TL;DR:

- Choosing the right mortgage repayment structure depends on personal financial habits and goals.

- In 2025, short fixed rates and split loans are popular due to evolving interest rates.

- Advanced strategies like overpaying and disciplined cashflow management can optimize mortgage costs.

New Zealand mortgage rates have dropped sharply in 2025, yet many first home buyers and existing homeowners feel more confused than ever about which repayment option actually suits them. Fixed, floating, split, revolving credit — the choices can feel overwhelming, especially when the stakes are as high as your family home. The good news is that with the right framework, choosing a repayment structure does not have to be a guessing game. This guide cuts through the noise, walking you through every major repayment type, how 2025’s rate environment shapes your decision, and the advanced strategies that can save you thousands over the life of your loan.

Table of Contents

- Mortgage repayment types explained

- Choosing the right repayment structure in 2025

- Rate strategy for 2025: fixed, floating and split loans

- Advanced strategies: overpayments, refinancing and cashflow management

- A fresh take: What most guides get wrong on repayment options in NZ

- Next steps: Get personalised advice on your repayment options

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your repayment options | Table, interest-only, revolving, offset and split loans each suit different needs for Kiwis in 2025. |

| Matching loan type to your goals | First home buyers often combine fixed and floating rates, while homeowners leverage overpayments and cashflow flexibility. |

| Take advantage of lower rates | With 2025 rates at historic lows, overpaying principal and avoiding repayment holidays can reduce overall costs. |

| Seek tailored expert advice | Mortgage advisers can help you navigate deposit requirements and choose strategies aligned with your financial situation. |

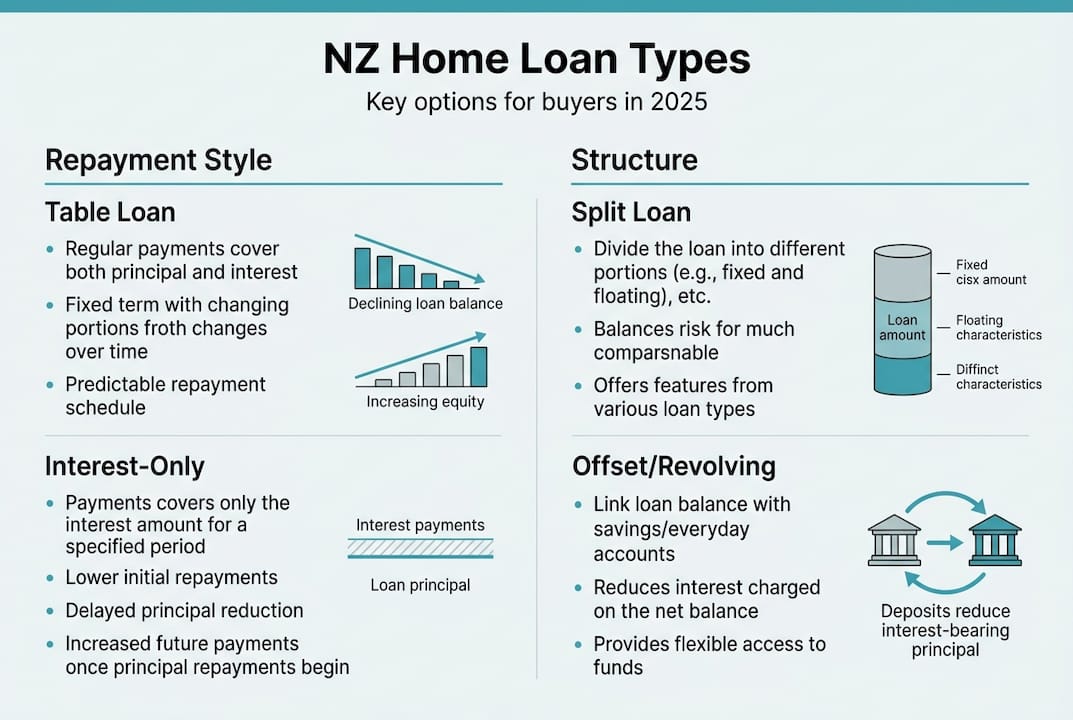

Mortgage repayment types explained

Understanding your repayment options is the foundation of smart mortgage planning. New Zealand lenders offer a wider range of structures than many buyers realise, and each one suits a different financial situation. According to a comprehensive NZ repayment guide, the main repayment types in NZ include table loans, interest-only, revolving credit, offset, reducing balance, and split loans. Knowing the difference between these structures is your first step toward making a confident decision.

Table loans (principal and interest) are the most common choice for owner-occupiers. Each repayment covers both the interest charged and a portion of the principal you borrowed, so your equity grows steadily over time. Early repayments are weighted heavily toward interest, but as your balance reduces, more of each payment chips away at the principal itself.

Interest-only loans keep your monthly repayments lower because you are not reducing the principal at all. This structure is most common among property investors who want to maximise cashflow, but it does mean your loan balance stays the same until you switch to principal and interest. It is rarely the best long-term choice for owner-occupiers.

Revolving credit and offset mortgages work like a large overdraft facility linked to your home loan. Your income and savings sit in the account, reducing the balance on which interest is calculated daily. These products can be a genuine game-changer for disciplined savers, but they require real financial self-control. You can explore how these work in more detail through this NZ mortgage repayment guide.

Split loans divide your mortgage into two or more portions, typically one fixed and one floating. This is especially popular with first home buyers who want the security of a fixed rate alongside some flexibility.

| Repayment type | Best suited for | Key benefit | Key risk |

|---|---|---|---|

| Table loan | Owner-occupiers | Steady equity build | Higher early repayments |

| Interest-only | Investors | Lower short-term payments | No principal reduction |

| Revolving credit | Disciplined savers | Minimise interest daily | Requires strict cashflow |

| Offset | Savers with surplus funds | Reduces interest charged | Complex to manage |

| Split loan | First buyers, homeowners | Stability plus flexibility | Requires active management |

Key things to keep in mind when comparing types:

- Table loans build equity fastest for owner-occupiers

- Interest-only suits investors, not long-term homeowners

- Revolving credit and offset reward financial discipline

- Split loans balance certainty with adaptability

- Understanding calculating mortgage repayments helps you compare true costs across structures

Choosing the right repayment structure in 2025

Now that the types are clear, it is crucial to match your personal circumstances to the right repayment plan. Your deposit size, income stability, and financial goals all play a role in which structure will serve you best in 2025.

For first home buyers, the Kāinga Ora First Home Loan is a strong starting point. This government-backed scheme allows eligible buyers to purchase with just a 5% deposit, provided income caps and KiwiSaver criteria are met. According to eligibility details, income caps apply at $95,000 for singles and $150,000 for households, making it accessible to a wide range of buyers.

Once you have your deposit sorted, the next question is structure. Research shows that first home buyers favour split fixed and floating loans for the combination of stability and flexibility they offer, with 70 to 80% typically fixed. This approach locks in a predictable repayment on the bulk of your loan while keeping a smaller floating portion you can overpay or redraw as needed.

Pro Tip: If you are a first home buyer with a tight budget, fixing 70 to 80% of your loan protects you from rate rises while keeping a floating portion open for lump-sum repayments when you have extra cash.

Here is a practical guide to matching your situation to the right structure:

- Small deposit (5 to 10%): A table loan with a split fixed and floating structure gives you stability and the ability to manage cashflow carefully.

- Stable income, larger deposit: Consider a revolving credit or offset mortgage to minimise daily interest and build equity faster.

- Variable income (self-employed): A floating or split loan offers flexibility to make larger repayments during good months without penalty.

- Investor: Interest-only may preserve cashflow, but always have a plan to switch to principal and interest before the interest-only period ends.

You can also learn more about the full home loan process NZ to understand how repayment choices fit into the broader picture of buying your first home.

| Buyer profile | Recommended structure | Reason |

|---|---|---|

| First buyer, 5% deposit | Split fixed/floating table loan | Stability and flexibility |

| Homeowner, strong savings | Revolving credit | Minimise daily interest |

| Investor | Interest-only | Preserve cashflow |

| Self-employed | Floating or split | Repayment flexibility |

Rate strategy for 2025: fixed, floating and split loans

You have chosen your structure — now here is how 2025’s rate environment shapes your loan repayment choices. The Reserve Bank of New Zealand has moved decisively, and the numbers are significant for anyone with a mortgage.

The OCR dropped to 2.5% in 2025, bringing fixed one-year rates to around 4.49%, two-year rates to approximately 4.65%, and three-year rates to about 4.85%. Floating rates remain higher, sitting in the 5.8 to 6% range. This gap between fixed and floating is a key factor in your decision-making right now.

Key considerations for your rate strategy:

- Short-term fixed rates (one to two years) are currently the most competitive and most popular among Kiwi borrowers

- Floating rates offer maximum flexibility but cost more in interest at present

- Long-term fixed rates (three years or more) provide certainty but may not capture future rate drops if the OCR continues to fall

- Split loans let you hedge your bets, locking in today’s low short-term rates while keeping some flexibility

Interestingly, data shows that only 10% of new loans were fixed for more than one year in early 2025, reflecting strong borrower preference for short fixes. However, if rates stabilise or begin to rise, longer-term fixes could become attractive again.

Pro Tip: Rather than chasing the absolute lowest rate, think about when your fixed term expires. Staggering your fixed periods means you are not rolling the entire loan over at once, reducing your exposure to rate movements at any single point in time.

If you want to reduce your monthly outgoings, there are practical ways to lower your repayments without simply extending your loan term. Combining a smart rate strategy with revolving credit strategies can also help you reduce the interest you pay over time. For a broader view, explore these repayment strategies NZ homeowners are using right now.

Advanced strategies: overpayments, refinancing and cashflow management

With your rate and repayment choices made, advanced strategies can further optimise your home loan management. The 2025 rate environment creates real opportunities for homeowners who are willing to be proactive.

One of the most powerful moves available right now is using rate drops to overpay your principal. Overpaying your principal while rates are lower means a greater share of each repayment reduces your actual debt, compressing your loan term and saving significant interest over time. Even small additional repayments made consistently can shave years off your mortgage.

For those using revolving credit or offset mortgages, disciplined cashflow management is essential. Parking your salary directly into a revolving credit account and only withdrawing what you need for living expenses can dramatically reduce the daily interest charged. The expert revolving credit insights from our advisers explain exactly how to make this work in practice.

Repayment holidays can feel like a lifeline during tough times, but they come at a real cost. Interest continues to compound on your outstanding balance during the holiday period, meaning you pay more in total over the life of the loan. Use them only when genuinely necessary.

Refinancing is another tool worth considering, particularly if your current lender’s rates are no longer competitive. However, be aware that extending your loan term lowers your repayments in the short term but increases total interest paid. For owner-occupiers, lenders typically require a loan-to-value ratio (LVR) of at least 80%, meaning your deposit or equity must be 20% or more for standard lending. High LVR loans above 80% are subject to Reserve Bank restrictions.

Useful actions to consider:

- Make regular overpayments, even small ones, to reduce principal faster

- Use a loan EMI calculator to model the impact of extra repayments

- Review your loan structure annually, especially when a fixed term is about to expire

- Consider refinancing if a better rate is available, but factor in any break fees or legal costs

- Explore mortgage repayment strategies tailored to the New Zealand market

A fresh take: What most guides get wrong on repayment options in NZ

Most mortgage guides focus almost entirely on rates. Fixed versus floating, which bank has the lowest number, how much you can save by switching. And while rates matter, they are only one piece of the puzzle. In our experience working with Auckland homeowners and first home buyers across New Zealand, the biggest factor in long-term mortgage success is not the rate you lock in — it is how well your repayment structure fits your actual financial behaviour.

A revolving credit mortgage at a slightly higher rate can outperform a fixed loan at a lower rate if the borrower consistently parks their income in the account and exercises real spending discipline. Conversely, a floating loan can become a financial trap for someone who lacks the structure to make regular repayments without a fixed schedule nudging them along.

The uncomfortable truth is that chasing the lowest rate without understanding your own cashflow habits is a recipe for disappointment. The smart strategies for homeowners that actually work are the ones built around your life, not just the market. Before you decide on a structure, ask yourself honestly: am I a disciplined saver, or do I need the structure of a fixed repayment to stay on track? Your honest answer to that question is worth more than any rate comparison table.

Next steps: Get personalised advice on your repayment options

Navigating 2025’s mortgage landscape is genuinely complex, and the right repayment structure for your neighbour may not be right for you. That is where personalised advice makes all the difference.

At Mortgage Managers, we work with first home buyers and existing homeowners across Auckland, the North Shore, West Auckland, and remotely throughout New Zealand to find repayment structures that fit real lives. Whether you are just starting out with managing your mortgage in 2025 or looking to refinance and restructure, our mortgage adviser services are here to guide you. Ready to take the next step? Apply for a mortgage in Auckland and let us help you find the right path forward.

Frequently asked questions

What is the most popular mortgage repayment option for first home buyers in New Zealand in 2025?

Split loans combining fixed and floating rates are the most popular choice, with around 70 to 80% typically fixed for stability and a smaller floating portion for flexibility.

Are New Zealand mortgage interest rates expected to stay low in 2025?

Rates dropped sharply in 2025, with the OCR sitting at 2.5% and one-year fixed rates around 4.49%, though future movements will depend on economic conditions.

How do repayment holidays affect your total interest paid?

Repayment holidays increase total interest due to compounding on your outstanding balance, so they should only be used when genuinely necessary and with a clear plan to resume repayments.

Can first home buyers get a mortgage with only a 5% deposit?

Yes, the Kāinga Ora First Home Loan allows eligible buyers to purchase with a 5% deposit, subject to income caps and other criteria including KiwiSaver contributions.

What are the benefits of offset or revolving credit mortgages?

Offset and revolving credit mortgages can significantly reduce the interest you pay by offsetting your savings against your loan balance daily, but they require consistent financial discipline to deliver those benefits.