Mortgage pre-approval is not the loan guarantee many first home buyers assume it to be. This conditional letter from lenders indicates your potential borrowing limit but remains subject to property checks, updated financials, and strict time limits. Understanding what pre-approval truly means in New Zealand’s current lending environment helps you navigate the home buying journey with realistic expectations, stronger negotiating power, and clearer budgets whether you’re working with limited deposits, credit challenges, or government assistance schemes.

Table of Contents

- Understanding Mortgage Pre-Approval In New Zealand

- Government Assistance And Low Deposit Options For First Home Buyers

- Financial Profile Assessment For Mortgage Pre-Approval

- Role Of Mortgage Advisers In Improving Pre-Approval Success

- Common Misconceptions About Mortgage Pre-Approval

- Step-By-Step Pre-Approval Process And Practical Tips For Success

- Discover Expert Mortgage Advising With Mortgage Managers

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Conditional nature | Pre-approval is conditional and valid typically 60-90 days, not a guaranteed final loan approval. |

| Government assistance | Kāinga Ora First Home Loans enable deposits as low as 5% for eligible buyers using schemes and KiwiSaver funds. |

| Financial scrutiny | Lenders rigorously assess credit history, income stability, and debt ratios under Reserve Bank regulations affecting capacity. |

| Adviser advantage | Mortgage advisers access 15+ lenders with one application, improving chances especially for complex credit or low deposit situations. |

| Time sensitivity | Expired pre-approvals require renewal to maintain buying power during extended property searches. |

Understanding mortgage pre-approval in New Zealand

Mortgage pre-approval provides a conditional written offer from lenders showing how much you could potentially borrow. This 60-90 day conditional indication helps you understand your budget limits before making property offers. Unlike final loan approval, pre-approval doesn’t guarantee funds will be released.

Lenders issue pre-approval based on your current financial position but reserve the right to reassess when you find a property. They’ll conduct property valuations, updated credit checks, and verify your circumstances haven’t changed. If your income drops, debts increase, or credit score deteriorates during the validity period, lenders can withdraw or reduce the approved amount.

The typical validity window spans approximately 60 to 90 days from issue date. After this timeframe expires, you’ll need to reapply with updated documentation. Many first home buyers mistakenly believe pre-approval lasts indefinitely or guarantees loan disbursement regardless of circumstances.

Pre-approval delivers several practical advantages during your property search:

- Clarifies realistic price ranges for properties you can afford

- Strengthens negotiating position with sellers who prefer committed buyers

- Identifies potential lending issues early before making offers

- Speeds final approval process once you find the right property

Understanding these mortgage pre-approval benefits prevents disappointment and helps you time your property search effectively. The conditional nature means you’re not locked into borrowing but have a reliable indication of your financial capacity under current lending standards.

Government assistance and low deposit options for first home buyers

New Zealand offers multiple pathways for first home buyers struggling to save traditional 20% deposits. The Kāinga Ora First Home Loan requires as little as 5% deposit for eligible buyers meeting income and house price caps. This government scheme bridges the gap between your savings and property purchase price.

KiwiSaver members can withdraw funds after three years of contributions to put towards first home deposits. These withdrawals combine with personal savings to meet minimum deposit requirements under various schemes. First home buyers with limited cash savings particularly benefit from leveraging KiwiSaver balances accumulated through employment contributions.

Several low deposit lenders in NZ accept deposits between 5% and 10% under specific conditions. These options typically require lenders mortgage insurance and attract higher interest rates compared to standard 20% deposit loans. The table below compares deposit requirements across different options:

| Option | Minimum Deposit | Eligibility Criteria | Key Considerations |

|---|---|---|---|

| Kāinga Ora First Home Loan | 5% | Income caps, house price limits, first home buyer status | Government backed, strict criteria |

| Welcome Home Loan | 5-10% | Income thresholds, property value limits | Available through participating lenders |

| Standard low deposit | 10-15% | Varies by lender, often requires strong credit | Lenders mortgage insurance required |

| KiwiSaver withdrawal | Contributes to deposit | 3+ years membership, first home purchase | Can be combined with other schemes |

Eligibility for these programmes depends on meeting specific income thresholds, property price caps, and residency requirements. Even with low deposit options available, lenders still assess your credit history, income stability, and debt levels rigorously. Government schemes reduce deposit barriers but don’t eliminate financial scrutiny during the pre-approval process.

Financial profile assessment for mortgage pre-approval

Lenders evaluate three core financial dimensions when assessing pre-approval applications: income consistency, credit history quality, and debt-to-income ratios. Reserve Bank lending restrictions since 2021 require banks to verify borrowers can service loans under stressed interest rate scenarios, typically 2-3% above current rates. This stress testing significantly impacts approved borrowing amounts.

Your credit score reflects payment history across all credit accounts including personal loans, credit cards, and utility bills. Late payments, defaults, or court judgments reduce approval chances and may require specialist lenders. Demonstrating consistent income through employment or self-employment records over 6-12 months strengthens your application substantially.

Credit card limits reduce borrowing capacity by $50k-$60k per $10k limit under current Reserve Bank rules. This calculation assumes you could potentially max out revolving credit facilities, forcing lenders to factor these amounts into debt servicing calculations. Paying down or closing unused cards before applying improves your borrowing power dramatically.

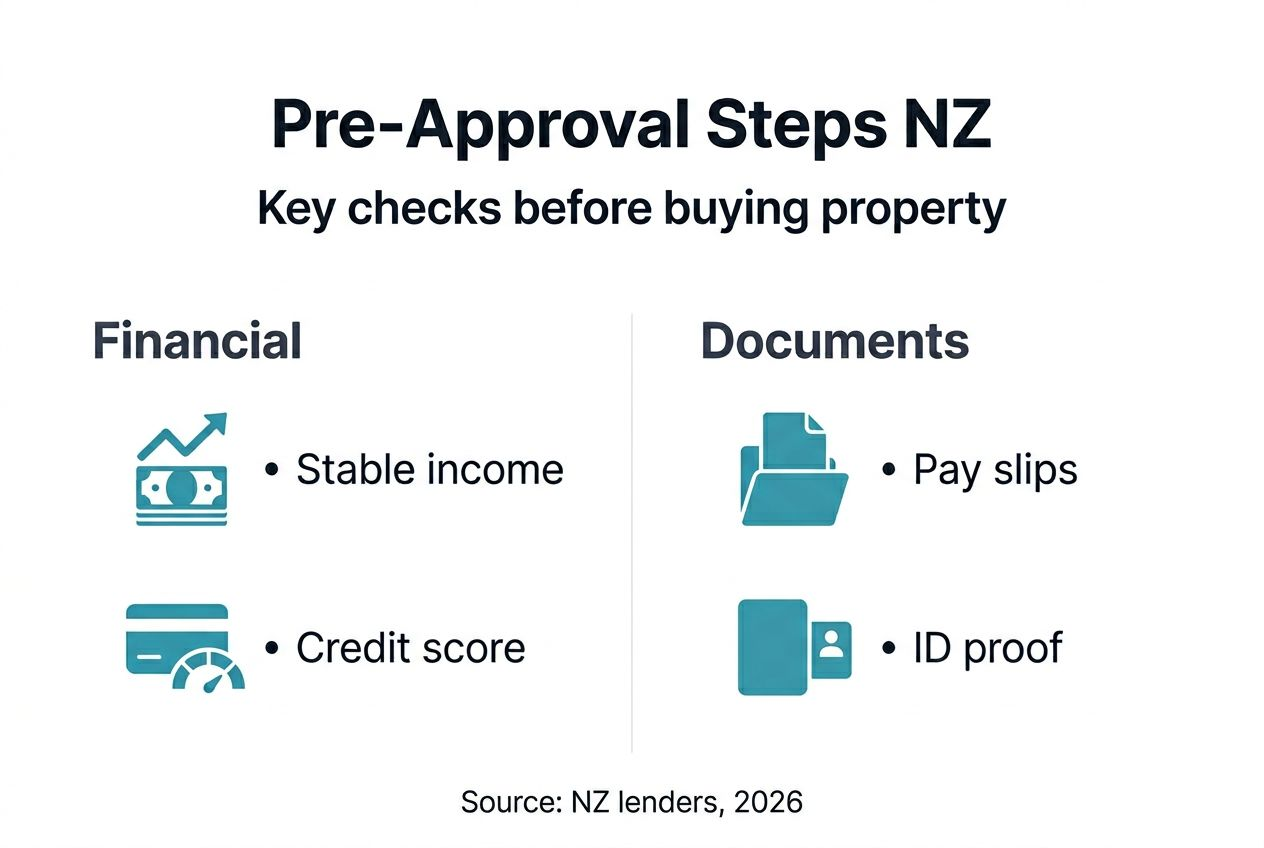

Lenders review these essential financial documents during pre-approval:

- Recent payslips covering last 3 months for salary earners

- Tax returns and financial statements for 2 years if self-employed

- Bank statements showing 3-6 months transaction history

- Credit reports detailing all existing debts and payment patterns

- Proof of deposit savings including KiwiSaver statements

- Identification documents and residency verification

Debt-to-income ratios compare your total monthly debt repayments against gross monthly income. Most New Zealand lenders prefer ratios below 40-45%, though this varies by institution and applicant circumstances. Higher ratios signal greater financial stress and reduced capacity to absorb rate increases or income disruptions.

Pro Tip: Before applying, obtain your credit report, pay down revolving credit limits to zero if possible, and gather complete documentation covering 6-12 months of financial activity to present the strongest possible application.

Accurate disclosure of all debts, even small personal loans or buy-now-pay-later schemes, prevents application delays or rejections. Lenders verify information through credit bureaus and bank statements, so omissions or inaccuracies undermine trust and approval prospects. The mortgage application checklist for NZ ensures you provide complete information upfront.

Role of mortgage advisers in improving pre-approval success

Mortgage advisers submit applications to multiple lenders simultaneously, dramatically expanding your options beyond single bank relationships. Advisers apply to 15+ lenders with one application, saving weeks of individual bank appointments and paperwork duplication. This multi-lender access proves particularly valuable when your financial profile doesn’t fit mainstream lending criteria.

First home buyers with credit impairments, irregular income, or minimal deposits face rejection from major banks applying standard policies. Specialist lenders and second-tier institutions often accommodate these situations with adjusted terms. Advisers know which lenders suit specific borrower profiles and structure applications to highlight strengths while addressing potential concerns proactively.

Experienced advisers negotiate interest rates, fee waivers, and loan terms on your behalf using relationships built over years of business referrals. They understand current lending appetite across institutions and can direct applications to banks actively seeking borrowers in your category. This insider knowledge improves both approval chances and final loan conditions.

Mortgage advisers provide these key functions during pre-approval:

- Assess your complete financial position before lender submission

- Match your profile with suitable lenders based on current policies

- Prepare applications highlighting strengths and mitigating weaknesses

- Negotiate competitive rates and terms across multiple institutions

- Manage documentation requirements and lender communications

- Explain conditional approval terms and next steps clearly

The benefits of using mortgage brokers in NZ extend beyond simple application lodgement to strategic positioning and ongoing support throughout the approval process. Advisers often identify opportunities to improve your financial position before applying, such as debt consolidation or credit repair strategies that strengthen future applications.

Pro Tip: Engage a mortgage adviser at least 3-6 months before serious property searching to address any credit issues, optimise debt levels, and understand realistic borrowing capacity under current lending conditions.

Understanding the role of mortgage brokers in NZ helps you leverage their expertise effectively. Most advisers operate on lender-paid commission, though some charge fees for complex situations. Clarify fee structures upfront to avoid surprises during the process.

Common misconceptions about mortgage pre-approval

Many first home buyers treat pre-approval as guaranteed funding, proceeding with property offers assuming lenders cannot withdraw approved amounts. Pre-approval remains conditional on property valuation, title checks, and your financial circumstances remaining unchanged. Lenders regularly decline final approval when property values fall short, undisclosed debts emerge, or employment situations change between pre-approval and settlement.

The 60-90 day validity period requires renewal if your property search extends beyond this timeframe. Some buyers mistakenly believe initial pre-approval covers indefinite searching periods. Expired approvals require complete reapplication with updated documentation, potentially revealing changed circumstances that affect borrowing capacity.

Government low deposit schemes reduce upfront cash requirements but don’t eliminate credit and income assessment standards. Buyers sometimes assume 5% deposit eligibility guarantees approval regardless of other financial factors. Lenders still verify income stability, employment continuity, and credit history meet their risk thresholds even when deposit barriers decrease.

Common pre-approval myths corrected:

- Pre-approval does not lock in interest rates beyond validity period

- Lenders can reduce approved amounts if circumstances deteriorate

- Multiple pre-approvals from different banks can impact credit scores

- Conditional approval still requires satisfactory property and legal checks

- Expired pre-approvals don’t automatically renew without reapplication

Understanding the complete mortgage approval process in NZ clarifies the distinction between conditional pre-approval and final unconditional approval. The gap between these stages creates risk for buyers who assume pre-approval equals guaranteed funding.

Property valuations conducted after offers frequently return figures below purchase prices in cooling markets. Lenders base final loan amounts on the lower of purchase price or valuation, potentially leaving buyers scrambling to cover shortfalls. Pre-approval amounts assume property values support the loan size, but this verification only occurs after you’ve committed to purchasing.

Step-by-step pre-approval process and practical tips for success

Securing mortgage pre-approval in New Zealand follows a structured sequence that benefits from thorough preparation and strategic timing. Understanding each stage helps you avoid delays and present the strongest possible application to lenders.

- Gather complete financial documentation covering 6-12 months of income, expenses, debts, and savings including KiwiSaver statements and deposit proof

- Consult with a mortgage adviser to assess your borrowing capacity, identify suitable lenders, and address any credit or income concerns before formal application

- Submit applications through your adviser to multiple lenders simultaneously or apply directly to your preferred bank with complete documentation packages

- Await lender assessment typically requiring 3-5 working days with complete documentation for conditional approval decisions

- Review conditional approval letter carefully noting validity period, approved amount, conditions, and required next steps when finding property

- Begin property search within approved budget knowing you have financial backing subject to property and final checks

- Provide property details to lender once offer accepted to trigger valuation and final unconditional approval process

Key documents requiring preparation before starting applications include:

- Three months consecutive payslips for employed applicants

- Two years tax returns and financial statements for self-employed buyers

- Six months bank statements from all accounts showing savings patterns

- Current credit report identifying all debts and payment history

- Proof of deposit including gift letters if family assistance involved

- Photo identification and proof of residency status

Timing your application strategically improves approval chances and reduces stress during property searches. Apply when your financial position appears strongest, after addressing credit issues, paying down debts, and accumulating maximum deposit savings. Avoid making major purchases or changing employment immediately before or during the pre-approval process.

Practical tips enhancing approval success:

- Close unused credit cards and reduce limits on retained cards to minimum necessary levels

- Maintain consistent banking patterns avoiding unusual large deposits or withdrawals during assessment periods

- Disclose all income sources and debts accurately even if minor to prevent verification issues

- Allow extra time if self-employed as income verification requires additional documentation and analysis

- Consider applying through advisers if your situation involves any complexity beyond standard employment and clean credit

Pro Tip: Compile your financial documents into organised digital folders before beginning applications so you can respond quickly to lender requests and avoid delays from missing information that extends the standard 3-5 day turnaround.

The steps to get a mortgage in NZ continue beyond pre-approval to final unconditional approval and settlement. Maintaining financial stability throughout this entire timeline protects your approved status and prevents last-minute complications. Referring to a comprehensive mortgage application checklist ensures you’ve covered all requirements before submission.

Discover expert mortgage advising with Mortgage Managers

Navigating New Zealand’s mortgage landscape demands expertise, lender access, and strategic positioning that most first home buyers lack. Mortgage Managers delivers personalised mortgage advice connecting you with multiple lenders through a single application process.

Our experienced advisers specialise in supporting first home buyers facing credit challenges, limited deposits, or complex income situations that mainstream banks struggle to accommodate. We streamline your pre-approval journey from initial assessment through to final loan settlement, negotiating competitive terms and explaining conditions clearly at every stage. Whether you’re accessing government schemes, navigating low deposit options, or seeking the best rates available, personal mortgage advisers at Mortgage Managers guide you confidently towards home ownership. Understanding the complete role of mortgage advisers in NZ helps you leverage professional support effectively. Partner with expert mortgage advisers who prioritise your success and simplify the path from pre-approval to property ownership.

Frequently asked questions

Are there any fees for applying for mortgage pre-approval?

Most New Zealand lenders don’t charge application fees specifically for pre-approval, though policies vary between institutions. Mortgage advisers typically receive commission from lenders rather than charging borrower fees, but some may have service fees for complex situations. Always clarify fee structures with both lenders and advisers upfront to avoid unexpected costs during your application process.

How long does mortgage pre-approval last in New Zealand?

Mortgage pre-approval typically remains valid for 60 to 90 days from the issue date depending on lender policies. If your property search extends beyond this validity period, you’ll need to reapply with updated financial documentation. Lenders reassess your circumstances during renewal to ensure your financial position hasn’t deteriorated since initial approval.

Can I get pre-approval with bad credit or low deposit?

Yes, government schemes like Kāinga Ora First Home Loans support buyers with deposits as low as 5%, while specialist lenders accommodate credit impairments that mainstream banks reject. Mortgage advisers prove particularly valuable for navigating these complex situations, matching your profile with appropriate lenders and structuring applications to maximise approval chances. Expect higher interest rates and additional conditions compared to standard lending.

What documents do I need to provide for pre-approval?

Common requirements include recent payslips or financial statements, bank statements covering 3-6 months, identification documents, proof of deposit savings, and details of all existing debts. Self-employed applicants need tax returns and business financial statements for typically two years. Having complete documentation prepared before applying significantly speeds the approval process and demonstrates financial organisation to lenders.