Buying your first home in Hobsonville brings plenty of excitement, but it also means facing new financial terms like mortgage insurance. If your deposit is under 20 percent, lenders in New Zealand will require insurance cover to protect their interests, not yours. With changes taking effect from July 2025, premiums for First Home Loan insurance are set to rise from 0.5 percent to 1.2 percent of the loan value. Understanding these costs helps you make smarter choices about your loan and the true impact on your future repayments.

Table of Contents

- What Mortgage Insurance Means In New Zealand

- Types Of Mortgage Insurance For Buyers

- When Lenders Require Insurance Cover

- Costs, Premiums And Financial Implications

- Obligations, Risks And Common Pitfalls

Key Takeaways

| Point | Details |

|---|---|

| Mortgage Insurance Protects Lenders | In New Zealand, mortgage insurance primarily protects lenders, not borrowers, particularly when the deposit is below 20%. |

| Two Types of Insurance | Understand the difference between Lenders Mortgage Insurance (LMI) and Mortgage Protection Insurance (MPI); LMI protects the lender, while MPI covers your mortgage payments in cases of income loss. |

| Cost Implications | The cost of mortgage insurance can significantly affect your total borrowing costs, so consider whether to pay upfront or add it to your loan. |

| Explore Alternatives | Before accepting a loan with mortgage insurance, evaluate the option of saving for a larger deposit to avoid insurance altogether, which can save money in the long run. |

What Mortgage Insurance Means In New Zealand

Mortgage insurance in New Zealand protects your lender, not you. When you’re buying your first home in Hobsonville and can’t put down a 20% deposit, your lender takes on extra risk. That’s where Loan Protection Insurance (LPI) comes in. Essentially, if you default on your mortgage and the property sale doesn’t cover what you owe, this insurance covers the shortfall. It’s a safety net for the bank, which is why they require it when your deposit is smaller than 20%.

You pay the premium upfront (or add it to your loan), but the coverage belongs to your lender. This is a crucial distinction many first home buyers miss. Unlike income protection insurance or life insurance, mortgage insurance doesn’t benefit you directly if something goes wrong. Instead, it protects the bank’s investment in your home loan. If your financial situation changes and you can’t make payments, the insurance pays out to cover what they lose. The premium typically costs between 1% to 3% of your loan amount, depending on your deposit size and mortgage insurance provider.

For Hobsonville buyers putting down, say, 15% instead of 20%, mortgage insurance becomes a standard requirement. The smaller your deposit, the higher the insurance cost and the greater the perceived risk. It’s not a penalty, but rather a reflection of real lending risk. Some lenders in New Zealand offer different LPI products with varying premiums and terms, so the cost isn’t always identical across institutions. This is where getting advice early makes a real difference. Rather than accepting the first quote, understanding what you’re actually paying for allows you to ask the right questions and potentially negotiate better terms.

Pro tip: Ask your mortgage adviser about mortgage protection cover options early in your planning—not just loan protection insurance, but also income protection and life insurance—so you understand the full cost of borrowing before you make an offer on a property.

Types Of Mortgage Insurance For Buyers

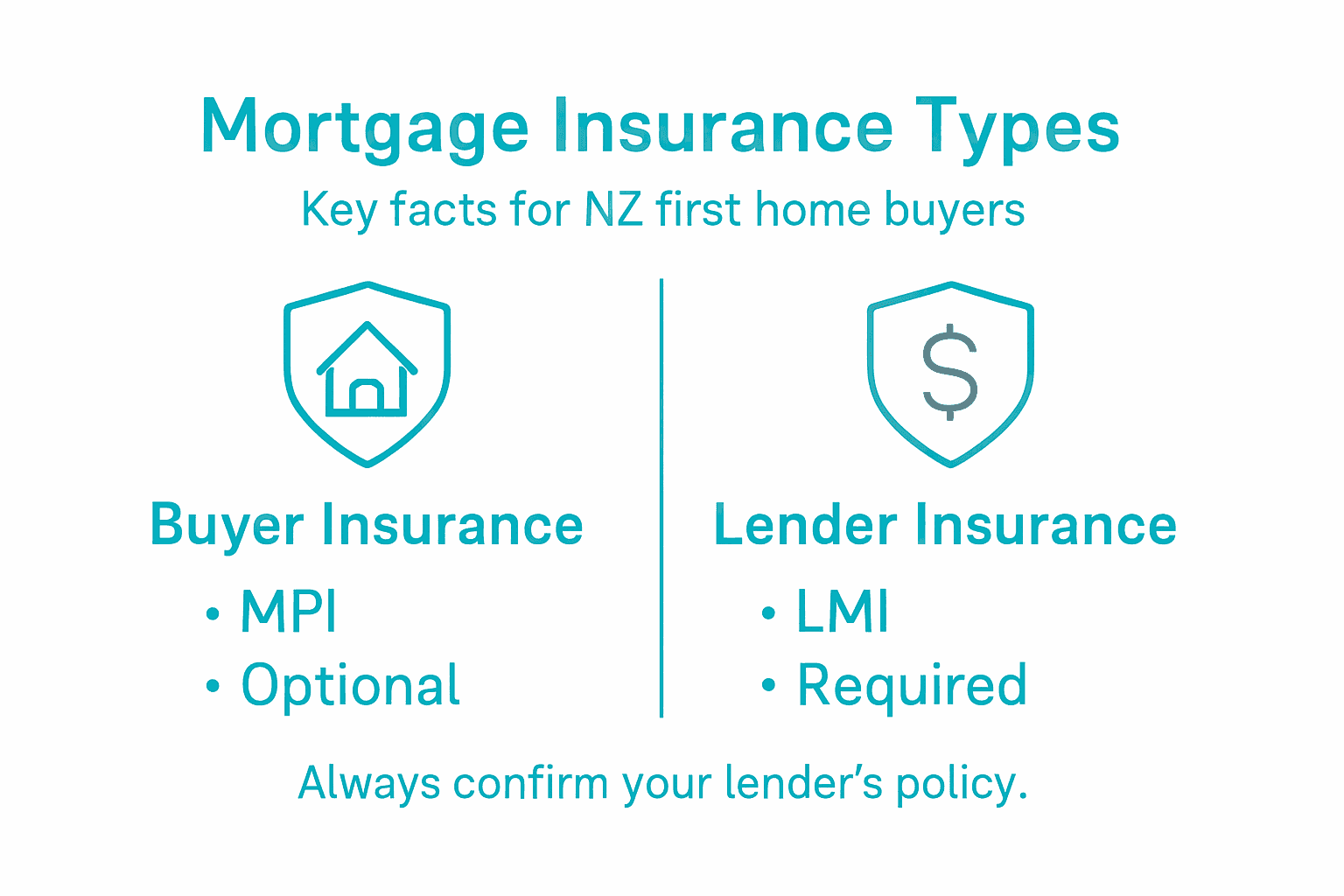

New Zealand offers several mortgage insurance options, and understanding the difference between them is critical before you commit to borrowing. The two main categories are Lenders Mortgage Insurance (LMI) and Mortgage Protection Insurance (MPI), and they serve completely different purposes. Lenders Mortgage Insurance is what your bank or lender requires when your deposit falls short of 20%. This protects the lender’s investment, not yours, and you’re the one paying the premium. Mortgage Protection Insurance, by contrast, is designed to cover your mortgage repayments if you become unable to work due to illness or injury. One protects the lender. The other protects you. Getting these mixed up could mean you’re paying for coverage that doesn’t actually help you when you need it most.

Lenders Mortgage Insurance (LMI) is non-negotiable if your deposit is less than 20%. For a first home buyer in Hobsonville putting down 15%, your lender will require this upfront. The cost ranges from 1% to 3% of your loan amount, depending on the size of your deposit and lenders mortgage insurance requirements. You can pay this as a lump sum before settlement or add it to your loan balance. Either way, you’re funding the insurance policy that protects the lender if you default. It doesn’t protect you financially, and it doesn’t reduce the amount you owe on your mortgage.

Mortgage Protection Insurance (MPI) is the optional insurance that actually benefits you. If you become unable to work through illness or injury, MPI covers your mortgage payments while you recover. Some policies include redundancy cover as well, which bridges the gap if you lose your job. This is where income replacement happens. Unlike LMI, you choose whether to take out MPI, and it’s genuinely designed with your financial security in mind. Many first home buyers overlook this because the bank doesn’t require it, but for Hobsonville buyers stretched financially to afford that deposit, losing your income could quickly lead to missing payments.

A comparison table can help visualise the differences:

| Insurance Type | Purpose | Who Benefits | Required | Cost |

|---|---|---|---|---|

| Lenders Mortgage Insurance | Protects lender from default | The bank | Yes (if deposit <20%) | 1-3% of loan |

| Mortgage Protection Insurance | Covers payments during income loss | You | Optional | Varies by provider |

The reality for most first home buyers is this: you’ll pay for LMI because the lender demands it. Whether you also take out MPI depends on your risk tolerance and financial circumstances. If you’re relying on two incomes to service the mortgage, or if losing your job would be catastrophic, MPI becomes less of a luxury and more of a necessity.

Pro tip: When comparing different mortgage structures, ask your adviser to outline both the mandatory LMI costs and the optional MPI premiums so you can see the total insurance expense before committing to your purchase.

When Lenders Require Insurance Cover

Lenders require mortgage insurance cover whenever your deposit sits below 20% of the property purchase price. This is the hard line that determines whether you’ll pay for insurance or not. If you’re putting down 20% or more, congratulations, you’ve cleared the threshold and insurance becomes optional rather than mandatory. But if you’re like most first home buyers in Hobsonville stretching to gather a 15% deposit, your lender will make insurance cover a non-negotiable condition of approving your loan. They’re not being difficult. They’re protecting themselves against the increased risk of lending on a smaller equity cushion.

The deposit threshold works like this: the smaller your deposit, the higher the risk from the lender’s perspective. A 10% deposit presents more risk than a 15% deposit, which presents more risk than 19%. Insurance premiums reflect this graduated risk. For First Home Loan borrowers specifically, insurance premiums on new applications have been subject to changes in government policy. From July 2025, premiums on new First Home Loan applications will increase as the government adjusts its subsidy approach. This matters for Hobsonville buyers planning to apply soon, as timing your purchase could affect your total borrowing cost. The insurance underwriting mechanism remains the same, but the amount you pay for that protection shifts based on policy changes and market conditions.

Here’s a summary of how deposit size impacts mortgage insurance cost and risk for New Zealand first home buyers:

| Deposit Size | Typical Insurance Premium | Lending Risk Level |

|---|---|---|

| 20% or more | No insurance required | Lowest risk |

| 15% | 1% to 3% of loan | Moderate risk |

| 10% | Higher, often above 3% | High risk |

| Below 10% | May not qualify for loan | Highest risk |

You have some flexibility in how you pay for mandatory insurance cover. You can settle the premium upfront before you take possession of your property, which means paying it as a separate transaction at settlement. Alternatively, you can add the insurance premium to your loan balance and pay it off gradually over the life of your mortgage. Neither option is inherently right or wrong, though adding it to the loan means you’re paying interest on the insurance premium itself, which increases the total cost. Some first home buyers add it to keep cash reserves available for unexpected expenses after purchase. Others prefer paying it upfront to avoid the extra interest charges. The choice depends on your financial position and cash flow situation.

Lenders also reassess insurance requirements if you refinance or vary your loan. If you later save enough to increase your deposit to 20% through additional payments or property appreciation, you may be able to remove or reduce insurance cover on a restructured loan. Conversely, if you’re taking out additional borrowing against your home, the deposit ratio recalculates on the total amount borrowed, potentially triggering new insurance requirements.

Pro tip: When discussing your loan with a mortgage adviser, ask about how your income stability interacts with insurance requirements, as lenders are increasingly focused on repayment capacity alongside deposit size, which can sometimes affect the overall risk assessment and insurance costs.

Costs, Premiums And Financial Implications

The cost of mortgage insurance has a direct impact on your borrowing capacity and monthly expenses as a first home buyer in Hobsonville. On a $400,000 loan with a 15% deposit, the insurance premium alone could range from $4,000 to $12,000 depending on the lender and current market conditions. These aren’t trivial amounts, and they matter when you’re already stretched to save your deposit. What makes this more complicated is that First Home Loan insurance premiums have increased significantly. The cost for borrowers rose from 0.5% to 1.2% of the loan value from July 2025, removing previous government financial support. For someone borrowing $400,000, that shift means an additional $2,800 out of pocket compared to previous years. This isn’t a small change, and it directly affects how much you’ll need to repay.

How you choose to pay the premium shapes your financial position immediately and long term. Pay it upfront at settlement, and you need to have the cash available alongside your deposit and other settlement costs. Many Hobsonville buyers are already stretched to their limit gathering deposits, so finding an extra $8,000 to $12,000 for insurance can be genuinely difficult. The alternative is adding the premium to your loan balance, which means you pay it off gradually over 25 or 30 years. The advantage is lower cash outlay now. The disadvantage is that you’re paying interest on the insurance premium itself. A $8,000 premium added to your loan at 7% interest over 25 years costs approximately $15,000 in total repayment (principal plus interest). That $7,000 difference between paying upfront and paying over time represents the true cost of choosing convenience. Neither option is wrong, but the financial implications differ substantially.

The table below highlights financial implications for paying mortgage insurance upfront versus adding it to the loan:

| Payment Method | Immediate Outlay | Long-term Cost Impact | Cash Flow Effect |

|---|---|---|---|

| Pay Upfront | Large payment | Lower total cost | Reduces initial cash |

| Add to Loan | Minimal upfront | Increased interest | Higher monthly repayments |

Your total monthly repayment increases when insurance is involved. Consider a $400,000 loan at current interest rates. Adding a $4,800 insurance premium (1.2% of loan) to your loan balance means you’re actually borrowing $404,800. That extra $4,800 translates to roughly $25 more per month over a 25-year term. Across a 30-year loan, it’s slightly less but still meaningful. Over the full loan term, you’re repaying $7,500 to $9,000 in extra interest charges on top of the insurance cost itself. These numbers compound, and they’re why getting professional advice early matters. A mortgage adviser can show you the exact numbers for your specific situation and help you decide whether to pay upfront or add to the loan.

There’s also a timing consideration that fewer first home buyers think about. If you’re planning to purchase before July 2025, you benefit from the lower premium structure. If you’re purchasing after, you face the new higher rate. For a Hobsonville buyer on the fence about timing, this could mean a difference of $2,800 on a $400,000 loan. That’s significant enough to factor into your purchase timeline if you have any flexibility.

Pro tip: Before committing to a property purchase, ask your mortgage adviser to calculate the exact insurance premium on your specific loan amount and show you the monthly repayment difference between paying upfront versus adding to the loan, then factor this into your overall borrowing assessment.

Obligations, Risks And Common Pitfalls

Most first home buyers in Hobsonville enter the mortgage insurance conversation without fully understanding their obligations and the long-term financial traps that can emerge. Your primary obligation is straightforward: you must pay the insurance premium if your deposit is below 20%. There’s no negotiating this with your lender. It’s a condition of the loan approval, not an optional extra you can politely decline. But here’s where things get murky. Many buyers don’t realise that accepting insurance isn’t just about paying a fee upfront. When you add that premium to your loan balance, you’re creating a compounding cost problem that extends decades into the future. The long-term cost implications of adding insurance to your mortgage are frequently underestimated. You’re not just paying the insurance amount. You’re paying interest on that insurance for the full term of your loan. On an $8,000 premium at 7% over 25 years, you’ll end up repaying approximately $15,000 total. That’s almost double the original insurance cost, and many buyers discover this uncomfortable reality only after they’ve already committed to the loan.

The second major pitfall is misunderstanding what you’re actually protected against. Mortgage insurance protects your lender, not you. If you face financial hardship and can’t make payments, the insurance pays out to cover the lender’s loss. You’re still liable for the debt. The insurance doesn’t disappear just because you’ve paid the premium. It sits there, attached to your loan, for as long as you’re borrowing below the 20% equity threshold. Some buyers mistakenly believe that insurance provides a safety net for their personal circumstances. It doesn’t. If you lose your job or face illness, mortgage insurance won’t help you keep making payments. This is why understanding the difference between mortgage insurance and income protection insurance matters. One protects the bank. The other protects you.

A third pitfall emerges when buyers don’t explore alternatives to paying for insurance immediately. If you’re a Hobsonville first home buyer with a 15% deposit on a $400,000 property, you could delay your purchase by six to twelve months, save aggressively, and increase your deposit to 20%. This eliminates the insurance requirement entirely. Or you could look for properties in lower price ranges where your deposit reaches 20%. The cost of waiting or adjusting your purchase price might be less than the cost of insurance spanning decades. Yet many buyers feel pressured to purchase now and don’t run these alternative scenarios. Your obligations feel set in stone, but they’re not always unavoidable with creative thinking.

Financial risks also emerge if your circumstances change after purchase. If property values decline and you’ve paid insurance on a 15% deposit, you might find yourself in a situation where you owe more than the property is worth, and the insurance is worthless to you. Conversely, if property values appreciate and you build equity, you may be able to refinance and remove the insurance. But refinancing costs money, and if interest rates have risen, refinancing might not make financial sense even with the insurance cost savings.

Pro tip: Before accepting a loan with mortgage insurance, run at least three scenarios with your mortgage adviser: paying insurance upfront, adding it to the loan, and delaying your purchase to save a larger deposit, then compare the total cost of each option over ten years to see which genuinely makes sense for your situation.

Take Control of Your Mortgage Insurance Journey with Expert Guidance

Navigating mortgage insurance in New Zealand can feel overwhelming for first home buyers in Hobsonville. From understanding Lenders Mortgage Insurance requirements when your deposit is below 20 percent to weighing up the benefits of optional Mortgage Protection Insurance, the financial decisions you make now will shape your homeownership journey for years to come. Avoid costly surprises by getting clear insights on premiums, risks, and payment options that often go unnoticed.

At Mortgage Managers, we specialise in helping you break down these complex insurance layers with trusted advice tailored to your unique circumstances. Whether you want to explore the smartest way to pay your insurance premium or find strategies to boost your deposit and reduce costs, our Auckland mortgage advisers are here to support you every step. Visit our main page to start your personalised plan, or learn more about mortgage protection cover and how it complements your home loan security. Don’t wait until settlement—ensure you fully understand your obligations and options by connecting with Mortgage Managers today for expert help you can count on.

Frequently Asked Questions

What is mortgage insurance in New Zealand?

Mortgage insurance in New Zealand protects lenders when borrowers cannot provide a deposit of 20% or more. It covers the lender’s loss if the borrower defaults on the mortgage.

How much does mortgage insurance cost?

The cost of mortgage insurance typically ranges from 1% to 3% of the loan amount, depending on the size of the deposit. This premium can be paid upfront or added to the loan balance.

What is the difference between Lenders Mortgage Insurance (LMI) and Mortgage Protection Insurance (MPI)?

Lenders Mortgage Insurance (LMI) protects the lender from default, while Mortgage Protection Insurance (MPI) covers the borrower’s mortgage payments if they become unable to work due to illness or injury. LMI is mandatory if the deposit is less than 20%, whereas MPI is optional.

How does the deposit size affect mortgage insurance requirements?

If your deposit is below 20% of the property purchase price, lenders will require mortgage insurance. The smaller the deposit, the higher the perceived risk and insurance cost associated with the loan.