Interest-only loans have a reputation for being risky, but that reputation is not always deserved. For many Kiwi homebuyers navigating New Zealand’s demanding property market, an interest-only structure can be a genuinely smart tool, particularly when cash flow is tight and you need breathing room in the early years of ownership. Whether you’re a first-home buyer stretching to get into the market or an investor looking to maximise returns, understanding how these loans work could reveal options you hadn’t considered. This guide walks you through the mechanics, the trade-offs, and how to decide if an interest-only loan fits your goals.

Table of Contents

- What is an interest-only loan?

- Interest-only vs principal and interest loans: What’s the difference?

- How do interest-only repayments actually work?

- Pros and cons of interest-only loans in New Zealand

- Who are interest-only loans best suited for?

- Risks and how to manage them

- How to apply for an interest-only loan in New Zealand

- Get expert help with your loan choices

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Lower initial payments | Interest-only loans offer the benefit of reduced repayments early on, making home ownership or investment more accessible. |

| Key risks to plan for | Be ready for higher payments later and sketch out a clear repayment strategy from the start. |

| Best fit for certain buyers | These loans mostly suit investors and buyers expecting income or property value growth. |

| Expert advice is essential | Consulting a mortgage adviser can help you avoid common mistakes and find the right loan for your needs. |

What is an interest-only loan?

An interest-only loan is exactly what it sounds like. For a set period, usually between one and five years, you pay only the interest charged on your loan balance. The principal, meaning the actual amount you borrowed, stays the same throughout that period. You’re not chipping away at the debt itself, just covering the cost of borrowing it.

As noted by specialist lenders in New Zealand, interest-only loans allow borrowers to pay just the interest for the initial period, which keeps monthly repayments noticeably lower. Once the interest-only term ends, your loan reverts to a standard principal and interest structure, and your repayments increase accordingly.

These loans are available from a range of sources, including major banks, non-bank lenders, and specialist providers. You can explore the full range of mortgage repayment types to see how interest-only fits alongside other structures.

Common uses include:

- First-home buyers who need lower initial repayments to manage living costs while settling in

- Property investors who want to maximise monthly cash flow

- Borrowers with irregular income who benefit from payment flexibility

- Those planning to sell or refinance before the interest-only period ends

An interest-only loan is not a shortcut or a workaround. Used with a clear plan, it is a legitimate financial tool that suits specific situations very well.

Now that you know what an interest-only loan is, let’s look at how they differ from principal and interest loans.

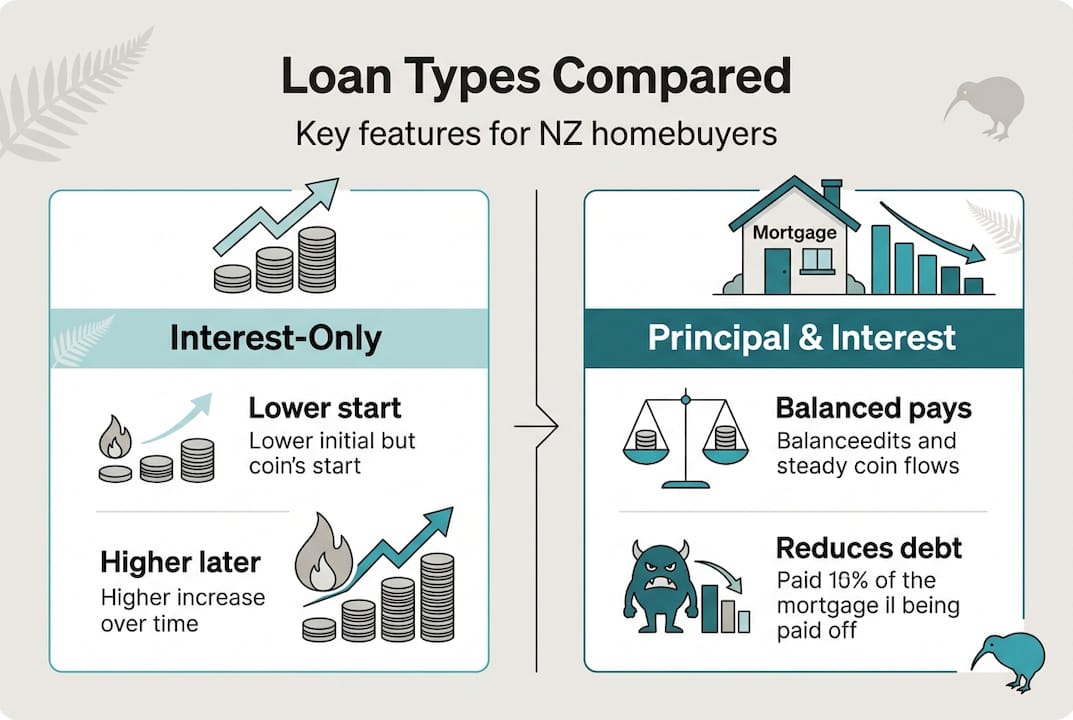

Interest-only vs principal and interest loans: What’s the difference?

The core difference is straightforward. With a principal and interest loan, every repayment reduces your debt and covers the interest charged. With an interest-only loan, your repayments during the initial period cover only the interest, so your debt balance stays flat.

Here’s a quick comparison to make this concrete:

| Feature | Interest-only loan | Principal and interest loan |

|---|---|---|

| Monthly repayments (initial period) | Lower | Higher |

| Debt reduction during initial period | None | Yes, from day one |

| Total interest paid over loan life | Higher | Lower |

| Equity growth in early years | Slower | Faster |

| Flexibility for cash flow | Greater | Less |

As shown when calculating mortgage repayments, interest-only repayments typically result in lower payments during the interest-only period but can increase sharply after. This is a critical point many borrowers overlook when comparing loan types.

The long-term cost difference matters too. Because you’re not reducing the principal during the interest-only period, you pay interest on a larger balance for longer. Over a 30-year loan, this can add tens of thousands of dollars to your total repayment.

Key differences at a glance:

- Interest-only loans offer lower short-term repayments but higher long-term costs

- Principal and interest loans build equity faster and cost less overall

- Interest-only loans suit borrowers with a clear strategy for the post-interest-only period

- Principal and interest loans suit borrowers focused on long-term wealth building through equity

Pro Tip: If you’re comparing both options, run the numbers over the full loan term, not just the first few years. The difference in total interest paid can be significant.

Understanding the differences is key, but how do interest-only repayments work in practice?

How do interest-only repayments actually work?

Let’s make this real with a practical example. Suppose you borrow $800,000 at a 5% annual interest rate, with an interest-only period of five years.

During the interest-only period, your monthly repayment is calculated simply:

- Take your loan balance: $800,000

- Multiply by the annual interest rate: 5% = $40,000 per year

- Divide by 12 months: $3,333 per month

After five years, the loan reverts to principal and interest. Now you’re repaying the full $800,000 over the remaining 25 years at the same rate. Your monthly repayment jumps to approximately $4,678. That’s an increase of over $1,300 per month.

| Loan phase | Monthly repayment | Principal balance |

|---|---|---|

| Interest-only (years 1 to 5) | $3,333 | $800,000 (unchanged) |

| Principal and interest (years 6 to 30) | ~$4,678 | Reducing each month |

As the mortgage calculator at Mortgage Managers illustrates, you pay just the interest on the outstanding balance for a set period, keeping repayments lower until the interest-only term ends. The jump in repayments when that term ends is sometimes called “payment shock,” and it catches borrowers off guard if they haven’t planned for it.

This is why having a clear exit strategy before you take out an interest-only loan is so important. Know what your repayments will look like after the interest-only period, and make sure your income can support them.

Now that the mechanics are clear, let’s explore the pros and cons.

Pros and cons of interest-only loans in New Zealand

Every financial product has trade-offs, and interest-only loans are no exception. Here’s an honest look at both sides.

Benefits:

- Lower monthly repayments during the interest-only period free up cash for other expenses

- Greater flexibility for investors who want to direct funds into property improvements or other investments

- Useful buffer for first-home buyers adjusting to the costs of homeownership

- Can improve short-term cash flow while property values (hopefully) appreciate

Drawbacks:

- You build no equity during the interest-only period, which limits your financial flexibility

- Total interest paid over the life of the loan is higher

- If property values fall, you could owe more than your home is worth

- Banks in New Zealand apply stricter criteria for interest-only applications, particularly post-2021 regulatory changes

As highlighted in analysis of the impact of interest rates in New Zealand, interest-only loans can ease financial pressure but carry risks if property values fall or borrowers can’t switch to principal and interest later. This is a real concern in a market where values can shift quickly.

The New Zealand lending environment has tightened considerably. Banks now scrutinise interest-only applications more carefully, and not every borrower will qualify.

Pro Tip: Before committing to an interest-only loan, speak with a qualified mortgage adviser. Using a mortgage adviser gives you access to a broader range of lenders and helps you assess whether this structure genuinely suits your situation.

Given these benefits and risks, which Kiwi buyers tend to use interest-only loans and why?

Who are interest-only loans best suited for?

Not every borrower benefits equally from an interest-only structure. These loans tend to work best for specific situations.

- Property investors are the most common users. Investors use interest-only loans to maximise cash flow or redirect funds into property improvements, making the lower repayments a strategic advantage rather than a temporary fix. You can read more about property investment loan basics to understand how this fits into a broader investment strategy.

- First-home buyers who are stretching their budget to enter the market may benefit from the lower initial repayments, giving them time to stabilise their finances before repayments increase.

- Self-employed borrowers with variable income often appreciate the flexibility, as lower required repayments reduce pressure during slower income periods.

- Borrowers with a clear exit plan, such as those intending to sell or refinance within five years, can use the interest-only period strategically without being exposed to the long-term cost disadvantage. Explore more about unlocking property investment to see how this plays out in practice.

Of course, using this loan successfully means knowing the main risks and how to manage them.

Risks and how to manage them

Going in with open eyes is the best protection. Here are the four main risks and practical ways to address each one.

- Higher repayments after the interest-only period. Many borrowers underestimate the jump in payments when moving to principal and interest, and some face difficulty refinancing. Budget for the higher repayment from day one, not just when it arrives.

- Property value doesn’t grow as expected. If values stagnate or fall, you may find yourself with little equity and limited options. Maintain a financial buffer and review your position annually.

- Tighter lending restrictions at refinancing time. Lender criteria can change. What qualifies you today may not qualify you in five years. Have a back-up plan and keep your credit profile strong.

- Reduced equity limits future flexibility. Less equity means less borrowing power for future purchases or renovations. Factor this into your long-term property plans.

Pro Tip: If you’re wondering whether a student loan or other existing debt affects your ability to qualify, check out the guidance on student loan and mortgage qualification to understand how lenders assess your full financial picture.

For those ready to explore or apply for interest-only loans, what’s the process?

How to apply for an interest-only loan in New Zealand

Applying for an interest-only loan follows a similar process to any mortgage application, but with a few additional considerations.

- Assess your eligibility. Lenders will look at your income, employment type, credit history, and the property you’re purchasing. Investment properties and owner-occupied homes may be assessed differently.

- Prepare a strong application. Show a clear budget that demonstrates you can manage the higher repayments after the interest-only period ends. An exit strategy, whether that’s refinancing, selling, or switching to principal and interest, strengthens your case considerably.

- Work with a mortgage adviser. A broker can match you with lenders who are most likely to approve your application and on the best terms. As alternative lenders become more active in this space, having expert guidance helps you access options beyond the main banks.

- Gather your documents. Expect to provide recent payslips or tax returns, bank statements, identification, and details of any existing debts or liabilities.

- Allow for assessment time. Lenders will expect strong evidence of income, a sound plan for switching to principal payments, and may apply stricter approval criteria on interest-only applications. Build in extra time for this process.

To bring everything together, let’s recap the most critical points before you make your decision.

Get expert help with your loan choices

Navigating interest-only loans on your own can feel like reading a map without a compass. The structure, the risks, the lender criteria, and the long-term implications all need to be weighed carefully against your personal situation. That’s where professional guidance becomes your greatest asset.

At Mortgage Managers, our team of experienced expert mortgage advisers based in Hobsonville works with homebuyers and investors across Auckland, the North Shore, West Auckland, and remotely throughout New Zealand. We compare interest-only and principal and interest options across a wide panel of lenders, so you get the structure that genuinely fits your goals. If you’re ready to take the next step, get mortgage advice from our team today and let us help you build a strategy that works for your situation.

Frequently asked questions

Can first-home buyers in New Zealand get interest-only loans?

Yes, some banks and lenders offer interest-only loans to first-home buyers, though approval criteria may be stricter than for standard principal and interest applications.

How long can I keep my mortgage interest-only?

Interest-only terms in New Zealand are usually between one and five years, after which the loan reverts to principal and interest repayments.

What happens at the end of the interest-only period?

Your loan automatically switches to principal and interest repayments. As shown when repayments rise after the interest-only period ends, the increase can be substantial, so planning ahead is essential.

Do interest-only loans cost more overall?

Yes. Because you’re not reducing the principal during the interest-only period, interest-only loans incur higher overall interest costs compared to principal and interest loans from the start.

Can I refinance an interest-only mortgage to another lender?

Yes, refinancing is possible, but your ability to do so will depend on your equity position, credit history, and the lender policies in place at the time you apply.