hobsonville, and remotely throughout New Zealand.

The team accesses broker rates that are not publicly advertised, negotiates directly with multiple lenders on your behalf, and helps you structure your loan to suit your goals, whether you are buying your first home, refinancing, or rolling off a fixed term. A free initial consultation costs you nothing and could save you tens of thousands over the life of your loan. Reach out to the Mortgagemanagers team today and get a clear picture of what rates are genuinely available to you.

FAQ

What are mortgage rates and how are they calculated?

Mortgage rates are the interest percentages lenders charge on home loans. In New Zealand, they are calculated based on the OCR, wholesale swap rates, bank funding costs, and your individual credit and LVR profile.

What is the difference between fixed and floating mortgage rates?

Fixed rates lock your repayments for a set term (6 months to 5 years) with limited extra repayment options. Floating rates move with market conditions, allow unlimited extra repayments, and carry no break fees, but currently sit 1%–2% above the best fixed rates.

How often do mortgage rates change in New Zealand?

Floating rates can change at any time but typically move after RBNZ OCR decisions, which are made eight times per year. Fixed rates change more frequently, as they respond to daily movements in wholesale swap markets.

Can I negotiate my mortgage rate with a bank?

Yes. Banks regularly offer rates below their advertised carded rates, particularly at fixed term rollover. Mortgage advisers access broker discounts of 0.25%–0.75% that are not publicly listed, making negotiation through an adviser the most effective approach.

When is the best time to lock in a fixed mortgage rate?

The best time is before an expected OCR cut, not after. Swap markets price anticipated cuts into fixed rates early, so waiting for an official announcement often means the opportunity has already passed.