Many first home buyers treat credit assessment like a locked door with no key. The truth is, it’s more like a checklist, and once you understand what’s on it, you can start ticking boxes well before you ever sit down with a lender. In 2025, New Zealand’s lending environment has evolved, with tighter responsible lending rules and more thorough documentation requirements than ever before. This guide walks you through exactly how credit assessment works, what lenders are looking for, and the practical steps you can take right now to put your best foot forward.

Table of Contents

- What is credit assessment and why does it matter for first home buyers?

- How does credit assessment work in 2025? Key factors considered by lenders

- Common misconceptions about mortgage credit checks

- Comparing lending options: banks vs non-bank lenders in 2025

- How to prepare for your credit assessment: practical steps for New Zealand home buyers

- Ready to take the next step with Mortgage Managers?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Credit assessment is predictable | Understanding the lender’s criteria allows you to take steps to meet them. |

| Preparation boosts approval odds | Gathering the right documents and cleaning up your credit history pays off. |

| Lender choices impact your options | Banks are stricter but cheaper; non-banks are flexible for complex situations. |

| Expert advice is valuable | Mortgage advisers can flag issues and help you secure approval. |

What is credit assessment and why does it matter for first home buyers?

Credit assessment is the process lenders use to decide whether to offer you a mortgage, and on what terms. Think of it as your financial report card. It tells the lender whether you’re a reliable borrower, whether you can afford the repayments, and whether lending to you is a responsible decision under New Zealand law.

For first home buyers, this process can feel intimidating because it touches nearly every part of your financial life. But understanding it removes the mystery. The approval process explained covers the full journey from application to settlement, and credit assessment sits right at the heart of it.

Here’s what lenders typically examine during credit assessment:

- Credit score and credit history: Your track record of repaying debts on time

- Income type and stability: Whether you’re salaried, self-employed, or on a variable income

- Existing debts and liabilities: Personal loans, credit cards, student loans, and hire purchase agreements

- Monthly living expenses: Your actual spending habits, not just your estimates

- Savings history and deposit size: Evidence that you can manage money consistently

- Account conduct: How you manage your bank accounts day to day

“Credit assessment is a crucial step in the mortgage approval process for New Zealanders.”

Each of these factors paints a picture of you as a borrower. No single factor automatically disqualifies you, but together they tell a story. Your job is to make that story as strong as possible.

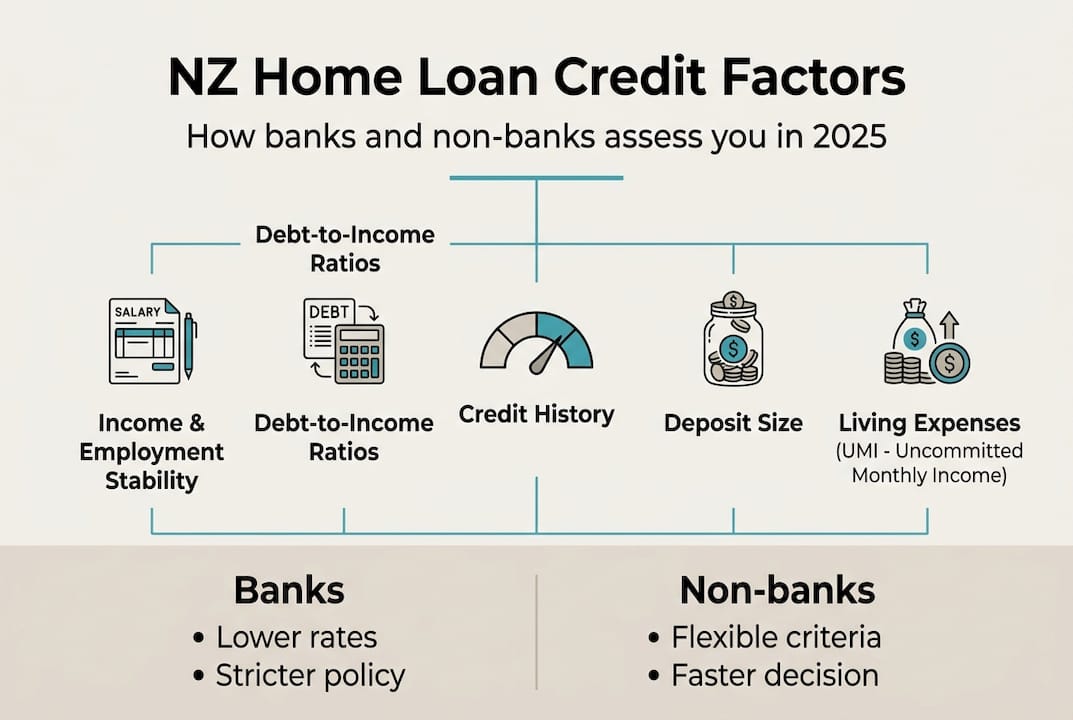

How does credit assessment work in 2025? Key factors considered by lenders

With that big-picture understanding, let’s look specifically at what New Zealand lenders focus on for home loans in 2025. The regulatory environment has shifted, and lenders are now required to apply stricter serviceability tests. Serviceability simply means: can you realistically afford this loan over the long term, even if interest rates rise?

Lenders evaluate income, expenses, liabilities, deposit size, and credit history to decide on a home loan. Here’s how each factor ranks in terms of impact:

| Assessment factor | Impact level | What lenders look for |

|---|---|---|

| Credit score | High | Score above 650 preferred by major banks |

| Debt-to-income ratio | High | Total debts vs gross annual income |

| Employment stability | High | Minimum 3-6 months in current role |

| Savings history | Medium | Genuine savings over 3+ months |

| Monthly expenses | Medium | Actual bank statement spending |

| Deposit amount | High | Minimum 10-20% of property value |

| Income type | Medium | Salaried preferred; self-employed needs 2 years of accounts |

Here’s a numbered breakdown of how lenders typically work through your application:

- Pull your credit report from a New Zealand credit bureau such as Centrix or Equifax

- Verify your income using payslips, tax returns, or financial statements

- Analyse your expenses by reviewing three to six months of bank statements

- Calculate your debt-to-income ratio to assess overall financial pressure

- Assess your deposit and confirm it meets their loan-to-value ratio requirements

- Make a lending decision based on their internal credit policy

If your credit history has some rough patches, it’s worth rebuilding your credit before you apply. Small, consistent improvements over six to twelve months can make a meaningful difference to your outcome. You can also explore mortgage eligibility tips tailored specifically for Auckland first home buyers.

Pro Tip: Request a free copy of your credit report at least six months before you plan to apply. Errors on credit reports are more common than people realise, and fixing them early gives you time to dispute inaccuracies without delaying your application.

Common misconceptions about mortgage credit checks

Understanding common misconceptions can help buyers prepare with confidence. Let’s clear up some of the most persistent myths that cause unnecessary anxiety.

Many buyers believe that poor credit means automatic rejection, but there are genuine ways to improve your eligibility and find a lender suited to your situation. Here are the myths worth setting aside:

- Myth: One missed payment ruins everything. A single late payment is far less damaging than a pattern of missed payments. Recency, frequency, and the size of the default all matter.

- Myth: Being rejected by one bank means all banks will say no. Different lenders have different credit policies. A rejection from one institution doesn’t close every door.

- Myth: Your credit score is fixed. Credit scores change over time. Responsible behaviour, paying down debts, and avoiding new credit applications all improve your score gradually.

- Myth: Lenders only care about your income. Income is important, but lenders weigh it against your expenses, debts, and overall financial behaviour.

“A rejection isn’t a verdict on your future. It’s a signal to understand what needs to change and who can help you get there.”

It’s also worth knowing that responsible lending laws in New Zealand mean some rejections are actually designed to protect you. If a lender declines your application because the repayments would stretch you too thin, that’s the system working as intended. Understanding common rejection reasons helps you address them directly rather than feeling defeated.

Comparing lending options: banks vs non-bank lenders in 2025

One of the most important choices for home buyers is which type of lender to approach. Here’s how major options compare in 2025.

| Feature | Banks | Non-bank lenders |

|---|---|---|

| Interest rates | Lower | Higher |

| Credit flexibility | Stricter | More flexible |

| Documentation required | Extensive | Moderate |

| Approval speed | Slower | Often faster |

| Best suited for | Strong credit profiles | Complex or imperfect credit |

Non-bank lenders can be more flexible on credit criteria, sometimes approving buyers that banks will not. This flexibility comes at a cost, typically a higher interest rate, but it can be a genuine stepping stone for buyers who need time to strengthen their financial position.

Here’s a quick summary of what each lender type offers:

- Banks: Competitive rates, strict criteria, best for buyers with stable employment and clean credit

- Non-bank lenders: Higher rates, flexible criteria, suited to self-employed buyers or those with past credit issues

- Credit unions and building societies: Member-focused, sometimes more lenient, worth exploring as an alternative

Understanding NZ responsible lending rules helps you see why lenders set the criteria they do. It’s not arbitrary. It’s designed to ensure you can sustain your mortgage without financial hardship.

Pro Tip: Never apply to multiple lenders at the same time without guidance. Each application triggers a credit enquiry, and too many enquiries in a short period can lower your credit score and raise red flags for future lenders.

How to prepare for your credit assessment: practical steps for New Zealand home buyers

Once you know the standards lenders apply, preparation is key. Here’s a checklist to help you get ready and stand out as a strong applicant.

Actively preparing your documents, building your deposit, and checking your credit before application genuinely boosts your chance of mortgage approval. Follow these steps in order:

- Get your credit report from Centrix, Equifax, or Illion and review it carefully for errors

- Gather your documents including three months of payslips, six months of bank statements, photo ID, and a list of all current debts

- Pay down small debts such as credit card balances and buy-now-pay-later accounts before applying

- Avoid new credit applications in the three to six months before you apply for a mortgage

- Build genuine savings by setting aside a consistent amount each month, even if it’s modest

- Reduce discretionary spending in the months before application so your bank statements reflect responsible habits

- Speak with a mortgage adviser early to get a realistic picture of where you stand and what needs attention

The mortgage management in 2025 landscape rewards buyers who prepare early. Lenders respond well to applicants who arrive organised, informed, and with a clear financial story to tell.

Pro Tip: A mortgage adviser can review your credit position before you apply and identify issues you might not even know exist. This early review can save you from a rejection that stays on your credit file.

Ready to take the next step with Mortgage Managers?

Understanding credit assessment is empowering, but knowing what to do with that knowledge is where a trusted adviser becomes your greatest asset. At Mortgage Managers, we work with first home buyers across Auckland, West Auckland, the North Shore, and throughout New Zealand to make the mortgage process feel manageable rather than overwhelming.

We take the time to review your full financial picture, match you with the right lender for your situation, and guide you through every stage of the approval process. Whether your credit history is spotless or has a few bumps, we’re here to help you find a path forward. Reach out to our team at Mortgage Managers and let’s start the conversation today.

Frequently asked questions

What credit score do I need for a first home loan in New Zealand in 2025?

Most major banks prefer a credit score above 650, but non-bank lenders may approve buyers with lower scores depending on the overall strength of their application.

Does student loan debt hurt my mortgage chances?

Student loans affect your overall serviceability calculation, but they don’t automatically disqualify you. Lenders consider overall income, debts, and expenses together as a complete financial picture.

How long does the credit assessment process take for a mortgage?

Most lenders complete their assessment within 3 to 10 business days, provided all documents are in order. Assessment timeframes depend heavily on how complete and organised your application is.

Can I get a mortgage after a recent default or missed payment?

Yes, it’s possible. You may need a larger deposit and a stronger overall application. Recent defaults can be overcome with the right strategy and expert guidance from a mortgage adviser.

Should I use a mortgage adviser to help with credit assessment?

Absolutely. A mortgage adviser matches your situation to the right lender, reviews your credit position before you apply, and significantly improves your odds of approval. Expert mortgage advisers make the entire process smoother and less stressful.