TL;DR:

- Mortgage statements in New Zealand are online transaction histories that detail your loan balance, repayment history, and interest charges. Understanding the principal and interest split reveals how your payments reduce debt over time, especially early in a fixed repayment schedule. Regular reviews help track progress, confirm rate changes, and assist with tax calculations for rental property income.

A mortgage statement is a detailed record of your home loan’s current status, showing your outstanding balance, payment history, interest charges, and any fees applied to your account. Most New Zealand homeowners access their mortgage statement example through their bank’s online portal rather than receiving a paper document in the post. NZ mortgage statements function as a live transaction ledger rather than a standardised monthly summary. Understanding what each line means puts you firmly in control of one of the largest financial commitments of your life. New Zealand home loans typically run for 25–30 years, so reading your statement correctly from day one matters enormously.

What does a mortgage statement example include?

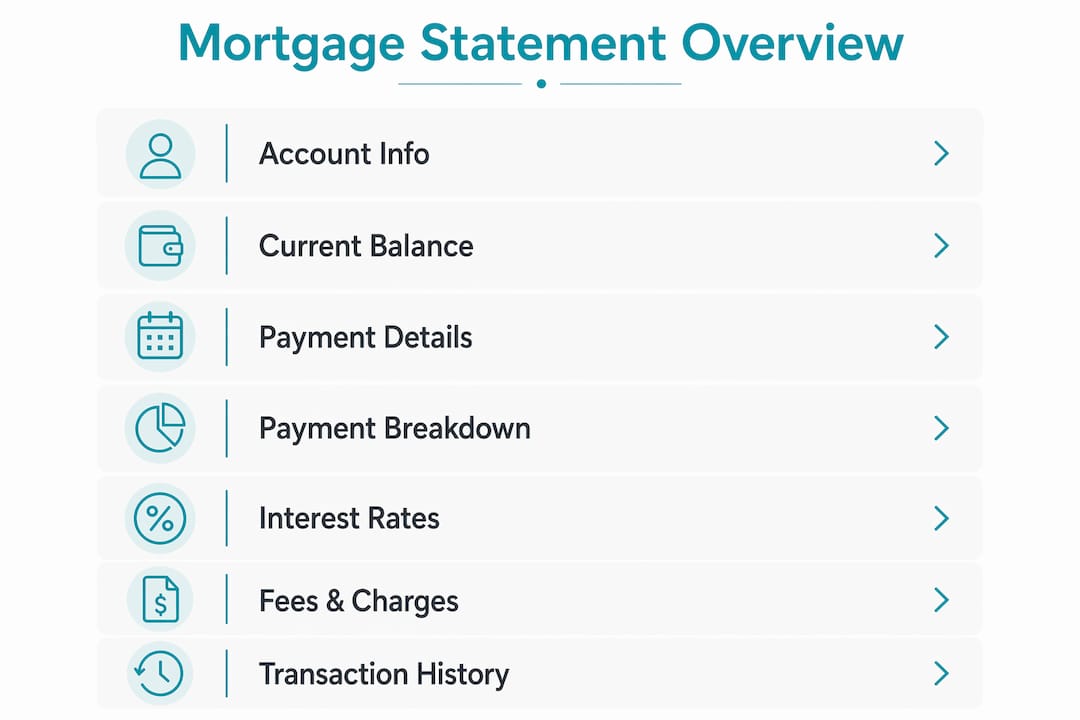

A typical New Zealand mortgage statement covers several distinct categories of information. Knowing where each figure comes from helps you spot errors, track progress, and plan ahead.

Account and borrower details

Every statement opens with your loan account number, the names of all borrowers on the loan, the property address, and the loan start date. These details confirm you are looking at the right account, which is especially relevant if you hold multiple loans or have split your mortgage across fixed and floating portions.

Current balance and principal outstanding

The current loan balance is the total amount you still owe the lender. This figure decreases with every repayment you make, though in the early years of a table loan the reduction is slow. Your principal outstanding is the same figure expressed specifically as the debt component, excluding any accrued interest not yet charged.

Payment details

This section shows your minimum repayment amount, the due date, and the frequency (weekly, fortnightly, or monthly). It also records whether you are ahead of schedule, on track, or in arrears. To understand how your repayment is calculated, the mortgage repayment structure guide from Mortgagemanagers explains the mechanics clearly.

Breakdown of each payment

Each repayment splits into two parts: the portion that reduces your principal and the portion that covers interest. In the early years of a 30-year loan, the interest portion dominates. A $700,000 loan at 6.00% over 30 years produces a monthly repayment of approximately $4,199, with total interest paid over the life of the loan reaching around $811,640. That figure illustrates why tracking the principal-versus-interest split on your statement is so valuable.

Interest rate information

Your statement will show the interest rate applied to each portion of your loan. If you have split your mortgage between a fixed rate and a floating rate, each portion appears separately with its own rate and expiry date. This section is where you confirm whether a rate rollover has occurred and whether the new rate matches what your lender quoted.

Fees, charges, and arrears

Any administration fees, break fees, or penalty charges appear as separate line items. If your account is in arrears, the overdue amount shows clearly alongside the date it became overdue. Catching these early prevents small issues from compounding.

Transaction history and year-to-date totals

The transaction history lists every debit and credit on your loan account in date order. The year-to-date section summarises total interest paid since 1 january, which is particularly useful for rental property investors. As of the 2025–26 tax year, rental property investors can deduct 100% of mortgage interest expenses, making this figure directly relevant to their tax returns.

| Statement component | What it tells you |

|---|---|

| Current loan balance | Total amount still owed to the lender |

| Principal vs. interest split | How much of each payment reduces debt vs. covers interest cost |

| Interest rate and type | Fixed or floating rate applied, with expiry date if fixed |

| Fees and charges | Any administration, break, or penalty costs charged |

| Year-to-date interest paid | Total interest charged since 1 january, useful for tax purposes |

How do you interpret the principal and interest sections?

The principal and interest split is the most misunderstood part of any sample mortgage statement. Getting clear on how it works changes the way you think about your loan progress.

How a table loan works

New Zealand table loans use a fixed repayment amount throughout the loan term. What changes over time is the composition of that payment. In the early years, most of your repayment covers interest. As the years pass, the interest portion shrinks and the principal portion grows. This is not a flaw in the system. It is simply how compound interest mathematics works on a declining balance.

Why early statements surprise new homeowners

Many first-time buyers open their first statement expecting to see a significant dent in their loan balance. The reality is different. On a $700,000 loan at 6.00%, the first monthly repayment of $4,199 might direct only around $699 toward principal, with the remaining $3,500 covering interest. That proportion shifts gradually over the following years. Seeing this on your statement is not a cause for alarm. It is a prompt to consider whether making extra repayments early could reduce your total interest cost significantly.

Here is a practical way to read the principal and interest sections on your statement:

- Locate the “payment breakdown” or “transaction detail” section of your statement.

- Identify the interest charge applied on your repayment date.

- Subtract the interest charge from your total repayment to find the principal reduction.

- Compare this month’s principal reduction to the same month last year to confirm the balance is shifting in your favour.

- Check the repayment options guide from Mortgagemanagers to see whether switching repayment frequency could accelerate your principal paydown.

Pro Tip: If you switch from monthly to fortnightly repayments, you make the equivalent of one extra monthly payment per year. Over a 30-year loan, this can cut years off your term and save tens of thousands of dollars in interest.

Understanding fixed vs floating rates is also critical here. A fixed rate locks your interest charge for a set period, making the interest portion of each payment predictable. A floating rate moves with the market, so your interest charge can rise or fall between statements.

How do mortgage statements connect to loan applications and financial planning?

Mortgage statements serve two distinct purposes. They are a record of your loan history, and they are a financial planning tool you can use right now.

What lenders look for in your statements

When you apply for a new mortgage or refinance an existing one, lenders request recent bank statements to assess your financial behaviour. NZ lenders review up to three months of transaction history, looking for consistent savings patterns, stable income, and the absence of unexplained large withdrawals. Your existing mortgage statement also confirms your current repayment history, which signals to a new lender whether you are a reliable borrower. The mortgage application checklist from Mortgagemanagers outlines exactly which documents you need to prepare.

Pre-approval and statement currency

Mortgage pre-approval in New Zealand is valid for 60–90 days. During that window, your financial position must remain consistent with what the lender assessed. If your statements show new debt, reduced income, or unusual spending in that period, the lender can withdraw the pre-approval before settlement. Keeping your statements clean during the pre-approval window is not optional.

Pro Tip: Avoid applying for new credit cards, car loans, or buy-now-pay-later accounts during your pre-approval period. These show up on your bank statements and can trigger a reassessment of your borrowing capacity.

Using statements for ongoing budgeting

Your mortgage statement is a financial GPS for your home loan. The year-to-date interest figure tells you exactly how much your loan has cost you this year. The current balance tells you your net equity position when combined with your property’s current value. Reviewing your statement quarterly, rather than only when something goes wrong, builds the financial discipline that lenders reward when you next need to borrow.

- Check your interest rate expiry date at least 60 days before it rolls over.

- Compare your current balance against your original amortisation schedule to confirm you are on track.

- Note any fees charged and query anything you do not recognise.

- Use the year-to-date interest figure for tax planning if you hold a rental property.

What do the terms on a mortgage statement mean?

Reading a mortgage statement template for the first time can feel like decoding a foreign language. These definitions cover the terms that appear most often.

- Principal: The original amount borrowed, or the portion of it still outstanding. Every repayment that reduces this figure builds your equity.

- Interest: The cost the lender charges for providing the loan. It is calculated daily on your outstanding balance and charged at each repayment date.

- Fixed rate: An interest rate locked for a set term, typically six months to five years in New Zealand. Your interest charge stays the same regardless of market movements during that period.

- Floating rate: An interest rate that moves with the lender’s standard variable rate. Your interest charge can change between statements.

- Arrears: Any repayment amount that is overdue. Arrears attract additional interest and can affect your credit record if left unresolved.

- Break fee: A charge applied when you exit a fixed-rate loan before the fixed term ends. The amount varies based on market interest rates at the time.

- Transaction code: A short reference code identifying the type of transaction, such as a regular repayment, a lump-sum payment, or a fee debit. Your lender’s website or app typically provides a key to these codes.

- Redraw balance: If your loan has a redraw facility, this figure shows how much of your extra repayments you can access. It does not appear on all statements.

If you ever spot a charge or transaction code you cannot identify, contact your lender in writing and request a full explanation. Borrowers have the right to a clear account of every charge applied to their loan.

Key takeaways

A mortgage statement is your most direct window into the true cost and progress of your home loan, and reading it correctly is the single most practical financial skill a New Zealand homeowner can develop.

| Point | Details |

|---|---|

| Statement format in NZ | Most NZ mortgage statements are online transaction histories, not standardised paper documents. |

| Table loan composition | Fixed repayments shift from mostly interest to mostly principal over the loan term. |

| Tax relevance | Rental investors can deduct 100% of mortgage interest from the 2025–26 tax year onward. |

| Pre-approval window | Mortgage pre-approval lasts 60–90 days; keep statements clean during this period. |

| Regular review habit | Checking your statement quarterly helps you catch errors, plan rate rollovers, and track equity growth. |

What I have learned from years of reading mortgage statements with clients

Most first-time buyers in New Zealand come to me with the same misconception: they assume their mortgage statement will show steady, visible progress from the very first month. When they see that the vast majority of their initial repayments cover interest rather than reducing the loan, the reaction ranges from surprise to genuine concern. My job is to reframe that moment.

The interest-heavy early years are not a sign that the loan is working against you. They are the mathematical reality of borrowing a large sum at compound interest. What matters is that you understand the trajectory. The principal reduction accelerates every single year. By year 15 of a 30-year loan, the split looks very different from year one.

The other thing I see regularly is homeowners who have never once opened their mortgage statement since settlement. They make their repayments faithfully but have no idea whether their rate has rolled over to a higher floating rate, whether fees have been applied, or whether they are ahead of or behind their original schedule. That is a costly form of financial passivity. A 15-minute quarterly review of your statement is one of the highest-return habits you can build as a homeowner.

I also want to address the tax point directly for investors. The return of full mortgage interest deductibility for rental properties from the 2025–26 tax year is significant. Your year-to-date interest figure on your statement is the number your accountant needs. Keep it accessible.

— Stuart

How Mortgagemanagers helps you make sense of your home loan

Reading a mortgage statement is one thing. Knowing what to do with the information is another. Mortgagemanagers is a locally owned Auckland mortgage advisory business that helps homeowners and buyers across New Zealand interpret their loan documents, choose the right loan structure, and make confident decisions at every stage of their mortgage.

Whether you are reviewing a statement for the first time, approaching a fixed-rate rollover, or preparing documents for a new application, the team at Mortgagemanagers provides clear, personalised guidance. As expert mortgage advisers, they work across multiple lenders to find the structure that suits your situation, not just the one your bank prefers. Reach out to Mortgagemanagers to talk through your statement and your options with an adviser who knows the New Zealand market.

FAQ

What is a mortgage statement in New Zealand?

A mortgage statement is a record of your home loan account showing your current balance, repayment history, interest charges, and any fees. In New Zealand, most lenders provide this as an online transaction history rather than a paper document.

How do I read the principal and interest split on my statement?

Locate the payment breakdown in your transaction history and subtract the interest charge from your total repayment. The remainder is the amount that reduced your principal. In the early years of a table loan, the interest portion is significantly larger.

How often should I review my mortgage statement?

A quarterly review is the minimum recommended practice. Check your interest rate expiry date, confirm no unexpected fees have been charged, and compare your current balance against your original repayment schedule.

Can my mortgage statement help with my tax return?

Yes, if you own a rental property. Your year-to-date interest figure shows the total mortgage interest charged for the financial year. From the 2025–26 tax year, residential rental investors in New Zealand can deduct 100% of this amount.

What should I do if I find an error on my mortgage statement?

Contact your lender in writing as soon as you identify the error. Provide the specific transaction date, amount, and the reason you believe it is incorrect. Lenders are required to investigate and respond to disputed charges.