If you’ve been saving hard and counting on the First Home Grant to help you across the line, there’s something important you need to know. The grant has been discontinued due to government budget priorities, and many first home buyers in New Zealand are still unaware of this change. The good news is that real, practical support still exists. Low deposit loans and KiwiSaver withdrawals are now the primary tools available to you, and understanding how they work could be the difference between waiting another five years and buying your first home this year.

Table of Contents

- What happened to the First Home Grant?

- Low deposit options: First Home Loan explained

- Who can get a First Home Loan?

- Kāinga Whenua and Māori land home buying

- Using KiwiSaver for your deposit

- Nuts and bolts: How to apply for support

- Get tailored support for your first home

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Grant discontinued | The First Home Grant no longer accepts applications in 2026. |

| 5% deposit loans | First Home Loan lets eligible buyers purchase with just a 5% deposit. |

| KiwiSaver support | KiwiSaver withdrawal provides critical funds for first home deposits after three years’ membership. |

| Eligibility matters | Check residency, income, and deposit rules to see what you qualify for. |

| Expert assistance helps | Mortgage advisers can guide you through changed support options and low deposit loans. |

What happened to the First Home Grant?

The First Home Grant was a cash contribution from the government to help eligible buyers with their deposit. It was popular, but it’s gone. The grant was scrapped due to budget constraints and a government decision to redirect funding toward social housing, with critics arguing the scheme was inefficient in addressing New Zealand’s broader housing challenges.

If you applied before the cut-off, your application may have been processed. For everyone else, the grant is simply no longer an option. That’s a hard pill to swallow, but it doesn’t mean you’re without support.

“The removal of the First Home Grant has shifted the focus to loan-based support, which is actually more flexible for many buyers.”

Here’s what government support still remains for first home buyers in 2026:

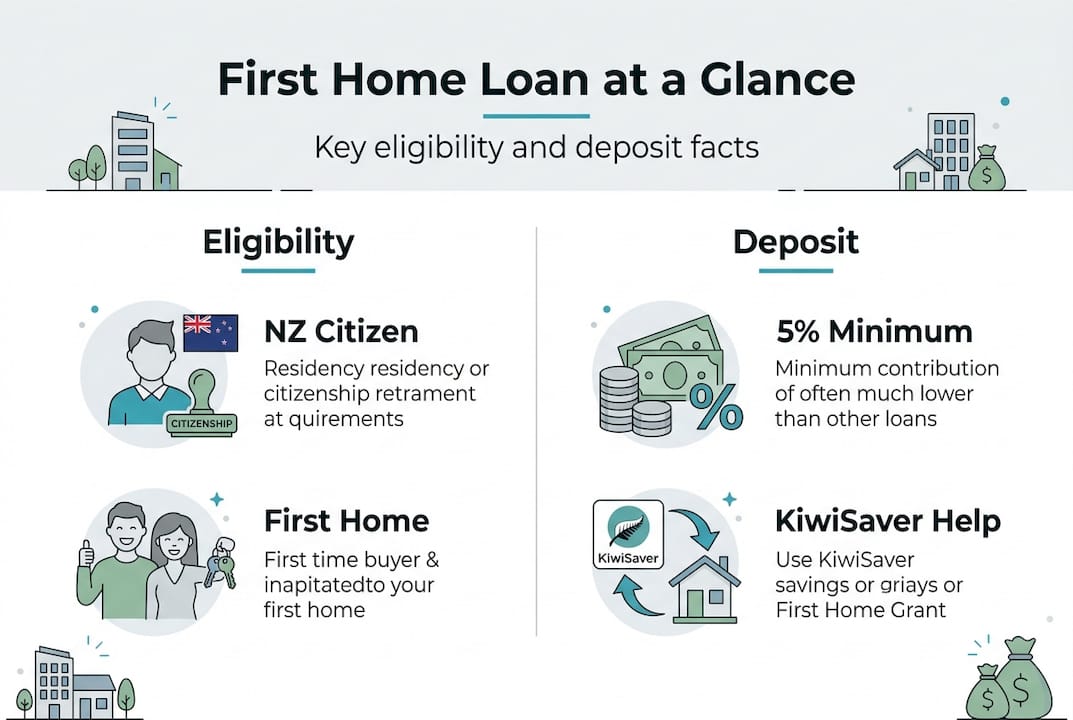

- First Home Loan backed by Kāinga Ora, allowing a 5% deposit

- KiwiSaver first home withdrawal after a minimum of three years’ membership

- Kāinga Whenua Loans for eligible Māori buyers purchasing or building on Māori land

- Welcome Home Loan pathways through participating lenders

Low deposit options: First Home Loan explained

With the grant gone, the First Home Loan is now the centrepiece of government support for first home buyers. The scheme is underwritten by Kāinga Ora through participating lenders, meaning the government essentially guarantees part of your loan so lenders feel comfortable offering you finance with a smaller deposit.

The headline figure here is significant. You only need a 5% deposit to qualify, which is far lower than the 20% most people assume is required. That changes the maths entirely for buyers who have been saving but feel like the finish line keeps moving.

Here’s how the deposit picture has shifted:

| Deposit requirement | Then (with First Home Grant) | Now (First Home Loan only) |

|---|---|---|

| Minimum deposit | 5% (grant topped up the rest) | 5% (loan covers the gap) |

| Government cash contribution | Up to $10,000 | None |

| KiwiSaver usable | Yes | Yes |

| Lender mortgage insurance | Sometimes required | May apply |

The deposit requirements in NZ are more accessible than many buyers realise, especially when you factor in KiwiSaver. Here’s how the approval process typically works:

- Check your eligibility against income and deposit thresholds

- Approach a participating low deposit lender who offers First Home Loans

- Submit your application with supporting documents (payslips, bank statements, KiwiSaver balance)

- Lender assesses your application and forwards to Kāinga Ora for underwriting approval

- Receive conditional approval and begin your property search

- Finalise the purchase and settle

Timelines vary, but most buyers move from application to conditional approval within two to four weeks when documentation is in order.

Pro Tip: Your KiwiSaver balance can form part or all of your 5% deposit. Check your 5% deposit eligibility early so you know exactly where you stand before approaching a lender.

Who can get a First Home Loan?

Knowing how the loan works is one thing. Knowing whether you qualify is another. The eligibility criteria cover residency, income, deposit, and how you intend to use the property.

| Criteria | Requirement |

|---|---|

| Residency | NZ citizen or permanent resident |

| First home status | Must not currently own property |

| Income (single) | Up to $95,000 per year (before tax) |

| Income (joint/multiple buyers) | Up to $150,000 combined |

| Minimum deposit | 5% of purchase price |

| Occupancy | Must intend to live in the home |

Here’s how the criteria play out across common buyer scenarios:

- Single buyer: Eligible if income is under $95,000 and you have a 5% deposit saved or in KiwiSaver

- Couple buying together: Combined income must sit under $150,000; both must meet residency requirements

- Buyer with dependants: Income thresholds remain the same; having children does not increase your cap

- Former property owner: If you no longer own property and meet a financial hardship test, you may still qualify as a second-chance buyer

- Mixed visa couple: One partner must be a citizen or permanent resident; the other’s visa status can complicate approval

For a full breakdown of your situation, the low deposit home loan guide is a practical starting point.

Pro Tip: If you’re self-employed, lenders will want to see two full years of tax returns and financial statements. Get these organised well before you apply to avoid delays.

Kāinga Whenua and Māori land home buying

For Māori buyers looking to purchase or build on Māori land, there’s a dedicated pathway worth knowing about. Kāinga Whenua Loans provide low deposit options specifically for housing on Māori land, with eligibility criteria that mirror the First Home Loan but are tailored to the unique legal structure of Māori land ownership.

The key differences and steps for Māori buyers include:

- Land type: The property must be on Māori freehold land, which has different legal title structures to general freehold

- Eligibility: You must be Māori and meet standard first home buyer income and deposit criteria

- Loan structure: The loan is designed to work within the constraints of Māori land ownership, where standard mortgages often can’t be registered

- Regional caps: Purchase price and income caps apply and may differ slightly from the standard First Home Loan

- Application process: Work with a lender experienced in Māori land transactions and engage your iwi or hapū early in the process

- Legal support: You’ll need a solicitor familiar with Te Ture Whenua Māori Act to navigate title and consent requirements

If this pathway applies to you, our low deposit mortgage guide for 2025 and 2026 covers the broader landscape of options available.

Using KiwiSaver for your deposit

KiwiSaver is genuinely a game-changer for first home buyers. After three years of membership, you can withdraw your contributions, your employer’s contributions, and any government contributions to use as a deposit on your first home. The key rule is that you must intend to live in the property.

Here’s how to request your KiwiSaver withdrawal:

- Confirm you’ve been a KiwiSaver member for at least three years

- Contact your KiwiSaver provider and request a first home withdrawal application form

- Complete the form and gather supporting documents, including a sale and purchase agreement or evidence of your property search

- Submit your application to your provider for processing

- Your provider transfers the funds directly to your solicitor’s trust account at settlement

Timing is everything here. Providers can take up to 10 working days to process a withdrawal, and some take longer. If you’re working to a settlement deadline, a delay in your KiwiSaver funds arriving can cause real stress.

Pro Tip: Start your KiwiSaver withdrawal paperwork as soon as your offer is accepted, not when settlement is a week away. Our KiwiSaver home deposit tips walk you through the timing in detail.

One common mistake is assuming you can withdraw everything. You must leave a minimum balance of $1,000 in your account. Plan your deposit calculations around this.

Nuts and bolts: How to apply for support

The First Home Loan scheme targets middle-income New Zealanders who face deposit barriers, and the application process is more straightforward than many expect. Here’s a consolidated checklist to bring all three programmes together:

First Home Loan:

- Confirm income and residency eligibility

- Calculate your 5% deposit (including KiwiSaver)

- Choose a participating lender and submit your application

- Provide payslips, bank statements, and ID

- Await Kāinga Ora underwriting approval

Kāinga Whenua Loan:

- Confirm Māori land title and your eligibility

- Engage a solicitor experienced in Māori land law

- Approach a lender with Kāinga Whenua experience

- Submit application with land title documentation

- Allow additional time for title and consent processes

KiwiSaver withdrawal:

- Check your membership duration and balance

- Request withdrawal forms from your provider immediately after offer acceptance

- Submit completed forms with your sale and purchase agreement

- Confirm funds will arrive before your settlement date

- Coordinate with your solicitor to receive funds into their trust account

For a step-by-step walkthrough of the low deposit loan process, or for additional government guidance, the HUD First Home Loan support page is a reliable reference point.

Get tailored support for your first home

Navigating the post-grant landscape on your own can feel like reading a map with half the roads missing. The rules have changed, the options are layered, and the stakes are high. That’s exactly where working with experienced mortgage advisers for your first home makes a real difference.

At Mortgage Managers, we work with first home buyers across Auckland, the North Shore, West Auckland, and remotely throughout New Zealand. We know which lenders are most flexible with low deposit applications, how to structure your KiwiSaver withdrawal for maximum impact, and how to position your application for the best possible outcome. When you’re ready to take the next step, applying for your first mortgage with the right guidance behind you makes the whole process far less daunting.

Frequently asked questions

Can I still get the First Home Grant in 2026?

No. The First Home Grant has been discontinued and is no longer available for new applications. Focus your energy on the First Home Loan and KiwiSaver withdrawal instead.

What is the minimum deposit for the First Home Loan?

You need at least a 5% deposit to qualify for a First Home Loan, and this can include funds from your KiwiSaver account and gifted money from family.

Who qualifies for a First Home Loan in New Zealand?

NZ citizens or permanent residents buying their first home, who meet the income and deposit criteria and intend to live in the property, can qualify.

How does KiwiSaver help with the deposit?

After three years of membership, you can withdraw your KiwiSaver savings to use as a deposit, provided you plan to live in the home you’re buying.

Are there options for buying a home on Māori land?

Yes. Kāinga Whenua Loans are specifically designed to support eligible Māori buyers with low deposit requirements when purchasing or building on Māori freehold land.