Securing your first home loan in New Zealand can feel overwhelming, especially when you’re working with limited savings or facing credit challenges. Many first-time buyers struggle to meet deposit requirements and worry about their credit history affecting approval chances. This comprehensive guide walks you through the entire first home loan process in 2026, including government assistance programmes like the Kāinga Ora First Home Loan, practical preparation strategies, and expert tips to strengthen your application. Whether you’re dealing with bad credit or simply need clarity on the steps ahead, you’ll discover actionable solutions to turn homeownership into reality.

Table of Contents

- Understanding The First Home Loan Landscape In New Zealand

- Preparing Your Application For First Home Loan Success

- Step-By-Step Guide To Applying For Your First Home Loan

- Common Challenges And Expert Tips For Securing Your First Home Loan

- How Expert Mortgage Advisers Can Help You Secure Your First Home Loan

- What Is The Kāinga Ora First Home Loan?

- Can You Get A Home Loan With Bad Credit In New Zealand?

- How Much Deposit Is Needed For A First Home Loan In 2026?

- What Documents Are Needed To Apply For A First Home Loan?

Key takeaways

| Point | Details |

|---|---|

| Low deposit options | Government schemes reduce deposit requirements to as low as 5% for eligible first-time buyers |

| Eligibility factors | Lenders assess income, credit history, existing debt, and employment status when reviewing applications |

| Preparation matters | Starting good financial habits six months before applying significantly improves approval chances |

| Expert guidance helps | Mortgage advisers navigate complex situations and connect buyers with suitable lender options |

Understanding the first home loan landscape in New Zealand

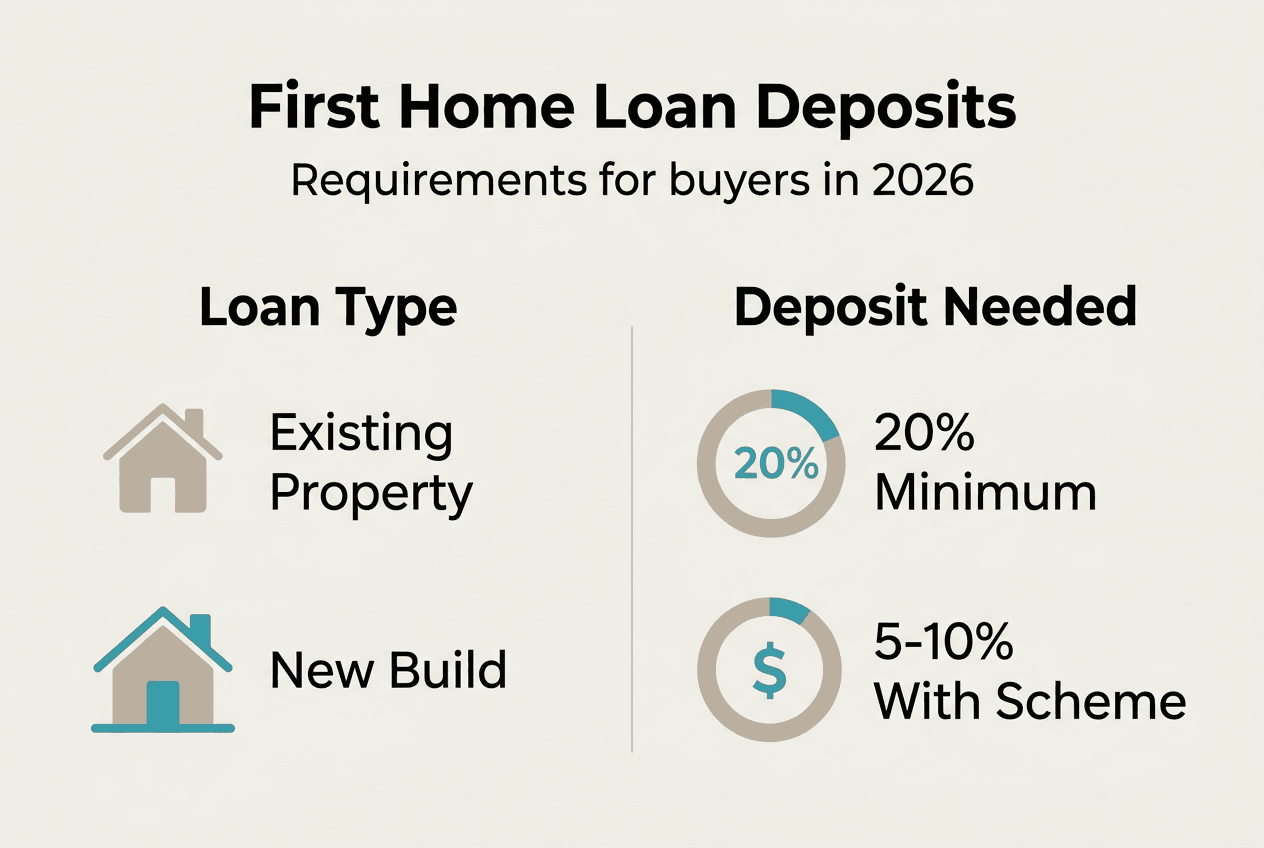

The New Zealand property market presents unique challenges for first-time buyers, but understanding your options makes the journey manageable. Traditional lenders typically require deposits ranging from 10% to 20% of the property’s purchase price, which can create a significant barrier for many aspiring homeowners. However, the Kāinga Ora First Home Loan allows buyers to purchase with a 5% deposit, dramatically lowering the entry threshold.

This government-backed programme works by having Kāinga Ora underwrite up to 15% of the loan, reducing the lender’s risk and making approval more accessible. The loan functions as a standard mortgage with market interest rates, not as a grant or subsidy. You’ll repay the full amount over the agreed term, just like any other home loan. Recent changes removed previous house price caps, expanding your property options significantly across all regions.

Eligibility for the Kāinga Ora First Home Loan requires meeting specific criteria:

- New Zealand citizenship, permanent residency, or resident visa holder status

- No previous property ownership in New Zealand or overseas

- Income limits that vary based on household size and location

- Minimum age of 18 years

- Intention to occupy the property as your primary residence

Deposit requirements vary across different loan types. Existing properties often require 20%, new homes 10%, and the First Home Loan scheme just 5%. Understanding these thresholds helps you set realistic savings goals and choose the right pathway for your circumstances.

| Loan type | Minimum deposit | Government backing |

|---|---|---|

| Standard existing property | 20% | No |

| New build standard | 10% | No |

| Kāinga Ora First Home Loan | 5% | Yes, up to 15% |

| Welcome Home Loan | 5-10% | Yes, partial |

Pro Tip: Focus your property search on new builds or properties eligible under government schemes if you’re working with a smaller deposit. These options provide more flexibility and often come with additional buyer protections.

The Kāinga Ora official site provides detailed information about current income limits and property requirements. These thresholds adjust periodically, so checking the latest figures ensures you’re working with accurate eligibility data when planning your application.

Preparing your application for first home loan success

Lenders evaluate multiple factors when assessing your home loan application, and understanding these criteria helps you prepare effectively. Income, expenses, consumer debt, credit record, and employment status all play crucial roles in determining your borrowing capacity and approval likelihood. Taking proactive steps at least six months before applying gives you time to strengthen weak areas and present your finances in the best possible light.

Your credit score significantly impacts lender decisions. Understanding your credit score helps you assess your mortgage prospects realistically and identify areas needing improvement. New Zealand credit scores range up to 1000, with higher scores indicating lower lending risk. You can request a free credit report annually to check for errors or issues requiring attention.

Consumer debt reduces your borrowing capacity substantially because lenders factor these ongoing commitments into their serviceability calculations. Credit cards, personal loans, car finance, and buy-now-pay-later arrangements all count against you. Paying down these debts before applying increases the amount lenders will approve and demonstrates financial responsibility.

Start implementing these preparation strategies immediately:

- Review your credit report and dispute any errors or outdated information

- Reduce discretionary spending and redirect funds towards deposit savings

- Close unused credit cards and reduce limits on cards you keep

- Maintain steady employment and avoid job changes during the application period

- Create a detailed budget tracking all income and expenses

- Gather documentation including payslips, bank statements, and tax returns

Pro Tip: Set up automatic transfers to a dedicated savings account immediately after each payday. This “pay yourself first” approach builds your deposit consistently without requiring constant willpower or decision-making.

Documentation requirements seem overwhelming initially, but organising everything early prevents delays later. Lenders typically request three to six months of bank statements, recent payslips, proof of deposit funds, identification documents, and explanations for any unusual transactions. Having these materials ready demonstrates preparedness and professionalism.

If you’re self-employed, expect additional scrutiny and documentation requirements. Lenders usually want two years of financial statements and tax returns to verify income stability. Working with a mortgage adviser who understands how to improve home loan eligibility in complex situations provides valuable guidance through this process.

Consider consulting resources like the bad credit home loan checklist if you’re concerned about past financial difficulties. Many buyers successfully secure financing despite previous challenges by demonstrating current financial stability and providing context for past issues. Transparency with lenders about your situation typically produces better outcomes than attempting to hide problems.

Taking time to prepare for a home loan properly positions you for success and reduces stress during the application process. The effort invested in preparation often determines whether your application receives quick approval or faces delays and complications.

Step-by-step guide to applying for your first home loan

Following a structured application process increases your approval chances and helps you avoid common mistakes. This systematic approach ensures you address all lender requirements and present your application professionally.

-

Confirm your eligibility for your chosen loan programme. Applicants must be a New Zealand citizen, permanent resident, or resident visa holder ordinarily resident in NZ and over 18 years old. Verify you meet income limits and haven’t previously owned property if applying through Kāinga Ora.

-

Gather all required documentation before starting your application. This includes proof of identity such as passport or driver’s licence, recent payslips or financial statements, bank statements covering three to six months, evidence of deposit savings, details of existing debts and commitments, and credit history information.

-

Research and compare lenders offering first home loans. Different institutions have varying criteria, interest rates, and fees. The Kāinga Ora programme removes previous house price caps, allowing you to target properties anywhere provided you meet other requirements. Standard banks, credit unions, and specialist lenders each offer different advantages depending on your circumstances.

-

Consider working with a mortgage adviser who can compare options across multiple lenders simultaneously. Advisers often access better rates and know which lenders suit specific situations, including complex cases involving bad credit or irregular income.

-

Submit your application with complete documentation. Missing information causes delays and creates negative impressions with lenders. Double-check everything before submission to ensure accuracy and completeness.

-

Respond promptly to any lender queries or requests for additional information. Quick, thorough responses demonstrate your commitment and keep the process moving forward efficiently.

-

Review the loan offer carefully before accepting. Understand the interest rate type, repayment terms, fees, and any special conditions attached to your approval.

| Application stage | Typical timeframe | Key actions |

|---|---|---|

| Documentation gathering | 2-4 weeks | Collect payslips, statements, ID |

| Lender comparison | 1-2 weeks | Research rates and terms |

| Application submission | 1-3 days | Complete forms, attach documents |

| Lender assessment | 1-3 weeks | Respond to queries promptly |

| Conditional approval | 3-7 days | Review and accept offer |

| Final approval | 1-2 weeks | Complete property checks |

Pro Tip: Apply for pre-approval before house hunting. This confirms your borrowing capacity and demonstrates to sellers that you’re a serious buyer with financing already arranged, strengthening your negotiating position.

The home loan checklist provides additional detail on each stage and helps you track progress through the application journey. Staying organised and methodical prevents oversights that could derail your application.

Understanding Kāinga Ora loan requirements thoroughly before applying saves time and prevents disappointment. The official requirements outline income thresholds, property criteria, and other eligibility factors that determine whether you qualify for this valuable programme.

Common challenges and expert tips for securing your first home loan

Many first-time buyers encounter obstacles during the application process, but understanding these challenges helps you prepare effective solutions. Bad credit represents one of the most common concerns, yet first-time homebuyers with bad credit can still secure a mortgage with a strong strategy and expert advice. The key lies in demonstrating current financial stability and providing context for past difficulties.

Credit issues affect approval prospects but don’t automatically disqualify you from homeownership. Over 1 in 10 Kiwis face mortgage rejection due to poor credit, highlighting how common this challenge is. Lenders want to see evidence that you’ve addressed the underlying problems and established better financial habits.

Working with mortgage brokers for complicated mortgages opens doors to specialist lenders who consider applications that mainstream banks might decline. These brokers understand which lenders accept specific situations and how to present your application most favourably. Their expertise proves invaluable when you’re dealing with non-standard circumstances.

Common pitfalls to avoid include:

- Applying for new credit during the mortgage application process

- Making large unexplained deposits that raise money laundering concerns

- Changing jobs or reducing income before settlement

- Failing to disclose existing debts or financial commitments

- Underestimating ongoing property costs in your budget

Transparency with lenders produces better outcomes than attempting to hide problems. If you’ve experienced bankruptcy, defaults, or other credit issues, provide clear explanations showing what caused the problems and how you’ve resolved them. Lenders appreciate honesty and often work with borrowers who demonstrate genuine efforts to improve their financial situation.

“The difference between approval and rejection often comes down to preparation and presentation. Buyers who take time to understand lender requirements and address weak areas before applying consistently achieve better outcomes than those who rush the process.”

Pro Tip: If you’ve had credit problems, wait at least six months after resolving them before applying for a mortgage. This gap demonstrates sustained improvement and gives you time to establish positive payment patterns that strengthen your application.

Reducing discretionary spending before applying shows lenders you can manage mortgage repayments comfortably. Review your bank statements from a lender’s perspective and eliminate or reduce expenses that suggest poor financial discipline. Subscription services, gambling, excessive dining out, and frequent cash withdrawals all raise concerns during assessment.

Implementing first home buyer tips from experienced professionals helps you avoid mistakes and navigate the process more smoothly. These strategies reflect lessons learned from thousands of successful applications and provide practical guidance for real-world situations.

Understanding that challenges are normal and usually surmountable helps maintain perspective during difficult moments. Almost every first-time buyer faces some obstacle during their journey to homeownership. The difference between success and failure often lies in persistence, preparation, and willingness to seek expert guidance when needed.

Consult mortgage approval tips for bad credit if credit issues concern you. These resources provide specific strategies for strengthening applications despite past financial difficulties and help you understand what lenders look for when assessing risk.

How expert mortgage advisers can help you secure your first home loan

Navigating the first home loan process becomes significantly easier with professional guidance from experienced mortgage advisers. These specialists understand current lender criteria, government programmes like Kāinga Ora, and how to present applications for maximum approval chances. They act as personal shoppers for your home loan, comparing options across multiple lenders to find the best fit for your unique circumstances.

Mortgage advisers prove especially valuable when you’re dealing with complex situations like bad credit, irregular income, or limited deposit savings. They know which lenders consider non-standard applications and how to structure your documentation to address potential concerns proactively. This expertise often means the difference between approval and rejection for buyers with challenging circumstances.

Working with Auckland mortgage brokers provides local market knowledge and connections with lenders active in your area. They understand regional property trends, pricing dynamics, and which programmes offer the best value for first-time buyers in specific locations. Understanding the role of a mortgage adviser helps you maximise the value of this professional relationship and ensures you’re asking the right questions throughout the process.

What is the Kāinga Ora First Home Loan?

The Kāinga Ora First Home Loan is a government-backed lending programme helping first-time buyers purchase property with just a 5% deposit. Kāinga Ora underwrites up to 15% of the loan value, reducing the lender’s risk and making approval more accessible for buyers who meet eligibility criteria. The loan carries standard market interest rates and repayment terms, functioning like a traditional mortgage rather than a grant or subsidy.

Can you get a home loan with bad credit in New Zealand?

Yes, securing a home loan with bad credit is possible when you take the right approach and seek expert guidance. Mortgage brokers can connect you with specialist lenders who consider applications from buyers with credit challenges, provided you demonstrate current financial stability. Following a comprehensive bad credit home loan checklist improves your chances by addressing potential concerns before lenders identify them.

How much deposit is needed for a first home loan in 2026?

Deposit requirements vary from 5% under the Kāinga Ora programme to 20% for standard existing property loans. New build properties typically require a 10% deposit through conventional lending channels. Your specific circumstances, chosen property type, and selected lender determine which deposit level applies to your situation.

What documents are needed to apply for a first home loan?

Essential documentation includes proof of identity like passport or driver’s licence, recent payslips or financial statements, bank statements covering three to six months, evidence of deposit savings, and details of existing debts. Having these documents ready before applying speeds up the assessment process and demonstrates preparedness to lenders. Additional documentation may be required depending on your employment type and specific lender requirements.