Like any investment it is important to take some time and review how your Kiwisaver is performing for you, and that includes how it is set up and how it performs.

A lot of people are talking about the poor performance of their KiwiSaver at the moment, but many of those people are not going to do anything about it… they just feel that it’s the market and nothing to do with their KiwiSaver provider.

Yes, the markets around the World may be in turmoil and many people are concerned as they see their KiwiSaver balances dropping, but some people have selected their KiwiSaver provider based on how they manage your money and are feeling more comfortable in the knowledge that they have protections in place.

What does your provider offer?

Let’s check what your KiwiSaver provider offers – please select your provider to see how protected you are:

Selecting A Kiwisaver Provider

As financial advisers we often see people that have their Kiwisaver with a bank so they can see the balance on their banking App, or with one of the providers that spends money advertising a specific period when they had the best returns for one of their funds.

There is more to selecting a KiwiSaver provider than having a fancy App or just looking at past returns.

When selecting a KiwiSaver provider you should look at the things that really make a difference to the way that they invest your money and make sure that you are comfortable that they do a good job.

There are three key things that your KiwiSaver should have;

- Diversification – this is a fundamental concept with any investment portfolio like Kiwisaver.

- Managing asset allocation as you age – KiwiSaver providers have various asset allocations that you can select or are automatically seletced depending on your tolerance for risk and time for an investment.

- Downside mitigation – this is important with any investment and including KiwiSaver. Some use Universa which has acted like an insurance policy for those institutional investors that opted for the protection offered with the Black Swan Protection Protocol.

These are three key components of an investment structure that we believe you should consider when selecting which fund manager you want to look after your KiwiSaver.

Most of us don’t know much about how our Kiwisaver providers manage our money and just trust that they will be doing the best they can for us. They may tell you about features like their banking App, or past performance if they can find a period where they performed well.

But most KiwiSaver providers will avoid telling you how they manage your money and the things that they don’t offer you.

When you know what your KiwiSaver provider offers you can start to make informed decisions.

Not All KiwiSaver Providers Are Equal

When the markets are going well everyone is happy.

People don’t really focus on what their fund managers are doing when they are seeing their fund balances increase, but when they start to decrease the focus comes onto the “why” are they not doing well.

As mentioned, because so many funds are not going well the fund managers have their marketing teams saying it’s the market and not them. They are telling you to “sit tight” and your fund will recover when the market does.

But why are not all funds performing badly?

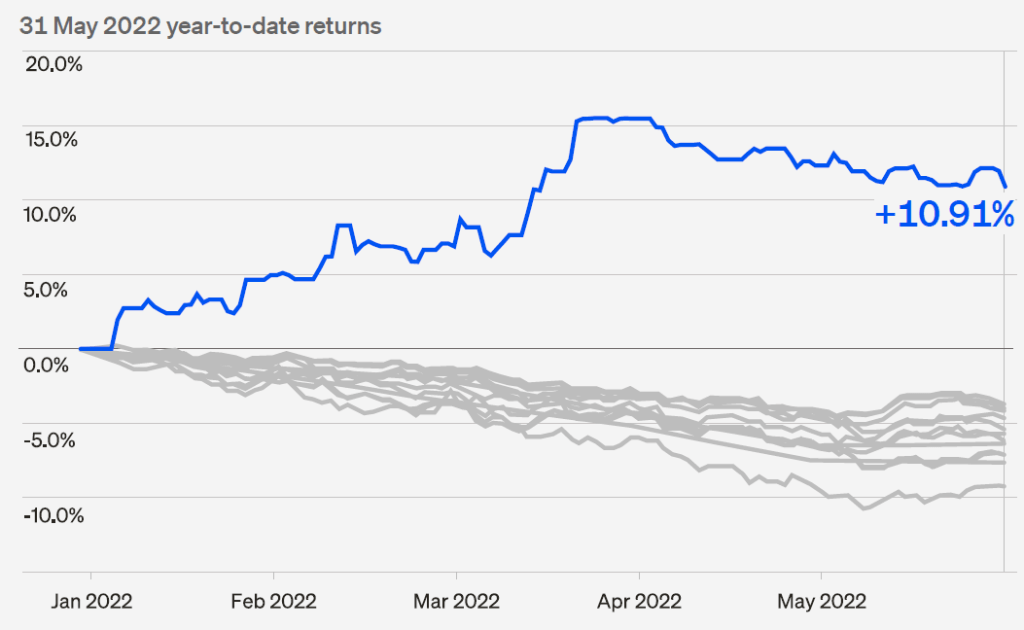

This graph illustrates how most KiwiSaver funds are performing with one that stands out. These are all Conservative KiwiSaver funds and of the 13 funds all except the 1 fund highlighted have lost their investors money.

Of course people may say that it’s great to look back in hindsight at a fund that has outperformed the others, but selecting to be in this fund was not luck, it was about understanding an important features that is often overlooked when things are going well – this stand-out fund benefited from the downside mitigation used.

Why Downside Mitigation Is So Important

When markets are going well people are focused on the upside (how much money they are making) and often forget to consider the downside (how much money they could lose).

Some of the fund managers that have been around for a while have seen market turmoil before and are more focused on how to manage the downside and not lose you money when things are not going well.

Good downside mitigation is like having an insurance policy – you might forgo some of the profits in the good times to have a safeguard that kicks in when the markets plunge. One of the best known is Universa which provides a back-stop for some investment managers.

Universa is a hedge fund with it’s flagship “Black Swan Protection Protocol” which provides institutional investors some protection against a plunge in markets. In plain English it acts like an insurance policy and means when a rear black swan event happens (a Global Financial Crisis, terrorists fly jets into skyscrapers, or a global pandemic freezes the global economy) then the fund cashes in option contracts and the investors receive large payouts. Forbes report that it’s institutional investors earned a staggering 3,612% in March 2020 when COVID shocked the world and markets plunged.

If you want to secure your KiwiSaver investments against a plunge in markets then you should switch to a provider that uses the “Black Swan Protection Protocol” as a downside mitigation.