TL;DR:

- Many Auckland first-time buyers now use deposits below 20% thanks to relaxed LVR rules in 2026.

- Preparing your credit report and understanding low deposit options early can significantly improve approval chances.

- Working with a mortgage adviser helps navigate complex credit issues and access tailored lending solutions.

Buying your first home in Auckland is one of the biggest financial decisions you’ll ever make, and the obstacles can feel enormous before you’ve even started. With median house prices sitting near $885,000 and strict credit checks standing between you and approval, it’s easy to feel like the goalposts keep moving. The good news is that more first-time buyers than ever are finding a way through, even with smaller deposits and imperfect credit histories. This guide walks you through the exact workflow, the real numbers, and the practical strategies that are helping Auckland buyers get across the line in 2026.

Table of Contents

- Understanding your starting point: Deposits, prices, and credit checks

- Step-by-step first-time buyer workflow in Auckland

- Low deposit strategies for Auckland’s first-time buyers

- Overcoming credit challenges: Getting approved when your record isn’t perfect

- Why the classic advice misses what matters in Auckland’s market

- How expert mortgage advisers help first-time buyers succeed

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Most buyers use low deposits | Over half of Auckland first-home buyers succeed with less than 20% saved upfront. |

| Strict credit checks | Lenders scrutinise credit history, but specialist options exist for buyers with blemishes. |

| Step-by-step workflow matters | Following a clear process boosts approval odds and reduces stress at every stage. |

| Expert help is a game-changer | Mortgage advisers open up more lender choices and smooth out challenges for first-timers. |

Understanding your starting point: Deposits, prices, and credit checks

Having set the scene, let’s break down exactly what you’ll need to get started. The first thing most buyers discover is that the traditional 20% deposit benchmark feels almost impossible in Auckland’s market. The Auckland median house price sits around $885,000, which means a 20% deposit alone would require $177,000 in savings. That’s a significant barrier for most people starting out.

Here’s what makes 2026 different from previous years. A record 57% of new first-home buyer lending in January 2026 was written at over 80% loan-to-value ratio (LVR). In plain terms, the majority of new buyers are now purchasing with deposits below 20%. This is a genuine shift in how the market is operating, and it opens real doors for buyers who have been sitting on the sidelines.

Key deposit benchmarks to know:

- A 5% deposit on an $885,000 home equals roughly $44,250

- A 10% deposit equals roughly $88,500

- Government schemes like the First Home Loan can help with deposits as low as 5%

- Non-bank lenders may accept deposits in the 10% to 15% range where banks won’t

Credit checks are the other major hurdle. Lenders scrutinise your credit history carefully, and the results can surprise you. Research shows that 30% of West Auckland first-home buyers have defaults on their credit record. If you’re in that group, you’re far from alone, but you do need a strategy.

Exploring your low deposit options early gives you a clearer picture of what’s achievable. Equally important is understanding home loan preparation well before you approach a lender. Knowing your credit score, your borrowing capacity, and your deposit position before you start saves weeks of wasted effort.

| Factor | Typical requirement | What to check |

|---|---|---|

| Deposit (bank) | 20% preferred | LVR rules and exceptions |

| Deposit (non-bank) | 10% to 15% | Lender-specific policies |

| Credit score | Good to excellent | Free credit report services |

| Stable income | 2+ years preferred | Payslips, tax returns |

| Debt-to-income ratio | Max 6x income | Total debt vs gross income |

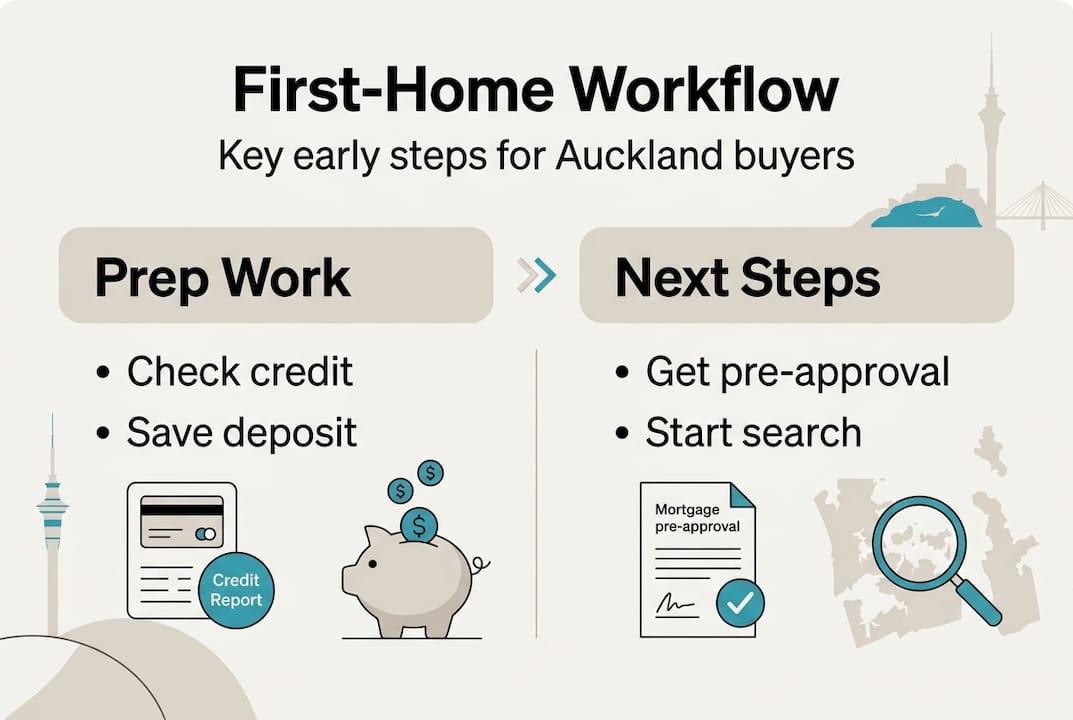

Step-by-step first-time buyer workflow in Auckland

Once you know your position, here’s exactly how to navigate the buying process. There were 23,634 first-home buyer purchases in New Zealand in the past 12 months, with the average buyer aged 36. That tells you this is a process that takes time, and the buyers who succeed are the ones who follow a clear sequence.

- Check your credit report. Get a free copy from a credit bureau like Centrix or Equifax NZ. Identify any defaults, late payments, or errors before a lender does.

- Calculate your borrowing capacity. Use an online calculator or speak with an adviser to understand what your income and deposit will support at current interest rates.

- Gather your documents. Payslips, bank statements, tax returns, and proof of savings are all standard requirements. The full Auckland mortgage application steps guide covers exactly what you need.

- Get pre-approval. This is your financial GPS for house hunting. It tells you your budget and signals to vendors that you’re a serious buyer.

- Find your property and make an offer. Once pre-approved, you can move quickly when the right home appears.

- Formal approval and settlement. Your lender does final checks, and your solicitor handles the settlement process.

Many buyers skip step one and go straight to house hunting. That’s where things unravel. Understanding how to get a mortgage in NZ before you start shopping is the single biggest time-saver in the process.

| Lender type | Deposit needed | Credit flexibility | Rate range |

|---|---|---|---|

| Major bank | 20% (or 10% with scheme) | Low | Competitive |

| Non-bank lender | 10% to 15% | Moderate to high | Slightly higher |

| Mortgage broker | Varies by lender | Highest | Best match found |

Pro Tip: Get your pre-approval sorted before attending open homes. Vendors and agents take pre-approved buyers far more seriously, and you won’t waste time falling in love with a home you can’t finance. Review the home loan process guide to understand each stage in detail.

Low deposit strategies for Auckland’s first-time buyers

Deposit shortfall? Here’s how real buyers are making it work in today’s market. The easing of LVR restrictions in December 2025 has been a genuine turning point. A record 57% of new FHB lending in January 2026 was written above 80% LVR, reflecting how many buyers are now entering the market with smaller deposits than previously possible.

However, the post-LVR easing data also shows rising sensitivity to debt-to-income (DTI) ratios. Lenders are watching how much total debt you carry relative to your income, even when deposit requirements are lower. This is a trade-off worth understanding before you apply.

Your main low deposit pathways:

- First Home Loan (Kāinga Ora backed): Allows a 5% deposit for eligible buyers, with income and purchase price caps applying

- Non-bank lenders: More flexible on deposit and credit, though interest rates are typically higher

- Guarantor loans: A family member uses equity in their home to support your application

- KiwiSaver withdrawal: First-home buyers can withdraw most of their KiwiSaver balance for a deposit

- Welcome Home Loan equivalent products: Some lenders offer similar structures with varying eligibility rules

The low deposit loan options available in 2026 are broader than most buyers realise. The first home buyers guide from Mortgage Managers walks through each pathway with eligibility criteria clearly explained.

Pro Tip: If you’re using a guarantor, make sure both parties get independent legal advice. A guarantor arrangement can accelerate your purchase significantly, but everyone involved needs to understand the obligations clearly before signing anything.

One trade-off to factor in: low deposit loans often attract a Low Equity Premium (LEP), which is an additional charge built into your interest rate. This can add meaningful cost over the life of your loan, so weigh it against the benefit of entering the market sooner rather than waiting years to save a larger deposit.

Overcoming credit challenges: Getting approved when your record isn’t perfect

If your credit isn’t perfect, this section is for you. A less-than-ideal credit history doesn’t automatically close the door on home ownership, but it does mean you need to approach the process differently and with more preparation.

Specialist non-bank lenders exist specifically to assess buyers with defaults, missed payments, or limited credit history. They do charge higher interest rates than the major banks, but for many buyers they represent the only realistic path to approval.

Documents that strengthen your application:

- A current credit report with any errors disputed and corrected

- Written explanations for any defaults or late payments (context genuinely matters)

- Payslips and bank statements showing consistent income over at least three months

- Evidence of regular savings behaviour, even small amounts over time

- A letter from your employer confirming your role and income stability

The order in which you tackle these matters. Start by pulling your credit report and disputing anything inaccurate. Then focus on paying down any outstanding debts before applying. Stable employment history is one of the strongest signals a lender can see.

“For credit issues, focus on explanations and supporting evidence rather than the score number alone. A well-documented application with a clear narrative can shift a lender’s assessment significantly.” — Mortgage approval tips for bad credit New Zealand

A mortgage broker is particularly valuable here. Brokers know which lenders are most receptive to specific credit profiles, and they can match your file to the right institution rather than sending you to a bank that will simply decline you. Review the mortgage application checklist to make sure you’ve covered every requirement. Understanding the features for first-time buyers that different lenders offer can also help you identify where your profile fits best.

Why the classic advice misses what matters in Auckland’s market

Everyone tells first-time buyers to save 20% and fix their credit. It’s sensible advice in theory. In Auckland’s market in 2026, it’s also incomplete. Saving 20% of an $885,000 home takes most people a decade or more, and the market rarely waits that long.

Relying solely on major banks can also quietly exclude genuine buyers. Banks have rigid credit scoring systems that don’t account for the full story behind your financial history. A missed payment from three years ago during a difficult period carries the same weight as a recent default in their models, which isn’t a fair reflection of your current position.

What actually moves the needle is a combination of the right lender match, a well-prepared application, and clear documentation of your circumstances. Auckland’s high prices make the First Home Loan and non-bank options more relevant than ever, and buyers who work with a broker familiar with Auckland’s lender landscape consistently find better outcomes.

An Auckland mortgage adviser who knows the local market isn’t just a convenience. They’re often the difference between an approval and a rejection, especially when your file has complexity.

How expert mortgage advisers help first-time buyers succeed

If you want expert backup at every step, here’s where to start. Auckland’s property market rewards buyers who move with confidence and preparation. Working with a team of advisers who understand the full landscape of lenders, schemes, and credit options gives you a genuine edge.

At Mortgage Managers, we work as your personal mortgage shoppers, comparing lenders across the market to find the best fit for your deposit size, income, and credit profile. Whether you’re dealing with a low deposit, a complicated credit file, or simply don’t know where to begin, our team of expert mortgage advisers is here to guide you. We also specialise in home loan options that the major banks simply don’t offer, giving you access to solutions that match your real situation rather than a standard template.

Frequently asked questions

How much deposit do I need to buy my first home in Auckland?

While 20% is the traditional benchmark, over half of recent first-home buyers purchased with less, using loans above 80% LVR, so a 5% to 10% deposit is a realistic starting point with the right lender or scheme.

Can I buy my first home in Auckland with bad credit?

Yes, specialist non-bank lenders offer options for buyers with defaults or imperfect credit, though you’ll typically pay a higher interest rate and need thorough documentation to support your application.

What steps should I take first when starting the mortgage process?

Start by pulling your credit report and calculating your borrowing capacity, as lenders assess credit history strictly and knowing your position early helps you address any issues before they delay your application.

How do government schemes help first-time buyers in Auckland?

Schemes like the First Home Loan allow a 5% deposit for eligible buyers, but post-LVR easing data shows these lower deposit loans often come with higher costs through Low Equity Premiums, so factor the total repayment into your planning.