Many first home buyers in New Zealand find themselves puzzled when they hear about property valuations during their home loan journey. You might wonder why the bank needs to value a property you’ve already agreed to purchase, or how this valuation differs from the asking price. These uncertainties can create stress during what should be an exciting milestone. This guide will clarify exactly what property valuations are, how they influence your borrowing capacity, and why understanding this process protects you from financial missteps. By the end, you’ll grasp how valuations work and their practical impact on your home purchase decisions.

Table of Contents

- Key takeaways

- What is a property valuation and why does it matter?

- How property valuations are conducted in New Zealand

- Factors that influence property valuation outcomes

- What property valuation means for your home loan and purchase

- How mortgage advisers can help you navigate property valuations

- Frequently asked questions about property valuations

Key Takeaways

| Point | Details |

|---|---|

| Valuation purpose | An independent assessment used by lenders to determine market value and the security backing your loan. |

| Valuation vs price | The valuation reflects market value as assessed by a registered valuer, not the seller’s asking price. |

| Borrowing impact | Lenders set your loan limits based on the lower figure of the price and the valuation, which can lower how much you can borrow. |

| Valuer credentials | Valuers are registered professionals with credentials recognised by the Valuers Registration Board and carry professional indemnity insurance. |

| First home prep | Ask for a copy of the valuation report to understand how the valuer assessed the property and use that insight in decisions. |

What is a property valuation and why does it matter?

A property valuation is an independent assessment conducted by a registered valuer to determine what a property is genuinely worth. This figure represents the property’s market value based on objective criteria, not emotional attachment or seller aspirations. Financial institutions use property valuations to determine the security value for home loans, ensuring the asset can cover the debt if circumstances change.

For first home buyers, this distinction matters enormously. You might fall in love with a property and agree to pay $850,000, but if the valuation comes back at $800,000, your lender will base their loan calculations on the lower figure. This protects both you and the bank from overextending on a property that might not hold its value.

Valuations serve several critical purposes in your home buying process:

- They establish the maximum amount banks will lend against a property

- They protect you from paying significantly more than market value

- They provide objective assessment independent of sales negotiations

- They reduce risk of negative equity if property values decline

Pro Tip: Request a copy of your valuation report even though the bank commissions it. Understanding how the valuer assessed your property helps you make informed decisions about your purchase and future property investments.

The valuation process creates a safety net for your financial future. When you understand that banks lend based on security rather than purchase price, you can negotiate more effectively and avoid overcommitting to properties that won’t support your borrowing needs. This knowledge transforms you from a passive participant into an informed decision maker who can spot potential issues before they derail your home loan application.

How property valuations are conducted in New Zealand

Registered valuers follow standard practices to assess property condition, comparable sales, and location factors. These professionals hold qualifications recognised by the Valuers Registration Board and maintain professional indemnity insurance. Their independence ensures lenders receive unbiased assessments free from sales pressure or emotional influence.

The valuation process typically unfolds through these key steps:

- Property inspection where the valuer examines physical condition, layout, and improvements

- Measurement and documentation of land size, building area, and notable features

- Research into recent sales of comparable properties within the local area

- Analysis of location factors including proximity to amenities and neighbourhood quality

- Compilation of findings into a formal valuation report with supporting evidence

During the physical inspection, valuers assess everything from structural integrity to cosmetic presentation. They note any weathertightness concerns, building code compliance, and maintenance issues that might affect value. This thorough examination takes between 30 minutes and two hours depending on property size and complexity.

Comparable sales analysis forms the backbone of most residential valuations. Valuers identify properties similar in size, age, condition, and location that have sold recently, typically within the past three to six months. They adjust these sale prices up or down based on differences between the comparable properties and yours. A property with a renovated kitchen might justify a higher valuation than a comparable home needing updates.

| Valuation component | What valuers examine | Impact on final value |

|---|---|---|

| Physical condition | Structure, weathertightness, maintenance | High |

| Location quality | Neighbourhood, amenities, transport links | High |

| Comparable sales | Recent similar property transactions | Very high |

| Legal factors | Zoning, easements, building consents | Medium to high |

Pro Tip: Ensure your property is presented well on valuation day. While valuers assess objectively, a tidy, well-maintained appearance can influence their perception of overall property care and condition.

The final valuation report provides lenders with a detailed property description, valuation figure, and supporting rationale. This document becomes a crucial part of your mortgage structure and loan approval process. Understanding how valuers work helps you anticipate potential issues and address them proactively before they impact your borrowing capacity.

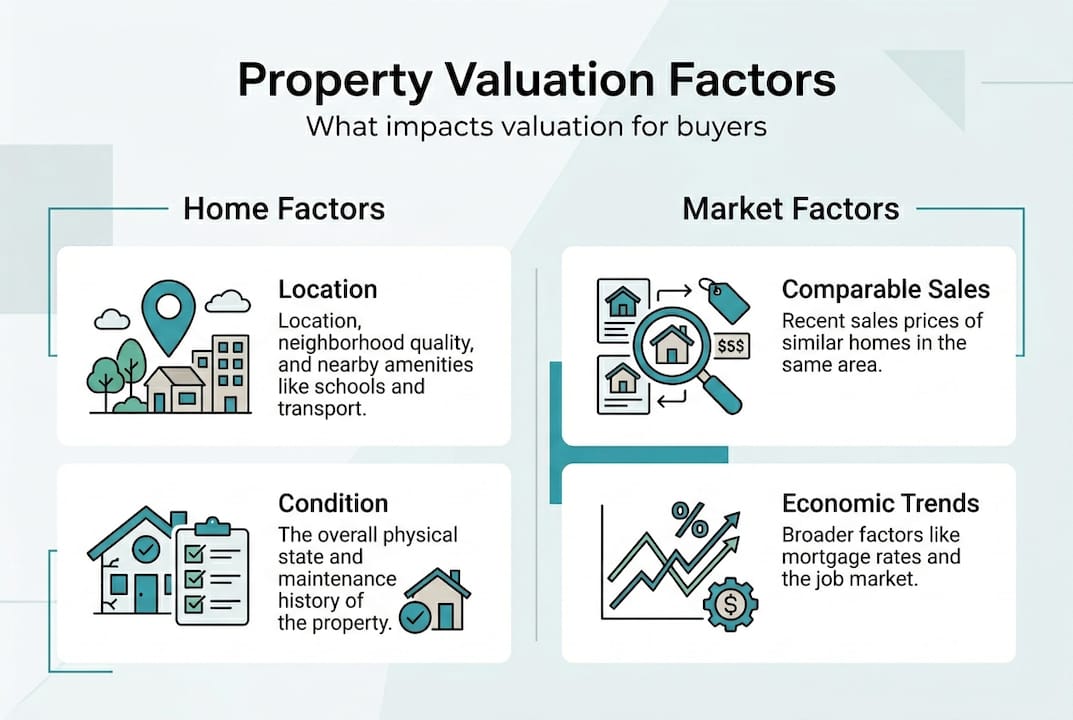

Factors that influence property valuation outcomes

Location stands as the single most influential factor in property valuations. A modest home in a highly desirable suburb will typically value higher than a larger property in a less sought-after area. Registered valuers consider location, property condition, and recent comparable sales when determining value. Proximity to quality schools, public transport, shopping centres, and employment hubs all contribute to location desirability.

Property condition directly impacts valuation outcomes. A well-maintained home with modern updates commands higher values than properties requiring significant repairs or renovations. Valuers assess everything from roof condition to plumbing systems, noting deferred maintenance that might concern lenders. Even cosmetic issues like dated bathrooms or worn carpets can reduce valuations by thousands of dollars.

Key factors affecting your property valuation include:

- Neighbourhood characteristics and local amenity quality

- Property age, construction quality, and maintenance history

- Recent sale prices of comparable homes within one to two kilometres

- Legal restrictions such as zoning limitations or easements

- Current market conditions including buyer demand and available inventory

Recent comparable sales provide the most objective valuation benchmark. Valuers analyse properties similar to yours that have sold in the preceding three to six months, adjusting for differences in size, condition, and features. In a rising market, valuations tend to increase as comparable sales reflect higher prices. Conversely, declining markets produce lower valuations as recent sales show weakening demand.

| Valuation factor | Positive influence | Negative influence |

|---|---|---|

| Location | Desirable suburb, good schools, transport | Remote area, limited amenities |

| Condition | Recent renovations, excellent maintenance | Deferred repairs, weathertightness issues |

| Market timing | Strong buyer demand, low inventory | Weak demand, oversupply |

| Legal factors | Clear title, compliant improvements | Zoning restrictions, easements |

Economic conditions create broader influences on property valuations. Interest rate changes affect buyer borrowing capacity and demand levels. When rates rise, fewer buyers can afford higher prices, potentially softening valuations. Employment trends, population growth, and investor sentiment also shape the market environment in which valuers operate.

Understanding these factors empowers you to assess whether a property might face valuation challenges before you commit to purchase. Properties in transition areas, those with obvious maintenance needs, or homes significantly overpriced relative to recent sales all carry higher risk of valuing below purchase price. This knowledge helps you negotiate more effectively and avoid disappointment during the loan approval process.

What property valuation means for your home loan and purchase

Banks use valuation value to determine how much they will lend on a home loan application. This creates direct practical implications for your borrowing capacity and deposit requirements. If you’ve arranged to purchase a property for $750,000 but it values at $720,000, the bank calculates your loan-to-value ratio based on the lower figure.

This valuation shortfall scenario requires you to bridge the gap with additional deposit funds. Assume you planned for a 20% deposit on $750,000, requiring $150,000 upfront. With a $720,000 valuation, the bank will lend a maximum of $576,000 at 80% LVR. You now need $174,000 in deposit funds to complete the $750,000 purchase, an unexpected additional $24,000.

Valuations protect you from several significant risks:

- Borrowing more than a property is genuinely worth

- Entering negative equity if property values decline

- Overcommitting financially to assets with limited resale potential

- Purchasing properties that won’t support future refinancing needs

Lenders typically require formal valuation reports before issuing final loan approval. This occurs after your conditional approval but before settlement. The timing means you’ve usually paid your deposit and committed legally to the purchase. Understanding this sequence highlights why getting mortgage advice before property hunting prevents costly surprises.

Pro Tip: Include a valuation clause in your sale and purchase agreement allowing you to withdraw if the property values below the purchase price. This protects you if the bank’s valuation creates a financing shortfall you cannot cover.

Valuation results influence your negotiating position throughout the purchase process. If a property values significantly below asking price, you gain leverage to renegotiate with the seller. Many sellers will reduce their price rather than lose a committed buyer over a valuation issue. This makes the valuation process a potential opportunity rather than purely a hurdle.

Understanding mortgage repayments becomes easier when you grasp how valuations set your borrowing limits. A property that values well supports larger loans at better interest rates, while valuation challenges might restrict your options or require lender mortgage insurance. This knowledge helps you set realistic expectations about what you can afford and how lenders will assess your application.

The valuation process ultimately serves your interests by preventing you from overpaying for property or borrowing beyond sustainable levels. While valuation shortfalls create immediate challenges, they protect you from far greater financial stress down the track. Embrace valuations as a safeguard rather than an obstacle, and use the information they provide to make smarter property decisions.

How mortgage advisers can help you navigate property valuations

Mortgage advisers bring specialist knowledge that transforms property valuations from confusing obstacles into manageable steps in your home buying journey. These professionals understand how different lenders interpret valuation reports and which banks might offer more favourable assessments for specific property types. Their experience helps you anticipate potential valuation issues before they derail your purchase plans.

Working with mortgage advisers means accessing insights about which properties might face valuation challenges based on location, condition, or market factors. They review properties you’re considering and flag potential concerns before you commit to purchase. This proactive approach saves you from emotional and financial disappointment when valuations come in lower than expected.

Mortgage advisers also negotiate with lenders when valuation results create financing gaps. Their established relationships with bank valuation teams sometimes allow for second opinions or detailed discussions about valuation methodology. Understanding the role of a mortgage adviser in New Zealand helps you appreciate how their expertise smooths the entire loan approval process. If you’re searching for local expertise, Auckland mortgage brokers offer personalised guidance tailored to regional market conditions and property characteristics.

Frequently asked questions about property valuations

What is a property valuation?

A property valuation is an independent assessment conducted by a registered valuer to determine a property’s market worth for lending purposes. Banks commission valuations to ensure the property provides adequate security for the loan amount requested. This differs from a property appraisal or the asking price, as it focuses specifically on what the property could sell for in current market conditions rather than seller expectations.

How much does a property valuation cost?

Property valuation costs typically range from $600 to $1,200 depending on property location, size, and complexity. Most lenders charge this fee to borrowers as part of the loan application process. Some banks waive valuation fees for customers meeting specific criteria or during promotional periods. Your mortgage adviser can identify lenders offering fee waivers or reduced valuation costs as part of their service.

Can I challenge a property valuation if it seems too low?

You can request a second valuation or provide additional evidence to support a higher value, though success varies. If you have recent comparable sales the valuer missed or evidence of improvements not reflected in the report, present these to your lender. Some banks allow formal valuation reviews where another valuer reassesses the property. Your mortgage adviser can guide you through this process and determine whether challenging makes sense in your situation.

How long does a property valuation remain valid?

Most lenders consider property valuations valid for three to six months from the inspection date. After this period, market conditions may have changed sufficiently to require a fresh assessment. If your loan application extends beyond the valuation validity period, expect to pay for an updated valuation. In rapidly changing markets, some lenders require more frequent valuations to ensure their security remains adequate.

Does property valuation affect my interest rate?

Property valuation indirectly affects your interest rate through its impact on your loan-to-value ratio. Higher LVRs typically attract higher interest rates as they represent greater lending risk. If your property values lower than expected, your LVR increases, potentially moving you into a higher rate tier. Conversely, properties that value well support lower LVRs and access to better interest rates. This makes valuation outcomes financially significant beyond just loan approval.