TL;DR:

- Mortgage calculators estimate your borrowing limit based on income, expenses, debts, and lender rules. In New Zealand, the debt-to-income cap and stress tests often lower your maximum loan than the theoretical limit. Using a stress-tested rate of 8.5% in calculations and consulting an adviser helps determine practical affordability.

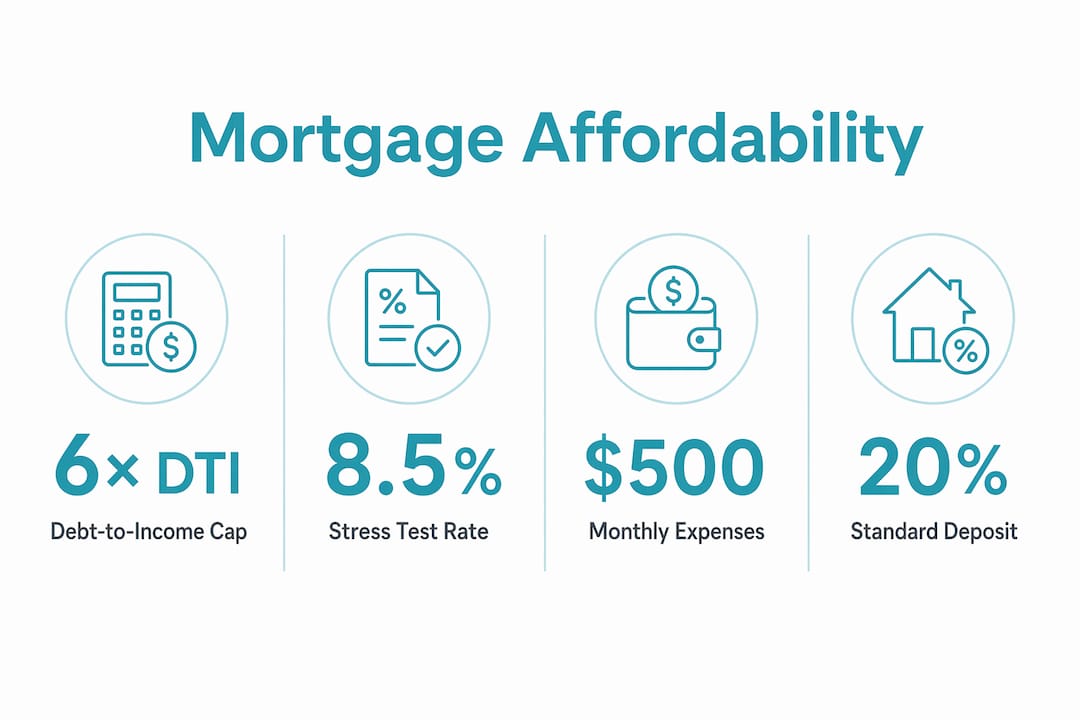

A mortgage calculator estimates the maximum home loan you can afford by combining your income, expenses, existing debts, and lender criteria into a single borrowing figure. In New Zealand, that figure is shaped by two hard limits: the Reserve Bank of New Zealand (RBNZ) debt-to-income (DTI) cap, which restricts most owner-occupier lending to 6× gross household income, and a serviceability stress test that calculates your repayments at interest rates of 8.0%–8.75%. Add deposit requirements, living costs, and government schemes like Kāinga Ora, and the picture becomes more detailed than a single number. This guide unpacks every layer so you can use a mortgage affordability calculator with confidence.

How do banks calculate how much mortgage you can afford in New Zealand?

Banks apply two tests simultaneously, and the lower result sets your borrowing limit. Understanding both tests is the most useful thing you can do before you touch any affordability calculator.

Test 1: The DTI cap. The RBNZ introduced formal DTI restrictions in july 2024. Most lenders now cap owner-occupier lending at 6× annual gross income. A household earning $120,000 per year can borrow a maximum of $720,000 under this rule. That ceiling sounds generous, but the second test often cuts it back.

Test 2: Serviceability stress test. Banks do not assess your repayments at today’s advertised rate. They stress test at 8.0%–8.75%, which is roughly 2%–3% above current market rates. This ensures you could still meet repayments if rates rise sharply. For many buyers, this test produces a lower maximum loan than the DTI cap, making it the binding constraint.

What banks deduct from your income. Banks assess your actual living expenses against the Household Expenditure Measure (HEM) benchmark and use whichever is higher. They also deduct the full repayment cost of any existing debts, including:

- Credit card limits (not just balances)

- Car loans and personal loans

- Buy Now Pay Later (BNPL) accounts

- Student loan repayments

Each of these reduces the income available to service a mortgage, which shrinks your maximum loan size. A $500 monthly car loan repayment can reduce your borrowing capacity by considerably more than $500 per month once stress-tested rates are applied.

Pro Tip: Run your numbers through a home loan affordability calculator using the stress-test rate of 8.5%, not the current advertised rate. The result will be more realistic and far less likely to leave you stretched.

What deposit amounts and schemes affect mortgage affordability?

Your deposit size directly affects how much you need to borrow, what interest rate you receive, and whether you qualify for government support. Getting this right before you apply saves you money from day one.

A 20% deposit is the standard threshold that avoids low-equity fees. Lenders add a premium of 0.25%–0.75% to your interest rate when your deposit falls below 20%. On a $600,000 loan, even a 0.5% rate premium adds thousands of dollars to your annual repayments.

The Kāinga Ora First Home Loan scheme changes the equation for eligible buyers. It allows a 5% deposit without the standard low-equity premium, provided you meet income caps of $95,000 for an individual or $150,000 for a couple. You must also intend to live in the property. This scheme removes one of the biggest upfront barriers for first-home buyers, particularly in regional centres where property prices are lower.

The table below shows how deposit requirements shift across different property prices, with and without Kāinga Ora support.

| Property price | 20% deposit required | 5% deposit (Kāinga Ora) |

|---|---|---|

| $500,000 | $100,000 | $25,000 |

| $650,000 | $130,000 | $32,500 |

| $800,000 | $160,000 | $40,000 |

| $1,000,000 | $200,000 | $50,000 |

Beyond the deposit itself, budget for additional purchase costs:

- Legal fees: typically $1,500–$3,000

- Building and LIM reports: $500–$1,500

- Home and contents insurance (first year upfront)

- Council rates adjustment at settlement

These costs are real and often catch first-home buyers off guard. Factor them into your savings target before you commit to a purchase price.

Pro Tip: Check your Kāinga Ora eligibility before you set a savings target. Qualifying for the 5% deposit scheme could mean you are ready to buy sooner than you think.

How to use a mortgage calculator effectively to plan your purchase

A mortgage calculator is only as accurate as the information you put into it. Garbage in, garbage out. Treat the calculator as a planning tool, not a pre-approval.

Gather these figures before you start:

- Gross annual income for all applicants, before tax

- Monthly living expenses, including rent, groceries, utilities, subscriptions, and transport

- All existing debt repayments, including minimum credit card payments and any BNPL commitments

- Your deposit amount, including any KiwiSaver balance you can withdraw

On KiwiSaver: after at least three years of contributions, you can withdraw your balance minus $1,000 towards your first home deposit. Combined with the Kāinga Ora First Home Loan, this can meaningfully reduce the gap between what you have saved and what you need.

Set the interest rate in your calculator to 8.5% rather than the current advertised rate. This mirrors the stress test banks apply and gives you a repayment figure you can genuinely plan around. Experts recommend borrowing below the maximum DTI cap to leave a buffer for rate changes, unexpected expenses, and life events.

Compare your affordability estimate against median house prices in the areas you are considering. If the numbers do not align, adjust your target location or savings timeline rather than stretching your borrowing limit. A mortgage adviser can run these comparisons across multiple lenders and locations, giving you a clearer picture than any single online tool.

Pro Tip: Borrow 10%–15% below your calculated maximum. That buffer is the difference between owning a home comfortably and being financially stretched every month.

What factors reduce your borrowing capacity and how can you improve it?

Most buyers are surprised to learn that their borrowing capacity is lower than the DTI formula suggests. The gap is almost always explained by debts and credit limits that quietly erode assessed income.

Credit cards are the single biggest hidden drag. A $20,000 credit card limit can reduce your borrowing capacity by $60,000–$80,000, even if the balance is zero. Banks treat the full limit as a potential liability. Reducing or cancelling unused credit cards before applying is one of the highest-impact steps you can take.

Other common capacity reducers include:

- Outstanding personal loans or car finance

- BNPL accounts (Afterpay, Laybuy, and similar services)

- Dependants, who increase living expense benchmarks

- Irregular or self-employed income, which banks assess conservatively

To improve your eligibility before applying:

- Pay down and close unused credit cards

- Settle personal loans where possible

- Avoid taking on new debt in the six months before application

- Confirm eligibility for government schemes like Kāinga Ora

- Consolidate high-interest debts to reduce monthly repayment obligations

A mortgage broker who understands lender-specific criteria can identify which lender’s assessment model suits your financial profile best. Not all banks apply the HEM benchmark the same way, and a broker can match you to the lender most likely to approve your application at the loan size you need.

Pro Tip: Six months before you apply, review every credit facility you hold. Closing a card you never use could add tens of thousands to your borrowing capacity at no cost.

What does mortgage affordability look like across New Zealand cities?

Affordability varies dramatically across New Zealand, and understanding where you stand relative to local median prices sets realistic expectations before you commit to a location.

Auckland’s median house price sits at approximately 10 times the median household income, making it the most challenging market for buyers on average wages. Regional centres and smaller cities sit at roughly 4–6 times income, offering meaningfully better affordability for buyers willing to consider alternatives to the main metros.

The table below illustrates estimated affordability benchmarks across key New Zealand locations.

| City / region | Estimated median price | Approx. income needed (6× DTI, 20% deposit) |

|---|---|---|

| Auckland | $950,000+ | $130,000+ household |

| Wellington | $750,000 | $105,000 household |

| Christchurch | $600,000 | $85,000 household |

| Hamilton | $650,000 | $90,000 household |

| Regional NZ | $400,000–$550,000 | $55,000–$80,000 household |

Combined incomes make a significant difference. Two incomes of $65,000 each produce a $130,000 household income, which unlocks a $780,000 borrowing capacity under the 6× DTI rule before stress testing. Single-income buyers face a harder path in Auckland and Wellington, where even the 6× cap falls short of median prices without a substantial deposit.

For buyers with limited credit history, the path forward often involves improving home loan eligibility through consistent savings, debt reduction, and confirming access to government schemes before approaching a lender directly.

Key takeaways

A mortgage calculator estimates your borrowing capacity using the RBNZ’s 6× DTI cap and a serviceability stress test at 8.0%–8.75%, with your deposit size and existing debts determining the final figure.

| Point | Details |

|---|---|

| DTI cap sets the ceiling | Most NZ lenders cap owner-occupier borrowing at 6× gross annual household income. |

| Stress tests often bind harder | Banks calculate repayments at 8.0%–8.75%, which frequently produces a lower limit than the DTI cap. |

| Deposit size changes everything | A 20% deposit avoids rate premiums; Kāinga Ora allows eligible buyers to start with just 5%. |

| Credit limits quietly shrink capacity | A $20,000 unused credit card limit can reduce borrowing by $60,000–$80,000. |

| Borrow below your maximum | Targeting 10%–15% below your calculated limit protects you from rate rises and unexpected costs. |

The honest truth about mortgage calculators in 2026

I have worked with hundreds of buyers who came to their first conversation clutching a calculator figure and a sense of certainty. The number was almost always higher than what any lender would actually approve. That gap is not a flaw in the calculator. It is a flaw in how most people use it.

The calculators that give you a realistic figure are the ones built around stress-tested rates and actual expense data, not optimistic assumptions. If you plug in your gross income and today’s advertised rate, you will get a number that feels exciting. If you plug in your net income after expenses and an 8.5% rate, you will get a number you can actually live with.

My strongest advice is this: use the calculator to set a direction, then sit down with a mortgage adviser before you set a budget. An adviser will run your numbers through multiple lenders, identify which government schemes you qualify for, and flag the debts that are quietly dragging your capacity down. That conversation is worth far more than any online tool, and it costs you nothing to have it.

The buyers who navigate this market well are not the ones who borrowed the most. They are the ones who borrowed the right amount, with a buffer, and a plan.

— Stuart

How Mortgagemanagers helps you find your real affordability number

Knowing your borrowing capacity on paper is one thing. Knowing which lender will approve it, at the best rate, with the right structure, is where Mortgagemanagers comes in.

Mortgagemanagers is a locally owned Auckland mortgage advisory business, based in Hobsonville and serving buyers across West Auckland, the North Shore, and remotely throughout New Zealand. The team works as your personal shoppers for a home loan, comparing lenders, interpreting affordability rules, and matching your financial profile to the lender most likely to say yes. Whether you are a first-home buyer exploring Kāinga Ora eligibility or a buyer with a complex income structure, Mortgagemanagers provides the expert guidance that turns a calculator estimate into a real approval.

FAQ

What is the maximum mortgage I can get in New Zealand?

Most NZ lenders cap owner-occupier borrowing at 6× gross annual household income under RBNZ DTI rules. Serviceability stress tests at 8.0%–8.75% often reduce the practical limit below that cap.

How much deposit do I need for a first home in New Zealand?

A 20% deposit avoids low-equity rate premiums. The Kāinga Ora First Home Loan allows eligible buyers to purchase with a 5% deposit, subject to income caps of $95,000 for individuals and $150,000 for couples.

Does a credit card affect how much I can borrow?

Yes. A $20,000 credit card limit can reduce your borrowing capacity by $60,000–$80,000, even with a zero balance. Banks treat the full limit as a potential liability when assessing your application.

Can I use KiwiSaver for a home deposit?

After at least three years of KiwiSaver contributions, you can withdraw your balance minus $1,000 towards a first home deposit. Combined with the Kāinga Ora First Home Loan, this can significantly reduce your upfront savings requirement.

What interest rate should I use in a mortgage affordability calculator?

Use 8.5% as your calculation rate, not the current advertised rate. This mirrors the stress test banks apply and gives you a repayment figure that reflects what lenders actually assess your capacity against.