Over 60% of Australian buyers looking at property in New Zealand are caught off guard by strict deposit requirements. With the standard expectation sitting at a hefty 20% deposit, navigating the New Zealand home market demands careful preparation and a clear understanding of lender expectations. Whether you are a first home buyer or an experienced investor, learning how deposit rules work in New Zealand helps you avoid costly mistakes while opening the door to smarter financial choices.

Table of Contents

- Understanding Deposit Requirements In Nz

- Minimum Deposit Amounts For Different Buyers

- Low Deposit Home Loans And Lvr Rules

- Special Considerations For Bad Credit Borrowers

- Additional Costs And Mistakes To Avoid

Key Takeaways

| Point | Details |

|---|---|

| Understanding Deposit Requirements | Most lenders require a deposit of around 20%, though first home buyers may find options as low as 10-15% under certain conditions. |

| Low Deposit Home Loans | Recent regulatory changes have made low deposit loans more accessible, with offerings for 5-10% deposits, often requiring careful risk assessment. |

| Bad Credit Considerations | Borrowers with poor credit history may face higher deposit requirements (30-40%) and should work on improving their credit score before applying. |

| Budget for Additional Costs | Beyond the deposit, potential buyers should factor in various additional costs such as legal fees and mortgage insurance, which can significantly increase upfront expenses. |

Understanding Deposit Requirements in NZ

Navigating home deposits in New Zealand requires strategic financial planning. Most lenders expect first home buyers to present a substantial deposit, typically around 20% of the property’s total value. This percentage represents a critical threshold for mortgage approval and demonstrates financial readiness to potential lenders.

Understanding deposit requirements involves more than just saving money. Home deposit requirements vary significantly based on individual financial circumstances, property type, and lending institution policies. First home buyers might find some lenders willing to consider lower deposit percentages, though this often comes with additional conditions like higher interest rates or mandatory mortgage insurance.

The New Zealand property market has several pathways for meeting deposit requirements. Some buyers utilise government assistance programmes, which can help reduce the initial financial barrier. Others might explore alternative strategies such as combining personal savings, KiwiSaver contributions, and potential family support. Each approach requires careful consideration of individual financial health and long term mortgage affordability.

Pro Buyer Tip: Research multiple lending institutions and compare their deposit requirements before committing. Understanding the fine print can save thousands in potential additional costs and help you secure more favourable mortgage terms.

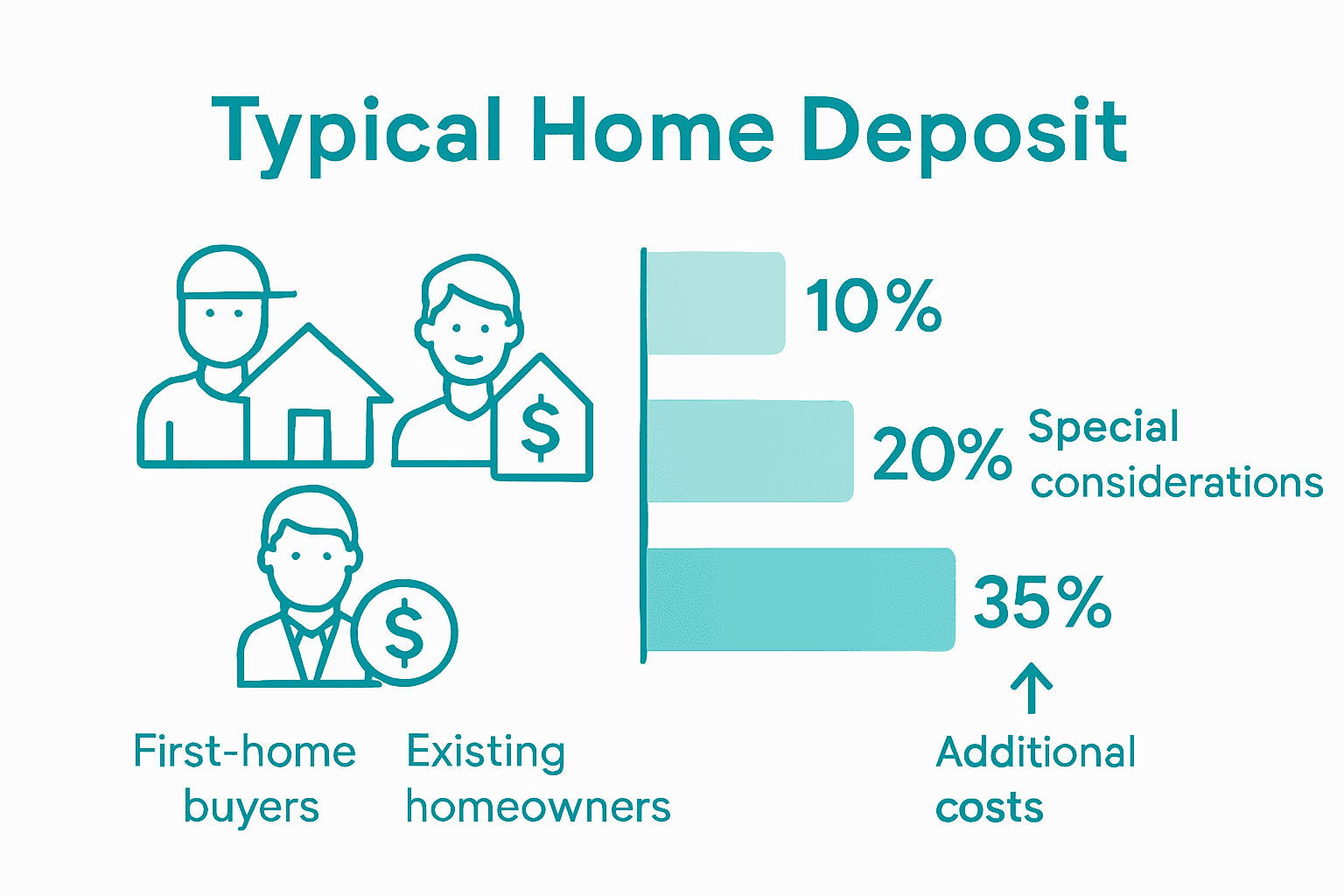

Minimum Deposit Amounts for Different Buyers

Navigating minimum deposit amounts requires understanding the nuanced landscape of home lending in New Zealand. First home buyers, investors, and experienced property owners encounter different deposit expectations based on their unique financial profiles. Low deposit home loans present alternative pathways for those struggling to meet traditional deposit requirements.

Different buyer categories face varied deposit expectations. First home buyers might access more flexible lending criteria, potentially securing mortgages with deposits as low as 10-15%. Existing homeowners typically need to demonstrate stronger financial stability, with most lenders expecting 20-30% deposit amounts. Investment property purchasers often face the most stringent requirements, with many banks mandating deposits around 35-40% to mitigate potential investment risks.

Banks and non-bank lenders assess deposit requirements through multiple lens. Credit history, income stability, employment type, and overall financial health significantly influence deposit expectations. Self-employed individuals, contractors, and those with variable income streams might need to provide larger deposits or additional financial documentation to secure mortgage approval.

Pro Buyer Tip: Calculate your borrowing capacity before house hunting. Understanding your precise deposit requirements can help you strategically plan your property purchase and avoid potential financial disappointment.

Here’s a comparison of deposit expectations for different types of buyers in New Zealand:

| Buyer Type | Typical Deposit Range | Special Considerations |

|---|---|---|

| First Home Buyer | 10% – 20% | May access government grants or KiwiSaver |

| Existing Homeowner | 20% – 30% | Strong financial history often expected |

| Investor | 35% – 40% | Stricter rules to manage investment risks |

| Bad Credit Borrower | 30% – 40% | Higher deposits to offset lending risk |

Low Deposit Home Loans and LVR Rules

Low deposit home loans represent a critical pathway for New Zealand homebuyers facing significant upfront financial barriers. Understanding loan-to-value ratio (LVR) rules is essential for navigating the complex mortgage landscape. Mortgage lending restrictions are evolving as regulatory bodies seek to balance financial stability with housing accessibility.

Traditionally, LVR rules have restricted low deposit borrowing, typically requiring buyers to demonstrate substantial financial capacity. Most lenders mandate minimum deposits around 20%, with stricter requirements for investment properties. However, recent regulatory changes are creating more flexible lending environments, particularly for first home buyers. Some specialised loan products now offer pathways for buyers with deposits as low as 5-10%, though these often come with additional risk management conditions.

The complexity of low deposit home loans extends beyond simple percentage calculations. Lenders assess multiple risk factors, including credit history, income stability, employment type, and overall financial health. Self-employed individuals and those with variable income streams might face more rigorous scrutiny, potentially requiring larger deposits or additional financial documentation to secure mortgage approval.

Pro Buyer Tip: Research multiple lending institutions and understand their specific low deposit loan criteria. Comparing offerings can reveal unexpected opportunities and potentially save thousands in long-term borrowing costs.

Special Considerations for Bad Credit Borrowers

Bad credit presents significant challenges in the home loan landscape, but it doesn’t necessarily prevent homeownership. Deposit requirements can be more complex for borrowers with credit challenges, with lenders implementing stricter assessment protocols to mitigate potential financial risks.

Borrowers with problematic credit histories typically encounter more rigorous lending criteria. Banks and non-bank lenders often require larger deposit amounts, sometimes ranging from 30-40% instead of the standard 20%, to compensate for perceived higher default risks. These increased deposit thresholds serve as a protective mechanism, allowing lenders to secure their investment while providing opportunities for borrowers to demonstrate financial rehabilitation.

Navigating bad credit home loans demands strategic financial planning. Potential borrowers should focus on improving their credit score, maintaining stable employment, and preparing comprehensive documentation that showcases financial responsibility. Some specialized lending institutions offer tailored products for individuals with credit challenges, though these often come with higher interest rates and more stringent repayment conditions.

Pro Buyer Tip: Obtain a comprehensive credit report and address any outstanding issues before applying for a home loan. Proactively resolving credit discrepancies can significantly improve your borrowing potential and demonstrate financial maturity to potential lenders.

Additional Costs and Mistakes to Avoid

Home loan deposits involve significantly more financial complexity than many first-time buyers anticipate. Unexpected costs can dramatically impact overall borrowing capacity, with Lenders Mortgage Insurance (LMI) representing a substantial potential expense for those unable to meet standard deposit requirements.

Beyond the base deposit, buyers must budget for numerous additional financial obligations. These can include legal fees, property valuation costs, building inspection charges, and potential mortgage establishment fees. Many borrowers underestimate these expenses, which can collectively add thousands of dollars to the upfront costs of purchasing a property. Some lenders charge application fees, ongoing account maintenance fees, and penalty charges for early loan refinancing or termination.

Below is an overview of common extra costs involved in purchasing a property in NZ:

| Additional Cost | Typical Amount | Purpose |

|---|---|---|

| Legal Fees | $1,500 – $3,000 | Conveyancing and contract review |

| Valuation Report | $500 – $1,000 | Confirms property market value |

| Building Inspection | $400 – $1,000 | Assesses property condition |

| Lenders Mortgage Insurance | Varies, 1-2%+ | Protects lender for low deposit loans |

| Application/Establishment Fees | $200 – $1,000 | Covers set-up costs for your mortgage |

Common mistakes can severely compromise a buyer’s mortgage application and long-term financial stability. Prospective homeowners should avoid rapidly changing employment, making large undocumented financial transactions, or opening multiple credit accounts in the months leading up to a mortgage application. Credit history scrutiny has become increasingly sophisticated, with lenders examining comprehensive financial behaviour rather than isolated credit scores.

Pro Buyer Tip: Create a comprehensive budget that includes all potential property purchase expenses beyond the deposit. Factor in a financial buffer of 10-15% to cover unexpected costs and provide breathing room in your financial planning.

Secure Your Home Deposit with Expert Mortgage Advice

Understanding the deposit requirements in New Zealand can feel overwhelming with all the different percentages, LVR rules and credit considerations discussed in the article. If you are a first home buyer, investor or facing challenges like bad credit the clear pain points include saving a sizeable deposit, navigating lender expectations and managing additional costs such as Lenders Mortgage Insurance. These hurdles can create stress and uncertainty which is why personalised mortgage guidance is essential.

At Mortgage Managers, we specialise in simplifying this complex process for buyers across Auckland, West Auckland, the North Shore and across New Zealand. As your local mortgage advisers based in Hobsonville we provide tailored solutions that match your unique financial situation. We help you understand your deposit options, identify low deposit home loan opportunities, and prepare for all related costs so that surprises do not derail your plans.

Take control of your home buying journey today. Visit Mortgage Managers to connect with expert advisers who can improve your borrowing potential and provide clear next steps. Don’t let confusing deposit requirements hold you back from owning your dream home. Get personalised support now and make your property goals a reality.

Frequently Asked Questions

What is the typical deposit range for first home buyers?

Most lenders expect first home buyers to present a deposit between 10% to 20% of the property’s total value.

Are there options for low deposit home loans?

Yes, some lenders offer low deposit home loans with deposits as low as 5-10%, although these often come with additional conditions and higher interest rates.

How do deposit requirements vary for different types of buyers?

First home buyers may secure loans with deposits as low as 10-15%, while existing homeowners typically need to provide 20-30%, and investors often face higher requirements of 35-40%.

What additional costs should buyers consider beyond the deposit?

Buyers should also budget for legal fees, property valuation costs, building inspection charges, Lenders Mortgage Insurance (LMI), and application fees, which can add significantly to upfront costs.