Many homeowners think mortgage refinancing is only for people in financial trouble, but that’s a myth. In reality, thousands of Kiwis refinance each year to reduce monthly repayments, access home equity for renovations or investments, or simply secure better interest rates. Whether you’re looking to ease your budget or fund your next property purchase, understanding how refinancing works puts you in control. This guide breaks down mortgage refinancing in clear, practical terms so you can decide if it’s the right move for your financial goals in 2026.

Table of Contents

- What Mortgage Refinancing Means And How It Works

- Benefits And Risks Of Mortgage Refinancing In New Zealand

- How To Evaluate If Mortgage Refinancing Is Right For You

- Common Refinancing Options And How They Compare

- How Mortgage Managers Can Simplify Your Refinancing Journey

Key takeaways

| Point | Details |

|---|---|

| Refinancing replaces your current mortgage | You take out a new loan with better terms, often at a lower interest rate or different structure. |

| It can reduce repayments or free equity | Lower rates cut monthly costs, while equity release provides cash for investments or renovations. |

| Costs and penalties matter | Early repayment fees, application charges, and valuation costs can reduce your overall savings. |

| Timing and market conditions are crucial | Refinancing works best when rates drop or your financial situation improves significantly. |

| Expert advice maximises benefits | Mortgage advisers help you navigate options, compare lenders, and avoid costly mistakes. |

What mortgage refinancing means and how it works

Mortgage refinancing means replacing an existing loan with a new one to get better terms. Instead of continuing with your current mortgage, you apply for a fresh loan that pays off the old one. The new mortgage typically offers advantages like a lower interest rate, different loan duration, or access to your home’s equity. For New Zealand homeowners, refinancing has become a strategic tool to manage finances more effectively, especially as interest rates fluctuate and property values shift.

The refinancing process involves several steps. You start by researching lenders and comparing their offerings, then submit an application with your chosen provider. The lender assesses your financial situation, including income, credit history, and property value. Once approved, the new loan pays out your existing mortgage, and you begin making repayments under the new terms. This might mean switching from a fixed rate to a floating rate, extending or shortening your loan term, or moving to a different lender entirely.

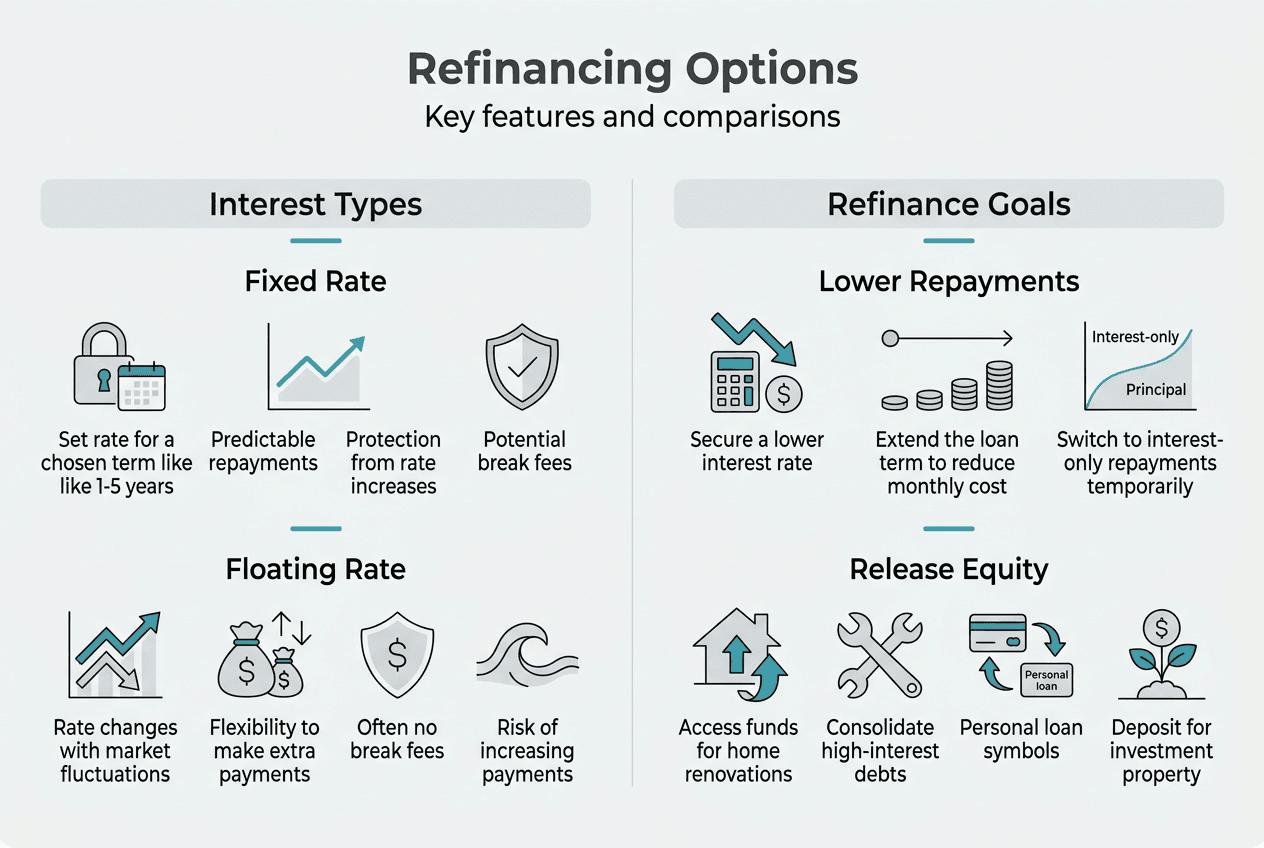

Homeowners typically consider refinancing for specific financial goals. Some want to reduce monthly repayments by securing a lower interest rate, which can save thousands over the loan’s life. Others aim to access equity built up in their property, using that cash for home improvements, investment properties, or consolidating high interest debt. Understanding common reasons for refinancing your mortgage helps you identify whether your situation aligns with typical refinancing scenarios.

The mechanics differ slightly depending on whether you choose fixed or floating rates. Fixed rate mortgages lock in your interest rate for a set period, providing payment certainty but potentially incurring break fees if you refinance early. Floating rates move with market conditions, offering flexibility but less predictability. Your choice depends on your risk tolerance, financial stability, and market outlook for 2026.

Additional costs can include application fees, legal expenses, valuation charges, and early repayment penalties from your current lender. These expenses vary significantly between lenders, so calculating the total cost is essential before committing. A refinancing step by step guide walks you through each stage, ensuring you don’t overlook critical details that could affect your savings.

Pro Tip: Before starting the refinancing process, gather recent payslips, bank statements, and your current mortgage documents. Having these ready speeds up your application and helps advisers provide accurate comparisons.

Key considerations when refinancing include:

- Your current interest rate compared to available market rates

- Remaining loan term and how refinancing affects your payoff timeline

- Equity position in your property and how much you can access

- Your credit score and how it influences approval and rate offers

- Financial goals such as reducing repayments versus accessing cash

Benefits and risks of mortgage refinancing in New Zealand

Refinancing can save homeowners thousands by lowering interest rates or reducing loan duration. When you secure a rate even one percentage point lower, the cumulative savings over years add up substantially. For example, dropping from 6.5% to 5.5% on a $500,000 mortgage could save you over $50,000 across a 25 year term. These savings reduce financial stress, free up cash for other priorities, and accelerate your path to mortgage freedom.

Accessing your home’s equity opens doors to strategic investments. Many Kiwi homeowners refinance to pull out equity for purchasing rental properties, funding business ventures, or completing major renovations that increase property value. This approach leverages your existing asset to build wealth, rather than letting equity sit idle. The key is ensuring the investment generates returns that justify the increased loan amount and interest costs.

However, costs and penalties may reduce refinancing benefits if not carefully considered. Early repayment penalties can be substantial, especially if you’re breaking a fixed rate mortgage before the term ends. Some lenders charge thousands in break fees, which might outweigh the interest savings from refinancing. Application fees, legal costs, and property valuation charges add to the expense, so you need a clear picture of total costs versus total savings.

Interest rate fluctuations significantly impact refinancing value. If rates are falling, refinancing to a lower rate makes sense. But if rates are rising or stable, the savings might not justify the effort and cost. In 2026’s economic climate, monitoring Reserve Bank of New Zealand announcements and market trends helps you time your refinance for maximum benefit. Waiting a few months could mean the difference between modest savings and substantial gains.

Another risk involves extending your loan term. While refinancing to a longer term reduces monthly repayments, it increases the total interest paid over the loan’s life. You might feel immediate relief from lower payments, but you’re committing to more years of debt and higher overall costs. Balancing short term cash flow needs with long term financial efficiency requires careful thought.

Pro Tip: Use an online mortgage calculator to model different scenarios before applying. Input various interest rates, loan terms, and costs to see which option delivers the best long term value for your situation.

“Refinancing isn’t just about getting a better rate. It’s about aligning your mortgage with your current financial goals and future plans. What made sense five years ago might not serve you well today.”

Common benefits include:

- Lower monthly repayments improving cash flow

- Access to equity for investments or major purchases

- Debt consolidation by rolling high interest loans into your mortgage

- Switching from interest only to principal and interest repayments

- Opportunity to remove mortgage insurance if equity has grown

Potential drawbacks to watch for:

- Break fees and penalties eating into savings

- Extended loan terms increasing total interest paid

- Application and legal costs adding unexpected expenses

- Risk of over leveraging if accessing too much equity

- Market timing challenges if rates don’t move as expected

Understanding should i refinance my mortgage involves weighing these factors against your personal circumstances. What works brilliantly for one homeowner might not suit another, which is why personalised advice proves invaluable. Knowing four common reasons mortgage refinance helps you benchmark your situation against typical scenarios.

How to evaluate if mortgage refinancing is right for you

Careful evaluation of costs, savings, and personal goals is essential before refinancing. Start by calculating your potential savings using current market rates compared to your existing rate. Subtract all refinancing costs, including break fees, application charges, legal expenses, and valuation fees. If the net savings exceed $5,000 over two years, refinancing typically makes financial sense. Anything less might not justify the effort and disruption.

Your evaluation should follow a systematic approach:

- Calculate your current mortgage details including remaining balance, interest rate, and monthly repayment amount.

- Research current market rates from multiple lenders to identify the best available offers for your situation.

- Estimate all refinancing costs by requesting quotes from lenders and asking about hidden fees or charges.

- Project your savings over different timeframes such as two years, five years, and the full remaining loan term.

- Consider your future plans including whether you’ll stay in the property or sell within a few years.

- Assess your credit score and financial stability to ensure you’ll qualify for competitive rates.

- Consult with mortgage advisers who can access wholesale rates and identify opportunities you might miss.

Timing your refinance according to market conditions maximises benefits. If the Reserve Bank signals rate cuts ahead, waiting a few months could secure even better terms. Conversely, if rates are rising, locking in current offers prevents missing the window. Economic indicators like inflation trends, employment figures, and housing market activity provide clues about rate direction.

Your long term financial plans matter enormously. If you’re planning to sell within two years, refinancing costs might not be recouped. But if you’re staying put for five or more years, even modest rate improvements compound into significant savings. Similarly, if you’re eyeing investment opportunities, accessing equity through refinancing could accelerate your wealth building strategy.

Pro Tip: Create a simple spreadsheet comparing your current mortgage costs against refinancing scenarios. Include columns for interest rate, monthly repayment, total interest over remaining term, and all upfront costs. This visual comparison makes the best choice obvious.

The table below shows how different refinancing scenarios affect a $500,000 mortgage over 20 years:

| Scenario | Interest Rate | Monthly Repayment | Total Interest Paid | Refinancing Costs | Net Benefit |

|---|---|---|---|---|---|

| Current mortgage | 6.5% | $3,731 | $395,440 | $0 | Baseline |

| Refinance to 5.5% | 5.5% | $3,439 | $325,360 | $3,500 | $66,580 |

| Refinance to 5.0% | 5.0% | $3,299 | $291,760 | $3,500 | $100,180 |

| Refinance with equity release | 5.5% on $550,000 | $3,783 | $357,920 | $3,500 | Access $50,000 equity |

Consulting mortgage advisers provides personalised insights you can’t get from online calculators. Advisers understand lender policies, have access to exclusive rates, and can structure deals that optimise your tax position or investment strategy. They also handle paperwork, negotiate with lenders, and ensure you avoid common pitfalls that cost homeowners money.

Understanding should i refinance my mortgage becomes clearer when you work through this evaluation framework systematically. Don’t rush the decision based on a single attractive rate. Consider the full picture, including your lifestyle, career stability, and financial aspirations. Exploring common reasons for refinancing your mortgage helps you identify whether your motivations align with successful refinancing outcomes.

Common refinancing options and how they compare

Different refinancing options suit varying goals like lowering rates or releasing equity. Fixed rate refinancing locks in your interest rate for one to five years, providing payment certainty and protection against rate rises. This option suits homeowners who value budgeting predictability and expect rates to increase. You’ll know exactly what you’re paying each month, making financial planning straightforward.

Floating rate refinancing offers flexibility and potential savings if rates fall. Your interest rate adjusts with market movements, meaning you benefit immediately when rates drop without needing to refinance again. This option works well for homeowners who can handle payment fluctuations and believe rates will trend downward. You can also make extra repayments without penalty, accelerating your mortgage payoff.

Equity release refinancing lets you access your home’s value as cash while maintaining ownership. You increase your loan amount to withdraw accumulated equity, using those funds for renovations, investments, or debt consolidation. This approach makes sense when your property value has grown substantially and you have a productive use for the capital. The key is ensuring the investment generates returns exceeding your mortgage interest rate.

Refinancing with your current lender often involves lower costs since you’re already a customer. Many banks offer retention rates to keep your business, which can be competitive without the hassle of switching institutions. However, loyalty doesn’t always pay. Switching lenders frequently unlocks better rates and terms, as lenders compete aggressively for new customers. Comparing both options ensures you’re getting the best possible deal.

The table below compares typical refinancing options available to New Zealand homeowners in 2026:

| Option | Interest Rate Range | Best For | Pros | Cons |

|---|---|---|---|---|

| Fixed rate refinance | 5.0% to 6.5% | Budget conscious homeowners expecting rate rises | Payment certainty, protection from rate increases | Break fees if refinancing early, miss out if rates fall |

| Floating rate refinance | 6.0% to 7.0% | Flexible borrowers expecting rate drops | No break fees, benefit from rate decreases | Payment uncertainty, higher starting rate |

| Equity release | 5.5% to 6.5% | Investors or renovators with substantial equity | Access cash without selling, leverage property value | Increased debt, higher repayments |

| Same lender refinance | 5.2% to 6.3% | Homeowners wanting convenience | Lower costs, faster process | Potentially higher rates than switching |

| Switch lender refinance | 4.8% to 6.0% | Rate shoppers willing to change banks | Best rates, fresh start | Higher costs, more paperwork |

Each option involves trade offs between cost, flexibility, and convenience. Fixed rates sacrifice flexibility for certainty, while floating rates do the opposite. Equity release provides immediate capital but increases your debt burden. Staying with your current lender saves hassle but might cost you thousands in missed savings. Your choice depends on your risk tolerance, financial goals, and how actively you want to manage your mortgage.

Key factors when comparing options:

- Your comfort level with payment fluctuations

- How long you plan to stay in the property

- Whether you need to access equity for specific purposes

- Your ability to make extra repayments when possible

- Current market conditions and rate forecasts

Exploring mortgage refinancing options with professional guidance ensures you select the structure that aligns with your circumstances. What looks attractive on paper might not suit your lifestyle or financial personality. An adviser can walk you through real examples and help you visualise how each option plays out over time.

How mortgage managers can simplify your refinancing journey

Navigating refinancing options alone can feel overwhelming with dozens of lenders, rate structures, and terms to compare. Mortgage Managers offers personalised advice tailored to your financial goals, whether you’re reducing repayments or leveraging equity for your next investment. Our expert advisers understand the New Zealand market intimately and have access to competitive mortgage products not always available when you approach banks directly.

We help Kiwi homeowners cut through complexity by comparing multiple lenders, explaining trade offs clearly, and handling all paperwork from application to settlement. Our advisers work for you, not the banks, ensuring recommendations align with your best interests. Whether you’re in Auckland, West Auckland, the North Shore, or anywhere across New Zealand, we’re here to make refinancing straightforward and stress free. Discover how mortgage advisers for home loans can save you time and money, or talk to Auckland mortgage brokers who genuinely care about your financial success. Contact us today for a no obligation chat about your refinancing options.

What is mortgage refinancing?

How do I know if refinancing is right for me?

Review your current interest rate against market rates and calculate potential savings after accounting for all costs. If you can save at least $5,000 over two years, refinancing typically makes sense. Consider your future plans, including how long you’ll stay in the property and whether you need to access equity. Professional advice from a mortgage adviser provides a tailored assessment based on your specific financial situation and goals.

What costs should I consider when refinancing?

Early repayment penalties from your current lender can be substantial, especially if you’re breaking a fixed rate term. Application fees, legal expenses, property valuation charges, and potential mortgage insurance costs add up quickly. Some lenders also charge establishment fees or ongoing account maintenance fees. Calculate all refinancing costs and fees upfront to get an accurate picture of your net benefit. Don’t let hidden charges erode your expected savings.

Can I refinance if I have bad credit?

Refinancing with bad credit is more challenging but definitely possible with the right approach and adviser support. Some lenders specialise in working with borrowers who have credit issues, though you’ll likely face higher interest rates initially. Improving your credit score before applying, providing a larger deposit, or demonstrating stable income can strengthen your application. The advantages of refinancing bad credit mortgages include accessing better terms than your current loan and an opportunity to rebuild your financial reputation.

How long does the refinancing process take?

The refinancing timeline typically ranges from two to six weeks, depending on lender efficiency and how quickly you provide required documentation. Simple refinances with the same lender often complete faster, sometimes within two weeks. Switching lenders involves more steps, including property valuation and legal work, which extends the process. Having all documents ready, responding promptly to requests, and working with an experienced adviser can significantly speed up your refinancing journey.

Should I refinance to a longer or shorter loan term?

Extending your loan term reduces monthly repayments, providing immediate cash flow relief, but increases total interest paid over the loan’s life. Shortening your term raises monthly payments but saves thousands in interest and gets you mortgage free sooner. Your choice depends on your current financial pressure, long term wealth goals, and career stability. If you’re financially comfortable, a shorter term builds equity faster. If you need breathing room or want to invest elsewhere, a longer term might make strategic sense despite higher total costs.