TL;DR:

- Using a combination of savings, KiwiSaver, and low-deposit options can help first-time buyers enter the market sooner.

- Preparing all documentation and obtaining pre-approval gives buyers a competitive edge and reduces last-minute stress.

- Delaying homeownership to save a traditional 20% deposit often results in missed opportunities due to rising property prices.

Saving for your first home in New Zealand can feel like running on a treadmill that keeps speeding up. House prices have climbed faster than most incomes, and the gap between where you are today and where you need to be can look overwhelming. But here’s the thing: with the right strategies in your corner, you can close that gap faster than you might think. This guide walks you through every key step, from understanding deposit requirements and making the most of KiwiSaver, to smart savings habits and low-deposit home loan options that could get you across the line sooner.

Table of Contents

- Understanding deposit requirements and home loan basics

- Maximising KiwiSaver for your home deposit

- Smart strategies to boost your deposit savings

- Low-deposit home loan options and their risks

- Getting your paperwork and process right

- What most first home buyers get wrong about deposit building

- How Mortgage Managers can help you on your first home journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| You may only need 5% | It’s possible to buy with as little as a 5% deposit if you qualify for the Kāinga Ora First Home Loan scheme. |

| KiwiSaver is a key tool | Withdrawing from KiwiSaver boosts your deposit, but consider the effect on your retirement savings. |

| Saving smart matters | Automating savings and avoiding unnecessary debt help you grow your deposit faster. |

| Preparation speeds approval | Having your paperwork and legal checks ready makes the home loan process smoother and less stressful. |

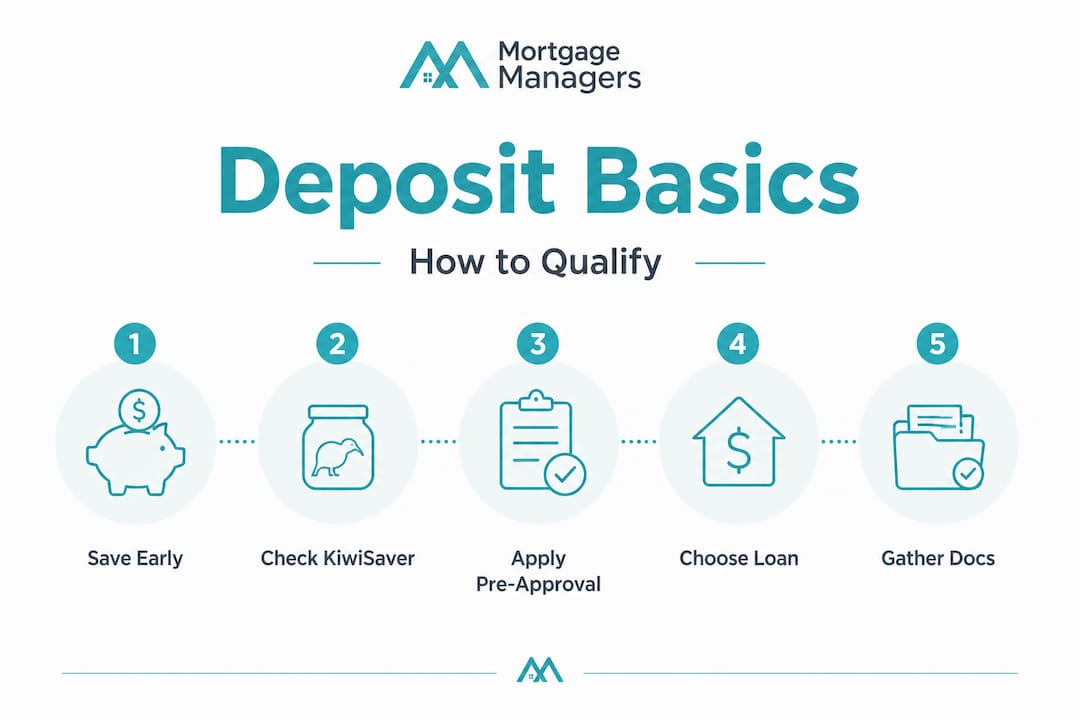

Understanding deposit requirements and home loan basics

Now that you know why a strong deposit matters, let’s break down the basics so you know what you’re aiming for.

Your deposit is the upfront amount you contribute toward the purchase price of a home. Lenders use it to assess how much risk they’re taking on. A larger deposit generally means better interest rates, more lender options, and lower ongoing repayments. For most standard lenders, a deposit of 20% is the benchmark that unlocks the most competitive terms. However, this isn’t the only path forward.

What counts toward your deposit?

Most lenders in New Zealand will accept a combination of the following sources:

- Personal savings held in a bank account for at least three months

- KiwiSaver first-home withdrawal funds (more on this shortly)

- Gifts from immediate family members (with a signed gift letter)

- The First Home Grant from Kāinga Ora (where eligible)

- Equity from a guarantor property (in some cases)

One of the most important options for first home buyers is the Kāinga Ora First Home Loan overview. This scheme allows qualifying buyers to purchase a home with just a 5% deposit, which is a significant reduction from the standard 20%. According to eligibility criteria, Kāinga Ora First Home Loan enables 5% deposit purchases, with income caps set at $95,000 for a single person with no dependants, or $150,000 for a single person with dependants or a couple. You must be a New Zealand citizen or resident, a first-time buyer, and intending to live in the property as your primary residence.

Deposit requirements at a glance

| Deposit level | Loan type | Key notes |

|---|---|---|

| 5% | Kāinga Ora First Home Loan | Income and property caps apply |

| 10% | Select bank low-deposit loans | Higher interest rate likely |

| 20% | Standard bank loans | Most competitive rates |

| 20%+ | Premium lending | Best rates and flexibility |

It’s also worth knowing a few key terms before you start. Pre-approval is a conditional agreement from a lender confirming how much they’ll lend you, which strengthens your position when making offers. Lender’s mortgage insurance (LMI) is a premium some lenders charge when your deposit is below 20%, to protect themselves against default risk. And your primary residence simply means the home you intend to live in, not an investment property.

For a deeper look at your borrowing options, the low deposit home loan guide is a helpful next step.

Maximising KiwiSaver for your home deposit

With the basics covered, your next move is making the most of KiwiSaver, often the biggest accelerator for NZ first home buyers.

KiwiSaver is a workplace savings scheme that most New Zealanders are enrolled in. What many people don’t realise is that it can also serve as a powerful engine for your home deposit. The KiwiSaver first-home withdrawal rules are clear: you must have been a member for at least three years, and you can withdraw your contributions, employer contributions, government contributions, and investment growth, but you must leave a minimum of $1,000 in your account. The funds are paid directly to your solicitor for the purchase of your first home in New Zealand, which must be your primary residence.

How to apply for your KiwiSaver withdrawal: step by step

- Confirm you meet the three-year membership requirement with your KiwiSaver provider.

- Request an application form from your provider (most have these online).

- Complete the form with your solicitor’s trust account details ready.

- Attach required documentation: proof of identity, your sale and purchase agreement, and confirmation from Kāinga Ora if applicable.

- Submit the application at least two to three weeks before settlement.

- Your provider processes the withdrawal and sends funds directly to your solicitor.

- Funds are applied toward your deposit on settlement day.

There’s an important update for 2026 that many buyers aren’t aware of yet. Targeted KiwiSaver changes for service tenancies now allow people such as farm workers in service tenancies, or those purchasing a first farm through an entity, to access their KiwiSaver withdrawal without needing to immediately occupy the property. This is a significant shift that opens the door for a broader group of New Zealanders.

For managing KiwiSaver for home buyers, timing really is everything. Apply early and communicate your settlement date clearly to your provider. Delays in processing can cause stress close to settlement.

Pro Tip: If you’re under 40 and contributing at least 3% of your income, maximising your contributions now could meaningfully increase what you can withdraw in two or three years. Even a small contribution increase today can translate to thousands more in your deposit fund.

One thing to weigh up honestly: withdrawing your KiwiSaver balance does reduce your retirement nest egg. This is a real trade-off. However, for many first home buyers, getting into property sooner creates long-term wealth through capital gains and equity building, which can offset that short-term reduction. For more guidance, explore tips for using KiwiSaver and consider your full financial picture before deciding.

Smart strategies to boost your deposit savings

KiwiSaver isn’t the only option. Let’s look at everyday habits and strategies that keep your savings growing.

The most powerful saving tool you have is a clear budget. The Sorted.org.nz Budget Planner and smart saving tips are an excellent free resource that helps you map your income against expenses and identify where money is slipping away. Once you can see your cash flow clearly, you can make deliberate changes.

Key strategies to grow your deposit faster:

- Automate your savings. Set up an automatic transfer to a dedicated savings account on payday. Treating savings like a bill means you spend what’s left, not save what’s left.

- Use a high-interest savings account. Not all savings accounts are equal. Look for accounts with competitive interest rates and minimal fees. Even a 1% difference compounds meaningfully over two or three years.

- Cut buy-now-pay-later (BNPL) services. Afterpay, Laybuy, and similar tools feel harmless but create spending patterns that lenders look at negatively. They also drain cash you could be saving.

- Consider a side hustle. Freelancing, weekend work, or selling unused items online can add hundreds of dollars a month to your savings.

- Talk to family about gifted deposits. Many lenders accept family gifts as part of your deposit, provided the gifter confirms in writing that repayment is not expected.

- Explore guarantor options. A close family member with equity in their property can sometimes act as a guarantor, allowing you to borrow more than your deposit alone would support.

Let’s put some numbers to this. Say you’re currently saving $300 per week. By adding just $100 more per week, you’d accumulate an extra $5,200 in a year and over $15,000 across three years. That kind of incremental shift, combined with your KiwiSaver balance, can dramatically change your timeline.

![]()

Pro Tip: Review your subscriptions, streaming services, and recurring expenses every three months. Most people find at least $50 to $100 a month they can redirect toward savings without noticing the lifestyle difference.

There are contrasting views on KiwiSaver withdrawal worth acknowledging. Some financial voices suggest preserving KiwiSaver for retirement and relying instead on savings alone. But for most first home buyers, using KiwiSaver remains the strongest accelerator available, especially when combined with consistent saving habits. For practical ideas tailored to Kiwis, the 6 deposit saving tips and ways to save for a deposit articles are well worth reading.

Low-deposit home loan options and their risks

Once you’ve started to grow your deposit, it’s time to check what options you actually have, even if it’s not a huge sum.

Buying with a small deposit is genuinely possible in New Zealand. The 5% deposit home loans available through the Kāinga Ora scheme give qualifying buyers a real pathway into the market. Participating banks include ANZ, ASB, BNZ, Westpac, and Kiwibank, among others. Meeting the income caps and first-home requirements is the critical step.

| Feature | Standard loan (20% deposit) | Low-deposit loan (5–10%) |

|---|---|---|

| Deposit required | 20% of purchase price | 5–10% of purchase price |

| Interest rate | Lower, more competitive | Higher (lender risk premium) |

| LMI/low equity premium | Not typically applied | May apply |

| Lender options | Wide | Limited to select banks |

| Approval timeline | Standard | Requires additional checks |

Working with a mortgage adviser before you apply gives you a clear picture of which lenders are likely to approve your application and at what rate. Entering a bank directly without this knowledge can cost you thousands in unnecessary premiums.

The Mortgage process for first home buyers follows a logical sequence: budget review, pre-approval, tidying up debt, KiwiSaver check, engaging a lawyer, making an offer with a finance clause, and finally settlement. Understanding this sequence means no stage catches you off guard.

To strengthen a low-deposit application, pay off any outstanding personal loans or credit cards before applying, demonstrate consistent savings behaviour over at least three months, and avoid applying for new credit in the months before you submit your home loan application. The low deposit mortgage guide outlines this in practical detail.

Getting your paperwork and process right

With your savings strategies in place and loan options clear, here’s how to get your application and paperwork sorted so you avoid last-minute stress.

Being organised here can genuinely be the difference between securing a property and losing it. Most lenders require the same core set of documents, and having these ready before you start viewing properties saves you weeks of scrambling.

Key steps to prepare your application:

- Gather three months of bank statements showing savings and income patterns.

- Collect recent payslips (usually the last two to three) and your latest tax return if self-employed.

- Prepare photo ID (passport or driver licence).

- Obtain written confirmation of your deposit sources, including any KiwiSaver balance and gift letters.

- Engage a property lawyer early so they’re ready to act when you find a home.

- Budget for upfront costs: legal fees typically range from $1,500 to $2,500, a builder’s report costs around $500 to $800, and a LIM (Land Information Memorandum) report can add $200 to $400.

- Always include a finance clause in your offer so you can withdraw without penalty if your loan isn’t approved.

The Mortgage process details reinforce how critical pre-approval is. It signals to sellers and agents that you’re a serious buyer, and it gives you a firm price ceiling so you don’t overcommit. Don’t underestimate the finance clause either. It’s your safety net, and removing it to compete in a hot market carries real financial risk.

What most first home buyers get wrong about deposit building

Stepping back, here’s what years of helping first home buyers has taught us about what really works and what doesn’t.

The most common mistake we see is buyers fixating on a 20% deposit as the only acceptable goal, then spending years waiting and watching property prices climb beyond their reach. This “all or nothing” thinking is costly. The market rarely waits for you to feel completely ready.

There’s a genuine opportunity cost to waiting. Suppose you could enter the market today with an 8% deposit and a property valued at $700,000. Even if you pay a slightly higher interest rate, the capital growth over three years in many Auckland and New Zealand markets has historically outpaced the extra cost of the low-equity premium. Every year you wait isn’t neutral. It’s often a step backward in real terms.

The contrasting advice on KiwiSaver withdrawal debate is worth examining honestly. Yes, pulling funds from KiwiSaver reduces your retirement balance in the short term. But owning property builds a different kind of long-term wealth, and for most first home buyers, the sooner you get in, the better your financial position over a lifetime. The fear of losing retirement savings shouldn’t paralyse you into inaction.

Small, consistent behaviours also matter far more than people expect. Saving an extra $50 a week for three years adds $7,800 to your deposit. A couple doing the same together adds $15,600. These aren’t small amounts. And when combined with KiwiSaver and smart deposit saving strategies, they become genuinely life-changing sums.

Here’s the insight that surprises most buyers we work with: being prepared, having your pre-approval in hand, your documents ready, and your KiwiSaver application submitted, is just as powerful as the size of your deposit. Sellers and agents respond to buyers who look ready. Preparedness is a competitive advantage that has nothing to do with how much money you’ve saved.

How Mortgage Managers can help you on your first home journey

Ready to put these tips into action? Here’s where Mortgage Managers can make your next move easier.

Navigating deposit requirements, KiwiSaver withdrawals, and low-deposit loan options on your own takes time and carries risk. At Mortgage Managers, our advisers act as your financial GPS, helping you find the right path through a complex landscape. We compare lenders across the market, help you understand what you genuinely qualify for, and guide you through every document and deadline without the stress.

Whether you’re ready to apply for a mortgage today or simply want to understand your options, our team is here to help. Based in Hobsonville and servicing Auckland and beyond, our expert mortgage advisers bring real local knowledge to every conversation. Take the first step and speak with a mortgage broker who genuinely understands your goals. You’ve done the reading. Now let’s get moving.

Frequently asked questions

Can I use my KiwiSaver for a first home deposit before three years?

No, you must be a member for at least three years before making a withdrawal for a first home deposit, as confirmed by the KiwiSaver first-home withdrawal rules.

Is it possible to buy a house in New Zealand with only a 5% deposit?

Yes, qualifying borrowers can access Kāinga Ora First Home Loans with just a 5% deposit, provided they meet income and residency criteria outlined in the Kāinga Ora First Home Loan eligibility requirements.

Will using my KiwiSaver for a deposit affect my retirement savings?

Yes, withdrawing KiwiSaver funds reduces your retirement balance, but as the contrasting advice on KiwiSaver withdrawal shows, getting into property sooner often creates long-term financial benefits that offset this.

Can gifts from family be used as part of my deposit for a mortgage?

Yes, most lenders accept gifted funds as part of your deposit, but the Kāinga Ora First Home Loan enables 5% deposit purchases rules require written confirmation from the giver that the money is a gift, not a loan.

How long does it take for KiwiSaver withdrawal funds to be available when buying a home?

Most providers process KiwiSaver first-home withdrawal rules applications within 8 to 15 business days, so apply well ahead of your settlement date.

Recommended

- How Can You Afford To Buy Your First Home? | Mortgage Managers

- First Home Grant explained: your guide to low deposit loans

- 7 Ways to Boost Home Loan Approval for First Buyers

- Getting A Home Loan With A 5% Deposit

- Explore Colorado Home Loan Types for First-Time Buyers

- Scott Smith: Demystifying Home Loans – 16W Media Group