Many first home buyers believe going directly to banks secures the best mortgage deals. The reality is quite different. 67% of New Zealanders who switched banks used mortgage advisers, revealing the crucial role brokers play in Auckland’s competitive home loan market. This article explains how mortgage brokers provide expert support, wider lender access, and better loan outcomes for first home buyers.

Table of Contents

- Introduction To Mortgage Brokers And Their Role In New Zealand

- How Mortgage Brokers Enhance Access To Multiple Lenders And Loan Products

- Expert Guidance, Personalised Advice, And Application Support

- Cost, Commission Model, And Common Misconceptions

- Tangible Benefits: Better Rates, Faster Approvals, And Advocacy

- Common Misconceptions About Mortgage Brokers In New Zealand

- How To Choose And Work Effectively With A Mortgage Broker In Auckland

- Summary And Next Steps For First Home Buyers

- Support From Expert Mortgage Advisers In Auckland

Key takeaways

| Point | Details |

|---|---|

| Wider lender access | Brokers connect you to banks, credit unions, and non-bank lenders banks don’t offer. |

| Expert guidance | Advisers stay current on lender policies and tailor loan recommendations to your situation. |

| No borrower fees | Lenders pay broker commissions, typically 0.6% to 0.8%, with no direct costs to you. |

| Better loan terms | Brokers negotiate competitive rates and improve approval chances through lender relationships. |

| Time savings | Brokers manage applications and paperwork, reducing your workload significantly. |

Introduction to mortgage brokers and their role in New Zealand

Mortgage brokers act as intermediaries between borrowers and lenders. They connect you with suitable home loan products from multiple financial institutions. In New Zealand’s diverse lending landscape, brokers provide access to banks, credit unions, building societies, and non-bank lenders.

Brokers differ fundamentally from bank loan officers. Bank staff represent one institution and promote only their products. Brokers work for you, comparing options across the market to find loans matching your financial circumstances and goals.

New Zealand’s regulatory framework ensures broker accountability. The Financial Markets Authority oversees mortgage advisers, requiring proper licensing, disclosure of commissions, and adherence to conduct standards. This legal structure protects borrowers and maintains professional standards.

For Auckland first home buyers, understanding why you should use a mortgage broker reveals advantages that direct bank applications cannot match.

Key functions mortgage brokers perform include:

- Assessing your financial situation and borrowing capacity

- Researching loan products from multiple lenders

- Comparing interest rates, fees, and loan features

- Preparing and submitting loan applications

- Negotiating terms with lenders on your behalf

- Managing documentation and communication throughout the process

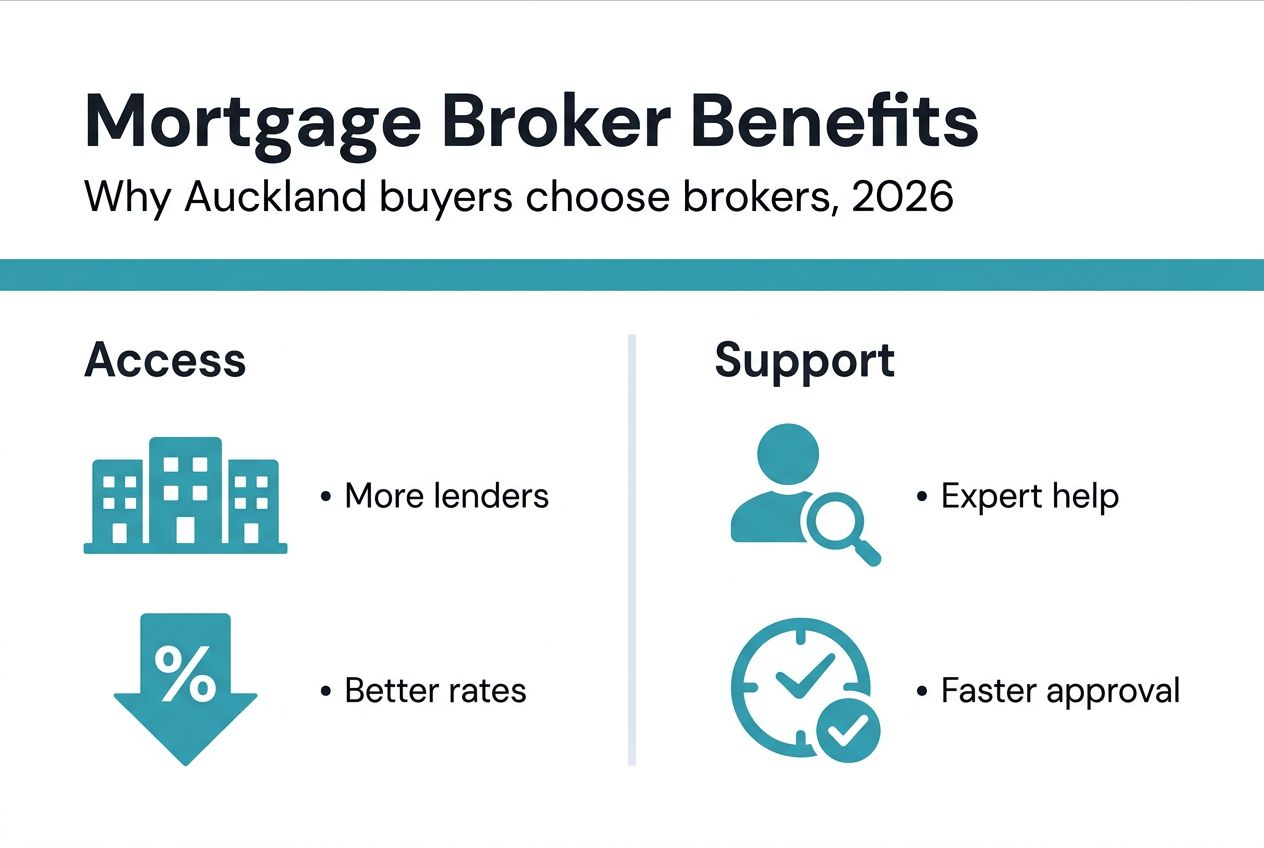

How mortgage brokers enhance access to multiple lenders and loan products

Mortgage brokers provide access to multiple lenders, enabling you to compare a wider range of loan products than any single bank offers. Their networks span major banks, smaller regional institutions, credit unions, and specialist non-bank lenders.

This diversity matters significantly for first home buyers. Traditional banks may decline applications that alternative lenders approve. Non-bank lenders often consider applications from self-employed borrowers, those with limited credit history, or buyers with smaller deposits.

Brokers identify competitive interest rates and favourable loan terms across the market. They know which lenders offer the best rates for specific borrower profiles. This knowledge proves invaluable when marginal rate differences translate to thousands of dollars over a loan’s lifetime.

| Access type | Direct bank application | Mortgage broker |

|---|---|---|

| Lender options | 1 institution | 15 to 30+ lenders |

| Loan products | 5 to 10 products | 100+ products |

| Specialist lenders | No access | Full access |

| Rate comparison | Manual research needed | Automatic comparison |

| Application flexibility | Single submission | Multiple suitable options |

For borrowers with unique circumstances, broker access to home loan options banks can’t provide opens doors that direct applications keep closed. First home buyers benefit particularly from this expanded choice.

The benefits of multiple lender access include:

- Competitive interest rates through market-wide comparison

- Diverse loan structures matching different financial situations

- Access to promotional rates and special offers

- Options for buyers with non-traditional income sources

- Alternative solutions when major banks decline applications

Expert guidance, personalised advice, and application support

Mortgage brokers stay current on constantly changing lender policies, interest rates, and regulatory requirements. This knowledge ensures your application meets current criteria and maximises approval chances. Lenders frequently adjust their lending policies, deposit requirements, and assessment criteria.

Brokers provide tailored recommendations on loan structure and terms. They analyse your income, expenses, savings, and future plans to suggest appropriate loan amounts, repayment schedules, and features. This personalised approach prevents borrowing too much or choosing unsuitable loan products.

Mortgage brokers can increase loan application approval rates by directing borrowers to lenders with criteria matching their financial situation. Rather than submitting applications randomly, brokers target lenders most likely to approve your specific circumstances.

Brokers manage application paperwork and liaise with lenders throughout the process. They handle documentation requirements, respond to lender queries, and coordinate settlements. This management reduces your workload significantly and prevents common errors that delay approvals.

They help you avoid common mistakes and application pitfalls. First time borrowers often overlook critical details or misunderstand lender requirements. Brokers guide you through complex processes, explaining each step clearly.

Pro Tip: Prepare all financial documents before meeting your broker. Gather pay slips, bank statements, tax returns, and identification upfront. Complete documentation accelerates the application process and demonstrates your financial organisation to lenders.

Exploring tips for first home buyers alongside broker services maximises your preparation and success chances.

Brokers provide expert mortgage adviser guidance covering:

- Current lending criteria and policy changes

- Optimal loan-to-value ratios for your situation

- Fixed versus floating rate recommendations

- Offset accounts and redraw facility benefits

- Insurance requirements and options

- Long-term refinancing strategies

Cost, commission model, and common misconceptions

Mortgage brokers receive commission from lenders, not borrowers. When a broker arranges your home loan, the lender pays them a commission for bringing in your business. Broker commissions are typically 0.6% to 0.8%, with most brokers charging no direct fees to borrowers.

This payment structure means you access professional mortgage advice and application support at no direct cost. The lender absorbs the commission as part of their customer acquisition expenses. Your interest rate and loan terms remain the same whether you apply through a broker or directly.

New Zealand’s regulatory framework requires brokers to disclose their commission structures transparently. Before proceeding, brokers must explain how they’re paid, whether they receive higher commissions from particular lenders, and any potential conflicts of interest.

Common misconceptions create unnecessary hesitation about using brokers. Many borrowers incorrectly believe brokers charge substantial fees, reducing loan affordability. Others assume brokers show bias toward lenders paying higher commissions, compromising advice quality.

Legal and regulatory requirements ensure broker impartiality and proper disclosure. The Financial Markets Conduct Act mandates that brokers act in clients’ best interests, disclose all material information, and maintain professional competence through ongoing education.

Choosing a mortgage broker in NZ requires understanding these cost structures and regulatory protections.

Understanding mortgage broker commissions clarifies the financial relationship:

- Misconception: Brokers charge borrowers high fees. Reality: Most brokers charge no direct fees; lenders pay commissions.

- Misconception: Broker services increase loan costs. Reality: Loan terms remain identical to direct bank applications.

- Misconception: Brokers recommend loans paying highest commissions. Reality: Regulations require recommendations in clients’ best interests.

- Misconception: Using brokers limits lender choice. Reality: Brokers access more lenders than individual borrowers can approach.

Tangible benefits: better rates, faster approvals, and advocacy

Mortgage brokers can negotiate better interest rates and loan terms inaccessible to individuals. Their ongoing relationships with lenders and volume of business provide negotiating leverage. Lenders offer brokers competitive rates to maintain strong referral relationships.

Brokers improve loan approval chances through strategic lender matching. They analyse your financial profile against each lender’s criteria, submitting applications only to institutions likely to approve. This targeted approach avoids multiple declined applications damaging your credit record.

67% of New Zealanders who switched banks for home loans used mortgage advisers, demonstrating their importance in securing competitive deals. Switching banks independently involves substantial research and negotiation. Brokers streamline this process significantly.

Brokers act as your advocate throughout the loan process. They prioritise your interests, not the lender’s. When issues arise, brokers negotiate solutions and push for faster processing. This advocacy proves particularly valuable for first home buyers navigating unfamiliar territory.

| Factor | Direct bank application | Mortgage broker |

|---|---|---|

| Lender access | Single bank only | 15 to 30+ lenders |

| Rate negotiation | Limited to no leverage | Strong negotiating position |

| Application management | Borrower handles entirely | Broker manages process |

| Advocacy | No independent support | Broker represents your interests |

| Time investment | Substantial research needed | Broker conducts research |

| Approval optimisation | Trial and error approach | Strategic lender matching |

Pro Tip: Leverage your broker’s lender relationships by asking them to negotiate rate reductions or fee waivers. Brokers often secure better terms than advertised standard rates, particularly when lenders compete for quality borrowers.

Achieving better home loan outcomes with brokers stems from their market knowledge and negotiating power.

Key benefits include:

- Interest rate reductions of 0.1% to 0.5% through negotiation

- Faster approval timeframes through efficient application management

- Higher approval rates via strategic lender matching

- Reduced application fees through broker relationships

- Ongoing support for refinancing and loan restructuring

Understanding broker negotiation benefits reveals the financial advantages of professional representation.

Common misconceptions about mortgage brokers in New Zealand

Several persistent myths discourage first home buyers from engaging brokers. Understanding the reality behind these misconceptions builds confidence in using professional mortgage advice.

The belief that brokers charge borrowers direct fees remains widespread. In reality, lenders pay broker commissions, making services free for most borrowers. Some brokers charge fees for complex situations, but they disclose these upfront.

Many assume brokers offer loans from just one or two preferred lenders. Brokers actually access dozens of lenders, providing far wider choice than direct bank applications. Their business model depends on finding suitable matches across the entire market.

Concerns about biased advice stem from commission structures. New Zealand regulations require brokers to recommend loans in your best interests, regardless of commission variations. Professional standards and legal obligations enforce this impartiality.

Some believe using brokers slows the loan process compared to direct applications. Brokers actually accelerate approvals through efficient application management, complete documentation, and lender relationship leverage. Their experience prevents delays common in direct applications.

Debunking mortgage broker myths reveals the value of professional mortgage support.

Clearing up misconceptions:

- Brokers provide services at no direct cost to most borrowers

- Wide lender networks offer genuine choice and competition

- Regulatory requirements ensure impartial, client-focused advice

- Professional management accelerates rather than delays applications

- Brokers maintain ongoing relationships, not just one-time transactions

How to choose and work effectively with a mortgage broker in Auckland

Selecting the right mortgage broker significantly impacts your home loan success. Start by verifying their lender network and market access. Ask how many lenders they work with and whether they access specialist non-bank lenders alongside major banks.

Inquire about commission and fee structures upfront. While most brokers charge no direct fees, understanding their payment model ensures transparency. Ask whether they receive higher commissions from particular lenders and how this affects recommendations.

Prepare your financial documents before your first meeting. Organised documentation demonstrates financial responsibility and accelerates the assessment process. Gather recent pay slips, bank statements, tax returns, proof of savings, and identification.

Communicate your borrowing goals and constraints clearly. Explain your target property price, preferred deposit amount, repayment capacity, and any concerns about approval. Clear communication enables brokers to target suitable lenders and loan products effectively.

Effective collaboration steps:

- Research potential brokers and verify their licensing and experience

- Schedule initial consultations with two or three brokers to compare approaches

- Provide complete financial information and documents promptly

- Ask detailed questions about loan options, costs, and approval likelihood

- Maintain regular communication throughout the application process

- Respond quickly to information requests and lender queries

- Review all loan documents carefully before signing

- Maintain the relationship for future refinancing and property purchases

Pro Tip: Maintain transparency and responsiveness during the application process. Quick responses to broker and lender requests prevent delays. Hiding financial issues or providing incomplete information jeopardises approvals and damages your relationship with the broker.

Learning how to choose a mortgage broker ensures you partner with professionals who genuinely support your home buying goals.

Summary and next steps for first home buyers

Mortgage brokers provide Auckland first home buyers with significant advantages over direct bank applications. Their access to multiple lenders ensures wider choice and competitive loan products. Expert guidance through the application process improves approval chances and secures better terms.

The commission-based payment model means you access professional advice at no direct cost. Regulatory protections ensure brokers act in your best interests, not lenders’. Common misconceptions about fees, bias, and limited choice don’t reflect the reality of professional mortgage broking.

Tangible benefits include negotiated interest rate reductions, faster approvals, and ongoing advocacy throughout the loan process. For first home buyers navigating Auckland’s property market, these advantages prove invaluable.

Your next practical steps involve preparing your financial documents, researching Auckland mortgage brokers, and scheduling initial consultations. Early engagement allows brokers to assess your situation, identify suitable lenders, and guide preparation activities that strengthen your application.

Finding a mortgage broker in Auckland connects you with local experts who understand the regional property market and lender landscape.

Support from expert mortgage advisers in Auckland

Ready to simplify your home loan journey? Mortgage Managers brings decades of Auckland market expertise to first home buyers throughout the region. Based in Hobsonville with easy access to West Auckland, the North Shore, and beyond, we provide personalised support tailored to your unique circumstances.

Our extensive lender network ensures you access competitive rates and suitable loan products major banks don’t offer. We act as your personal shoppers for a home loan, comparing options and negotiating terms on your behalf. Whether you’re navigating first home buyer schemes or complex financial situations, our team guides you through every step.

Find a mortgage broker in Auckland who prioritises your interests and delivers results. Discover how our Auckland mortgage adviser expertise transforms the home buying process from overwhelming to achievable. Contact us today to discuss your home loan goals.

Frequently asked questions

What does a mortgage broker do?

Mortgage brokers compare loan products from multiple lenders including banks, credit unions, and non-bank institutions. They assist with application preparation, paperwork management, and lender communication throughout the process. Brokers provide personalised loan advice tailored to your financial situation and goals.

Are mortgage brokers free to use for borrowers?

Most mortgage brokers charge no direct fees to borrowers. Lenders pay broker commissions, typically 0.6% to 0.8% of the loan amount, for arranging home loans. Regulations require transparent disclosure of all costs and payment structures before proceeding.

How do mortgage brokers improve my chances of loan approval?

Brokers know lender requirements thoroughly and match your application to suitable institutions. They tailor applications to fit specific criteria, avoiding common pitfalls that trigger declines. Strategic lender selection prevents multiple declined applications damaging your credit record.

Can I use a mortgage broker and still apply directly to a bank?

Using a broker provides access to wider lender choice than single bank applications offer. Direct bank applications limit your options to one institution’s products. Combining approaches creates complexity and potential confusion, though it’s technically possible.