Jumping into the property market in Auckland can feel overwhelming, especially when you are trying to work out exactly what a home deposit means for your first purchase. The deposit is not only a financial hurdle but also a legally binding commitment, forming part of the Sale and Purchase Agreement and securing your place in the buying process. This guide helps you untangle the differences between standard, low, and special deposit options so you can approach your first home search with confidence and clarity.

Table of Contents

- Meaning of Deposit in Home Buying Process

- Standard, Low and Special Deposit Types Explained

- Minimum Amounts, Sources and KiwiSaver Use

- How Deposit Size Affects Loan Approval and Rate

- Risks, Costs and Common Deposit Mistakes

- Alternatives and Tips for Low Deposit Buyers

Key Takeaways

| Point | Details |

|---|---|

| Understanding Deposits | A deposit is a commitment to the seller, reflecting your intent and financial capability to purchase a property. It is critical to know the deposit amount required based on your financial situation and lender’s requirements. |

| Types of Deposits | Familiarise yourself with the differences between standard, low, and special deposits, as each affects your borrowing experience, interest rates, and eligibility. |

| Deposit Sources | Lenders evaluate the source of your deposit, with personal savings being the most favourable, while family gifts and KiwiSaver withdrawals should be documented properly. |

| Planning and Timing | Engage with a mortgage adviser six to twelve months before buying to optimise your financial situation and explore potential lending options effectively. |

Meaning of Deposit in Home Buying Process

When you decide to buy a property in Auckland, the deposit is your formal commitment to the seller that you’re serious about the purchase. Think of it as putting your money where your mouth is. The deposit is a sum of money you pay as part of the Sale and Purchase Agreement, which is the legally binding contract between you and the seller. This amount becomes part of your total purchase price, and the deposit secures the property whilst the rest of the transaction progresses towards settlement.

The deposit serves multiple purposes in the home buying process. First, it demonstrates to the seller that you have genuine financial capacity and intent to complete the purchase. Secondly, it provides legal protection for both parties by outlining the terms, conditions, and settlement requirements in the agreement. Under New Zealand’s property transaction framework, the deposit is held in trust and represents a contractual obligation that legally binds you as the buyer. If you fail to complete the purchase without valid reason, you stand to lose this deposit. Conversely, if the seller fails to settle, they must return your deposit plus compensation in many cases.

In Auckland’s competitive property market, understanding your deposit requirement is crucial before you start house hunting. The deposit amount you’ll need typically depends on several factors including your loan to value ratio (LVR), your financial position, and the lender’s requirements. Most first home buyers in Auckland will need to have somewhere between 10% and 20% of the purchase price ready as a deposit, though some lenders offer low deposit options with mortgage insurance. The specific details of how much you’ll pay, when you’ll pay it, and what conditions apply all get documented in your Sale and Purchase Agreement. This is why having professional guidance when entering into these agreements can make a significant difference to your financial outcome.

Pro tip: Before you start your property search, speak with a mortgage adviser to determine exactly how much deposit you can realistically save and what loan options are available to you, as this will directly influence which properties you can actually afford to pursue.

Standard, Low and Special Deposit Types Explained

Not all deposits are created equal. Auckland’s property market offers several deposit options depending on your circumstances, and understanding the differences between them can unlock opportunities you might not have realised were available. The type of deposit you choose affects your loan eligibility, the interest rates you’ll pay, any additional costs you’ll incur, and how quickly you can move into your new home.

A standard deposit is traditionally around 20% of the purchase price. If you’re buying a $600,000 property in Auckland, that’s $120,000 sitting in your bank account before you exchange contracts. The advantage here is straightforward: lenders love seeing substantial deposits because it reduces their risk. You’ll typically access better interest rates, avoid Lender’s Mortgage Insurance (LMI), and have more negotiating power with sellers. However, saving 20% takes time, and many first home buyers simply can’t accumulate that much capital whilst paying rent and living expenses.

Then there are low deposits, which range from as little as 5% up to 10%. This is where things get interesting for Auckland first home buyers. Government-backed schemes like Kāinga Ora’s First Home Loan allow you to purchase with significantly less capital upfront, making homeownership achievable sooner rather than later. The trade-off is that you’ll typically pay Lender’s Mortgage Insurance, which protects the lender if you default. Yes, this adds cost, but it also means you’re not trapped renting indefinitely whilst you scrape together an extra $40,000 or $50,000. Many first home buyers find this is a smart financial move because you’re building equity in your own property rather than paying your landlord’s mortgage.

Special deposits apply to unique situations. New builds sometimes come with developer incentives or deposit assistance schemes. Properties purchased through specific assistance programmes may have tailored deposit requirements. These options exist because different circumstances call for different solutions. Your situation might qualify for something that standard lending criteria wouldn’t normally accommodate.

Here’s what matters most: understanding low deposit home loan options is crucial because the deposit type you select shapes your entire borrowing experience. Higher deposits mean lower interest rates and fewer fees. Lower deposits mean faster entry to the market and more monthly cash flow for other priorities. Neither is universally “better” – it depends on your specific goals, timeline, and financial position.

Pro tip: Don’t automatically assume you need 20% saved before approaching a lender; speak with a mortgage adviser about low deposit options available to you, as you might be able to purchase sooner whilst still making a financially sound decision.

Here’s a summary of the main deposit types and their unique features:

| Deposit Type | Typical Amount | Eligibility | Pros and Cons |

|---|---|---|---|

| Standard | 20% of price | Most buyers | Lower rates, no mortgage insurance, but slow to save |

| Low | 5–10% of price | First home buyers, those with government support | Faster entry, possible insurance cost, higher interest rates |

| Special | Varies, often less than standard | Buyers using developer or assistance schemes | Custom terms, may be more flexible, but less widely available |

Minimum Amounts, Sources and KiwiSaver Use

The minimum deposit you need varies significantly depending on which lending option you choose and your personal circumstances. At the lowest end, some first home buyers in Auckland can secure a mortgage with just 5% of the purchase price as a deposit. That’s only $30,000 on a $600,000 property. However, most lenders typically want to see between 10% and 20%. The key is understanding what minimum amounts different lenders will accept and then exploring where you can actually source that money.

Deposit sources matter as much as the amount itself. Lenders scrutinise where your deposit comes from because they want to ensure you have genuine savings discipline and financial stability. Your own savings remain the strongest source, showing you can manage money responsibly. Family gifts are commonly accepted, though most lenders require a statutory declaration confirming the money is a gift, not a loan. Some buyers inherit money or receive settlements that unlock deposit funds. Employer bonuses, tax refunds, and insurance payouts can all contribute. What lenders generally won’t accept are borrowed funds masquerading as your own money, as this increases your actual debt levels beyond what appears on paper.

Then there’s KiwiSaver, which has become a genuine game changer for Auckland first home buyers. If you’re a first home buyer who’s been contributing to KiwiSaver, you can withdraw your entire balance to put towards your deposit. This includes both your contributions and your employer’s contributions, plus any investment growth. For many people in their late twenties and thirties who’ve been saving through KiwiSaver for five to ten years, this can represent $40,000, $60,000, or even more sitting ready to deploy. Managing KiwiSaver for your first home deposit requires careful planning because once you withdraw it, that money is gone from your retirement savings. However, using it strategically to enter the property market earlier can actually strengthen your long-term financial position because you start building home equity sooner.

The strategy here is combining multiple sources intelligently. Perhaps you have $30,000 in personal savings, your parents gift you $20,000, and you withdraw $25,000 from KiwiSaver. Suddenly you have a $75,000 deposit (12.5% on a $600,000 purchase) without having to wait another three years to save. KiwiSaver first home withdrawals come with specific rules about timing and eligibility that are worth understanding before you approach a lender. The tax implications are minimal, but the opportunity cost of removing retirement savings does matter, so it’s worth having a conversation with a mortgage adviser about whether this timing makes sense for your situation.

Pro tip: Start documenting all your deposit sources now, including gathering bank statements showing consistent savings patterns and written confirmation from anyone gifting money, as lenders will request this paperwork during the application process and having it ready accelerates your approval timeline.

This table highlights key sources of a home deposit and how lenders assess them:

| Deposit Source | Lender Assessment Focus | Common Requirements |

|---|---|---|

| Personal Savings | Proven saving discipline | Bank statements, consistent patterns |

| Family Gifts | Not a loan, genuine gift | Statutory declaration, gift letter |

| KiwiSaver Withdrawal | Meets legal and fund rules | KiwiSaver application, eligibility proof |

| Inheritance/Settlement | Verifiable, one-off capital | Legal documents, clear ownership trail |

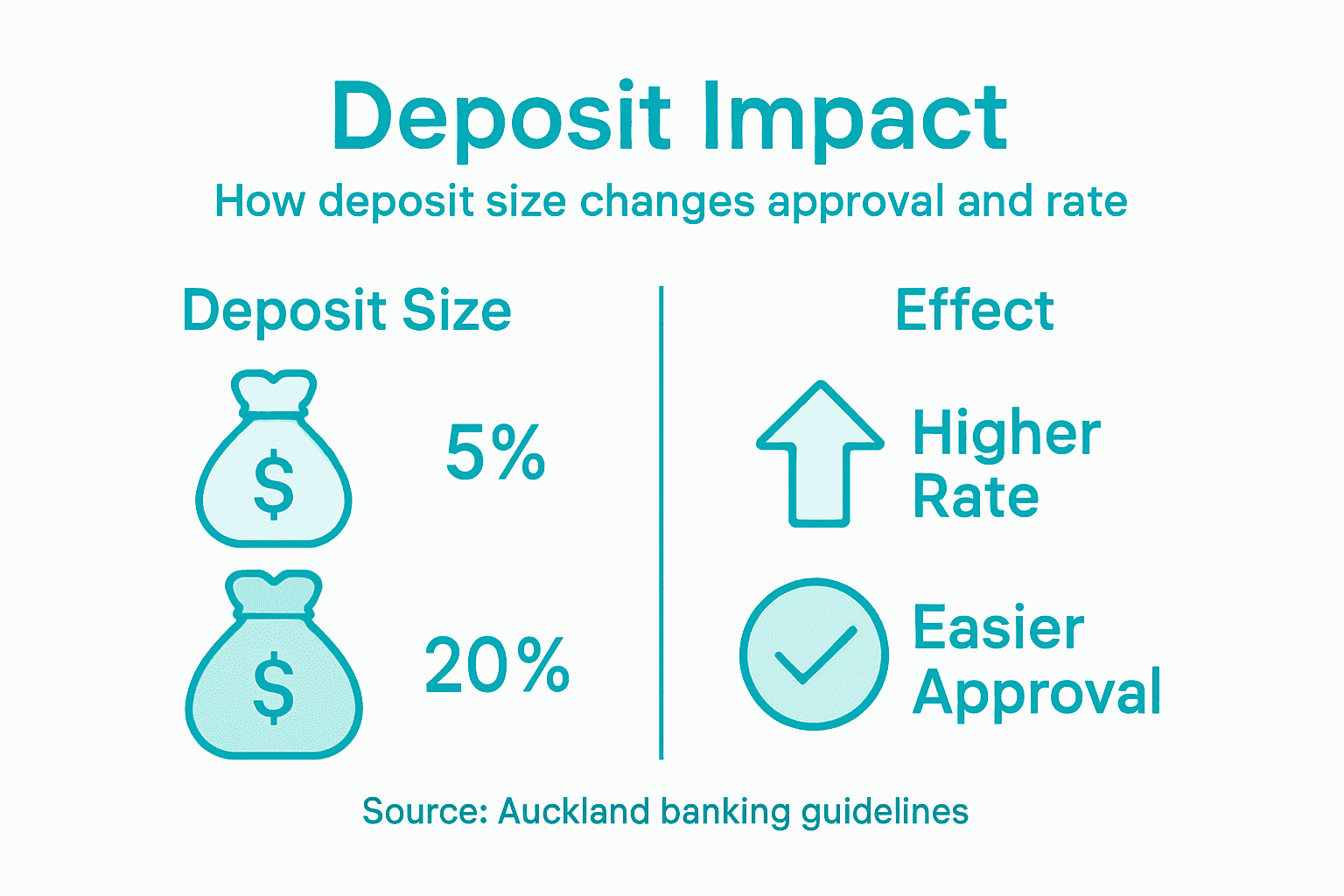

How Deposit Size Affects Loan Approval and Rate

Your deposit size is one of the most influential factors in whether a lender approves your mortgage application and what interest rate you’ll pay. Lenders view larger deposits as a sign of financial responsibility and reduced risk. When you’re putting down 20% of the purchase price, you’re demonstrating that you can save substantial amounts and that you have genuine skin in the game. The lender’s exposure drops significantly because even if property values fall, they have a comfortable buffer before their security is threatened. Conversely, a smaller deposit means the lender is exposed to greater risk, and they adjust their pricing accordingly.

Loan approval becomes easier with a larger deposit. With 20%, most mainstream lenders will approve your application relatively straightforwardly, assuming your income and credit history are sound. Drop to 10%, and you’ll face more scrutiny. Go down to 5%, and getting a home loan with a 5% deposit requires finding lenders willing to accept higher risk, which often means paying Lender’s Mortgage Insurance. Some lenders won’t even consider applications below 10% without mortgage insurance in place. This isn’t because they’re being difficult; it’s a regulatory and risk management requirement. Your deposit size directly determines which lenders will consider your application and under what conditions.

Interest rates shift noticeably based on your deposit. Here’s what typically happens across Auckland’s lending market: a buyer with a 20% deposit might secure a rate of 5.49% on a five-year fixed mortgage, whilst someone with 10% might pay 5.65%, and a 5% deposit could attract 5.85% or higher depending on the lender and whether mortgage insurance is involved. That 0.36% difference might sound small, but on a $480,000 loan (20% deposit on a $600,000 property), it’s approximately $1,728 extra per year in interest costs. Over a 25-year mortgage, that compounds into tens of thousands of dollars. The relationship between deposit size and rate is direct and significant.

Mortgage insurance adds another layer of cost when your deposit falls below certain thresholds. If you have 10% or less, lenders typically require you to pay an insurance premium, which can range from 2% to 5% of your loan amount depending on how small your deposit is. This insurance protects the lender, not you, which feels frustrating but it’s what enables low deposit lending to exist. That insurance cost gets added to your total loan amount, increasing your monthly repayments. The mathematics can still work in your favour if entering the property market five years earlier means five extra years of building equity, but you need to understand the full cost picture before committing.

Pro tip: Use a mortgage calculator to compare the total cost of different deposit scenarios, including interest rate differences and any mortgage insurance, rather than focusing solely on the deposit amount you need to save, as this reveals the true financial impact of your timing decision.

Risks, Costs and Common Deposit Mistakes

Deposit mistakes can be expensive, legally binding, and surprisingly easy to make. Many first home buyers in Auckland focus so intently on saving the deposit amount that they overlook the contractual and financial risks embedded in the deposit process itself. The deposit isn’t just money you hand over and forget about—it’s a legally binding commitment governed by the terms in your Sale and Purchase Agreement. Understanding deposit conditions such as refundability, payment deadlines, and withdrawal consequences is absolutely critical because these details determine whether you lose your deposit if circumstances change.

One of the biggest mistakes is failing to have proper legal review of the Sale and Purchase Agreement before you commit. Buyers sometimes rush to exchange contracts without thoroughly understanding what conditions apply to their deposit. You might assume your deposit is refundable in certain circumstances only to discover later that it isn’t. Another common error is not having adequate funds ready at settlement. You’ve scraped together your deposit, secured your mortgage approval, and then suddenly faced unexpected costs like legal fees, inspections, or building reports that weren’t budgeted for. Suddenly you’re short of cash at the final hurdle. Additionally, many first home buyers underestimate the true cost of low deposits. They see the 5% or 10% figure and think “I can do this,” without factoring in Lender’s Mortgage Insurance costs, which can add $15,000 to $30,000 to your total loan amount depending on how small your deposit is.

Timing errors represent another significant risk category. Deposits must be paid by specific dates outlined in your agreement. Miss that deadline without valid reason, and you’re in breach of contract. The seller can keep your deposit and potentially pursue you for damages. Similarly, withdrawing from a purchase after deposit payment is legally complex and costly. You can’t simply change your mind because you got cold feet or saw another property you liked better. Six of the biggest mistakes homeowners make with lending often stem from not understanding their contractual obligations upfront, and deposit-related mistakes rank high on that list.

Financial risks extend beyond the deposit itself. Many first home buyers don’t account for the full cost of homeownership when planning their deposit strategy. You’ve used your KiwiSaver, depleted your savings, and borrowed from family just to get the deposit together. Then settlement arrives and you have almost nothing left for rates, insurance, maintenance, or emergencies. Your mortgage is approved for $480,000, but you’re stretched thin financially and one unexpected repair could create serious hardship. The safest approach is ensuring your deposit doesn’t drain your entire financial reserves.

Pro tip: Have a conveyancer or lawyer review your Sale and Purchase Agreement before you exchange contracts, ensuring you fully understand every deposit condition, and simultaneously build a settlement fund separate from your deposit to cover closing costs and unexpected expenses.

Alternatives and Tips for Low Deposit Buyers

If you’re a first home buyer in Auckland with limited savings, you’re not locked out of the property market. Multiple pathways exist specifically designed to help people with smaller deposits enter homeownership. Government-backed schemes like Kāinga Ora’s First Home Loan allow deposits as low as 5%, fundamentally changing what’s possible for buyers who thought they were years away from purchasing. Beyond government programmes, family assistance remains powerful. A parental gift can bridge the gap between what you’ve saved and what you need, though documentation is essential. Some families structure this as a guarantee instead, where parents guarantee part of the loan to the lender, reducing the required deposit without actually gifting money upfront.

Working with a mortgage adviser to navigate low deposit loan options is genuinely one of the smartest moves you can make as a low deposit buyer. A good adviser knows which lenders are actively lending at 5%, 7%, or 10% deposits, what conditions each lender requires, and how to position your application for the best possible outcome. They’ll explain Lender’s Mortgage Insurance in detail and help you calculate whether paying insurance now to enter the market early is worth the long-term cost. They might also identify alternative funding sources you hadn’t considered. If you own property elsewhere or have equity locked in an existing home, you might borrow against that equity for your deposit rather than depleting savings. Government grants and no-interest loans from community providers exist for qualifying buyers, though eligibility varies. Your adviser will know which programmes you might access.

Your credit score matters significantly when you have a small deposit. Lenders scrutinise low deposit applications more closely, and a strong credit history reassures them you’re trustworthy with borrowed money. Start managing your credit now by paying bills on time, reducing credit card balances, and avoiding missed payments. Reducing personal debt also strengthens your application. If you have car loans, personal loans, or credit card debt, paying these down before applying improves your serviceability ratios, which determines how much mortgage a lender will approve. You might not need to eliminate all debt, but reducing it demonstrates financial discipline.

Timing and strategy matter for low deposit buyers. Rather than rushing to purchase, spend six to twelve months optimising your financial position. Build an extra $20,000 in savings, pay off your car loan, improve your credit score, and research which lenders and government schemes suit your situation. This preparation often results in better loan terms, lower interest rates, and less stress during the approval process. Many first home buyers find that six months of focused financial planning unlocks significantly better lending options than rushing to buy unprepared.

Pro tip: Start conversations with mortgage advisers six to twelve months before you plan to buy, not when you’re ready to make an offer, as this gives you time to implement their recommendations and strengthen your application significantly.

Secure Your Auckland Home with Expert Deposit Guidance

Navigating the complexities of deposits in Auckland’s property market can feel overwhelming. Whether you are managing low deposit options, KiawiSaver withdrawals, or understanding lender requirements, having expert advice is essential. Many first home buyers face challenges like timing deposit payments, avoiding costly mistakes, and balancing financial risks. With Mortgage Managers based right here in Hobsonville, you gain access to local specialists who truly understand the unique deposit landscape impacting Auckland buyers.

Take control of your home buying journey today by partnering with advisers who can help you explore every deposit avenue, from standard and special deposits to unlocking government-backed schemes. Don’t let uncertainty delay your dream. Visit Mortgage Managers now to find out how our tailored mortgage advice supports your goals with clear strategies and faster approvals. Start your application with confidence and secure your new home sooner by consulting Mortgage Managers —your trusted Auckland mortgage advisers.

Frequently Asked Questions

What is the purpose of a deposit when buying a home?

The deposit serves as a formal commitment to the seller, demonstrating your serious intent to purchase the property and forming part of the total purchase price.

How much deposit do I need for a home in Auckland?

Typically, first home buyers in Auckland need to save between 10% and 20% of the purchase price as a deposit, though some lenders offer options with lower deposits, such as 5% with mortgage insurance.

What happens to my deposit if I can’t finalise the purchase?

If you fail to complete the purchase without a valid reason, you may lose your deposit. Conversely, if the seller fails to settle, they may be required to return your deposit plus compensation.

How does my deposit size affect my mortgage approval?

Lenders view larger deposits as a sign of financial responsibility, making approval easier and often resulting in lower interest rates. Smaller deposits can lead to higher scrutiny and potentially higher costs, including mortgage insurance.